Spare Parts Logistics Market Size, Share & Industry Analysis, By Transportation Mode (Airways, Railways, Roadways, And Waterways), By Service Type (Warehouse Services, Transportation, Inventory Management, And Administration & Supplies), By Vehicle Type (Hatchback/Sedan, SUVS, LCVS, and HCVS), By End-Use (OEM Parts and Aftermarket Parts), By Spare Parts Type (Body & Structural Parts, Brake System Parts, Powertrain Components, Suspension & Steering, Engine & Cooling, Exhaust System, Wheels & Accessories, and Others), and Regional Forecast, 2026-2034

Spare Parts Logistics Market Size and Future Outlook

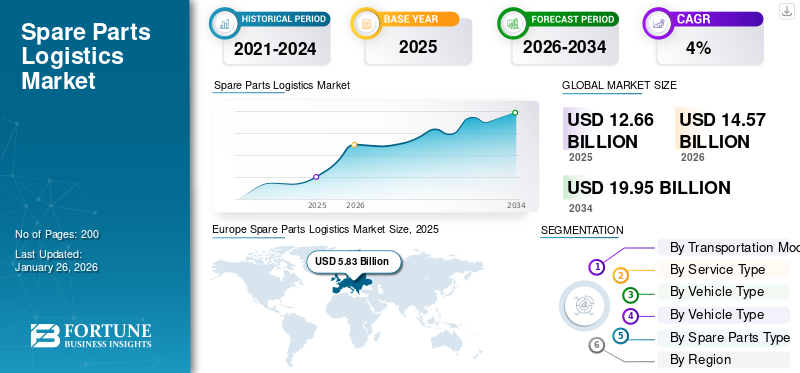

The global spare parts logistics market size was valued at USD 12.66 billion in 2025 and is projected to grow from USD 14.57 billion in 2026 to USD 19.95 billion by 2034, exhibiting a CAGR of 4.00% during the forecast period. Europe dominated the global market with a share of 46.07% in 2025.

Spare parts logistics involves the planning, management, and coordination of sourcing, storing, and distributing vehicle components. It ensures the timely delivery of spare parts to manufacturers, service centers, and customers, minimizing downtime and maintaining optimal vehicle performance. This logistics sector includes inventory control, warehousing, transportation, and demand forecasting, aiming to enhance efficiency, reduce costs, and meet customer expectations in the fast-paced automotive aftermarket environments.

The market is growing due to rising vehicle ownership, aging vehicles, and increased demand for aftermarket services. The integration of advanced technologies in the logistics operation increases service costs which may hamper market expansion. However, the growth of e-commerce platforms providing access to spare parts is expected to fuel market growth during the forecast period.

Leading players in the industry include global logistics providers such as DHL Supply Chain, UPS Supply Chain Solutions, FedEx Corporation, DB Schenker, Kuehne + Nagel, CEVA Logistics, Yusen Logistics, XPO Logistics, and Nippon Express. These companies offer comprehensive logistics services, including warehousing, transportation, and inventory management, to support the efficient distribution of automotive spare parts globally.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Rising Vehicle Ownership to Drive Market Demand

As more vehicles are on the road, the demand for maintenance, repairs, and replacement parts increases. Older vehicles, in particular, require more frequent servicing, leading to a higher need for spare parts. This surge necessitates efficient logistics solutions to ensure timely delivery of components to service centers and repair shops. Consequently, logistics providers are expanding their networks and enhancing inventory management to meet this growing demand, thereby fueling the global spare parts logistics market growth. According to the OICA, global vehicle sales reached 82 million in 2024, up from 80 million in 2023. This marks around 2.5% growth in vehicle ownership, which generates the demand for spare parts, further propels the need for robust logistics infrastructure globally.

Market Restraint

Global Economic Downturns to Restrain Market Growth

Rising fuel costs increases transportation expenses, making the delivery of spare parts more expensive and less profitable. Trade tariffs and international trade barriers can disrupt supply chains, causing postponements and increasing costs for spare parts manufacturers and distributors. Geopolitical instability further affects the availability and price of raw materials needed for manufacturing automotive parts. Furthermore, economic downturns, reduced consumer spending on vehicle maintenance leads to a decline in demand for spare parts. These factors collectively create uncertainty and financial strain, limiting the growth potential of the market.

Market Opportunities

Sustainability and Green Logistics Present Significant Growth Opportunities

The shift toward electric mobility and renewable energy sources for logistics operations reduces carbon emissions and promotes energy-efficient transportation. Companies that adopt electric delivery vehicles, optimize routes for fuel efficiency, and use sustainable packaging materials can reduce operational costs while strengthening their appeal among environmentally-conscious consumers. Additionally, green logistics solutions enable companies to comply with stricter regulations, particularly in Europe and North America, while fostering innovation in energy-efficient supply chain management. As sustainability becomes priority for businesses and consumers, logistics providers embracing green practices are better positioned to attract new clients, expand market shares, and achieve long-term growth. In February 2025, CEVA Logistics announced the addition of 23 electric trucks to replace diesel vehicles in France, Belgium, and the Netherlands, supporting its goal of achieving net zero by 2050.

Market Challenge

Inadequate Delivery Networks Could Hamper Market Development

Delivering spare parts to end consumers or repair shops, particularly in remote or rural areas, can be inefficient and costly due to limited infrastructure and geographical barriers. Tight delivery timelines are essential for customer satisfaction, but logistical difficulties such as traffic congestion, unreliable road conditions, and inadequate delivery networks often result in delays. Additionally, delivering bulky or heavy automotive parts requires specialized handling and transportation, increasing operational complexity and cost. As a result, companies face higher expenses and struggle to maintain fast, reliable service. These obstacles undermine the efficiency of the supply chain, limiting the market's ability to meet growing demand and negatively impacting overall growth.

Spare Parts Logistics Market Trends

Rise in E-commerce Platform to Fuel Market Development

Online platforms allow customers to easily access a vast inventory of spare parts, increasing demand across regions. This surge in online orders requires robust logistics networks to manage warehousing, packaging, and last-mile delivery. E-commerce also drives the adoption of advanced technologies such as automated inventory management, reverse logistics, real-time tracking, enhancing operational efficiency. Additionally, B2B e-commerce simplifies bulk ordering for workshops and dealers, reducing lead times. As consumers and businesses increasingly prefer online purchasing for convenience and price comparison, logistics providers must scale up their operations and adopt innovative solutions. This trend is directly contributing to the expansion and modernization of the spare parts supply chain ecosystem. For instance, in March 2024, General Motors (GM) consolidated its parts and accessories websites for Chevrolet, GMC, Buick, and Cadillac into a unified online store. This strategic move increased e-commerce traffic and sales by offering customers a single platform to purchase OEM parts and accessories. The initiative aims to enhance customer experience and reclaim market share from third-party retailers.

Download Free sample to learn more about this report.

Impact of Tariffs

Increased costs of Imported Parts and Supply Chain Disruption to Hamper Market Demand

Tariffs significantly impact the spare parts logistics market by increasing the cost of imported components and disrupting global supply chains. In March 2025, the U.S. implemented a 25% tariff on imports from countries such as Canada and Mexico, affecting essential components such as engines, transmissions, and catalytic converters. These measures have increased costs for manufacturers and consumers, as tariff expenses are often passed along the supply chain. The Auto Care Association predicted that such tariffs could strain the USD 100 billion automotive parts industry, potentially raising prices for consumers and causing delays in vehicle repairs. Additionally, retaliatory tariffs from affected countries have added complexity to logistics, leading to delays and uncertainties in supply chains.

Segmentation Analysis

By Transportation Mode

Roadways Segment Leads due to its Flexibility

By transportation mode, the market segments are categorized into airways, railways, roadways, and waterways.

The roadways segment dominates the market, holding the largest market share of 45.44% in 2026. Road transportation drives growth in market for spare parts logistics due to its flexibility, speed, and ability to reach remote areas. It enables efficient last-mile delivery and is ideal for smaller shipments. With the rising demand for quick delivery and easy access to spare parts, roadways remain the dominant mode of transport, particularly in regions with well-developed road infrastructure.

In July 2022, TCI Transportation and Command Delivery Systems (CDS) merged to enhance their automotive parts distribution services. The merger combines CDS's expertise in parts delivery with TCI's extensive trucking network, aiming to expand their reach and service capabilities across the U.S. The unified entity will operate under the CDS brand, with TCI Environmental Services, Inc. as the legal entity.

Water transportation is expected to gain traction and witness fastest-growing CAGR during the forecast period. Water transportation showcases a vital role in the market, especially for large bulk shipments and long-distance trade. It offers cost-effective solutions for transporting heavy or oversized components. With the increase in global trade and demand for cost-efficient delivery, waterways continue to drive the market by providing a reliable means for international shipments.

By Service Type

Need for Quick Turnaround Times, Especially in Emergency Repairs Fuels Transportation Segment Demand

By service type, the market is characterized into warehouse services, transportation, inventory management, and administration & supplies.

The transportation segment is projected to dominate the market with a share of 41.24 in 2026. Internal transportation services are crucial to the market, ensuring timely delivery to customers, manufacturers, and distributors. Road, air, and sea transportation systems offer critical flexibility and reliability, fulfilling the growing demand for fast and efficient spare parts delivery. The need for quick turnaround times, especially in emergency repairs, continue to make transportation the dominant service type in this sector. The segment is anticipated to capture 42% of the market share in 2025.

The inventory management is the fastest-growing segment as it ensures efficient stock control, reduces excess inventory costs, and minimizes lead times. With supply chains becoming more intricate and demand for spare parts increasing, companies are adopting advanced technologies such as automation and AI for better forecasting and stock tracking. These innovations are improving overall logistics efficiency and contributing to the segment growth. The segment is expected to record a CAGR of 6.44% during the forecast period.

In September 2024, Advance Auto Parts completed the implementation of a warehouse management system (WMS) at its distribution center in Thompson, Georgia, marking a significant step in its supply chain overhaul. This initiative is part of a broader strategy to consolidate operations into 14 large distribution centers, each operating on a unified WMS. The company aims to enhance inventory productivity and streamline replenishment processes nationwide.

By Vehicle Type

Rising Demand for SUVs Elevates the Spare Parts Demand Propelling Segment Demand

By vehicle type, the market is divided into hatchback/sedan, SUVs, LCVs, and HCVs.

SUVs dominate the market due to their increasing popularity globally. These vehicles require specialized parts, including suspension systems, engines, and brake components. As the demand for SUVs rises, the need for spare parts specific to this vehicle type also grows, ensuring a steady demand for logistics services dedicated to parts distribution. According to the IEA, around 48% of the global car sales comprise SUVs in 2023. The SUVs segment is expected to account for 37.26% of the market share in 2026.

Heavy Commercial Vehicles (HCVs) are witnessing the fastest growth in the market due to expanding businesses such as freight, construction, and transportation. HCVs require specialized components, such as engines, brakes, and transmission systems, creating the need for efficient logistics solutions to manage their distribution. This demand is fueling rapid growth in the segment.

Hatchback/sedan segment is likely to record a CAGR of 4.98% during the forecast period.

By End-use

Reliability and Adherence to Original Specifications Augments OEM Segment Growth

By end-use, the market is divided into OEM parts and aftermarket parts.

OEM (Original Equipment Manufacturer) parts dominate the spare parts logistics market due to their high quality and essential role in maintaining vehicle performance. These parts are favored by manufacturers, repair shops, and consumers for their reliability and adherence to original specifications, ensuring consistent demand and market dominance. This segment is expected to account for 54.20% of the market share in 2026.

Aftermarket parts represent the fastest-growing segment due to increasing vehicle ownership, especially in emerging markets, and increasing consumer demand for cost-effective alternatives to OEM parts. As vehicles age and require more frequent maintenance, the preference for affordable replacement parts drives intensifies. As a result, logistics providers focusing on efficient delivery systems to meet the rising demand. The segment is expected to record a CAGR of 6.69% during the forecast period.

In November 2024, AISIN Corporation established AISIN Aftermarket & Service of America, Inc., a new company dedicated to the automotive aftermarket in the Americas. Formed through the merger of AWTEC, specializing in transmission remanufacturing, and the aftermarket division of AISIN World Corp. of America. This strategic move aims to expand its product offerings beyond its in-house brands. The expanded lineup will include cooling systems, drivetrain products, steering and suspension components, chemicals and fluids, and a wide range of maintenance-related items such as wiper blades, lubricants, batteries, tire accessories, wheel balancers, and car lifts.

By Spare Parts Type

To know how our report can help streamline your business, Speak to Analyst

Increasing Procurement of EVs Generates Powertrain Component Demand

By spare parts type, the market is divided into structural parts, brake system parts, powertrain components, suspension & steering, engine & cooling, exhaust system, wheels & accessories, and others.

Powertrain components, including engines, transmissions, and drivetrains, dominate the market due to their critical importance in vehicle operation. With the increasing procurement of electric vehicles (EVs), demand for powertrain components, especially electric motors and batteries, is surging, contributing to the highest CAGR in the market. According to IEA, the proportion of electric cars in total sales rose from approximately 4% in 2020 to 18% in 2023.

The brake system parts segment is poised for holding 25% of the market share in 2025.

Body and structural parts, such as bumpers, doors, and windows, hold the second-largest market share due to their essential role in vehicle safety and aesthetics. These parts are in constant demand for repairs and replacements, especially following accidents, ensuring steady growth in the logistics sector. The segment is likely to record a CAGR of 4.13% during the forecast period.

Spare Parts Logistics Market Regional Outlook

Europe

Europe leads the spare parts logistics market due to its well-established automotive industry, aging vehicle fleet, and increasing demand for both OEM and aftermarket parts. The regional market value in 2026 was USD 6.68 billion, and in 2025, the market value led the region by USD 5.83 billion. The region's stringent environmental regulations promote the adoption of green logistics practices, such as the use of electric delivery vehicles. Additionally, high levels of vehicle sales, particularly electric vehicles, and the rising trend of e-commerce for spare parts drive continued growth in the logistics market. In November 2023, Chirey Motor México partnered with DHL Supply Chain to enhance its auto parts logistics across Mexico. The alliance involves relocating over 92 containers, totaling 240,000 parts, to a new facility. The upgraded system aims to reduce transit times to 1 to 3 days, improve same-day fulfillment, and improve inventory availability to seven months, with a fill rate target of 92%. The market value in Poland is expected to be USD 0.45 billion in 2025. Europe contributed approximately USD 5.83 billion to the global market in 2025, accounting for 46.07% share, and is expected to reach USD 6.68 billion in 2026.

On the other hand, Germany is projecting to hit USD 1.92 billion and France is likely to hold USD 0.59 billion in 2026.

Europe Spare Parts Logistics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In North America, the spare parts logistics market is driven by highs level of vehicle ownership, strong aftermarket demand, and the presence of major automotive manufacturers. The region's advanced infrastructure and significant e-commerce growth also contribute to market expansion. Additionally, increasing vehicle predictive maintenance and repair needs, along with a growing focus on electric vehicles, further boost demand for logistics services for spare parts in the region. The market in North America reached USD 3.27 billion in 2025, representing 25.79% of total market revenue, and is projected to reach USD 3.69 billion in 2026.

The U.S. is likely to dominate the market size of USD 1.99 billion in 2026. The growth of the market in the country is driven by the aging vehicle fleet, a prompt increase in the maintenance and repairs, and the e-commerce emergence which provides reliable parts delivery. Moreover, various automakers are also establishing parts distribution centers to make efficient and timely delivery to the dealers and customers. For instance, in May 2025, Stellantis opened an automated parts distribution center in Hudson Valley, New York. The facility is widespread in 500,000 sqft., making available around 46,000 various types of parts in stock.

Asia Pacific

Asia Pacific experiences significant growth in the market, driven by rising vehicle ownership, urbanization, and the expansion of the automotive manufacturing sector, particularly in China and India. In 2025, the Asia Pacific market stood at USD 2.64 billion, representing 20.84% of global demand, and is projected to grow to USD 3.08 billion in 2026. The growth of e-commerce and digital platforms for spare parts sales further accelerates logistics demand. Additionally, the region's infrastructure development and growing middle-class consumer base contribute to the increasing need for efficient logistics services for spare parts solutions. In December 2023, Maersk inaugurated a 3,000 m² automotive parts warehouse for Nissan in Wuhan, China, enhancing its long-term partnership with the automaker. The facility, located near the Yangluo port, offers services including inbound and outbound operations, inspections, mix bundling, and quality assurance. This development aims to improve supply chain efficiency and support Nissan's global export operations. The market in China is expected to hit USD 1.17 billion in 2026. On the other hand, South Korea market is poised for a significant value of USD 0.37 billion and Japan is likely to reach USD 0.62 billion in 2026.

Rest of the World

Rest of the World recorded a market size of USD 0.92 billion in 2025, capturing 7.30% of the global market share, and is projected to reach USD 1.12 billion in 2026. In regions such as South America and the Middle East and Africa, growth is driven by rising vehicle sales, increasing demand for aftermarket parts, and improving infrastructure. Growing urbanization and economic development in these regions are increasing the need for automotive maintenance and repairs, thus driving the demand for logistics services for spare parts. Furthermore, expanding cross-border trade in parts fuels market growth. In October 2024, Neweast General Trading signed a lease with DP World's Jebel Ali Free Zone (Jafza) to establish the largest automotive spare parts distribution hub in the Middle East and Africa (MEA) region. The AED 500 million (USD 136.2 million) investment will transform a 165,000 sq. meter space into a facility supporting over 160 premium aftermarket brands. The hub is expected to be operational by October 2024 and aims to enhance order fulfillment across the region.

Competitive Landscape

Key Market Players

Key Firms Focus of Leveraging Advanced Technologies to Improve Efficiency And Reduce Costs

The competitive landscape of the market is marked by the presence of both global and regional players offering comprehensive solutions for transportation, warehousing, and inventory management. Major logistics companies, such as DHL, Kuehne Nagel, and DB Schenker, dominate the market by leveraging advanced technologies such as AI, IoT, and automation to improve efficiency and reduce costs. Regional players are focusing on providing specialized services tailored to local market needs, including last-mile delivery and e-commerce integration. The increasing adoption of green logistics practices and electric vehicle (EV) parts handling is a key differentiator. Additionally, partnerships between automotive manufacturers and logistics providers are becoming more common to ensure timely delivery and inventory optimization. Competition remains intense, with companies focusing on innovation, speed, and sustainability to strengthen their market positions.

List of Key Spare Parts Logistics Companies Profiled-

- Kuehne Nagel (Switzerland)

- DHL Supply Chain (Germany)

- XPO Logistics (U.S.)

- CEVA Logistics (Switzerland)

- Rhenus Logistics (Germany)

- Dachser (Germany)

- UPS Supply Chain Solutions (U.S.)

- DB Schenker (Germany)

- Yusen Logistics (Japan)

- Hellmann Worldwide Logistics (Germany)

- Geodis (France)

- Nippon Express (Japan)

- Kintetsu World Express (Japan)

- Sinotrans (Japan)

- Kerry Logistics (Hong Kong)

- Expeditors International (U.S.)

- Panalpina (now part of DSV) (Switzerland)

- Groupe Charles André (France)

- Inchcape (U.K.)

Key Industry Developments

October 2024- OMODA & JAECOO (Thailand), a subsidiary of Chery Automobile, partnered with DHL Supply Chain to enhance warehouse and transportation services for automotive parts and components. The 1,000+ square meter warehouse utilizes advanced technologies for efficient after-sales services. Additionally, the company fully equipped its showrooms with vehicle displays, maintenance areas, training centers, and PDI centers, supporting full-scale operations and customer deliveries of the OMODA C5 EV and JAECOO 6 EV.

September 2024- Volkswagen celebrated the 20th anniversary of its Parts and Accessories Center (PAC) in Vinhedo, São Paulo, Brazil. Since 2010, CEVA supported Volkswagen's logistics operations, handling warehousing and distribution of automotive parts. PAC, the largest in Latin America, serves over 600 dealers and exports to more than 30 countries, supporting the Volkswagen Group's growth across the region.

October 2023- Kardex delivered a customized, future-proof AutoStore solution to automotive supplier VHIT. This automated storage and retrieval system, designed for the Offanengo site in Italy, would enhance spare parts supply chain efficiency.

July 2022- CEVA Logistics signed a three-year contract to manage critical supply chain operations for Volkswagen's global transmission production at the Córdoba Industrial Center in Argentina. CEVA oversees inbound logistics, parts warehousing, inventory management, and supply to the production line. The Córdoba plant, operational since 1980, manufactures transmissions for various Volkswagen models, including Polo, Tiguan, and Transporter T6.

March 2022- General Motors (GM) awarded CEVA Logistics as a 2021 Supplier of the Year in the Inbound Material Management category at its 30th annual awards ceremony in Phoenix, Arizona. CEVA was recognized for exceeding GM's expectations, contributing to innovative technologies, and maintaining top-quality standards. GM honored a total of 134 global suppliers for their outstanding performance across various categories.

Investment Analysis and Opportunities

The industry of spare parts logistics presents significant investment opportunities driven by increasing vehicle sales, the growth of e-commerce, and rising demand for both OEM and aftermarket parts. Investment in innovative technologies, such as AI, IoT, and automation, is crucial for enhancing inventory management, reducing operational costs, and improving delivery efficiency. Additionally, investments in green logistics, such as electric vehicle fleets and sustainable packaging, are gaining momentum as consumers and governments prioritize environmental concerns. The expanding automotive markets in Asia Pacific and Latin America offer attractive opportunities for regional logistics expansion. Furthermore, companies are also investing in partnerships with OEMs and aftermarket suppliers to optimize the supply chain.

Report Coverage

The global spare parts logistics market report analyzes the market in-depth. It highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, transportation mode, service type, vehicle type, end-use, and spare parts type. Besides this, the market research reports provide insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to market growth over the recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.00% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Transportation Mode

By Service Type

By Vehicle Type

By End-use

By Spare Parts Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market was valued at USD 14.57 billion in 2026 and is anticipated to reach USD 19.95 billion by 2034.

The market will exhibit a CAGR of 4.00% during the forecast period.

In transportation mode, roadways segment leads the market.

E-commerce platform integration, rise in vehicle ownership, and aging vehicles are the key factors that drive the growth of the market.

Key companies such as DHL, Kuehne + Nagel, and DB Schenker, among others, dominate the market.

Europe dominated the global market with a share of 46.07% in 2025.

Key trends in market include digital transformation through AI and IoT, integration with e-commerce, sustainability initiatives, automation, and collaborative supply chain models, driving operational efficiency and supporting market expansion.

The market is expected to grow steadily and reach USD 18.77 billion by 2032, driven by technological advancements such as AI and IoT, the rise of e-commerce, and sustainability initiatives, ensuring efficient, eco-friendly supply chains.

The spare parts logistics market is typically segmented by transportation type (airways, railways, roadways, and waterways), by service type (warehouse services, transportation, inventory management, and administration & supplies), by vehicle type (hatchback/sedan, SUVS, LCVS, AND HCVS), by end-use (OEM parts, and aftermarket parts), by spare parts type (body & structural parts, brake system parts, powertrain components, suspension & steering, engine & cooling, exhaust system, wheels & accessories, others).

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us