Space Power Supply Market Size, Share & Industry Analysis, By Power Source (Solar & Nuclear Power, Battery Power/Storage), By Battery Shape (Cylindrical, Prismatic & Pouch-Type Batteries), By Battery Capacity (Low, Medium, & High Capacity), By Product Type (Solar Panel, Power Management Devices, Power converter, Energy Storage), By Application (Communication Satellites, Earth Observation Satellites, Navigation Satellites, Space Probes & Rovers, Space Stations, Launch Vehicles & Rockets), By End-User (Government & Military, Commercial Operators), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

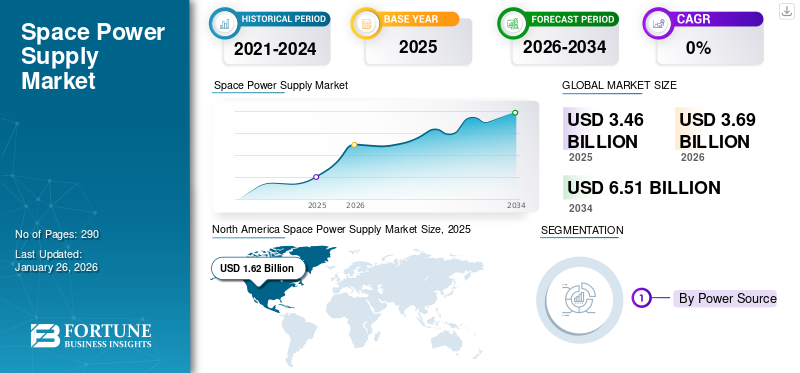

The global space power supply market size was valued at USD 3.46 billion in 2025. The market is projected to grow from USD 3.69 billion in 2026 to USD 6.51 billion by 2034, exhibiting a CAGR of 7.36% during the forecast period. North America dominated the space power supply market with a market share of 46.92% in 2025.

Space power supplies are critical components in spacecraft and satellite systems, providing reliable and efficient power distribution to support various mission requirements. The space market share is expected to grow due to increasing demand for satellite-based services, such as weather forecasting and remote sensing. The market is anticipated to witness growth due to several key factors. Firstly, the development of low-earth orbit satellites is increasing, as they are in high demand for their ability to enhance 5G terrestrial networks. Additionally, technological advancements have made satellites more affordable, compact, and smarter. The market also witnessed an increasing demand for space-based services, such as telecommunications and remote sensing, during the pandemic. Furthermore, the market is set to experience a boost due to rising demand for solar arrays for various satellite operations. Moreover, silicon carbide (SiC) and gallium nitride (GaN) are being increasingly used in space power supply systems due to their superior performance and efficiency compared to traditional silicon-based devices.

Key players in the market such as AAC Clyde Space (U.K.), Airbus S.A.S (Netherlands), AZUR SPACE Solar Power GmbH (Germany) and Teledyne Technologies are collaborating with major space agencies and space technology companies for the supply of space power supply system and components. For instance, in September 2024, Airbus received a contract from MDA Space Ltd. for the supply of solar arrays for MDA AURORATM, the software-defined satellite product line. Moreover, Airbus, Boeing, and Lockheed Martin are driving technological advancements to maintain competitiveness. a growing emphasis on sustainability and cost-effectiveness is shaping the market, where companies invest in eco-friendly power sources and energy-efficient systems.

The COVID-19 pandemic significantly affected the market as supply chain disruptions globally delayed the production and delivery of space-grade power supply components and systems. Restrictions on international travel and workforce limitations imposed to curb the spread of the virus further exacerbated these challenges. These disruptions resulted in project delays and high costs for space missions and affected the overall demand for space power supply systems.

Download Free sample to learn more about this report.

Space Power Supply Market Overview & Key Metrics

Market Size & Forecast

- 2025 Market Size: USD 3.46 billion

- 2026 Market Size: USD 3.69 billion

- 2034 Forecast Market Size: USD 6.51 billion

- CAGR: 7.36% from 2026–2034

Market Share

- North America dominated the space power supply market with a 46.92% share in 2025, driven by the presence of major space agencies (NASA, CSA) and leading manufacturers such as Northrop Grumman, Teledyne Technologies, and Airbus. Growth in this region is attributed to increased satellite launches, advancements in nuclear and solar power solutions, and rising demand for space-based communication and Earth observation services.

- By power source, the battery power/storage segment led the market due to growing use of lithium-ion technologies in satellites, while solar power systems are expected to expand rapidly due to their cost-effectiveness and renewable nature.

Key Regional Insights

- North America: Largest market, valued at USD 1.50 billion in 2024; growth driven by strong space exploration programs and commercial satellite deployments.

- Asia Pacific: Fastest-growing region, led by China, India, and Japan focusing on low-cost satellite launches and increasing LEO constellation deployments.

- Europe: Moderate growth fueled by ESA projects, sustainability focus, and investments in Americium-based RTGs.

- Middle East: Expanding market with increasing investment in space services and collaborations for satellite manufacturing.

- Rest of the World: Growth supported by emerging players in Latin America and Africa focusing on satellite connectivity and remote sensing services.

Space Power Supply Market Trends

Integration of Lithium-Ion-based Power is a Key Market Trend

The integration of lithium-ion-based power is a key market trend, driven by high energy density, long cycle life, and low weight of lithium-ion batteries. The space power supply market growth is expected to be significant in the coming years, fueled by policy support and incentives and the integration of renewable energy sources. Lithium-ion batteries are relatively small and compact, which is a significant reason for their adoption into spacecraft designs. Numerous companies are manufacturing lithium ion batteries for space applications. For instance, in October 2024, EnerSys announced the successful launch of its ABSL™ lithium-ion space battery on NASA's Europa Clipper spacecraft. The launch occurred on October 14, 2024, using a SpaceX Falcon Heavy rocket from Kennedy Space Center. This achievement highlights EnerSys's leadership in providing stored energy solutions for industrial applications. Such developments are expected to drive the growth of the market during the forecast period.

Trends in Nuclear Power

The trends in nuclear power for space applications are aimed at improving reliability, efficiency, and power output, focusing on both Radioisotope Thermoelectric Generators (RTGs) and fission reactors.

Radioisotope Thermoelectric Generators (RTG)

Plutonium-238 (Pu-238) RTGs remain the dominant choice for deep-space missions due to their proven reliability and long lifespan, powering recent missions such as the Perseverance rover and the upcoming Europa Clipper with Multi-Mission RTGs (MMRTGs). However, alternatives such as Americium-241 are gaining traction, particularly in Europe, despite the need for additional shielding due to gamma radiation.

Research is also directed toward improving thermoelectric conversion rates and integrating supplementary batteries to better manage peak power demands, enhancing overall system efficiency. For higher power needs, Small Modular Reactors (SMRs) are being prioritized, with designs such as NASA’s Kilopower and Russia’s TOPAZ-II providing compact solutions for crewed missions and high-energy instruments. These modern reactors can automatically adjust their power output based on demand, which reduces thermal stress and enhances safety.

Internationally, advancements are being made in next-generation reactors, with the U.S. and Russia leading the charge, while China's HTR-PM showcases the viability of high-temperature gas-cooled reactors. This collaborative global effort reflects a growing commitment to harness nuclear power for future space exploration, ensuring that missions are equipped with reliable and efficient energy sources.

Nuclear Fission Reactors

Nuclear Fission systems are reliable and long-lasting, making them suitable for power at surface bases, life support, communications, and scientific instruments. Nuclear fission systems, including Nuclear Thermal Propulsion (NTP) and Nuclear Electric Propulsion (NEP), are advancing rapidly. These technologies promise faster travel times, higher efficiency, and longer mission durations for deep space exploration.

- North America witnessed space power supply market growth from USD 1.36 Billion in 2023 to USD 1.50 Billion in 2024.

For instance, NASA, in partnership with DOE, is currently developing a 40-kilowatt class fission power system for lunar surface operations, targeting deployment in the early 2030s. To achieve this, L3Harris has partnered with Westinghouse in Cranberry Township, Pennsylvania, to develop a Fission Surface Power solution under a Phase 1 contract awarded by NASA and the U.S. Department of Energy. This initial phase of NASA’s Fission Surface Power Project aims to make conceptual designs for a compact, electricity-generating nuclear fission reactor intended for future lunar missions. Such advancements make nuclear power a practical and scalable solution for powering habitats, equipment, and scientific experiments on the Moon and, eventually, on other planets, driving the growth and adoption of nuclear energy for space exploration.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Surge in Satellite Constellations Coupled with Rising Demand for Satellite Communications Boost Market Growth

The surge in the deployment of satellite constellations serving diverse purposes, such as Earth observation, communication, and navigation, is driving the demand for space-grade power supply. These constellations necessitate advanced electronics to guarantee consistent and reliable operation within the challenging space environment.

A satellite constellation, also known as a swarm, constitutes a network of identical or similar artificial entities pursuing a common objective and under the control of the same entity. These groups communicate with ground stations globally and are occasionally interconnected, operating as a cohesive system designed to complement one another.

With numerous satellite constellations currently orbiting the Earth, the planet is poised to witness a substantial increase in launches over the next few years. Both existing and upcoming satellite constellations play crucial roles in various domains, such as the Internet of Things, telecommunications, navigation, weather monitoring, and Earth and space observation, among others.

- For instance, SpaceX expanded its Starlink satellite network with the successful launch of 28 new satellites on May 6, 2025, bringing the total to over 7,200 in low Earth orbit. This latest deployment strengthens Starlink’s position as a leader in global satellite internet, especially as demand for reliable connectivity grows.

Surge in the Number of Small Satellites to Propel Market Growth

The increasing number of small satellites is a driving factor for the space power supply market due to the rising demand for compact satellites that can be built depending on the requirements and launched at a lower cost than traditional satellites. Small satellites have advantages, such as low weight and dimensions, short time required for their development, and high performance in complex computing operations, making them cost-effective for various applications, including communication, navigation, Earth observation, and deep space exploration.

North America dominates the small satellite market due to the presence of leading small satellite manufacturers, ground station operators, and launch service providers with a highly developed space industry ecosystem. Satellite projections indicate that from 2024 to 2029, annual launches will rise from 3,220 to 4,662 units, an increase of 1,442 satellites within five years. Over the longer term, nearly 18,500 small satellites are expected to be launched between 2024 and 2032.

The U.S. government also plays a major role in business development, with agencies such as NASA and the U.S. Department of Defense funding many small satellite missions and programs. Although the COVID-19 pandemic had a severe impact, the market has been resilient due to high demand from numerous applications such as communication, navigation, and earth observation.

Market Restraints

Supply Chain Disruptions and Associated High Costs and Regulations to Impede Market Growth

The market is poised to face challenges as it contends with supply chain disruptions and geopolitical tensions. Supply chain disruptions stemming from various factors such as raw material shortages, transportation issues, and geopolitical instabilities pose a significant threat to the smooth operation of the space power supply industry. These disruptions can result in delays, increased costs, and hampered production efficiency, impacting the overall growth of the market.

The high cost of designing and manufacturing space power electronics that can withstand extreme space conditions is a significant challenge that is hindering the global space power supply market growth. The space industry is highly regulated, and all components require stringent quality inspections and legal documentation before use in a spacecraft, which adds to the cost. Additionally, the use of sophisticated control systems and the high costs of testing and raw materials also contribute to elevated expenses of space power electronics.

The trend toward smaller satellites, being more cost-effective to build, launch, and operate, has reduced costs while allowing for faster and more flexible deployments, including satellite mega-constellations. However, the demand for high-performance, lightweight components that rely heavily on satellites is increasing, which is driving the market for space power supplies.

Moreover, telecom companies, such as PLDT, are racing to integrate Low Earth Orbit (LEO) satellites into their infrastructure to prepare for the arrival of Starlink, owned by SpaceX and Elon Musk, in the Philippines, further leading to higher costs for space power supply.

Market Opportunities

Rising Investments in Deep Space Exploration and Shift Toward Commercial Space Exploration are Prominent Market Opportunities

In-Situ Resource Utilization (ISRU) is a crucial idea and technique in space exploration that entails harnessing resources found on extraterrestrial bodies such as the Moon, Mars, asteroids, or other planets to support human missions and settlements. Instead of relying only on Earth-based supplies, ISRU intends to lower mission costs, boost self-sufficiency, and enable long duration space exploration by utilizing accessible resources in space.

ISRU uses space-based resources for deep space exploration. ISRU can increase safety for crew and enhance mission capabilities, which allows them to explore farther from Earth with more independence. The first mission was uncrewed to test the SLS rocket's safety and the ability of the Orion capsule to reach the Moon, perform in lunar orbit, and return to Earth for an ocean splashdown. The SLS rocket launched ten CubeSats into space to conduct experiments and demonstrate technologies.

A Japanese private lunar successfully entered orbit around the Moon and is preparing for a touchdown attempt in June 2025. This marks a significant step for commercial lunar exploration, showcasing the growing role of private companies in deep space missions. Also, India is set to launch 52 satellites over the next five years to boost space surveillance and defense capabilities. Notably, half of these satellites will be built by the private sector, with ISRO transferring SSLV technology to enable rapid small satellite launches. These developments will propel the space power supply market share in Asia.

Space Nuclear Power System Developments: Roadmap

1961: First Use of Nuclear Power in Space (Transit 4A Satellite)

The U.S. Navy’s Transit 4A navigation satellite became the first U.S. spacecraft powered by nuclear energy. The spacecraft used a Radioisotope Thermoelectric Generator (RTG) fueled by plutonium-238.

1961-1975: Expansion of RTG Use and Soviet Reactor Programs

The U.S. continued to develop RTGs for missions such as the Nimbus III weather satellite (1969), which combined RTGs and solar cells for power. USSR developed and launched about 40 nuclear-electric satellites, using the BES-5 fission reactor and later the TOPAZ-II reactor, which produced up to 10 kilowatts of electricity.

1969: Apollo 12-17 Lunar Surface Experiments

The experimental equipment left on the Moon by Apollo missions 12 through 17 was powered by radioisotope thermoelectric generators, each providing 70 watts of electricity.

Viking 1: First Successful Mars Landing and Exploration Mission

Launched on August 20, 1975, Viking 1 was the first spacecraft to achieve a successful landing on Mars, arriving on the surface in 1976. The lander was powered by two Radioisotope Thermoelectric Generators (RTGs), which provided continuous electrical power essential for its extended mission.

2010–2020: Russian and U.S. Megawatt-Class Reactor Development

Russia began developing standardized space modules with nuclear-powered propulsion, aiming for megawatt-class systems crucial for crewed missions to the Moon and Mars. The Keldysh Research Centre’s concept uses a small gas-cooled fission reactor to power plasma thrusters, with launches envisioned for the early 2020s.

2024: Advanced Space Nuclear Power Conversion

Rolls-Royce LibertyWorks was awarded a USD 1 million contract by NASA in April 2024 to develop a preliminary design for an Advanced Closed Brayton Cycle power conversion system for next-generation space-based nuclear microreactors.

Key Insights on Nuclear Power

- In January 2025, The PULSAR research project, led by Tractebel, introduced the conceptual design of an efficient plutonium-238-fueled radioisotope power system for lunar missions, addressing the challenges of weight and fuel requirements associated with current RTGs. Funded by the European Commission, the project involves collaboration with various research institutions to explore the production of Pu-238 in the EU.

- In January 2025, Westinghouse was selected by NASA and the U.S. Department of Energy to continue developing a space microreactor under the Fission Surface Power (FSP) project, aiming to provide reliable nuclear power for astronauts on the Moon and beyond.

- In January 2024, Zeno Power Systems collaborated with the U.S. Department of Energy to recycle strontium-90, a byproduct of nuclear fission, to create compact radioisotope power sources for satellites, addressing the limited supply of plutonium-238. The company aims to deliver its first RPS-powered satellite to the U.S. Air Force by 2026, expanding its applications in national security and space exploration.

Segmentation Analysis

By Power Source

Increasing Demand for Satellites Drive Battery Power Segment Growth

Based on power source, the market is categorized into solar power, nuclear power, and battery power/storage.

Battery power/storage is estimated to be the largest segment and holds a dominant market share of 58.63% in 2026. Battery power sources such as non-rechargeable (primary batteries) and rechargeable (secondary batteries), Battery charge/discharge units (BCDUs), power conditioning, and distribution are considered in the scope. The segment’s growth is driven by the increasing demand for satellites used for various purposes such as Earth observation, communication, navigation, weather forecasting, telescopes, space science, and human space exploration activities.

The solar power segment is estimated to grow with a significant CAGR during the forecast period. The solar power segment comprises solar panels, inverters-convert DC to AC, monitoring equipment, racking and mounting components, power conditioning and distribution systems. The growth of solar power supply in space is driven by several factors, including the potential for non-intermittent renewable electricity, the increased efficiency due to the absence of atmospheric absorption, and the potential for flexible and remote power supply, particularly for military and mining operations, disaster zones, and remote locations.

- For instance, in April 2024, a U.K.-based startup announced a major breakthrough in their plans to beam solar energy from space to Earth. At a lab in Oxford, Space Solar was able to light up an LED sign by wirelessly beaming energy through the air from all angles to unveil the world's first 360-degree wireless power transmission.

By Battery Shape

Growing Demand for Space Efficiency to Propel Cylindrical Batteries Segment

Based on battery shape, the market is categorized into cylindrical batteries, prismatic batteries, and pouch-type batteries.

Cylindrical batteries are estimated to be the largest and fastest-growing segment during the forecast period. The growing adoption of software-based solutions, such as digital logbooks, digital maintenance manuals, and other aircraft health monitoring software, boosts segment growth. Cylindrical batteries are known for their compact and efficient use of space, making them suitable for devices with limited room for battery placement. The increasing use of cylindrical batteries in space applications is attributed to their efficient use of space, mechanical stability, ease of manufacture, compatibility, safety features, and reliability. These qualities make them a preferred power source for various space technologies and missions, making them a favorable choice among end-users.

The prismatic battery segment is projected to witness significant growth during the forecast period. The growth of prismatic shape batteries in space applications is fueled by their efficient space utilization, improved safety and durability, customization and scalability, consistent heat distribution, simplified manufacturing, and cost benefits.

By Battery Capacity

Medium Capacity (100-500 Wh) Batteries to Experience High Growth due to Rise in Use of Small & Medium Satellites for Various Military Operations

Based on battery capacity, the market is divided into low capacity (<100 Wh), medium capacity (100-500 Wh), and high capacity (>500 Wh).

The medium capacity (100-500 Wh) segment is projected to experience the highest growth during the forecast period. An increase in small and medium satellites for military operations, along with an easy integration of medium-capacity batteries in some satellites, is expected to support the segment’s growth in the coming years.

The low capacity (<100 Wh) segment dominated the market in 2024. The growing number of nanosats and CubeSats being launched is driving the growth of the low capacity segment. Additionally, the growth is driven by the increasing demand for compact and efficient energy storage solutions in various space applications, including CubeSats, nanosats, and other form factors. The Saft solution for high-power space applications is based on the Saft VL51ES Li-ion cells. For instance,

- In April 2024, Satellite Technology and Research Centre, a research organization under the University of Singapore, unveiled the successful launch of a microsatellite to improve maritime communications.

By Product Type

Environmental Benefits and Cost-Effectiveness of Solar Power to Enhance the Growth of Solar Panel Segment

Based on product type, the market is divided into solar panels, power management devices, power converters, energy storage, and others.

The solar panel segment dominated the market in 2024. The growing adoption of solar power for space applications is due to a variety of advantages offered, such as environmental benefits and cost-effectiveness, which is driving the solar panel segment growth in the market.

The power management devices segment is expected to grow at the highest CAGR during the forecast period. The segment’s growth is owed to the increasing demand for efficient and reliable power systems to support the expanding number of satellites used for various purposes such as Earth observation, communication, navigation, weather forecasting, telescopes, space science, and human space exploration activities. For instance,

- The Energy Storage segment is expected to emerge as the leading segment with a 38.08% share in 2026.

- In July 2023, Renesas Electronics Corporation unveiled a complete space-ready reference design for the AMD Versa adaptive system-on-chip XQRVC1902. The ISLVERSALDEMO2Z reference design was developed in collaboration with AMD and integrates key radiation-hardened components for power management, including four new and recently released products, into an ultra-compact design.

To know how our report can help streamline your business, Speak to Analyst

By Application

Advancements in Technology to Enhance Communication Satellites’ Growth

Based on application, the market is divided into communication satellites, navigation satellites, space stations, earth observation satellites, space probes and rovers, and launch vehicles and rockets.

The communication satellites segment held the dominant market share of 41.25% in 2026 and is projected to experience fastest-growth during the forecast period. The growth of communication satellites is driven by advancements in technology, increasing demand for global connectivity, reliability and security, new service demands, and the need to address orbital debris and congestion.

These factors have contributed to the unprecedented growth of commercial satellites in lower earth orbit and the development of new technologies, such as high-throughput satellites and small satellites, which have improved the efficiency, capacity, and cost-effectiveness of satellite communication systems. For instance,

- In November 2023, SpaceX launched the O3b mPOWER communications satellites. The two Boeing-built satellites aboard the flight will add to the O3b group of communication satellites operated by provider SES S.A. of Luxembourg.

The launch vehicles and rockets segment is projected to witness significant growth during 2025-2032. Numerous new and frequent launches are expected to drive the growth of this segment in the forecast period. Additionally, upcoming scheduled launches and maintenance of pre-existing space missions are expected to drive segmental growth.

By End-user

Government and Military Held Dominant Share Owing to Regulatory Oversight on Space Operations

Based on end-user, the market is divided into government and military, commercial operators, and research institutions.

The government and military segment is estimated to be the largest segment, 69.35% share in 2026, accounting for a dominant market share. The prevalence of government bodies regulating space operations in a particular country or region is a major reason for a dominating market share. For instance,

- In April 2024, a critical engine certification test series at NASA's Stennis Space Center located near Bay St. Louis, Mississippi, marked a significant milestone in producing new RS-25 engines to power the Artemis campaign to the Moon and beyond.

The commercial operators segment is projected to witness the highest growth. The segment is estimated to hold a significant market share during the forecast period. The substantial growth for the segment is driven by the increasing demand for space-based services, such as satellite communications, Earth observation, and navigation, which require reliable and efficient power systems.

SPACE POWER SUPPLY MARKET REGIONAL OUTLOOK

The global market is segmented into regions such as North America, Europe, Asia Pacific, the Middle East, and rest of the world.

North America Space Power Supply Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America generated USD 1.62 billion, contributing 46.92% to global market revenue, and is projected to grow to USD 1.73 billion in 2026. The maximum number of companies operating in space power supply is present in the U.S. In addition, the region has two major space agencies, NASA and Canada Space Agency (CSA). The U.S. market is projected to reach USD 1.54 billion by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 0.96 billion in 2025, capturing 27.66% of the global market share, and is projected to reach USD 1.03 billion in 2026. Digitalization and technological advancements in this region are enhancing the space power industry. Thus, stronger growth is expected during the forecast period. The Japan market is projected to reach USD 0.22 billion by 2026, the China market is projected to reach USD 0.45 billion by 2026, and the India market is projected to reach USD 0.19 billion by 2026.

Europe

The Europe market accounted for USD 0.77 billion in 2025, representing 22.24% of the global industry, and is expected to reach USD 0.82 billion in 2026. Europe's market size is estimated to grow at a moderate rate owing to increasing demand, technological advancements, and a positive industry outlook. The UK market is projected to reach USD 0.31 billion by 2026, while the Germany market is projected to reach USD 0.13 billion by 2026.

Middle East & Rest of The World

The Middle East & Africa market generated USD 0.07 billion in 2025, representing 2.13% of the global market landscape, and is expected to reach USD 0.08 billion in 2026. The Middle East is expected to grow due to the expansion of the space-based services market and the strengthening economies in the region.

The rest of the world's growth is based on the expansion of the space industry and increasing collaborations with major market players. Latin America accounted for USD 0.04 billion in 2025, representing 1.05% of the global market share, and is projected to reach USD 0.04 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Adapt Service Portfolio Expansion Strategies to Ensure Market Survival

The space power supply market is dominated by several key players and is characterized by a consolidation of global companies operating within the industry. Notable, key players are providing high-quality, advanced batteries and power supply solutions. Most of these players are focusing on increasing their battery capacity while expanding their global network. The top five players in the industry include Northrop Grumman Corporation, Saft Groupe SA, Airbus S.A.S, EaglePitcher Technologies, and GS Yuasa International Ltd.

List of Top Space Power Supply Companies Profiled

- AAC Clyde Space (U.K.)

- Airbus S.A.S (Netherlands)

- AZUR SPACE Solar Power GmbH (Germany)

- DHV Technology (Spain)

- EaglePitcher Technologies (U.S.)

- GS Yuasa International Ltd. (Japan)

- Northrop Grumman Corporation (U.S.)

- Rocket Lab USA, Inc. (U.S.)

- Saft Groupe SA (France)

- Teledyne Technologies Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Teledyne Micropac introduced a patent-pending, standard 3U VPX power supply card designed for Low Earth Orbit (LEO) satellites. This compact device, about the size of an index card, delivers up to 600W output. The VPX-3U-SP-PSC accelerates satellite design and integration by adhering to key standards (PMBus, VITA 62/48/78). It offers selectable or software-controlled voltage rails, allowing for flexible power management.

- February 2025: Pixxel and DHV Technology successfully collaborated on the Firefly satellite constellation. DHV provided six sets of high-performance solar panels, ensuring reliable power for Pixxel’s advanced hyperspectral satellites.

- March 2024: The Northrop Grumman Corporation, a player in the space power supply market, honored EaglePicher Technologies with its Supplier Excellence Award. EaglePicher's contributions include advanced defense strategies and ensured mission accomplishment. Recognized for its exceptional performance, EaglePicher played a vital role in supporting Northrop Grumman’s production and distribution objectives as the industry works to assist Department of Defense clients and other commercial entities.

- September 2023: 5N Plus Inc., the parent company of AZUR SPACE Solar Power GmbH, unveiled the world's largest and most efficient next-generation long-duration solar energy storage project, said to be powered by the triple junction solar cells supplied by the company's wholly-owned subsidiary, AZUR SPACE Solar Power GmbH.

- September 2023: Tuthill Corporation, a private organization based in the U.S., entered into an agreement to acquire EaglePitcher Technologies. The transaction is closed in 2023, subject to required regulatory approvals and other customary closing conditions.

REPORT COVERAGE

The report provides detailed information on the competitive market landscape and focuses on leading companies, product types, and leading product applications. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the above factors, it contains several factors that have contributed to the sizing of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.36% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Power Source

|

|

By Battery Shape

|

|

|

By Battery Capacity

|

|

|

By Product Type

|

|

|

By Application

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights stated that the global market size was USD 3.69 billion in 2026 and is projected to record a valuation of USD 6.51 billion by 2034.

Registering a CAGR of 7.36%, the market will exhibit rapid growth during the forecast period.

By power source, the battery power/storage segment is projected to dominate the market during the forecast period.

Northrop Grumman Corporation, Saft Groupe SA, and Airbus S.A.S are the major players in the global market.

North America dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 290

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us