Spaceport Market Size, Share & Industry Analysis, By Spaceport Type (Vertical Launch Spaceports, Horizontal Launch & Landing Spaceports, Reentry & Landing Spaceports, & Others), By Service Offering, By Launch Type, By Application (Commercial Satellite Launch Support, Defense & National Security Missions, Government Civil Space Missions, Human Spaceflight & Space Tourism, Research, Testing & Demonstration, Reusable Vehicle Recovery, & Others), By End User (Commercial Launch Operators, Government Space Agencies, Defense / Military Agencies, & Others), and Regional Forecast, 2026-2034

Spaceport Market Size and Future Outlook

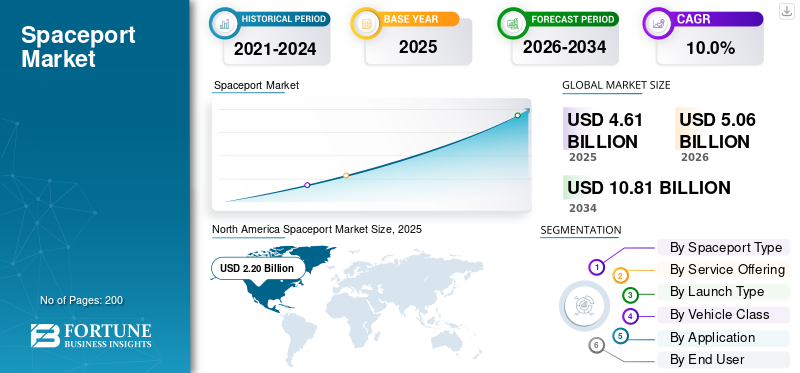

The global spaceport market size was valued at USD 4.61 billion in 2025. The market is projected to grow from USD 5.06 billion in 2026 to USD 10.81 billion by 2034, exhibiting a CAGR of 10.0% during the forecast period. North America dominated the spaceport market with a market share of 47.72% in 2025.

A spaceport is a launch and reentry facility that supports space launches, payload processing, mission control, propellant handling, range safety, and recovery-related spaceport operations. The market is growing due to increasing satellite launches, rising demand for satellite based services, expanding space exploration, reusable launch vehicles, space tourism, and stronger national space programs. Growth is visible across space launches, North America Europe, Asia Pacific, where governments and private operators are expanding infrastructure for faster, safer, and more flexible access to earth orbit.

Key players includes Blue Origin LLC, Rocket Lab, Arianespace/ArianeGroup, and China’s major launch entities. These leading companies are driving the market through reusable launch vehicles, new launch pads, commercial payload services, and high-velocity deployment. Blue Origin LLC is advancing New Glenn and Launch Complex 36, Rocket Lab supports the commercial spaceport model through Launch Complex 1, and ISRO’s new launch-pad investments strengthen Indian space research and future commercial space activity.

Download Free sample to learn more about this report.

SPACEPORT MARKET TRENDS

Shift toward Reusable Launch Vehicles and High-Cadence Commercial Spaceport Operations to be a Significant Market Trend

A major trend in the market is the shift from one-time launch infrastructure toward reusable launch vehicles, rapid turnaround capability, and higher-frequency spaceport operations. Spaceports are now being designed not only for satellite launches, but also for booster recovery, refurbishment, reentry support, mission control, and repeat commercial access to earth orbit. This trend is strongest in North America, but it is also influencing Europe and Asia Pacific as governments and private operators invest in modern launch pads, recovery zones, and commercial launch-support infrastructure.

In August 2025, the U.S. FAA marked its 1,000th licensed or permitted commercial space operation. The FAA noted that the first 500 operations took 32 years, while the next 500 took only four years, showing the rapid rise of commercial launch and reentry activity.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Satellite Launch Demand and Satellite-Based Services Drive Market Growth

The strongest driver for the global spaceport market growth is the rapid increase in satellite launches for communications, Earth observation, navigation, defense surveillance, and other satellite based services. As more commercial and government payloads move into earth orbit, demand is rising for launch pads, payload processing, integration facilities, range safety, mission control, and recovery-ready spaceport operations. This is pushing spaceports to shift from occasional launch facilities into high-utilization infrastructure hubs that support both national space programs and private commercial space activity.

In 2024, BryceTech reported 259 orbital launches and 2,873 spacecraft deployed globally, with commercial providers accounting for about 70.00% of orbital launches and small satellites representing 97.00% of spacecraft launched. This supports the demand-side growth of spaceports, especially for commercial satellite launch support.

MARKET RESTRAINTS

Regulatory, Environmental, and Range-Safety Approvals Restrain Market Growth

A major restraint for the market is the long and complex approval process around launch licensing, environmental review, airspace closure, public safety, and range coordination. Spaceports cannot scale only by building more pads, every increase in space launches, reentry activity, or reusable launch vehicle operation need to have clear safety, environmental, and airspace requirements. This slowdown the increasing space launches, delay new commercial spaceport projects, and increase compliance costs for operators, especially for launch sites that are located near coastal habitats, public roads, populated areas, or busy airspace.

MARKET OPPORTUNITIES

Emerging Commercial Spaceports and Small-Satellite Launch Demand Create Strong Growth Opportunities

A major opportunity in the market is the development of new commercial spaceport infrastructure in countries that want independent launch access and a share of the growing small-satellite economy. As demand for satellite launches, satellite based services, and low-cost access to earth orbit increases, emerging launch sites in India, China, Brazil, Oman, Australia, and other countries attract commercial operators that need flexible pads, payload integration, range safety, and faster launch windows. This opportunity is important since the market is no longer limited to traditional launch hubs, newer spaceports can compete by serving small launch vehicles, responsive launch missions, and regional commercial space customers.

MARKET CHALLENGES

Airspace, Maritime Coordination, and Range-Capacity Bottlenecks Challenge Market Growth

Major challenge for the market is managing higher launch cadence without creating bottlenecks in airspace, maritime zones, and range-safety systems. As space launches, reentries, reusable launch vehicles, and satellite launches increase, spaceports must coordinate with aviation authorities, shipping routes, defense ranges, local communities, and environmental regulators. This makes spaceport operations more complex, especially for coastal launch sites where falling debris zones, weather windows, flight paths, and public-safety corridors must be managed carefully.

Impact of Ongoing Conflicts

Ongoing Conflicts Accelerate Sovereign Launch, Defense Satellite Demand, and Spaceport Modernization

The ongoing Russia-Ukraine conflict, conflicts in the Middle East region, disputes in the Red Sea region, and other conflicts are contributing toward the shaping of the global market by two approaches. On one hand, these conflicts are increasing demand for secure communications, ISR services, resilience, navigation resilience, missile warning and military satellites' launches. On the other hand, these conflicts are forcing nations to rely less on foreign entities for launch services. The increased demand will fuel growth in services such as launch pad, range safety, mission control services, and payload integration.

In March 2022, the European Space Agency decided to suspend its collaboration with Roscomos in the context of the ExoMars mission amid Russia's invasion of Ukraine. Also, the ESA reported the removal of Soyuz rockets from Europe's spaceport based in French Guiana owing to the conflict with Russia.

In December 2024, the European Commission signed a concession contract for a 290-satellite secure connectivity system called IRIS2.

Segmentation Analysis

By Spaceport Type

Due to High Orbital Launch Demand, Vertical Launch Spaceports Segment Dominated Market

In terms of spaceport type, the market is categorized into vertical launch spaceports, horizontal launch & landing spaceports, reentry & landing spaceports, and sea-based / mobile spaceports.

Vertical Launch Spaceports segment held the largest global spaceport market share in 2025, since almost all orbital missions, heavy-lift launches, small satellites deployments, and defense and governmental launches rely on vertical launch spaceports. The reason behind that is the significant investment required for building and operating a vertical launch site. This type of launch site requires the presence of a launch pad, flame trenches, integration facility, propellant facility, range safety systems, payload processing facility, and mission control system. Moreover, this segment supports the largest share of satellite launches, space exploration missions, and access to earth orbit, resulting in segment dominance.

Reentry & landing spaceports segment is expected to grow at a highest CAGR of 13.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service Offering

Due to High Fixed-Infrastructure Requirement, Launch Pad / Runway Infrastructure Dominated Market

On the basis of service offering, the market is classified into launch pad / runway infrastructure, payload processing & integration, vehicle assembly & ground support, range safety & mission control, propellant storage & fueling, and spaceport leasing & commercial services.

Launch pad / runway infrastructure segment dominated the market in 2025, as it forms the main physical layer required for every major launch activity. Before a spaceport can scale payload processing, range safety, propellant handling, mission control, or commercial leasing, it needs launch pads, runways, flame trenches, mobile gantries, integration access, deluge systems, and vehicle-support infrastructure. This segment holds the largest market share as modern spaceport operations are becoming more infrastructure-intensive, mainly as countries expand capacity for heavier vehicles, reusable launch vehicles, higher launch cadence, and commercial access to earth orbit.

Range safety & mission control segment is expected to show the fastest growth, registering a CAGR of 11.3% over the forecast period.

By Launch Type

Due to Growing Satellite Deployment and Access-to-Orbit Demand, Orbital Launch Segment Dominated Market

On the basis of launch type, the market is classified into orbital launch, suborbital launch, reentry / recovery operations, and test & demonstration launch.

Orbital launch segment dominated the market in 2025, as most high-value demand is linked to placing satellites, crew/cargo vehicles, defense payloads, and scientific spacecraft into earth orbit. Unlike suborbital or test launches, orbital missions require deeper launch infrastructure, payload integration, range safety, mission control, propellant systems, and post-launch tracking, making them the largest revenue-generating launch type. The dominance is also supported by rising satellite launches, expanding satellite based services, commercial constellations, and national space programs focused on communications, Earth observation, navigation, security, and space exploration.

Reentry / recovery operations segment is expected to show the fastest growth, registering a CAGR of 15.1% over the forecast period.

By Vehicle Class

Due to High Payload Capacity and Deep-Space Mission Requirements, Heavy / Super-Heavy Launch Vehicles Segment Dominated Market

On the basis of vehicle class, the market is classified into small launch vehicles, medium launch vehicles, heavy / super-heavy launch vehicles, and sounding rockets / test vehicles.

Heavy / super-heavy launch vehicles segment held the largest market share in 2025, as they need a high investment in spaceport infrastructure and support the highest-value missions. These vehicles need secure launch pads, large integration facilities, heavy propellant systems, flame trenches, mobile launch structures, range safety, mission control, and recovery-support infrastructure. Additionally, their dominance is also linked to lunar missions, national security payloads, large communication satellites, interplanetary missions, and future human space exploration programs. While small launch vehicles are growing faster in some regions, heavy and super-heavy vehicles continue to hold the largest infrastructure share as they are central to high-mass payload delivery, deep-space access, and strategic government-backed space programs.

Small launch vehicles segment is expected to show the fastest growth, registering a CAGR of 12.6% over the forecast period.

By Application

Due to Rising Commercial Satellite Deployment, Commercial Satellite Launch Support Segment Dominated Market

The market is further divided by application, into commercial satellite launch support, defense & national security missions, government civil space missions, human spaceflight & space tourism, research, testing & demonstration, reusable vehicle recovery, and others.

Commercial satellite launch support segment dominated the global market in 2025, as the largest demand for spaceport infrastructure comes from launching communication, Earth observation, navigation, and constellation satellites into earth orbit. This segment drives continued use of launch pads, payload processing facilities, integration buildings, range safety systems, mission control, propellant handling, and post-launch tracking. As satellite based services expand across broadband connectivity, remote sensing, defense monitoring, and data applications, spaceports are becoming important infrastructure for commercial payload customers and launch operators rather than only government-led space programs.

Reusable vehicle recovery segment is expected to show the fastest market growth, registering a CAGR of 14.3% over the forecast period.

By End User

Due to High Launch Cadence and Commercial Payload Demand, Commercial Launch Operators Dominated Market

Based on end user, the market is segmented into commercial launch operators, government space agencies, defense / military agencies, and others.

Commercial launch operators dominated the market in 2025, as they generate the highest regular demand for launch pads, payload integration, range safety, mission control, and recovery-linked spaceport operations. The market is increasingly shaped by private and semi-commercial operators supporting communication satellites, Earth observation payloads, rideshare missions, small-satellite constellations, defense payloads, and reusable launch vehicles. As commercial space activity expands, spaceports are becoming less dependent on occasional government missions and more tied to operators that can deliver frequent, scheduled, customer-backed access to earth orbit.

Defense / military agencies segment is expected to show the fastest market growth, registering a CAGR of 12.2% over the forecast period.

Spaceport Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Spaceport Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share for spaceport solutions, and is anticipated to grow at a CAGR of 8.9% during the forecast period. Region has established launch ecosystem, including the U.S. with its recognized federal ranges, licensed commercial spaceports, reusable launch vehicle operations, high-frequency satellite launches, and large private-sector participation. The region also benefits from the existence of SpaceX, Blue Origin LLC, Rocket Lab, ULA, NASA, the U.S. Space Force, and FAA-regulated commercial launch infrastructure.

U.S. Spaceport Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 2.17 billion in 2025, growing at a CAGR of 8.6% over the forecast period.

Europe

Europe market is anticipated to grow at a fastest pace with registering a highest CAGR of 11.5% during the forecast period. Europe is a strategically important market, led by France/French Guiana, Russia, the U.K., and emerging Nordic launch sites. The region is rebuilding its launch independence after disruption in Soyuz access and the Ariane transition period. Ariane 6’s first flight from Europe’s Spaceport in July 2024 restored Europe’s independent access to space and strengthened the region’s position in orbital launch, commercial satellite missions, and institutional space programs. Moreover, the U.K. is becoming an important growth pocket, with SaxaVord becoming the U.K.’s first licensed vertical launch spaceport and the first fully licensed vertical spaceport in Western Europe.

France Spaceport Market

France market reached approximately USD 0.39 billion in 2025, equivalent to around 45.38% of Europe revenues.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 10.6% over the forecast period. Region’s growth is driven by China, India, Japan, New Zealand, and South Korea space exploration and ISR satellite mission. China has the largest share in the region by way of high launch cadence, national launch centers and the Hainan commercial spacecraft launch site, which achieved dual-pad readiness with launches from No. 1 and No. 2 pads. India is also growing its spaceport, with the Third Launch Pad at Sriharikota approved in January 2025 to support next-generation launch vehicles, standby launch capacity, and upcoming human spaceflight missions. The region’s market is still dominated by vertical launch infrastructure, but reentry, reusable vehicle recovery, commercial payload processing, and small-launch services are expected to grow faster through 2034.

China Spaceport Market

The Chinese market revenues stood at around USD 0.73 billion, representing roughly 51.83% of the global sales.

India Spaceport Market

The Indian in 2025 stood at around USD 0.24 billion in 2025, accounting for roughly 16.92% of Asia Pacific revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at an 8.4% CAGR during the forecast period. Latin America is led by Brazil’s Alcântara Launch Center, which is moving from a government/test-led base toward commercial launch operations. Brazil’s Operation Spaceward was positioned as a step into the global launch market. In the Middle East & Africa, Oman’s Etlaq Spaceport is the strongest new launch-site signal, with Duqm-1 validating Oman’s first suborbital launch capability in December 2024.

Latin America Spaceport Market

The market in Latin America reached around USD 0.07 billion in 2025, accounting for roughly 55.48% of revenues.

Middle East & Africa Spaceport Market

Africa’s market stood at around USD 0.06 billion in 2025 and is expected to reach USD 0.11 billion in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Reusable Launch Capability and Launch Cadence Shape Competitive Positioning

The global spaceport market is led by private leading companies, government-backed agencies, and spaceport operators. North America holds dominating competitive position, supported by SpaceX, Blue Origin LLC, ULA, Rocket Lab, NASA, and the U.S. Space Force. The region benefits from high launch cadence, reusable launch vehicles, mature launch ranges, and strong commercial payload demand.

Competition is expanding globally as players invest in launch infrastructure, payload services, and recovery capability. Blue Origin LLC is advancing New Glenn and Launch Complex 36, Rocket Lab is strengthening small-satellite launch through Launch Complex 1 in New Zealand, and ArianeGroup/Arianespace are restoring Europe’s independent launch position through Ariane 6. Overall, key players are competing on launch frequency, reusability, payload flexibility, and reliable access to earth orbit.

LIST OF KEY SPACEPORT COMPANIES PROFILED IN REPORT

- Space Exploration Technologies Corp. (U.S.)

- Blue Origin LLC (U.S.)

- Rocket Lab USA, Inc. (U.S.)

- United Launch Alliance, LLC (U.S.)

- Virgin Galactic Holdings, Inc. (U.S.)

- Arianespace SA (France)

- ArianeGroup SAS (France)

- Maritime Launch Services Inc. (Canada)

- Southern Launch Space Pty Ltd (Australia)

- Equatorial Launch Australia Pty Ltd (Australia)

- SaxaVord Spaceport Ltd. (U.K.)

- Spaceport America (U.S.)

- Japan Aerospace Exploration Agency / JAXA (Japan)

- Indian Space Research Organisation / ISRO (India)

- China Aerospace Science and Technology Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Canada announced a 10-year agreement to lease a dedicated launch pad at Spaceport Nova Scotia USD 144.79 million, operated by Maritime Launch Services.

- April 2025: The S. Space Systems Command awarded National Security Space Launch Phase 3 Lane 2 contracts to SpaceX, United Launch Services, and Blue Origin. The anticipated contract values were USD 5.92 billion for SpaceX, USD 5.37 billion for ULA, and USD 2.39 billion for Blue Origin, totaling around USD 13.68 billion.

- April 2025: The FAA completed the environmental review for SpaceX’s Starship/Super Heavy increased cadence at Boca Chica, allowing the proposed action of up to 25 annual Starship/Super Heavy orbital launches, including up to 25 annual Starship landings and 25 annual Super Heavy landings.

- March 2025: China’s Hainan commercial spacecraft launch site completed a Long March-8 mission carrying 18 low Earth orbit satellites, marking the inaugural launch from the site’s No. 1 pad and confirming dual-pad readiness after the No. 2 pad’s November 2024 launch.

- January 2025: India approved the Third Launch Pad at ISRO’s Satish Dhawan Space Centre, Sriharikota. The project value approximately USD 460.25 million, and is intended to support NGLV, LVM3 upgrades, and future human spaceflight missions.

- October 2024: The European Commission awarded the 12-year IRIS concession contract to the SpaceRISE consortium for a secure connectivity satellite system of more than 290 satellites and associated ground infrastructure. The officially disclosed structure is a public-private partnership, program value is USD 11.13 billion.

- August 2024: Norway’s Andoya Spaceport received permission to commence operations. The spaceport has a permit for up to 30 launches per year, with Isar Aerospace using the first launch pad.

- July 2024: ESA completed the inaugural flight of Ariane 6 from Europe’s Spaceport in French Guiana, restoring Europe’s independent access to space and supporting future commercial, institutional, and deep-space launch demand.

REPORT COVERAGE

The global spaceport market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

By Segmentation

|

By Spaceport Type

|

|

By Service Offering

|

|

|

By Launch Type

|

|

|

By Vehicle Class

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stands at USD 5.06 billion in 2026 and is projected to reach USD 10.81 billion by 2034.

In 2025, North Americas market value stood at USD 2.20 billion.

The market is expected to exhibit a CAGR of 10.0% during the forecast period.

Vertical launch spaceports is the leading segment in the market by spaceport type.

Rising satellite launch demand and satellite-based services drive the market growth.

Top players in the market include Blue Origin LLC, Rocket Lab USA, United Launch Alliance, Arianespace, ArianeGroup, Maritime Launch Services, SaxaVord Spaceport, and Southern Launch.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us