Spinal Needles Market Size, Share & Industry Analysis, By Product Type (Pencil-Point Needles, Directional Spinal Needles, Atraumatic Needles, and Others), By Gauge Size (18G to 22G, 23G to 25G, and 26G and Above), By Application (Diagnostics and Therapeutics), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Spinal Needles Market Size and Future Outlook

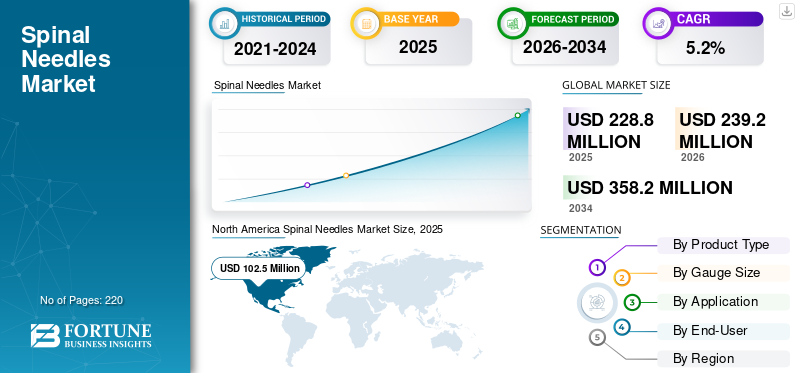

The global spinal needles market size was valued at USD 228.8 million in 2025. The market is projected to grow from USD 239.2 million in 2026 to USD 358.2 million by 2034, exhibiting a CAGR of 5.2% during the forecast period. North America dominated the spinal needles market with a market share of 44.8% in 2025.

The spinal needle is a medical device used for placement of medicines into the lower back area during spinal anesthesia, and for procedures such as lumbar puncture. These needles help doctors deliver fast pain control for surgeries and some diagnostic tests. The market growth is prominently attributed to the growing number of spinal surgeries, especially in older patients who often need orthopedic, urology, and general surgeries. In addition, healthcare professionals also prefer spinal anesthesia in many cases as it can support quicker recovery and lower medicine use after surgery. Moreover, rising emphasis on surgical safety amongst healthcare professionals is also projected to have a positive impact on the market growth.

- For instance, according to Becker’s Spine journal, an estimated 0.34 million spinal surgeries were performed in the U.S. in 2023.

Furthermore, many key industry players, such as B. Braun Melsungen AG, BD, Teleflex Incorporated, Smiths Medical, Inc., and Vygon SAS operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

SPINAL NEEDLES MARKET TRENDS

Preference for Pencil-Point Designs is One of the Important Trend Observed in Market

The market is witnessing considerable demand for pencil-point spinal needles as they are commonly selected for smoother insertion and patient-friendly outcomes in routine practice as well as in anesthesia settings. In addition, a growing number of pencil-point product approvals are also playing a prominent role in encouraging this trend. Furthermore, procurement teams often standardize a few trusted SKUs across departments to simplify training and stocking, which benefits established pencil-point product lines.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Surgical Volumes to Accelerate Market Growth

The growing number of surgical procedures is prominently expected to accelerate the global spinal needles market growth during the forecast period. As the surgical volume increases, it eventually leads to a higher number of spinal anesthesia procedures, and that directly increases spinal needle use. In addition, as populations age, procedures such as joint replacements and other elective surgeries become more common, which raises routine demand in operating rooms.

- For instance, according to a data published by the American College of Rheumatology in February 2026, an estimated 790,000 total knee replacements and 544,000 hip replacements procedures are performed in the U.S per year.

MARKET RESTRAINTS

Strict Quality and Compliance Expectations to Deter Market Growth

Spinal needles are used in sensitive procedures, so hospitals and regulators expect tight quality controls, strong packaging integrity, and consistent performance. Any labeling issue or quality concern can slow purchasing decisions and create extra checks in hospital supply chains. If products need rework, re-labeling, or replacement, it can disrupt routine use and increase administrative burden for providers.

MARKET OPPORTUNITIES

NRFit Conversion and Safer Connections to Offer Lucrative Market Growth Opportunities

A major opportunity is supporting hospitals as they transition to NRFit neuraxial connectors, which aim to reduce the risk of incorrect connections. This shift creates demand not only for compatible spinal needles, but also for complete neuraxial procedure sets that match the safer connector format. In addition, market players that offer conversion support, training, and a full range of NRFit-compatible products are well-positioned to win long-term supply contracts.

- For instance, in July 2024, B. Braun announced the first U.S. hospital conversion to NRFit connectors, signaling that adoption is moving forward and can lead to gradual increase in demand.

MARKET CHALLENGES

Training and Change Management in Hospitals to Pose a Critical Challenge to Market Growth

Even when hospitals want safety upgrades, switching products is not instant. Staff must be trained, old stock must be run down, and new connectors and compatible accessories must be introduced without interrupting daily procedures. In addition, hospitals may also take time to align anesthesia, nursing, procurement, and safety teams on one standard approach. This operational change effort can slow adoption and create temporary parallel usage of old and new systems.

Segmentation Analysis

By Product Type

Consistency in Anesthesia Outcomes Offered by Pencil-Point Needles to Accelerate Segment Growth

Based on the product type, the market is divided into pencil-point needles, directional spinal needles, atraumatic needles, and others.

The pencil-point needles segment is anticipated to account for the largest spinal needles market share. These needles are considerably preferred by many clinicians for routine spinal anesthesia use and for standardization across departments. In addition, healthcare facilities often choose them as a default option to reduce variability, simplify training, and maintain consistent outcomes. Moreover, they are also available across multiple gauge sizes and lengths, making them suitable for different patient needs and common hospital protocols.

The directional spinal needles segment is anticipated to rise with a CAGR of 5.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Gauge Size

Strict Regulations for Class II Devices to Accelerate Segment Growth

Based on gauge size, the market is segmented into 18G to 22G, 23G to 25G, and 26G and above.

In 2025, the 23G to 25G segment dominated the global market. 23G to 25G spinal needles are widely used as they balance clinician handling with routine procedural needs in many adult cases. Hospitals prefer to stock commonly used gauges to avoid complexity in inventory and to keep anesthesia carts consistent across operating rooms. These gauge sizes also align with standard purchasing patterns where supply teams prefer fewer SKUs with reliable availability.

The 26G and above segment is anticipated to rise with a CAGR of 6.1% over the forecast period.

By Application

Higher Volume of Anesthesia Procedures to Boost Therapeutic Application Segment Growth

Based on application, the market is bifurcated into diagnostics and therapeutics.

In 2025, the therapeutics segment dominated the global market. Therapeutics use drives a large share as spinal anesthesia is a routine method to support surgical pain control, especially in high-volume procedures. Compared to purely diagnostic use, therapeutic procedures happen daily in hospitals and ASCs, creating repeat demand for single-use spinal needles. In addition, providers also value dependable supply for scheduled surgery lists, which keeps consumption steady over the year.

The diagnostic segment is anticipated to rise with a CAGR of 3.6% over the forecast period.

By End-User

Higher Number of Neuraxial Procedures in Hospitals & ASCs to Accelerate Segment Growth

Based on end-user, the market is segmented into hospitals and ASCs, specialty clinics, and others.

In 2025, hospitals and ASCs held the highest market share. Hospitals and ASCs account for most demand as they perform the majority of surgeries requiring spinal anesthesia and related neuraxial procedures. They also buy through standardized procurement systems, which favors high-volume, repeat purchasing. Hospitals typically keep multiple procedure areas running every day, so spinal needle consumption is steady and predictable. In addition, safety-driven conversions often start in larger health systems that can run formal implementation programs. Furthermore, the segment is set to hold 77.4% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 5.6% during the study period.

Spinal Needles Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Spinal Needles Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 98.4 million, and also maintained the leading share in 2025, with USD 102.5 million. The market in North America is expected to increase due to higher volume of surgical procedures, and growing number of product launches.

U.S. Spinal Needles Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 91.6 million in 2026, accounting for roughly 38.3% of global sales.

Europe

Europe is projected to record a growth rate of 4.7% in the coming years, and reach a valuation of USD 64.6 million by 2026. The region is estimated to witness considerable market growth due to rising investments for new product development, and growing number of spinal surgeries.

U.K. Spinal Needles Market

The market size of the U.K. in 2026 is estimated at around USD 10.7 million, representing roughly 4.5% of global revenues.

Germany Spinal Needles Market

Germany’s market size is projected to reach approximately USD 14.7 million in 2026, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 49.6 million in 2026 and secure the position of the third-largest region in the market.

Japan Spinal Needles Market

The Japan market size in 2026 is estimated at around USD 8.7 million, accounting for roughly 3.7% of global revenues.

China Spinal Needles Market

China’s market size is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 16.6 million, representing roughly 6.9% of global sales.

India Spinal Needles Market

The Indian market value in 2026 is estimated at around USD 11.2 million, accounting for roughly 4.7% of global revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 12.7 million in 2026. In the Middle East & Africa, the GCC is set to reach a value of USD 2.0 million in 2026.

South Africa Spinal Needles Market

The South Africa market is projected to reach around USD 0.8 million in 2026, representing roughly 0.35% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansion Along with New Product Launches by Key Players to Boost Market Progress

The global spinal needles market is moderately consolidated, with key companies such as B. Braun Melsungen AG, BD, Teleflex Incorporated, Smiths Medical, Inc., and Vygon SAS playing a major role. Their strong market presence is driven by strategic initiatives such as expanding production capacity and launching technologically advanced products.

- For example, in January 2025, BD (Becton, Dickinson and Company) announced plans to expand its production line for critical medical devices in the U.S.

Other important participants in the global market include Sarstedt AG & Co. KG, Pajunk GmbH Medizintechnologie, Argon Medical Devices, Inc., Merit Medical Systems, Inc., Romsons Scientific & Surgical Pvt. Ltd. These companies are expected to focus on collaborations and partnerships to strengthen their global market share during the study period.

LIST OF KEY SPINAL NEEDLES COMPANIES PROFILED

- Braun Melsungen AG (Germany)

- BD (U.S.)

- Teleflex Incorporated (U.S.)

- Smiths Medical, Inc. (U.S.)

- Vygon SAS (France)

- Sarstedt AG & Co. KG (Germany)

- Pajunk GmbH Medizintechnologie (Germany)

- Argon Medical Devices, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Romsons Scientific & Surgical Pvt. Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- December 2025: RIVANNA received FDA approval for its Accuro 3S Needle Guide Kit. The newly launched product is specifically designed for safety and effectiveness of ultrasound-guided needle placement.

- September 2025: Ruthless Spine received FDA approval for its NavJam Jamshidi device. The new device assists in spinal screw placement with safe and effective outcomes.

- June 2023: SingHealth is planning to introduce an AI-based tool for precise spinal anesthesia. Currently, the technology is in pilot phase and operating in KK Women’s and Children’s Hospital.

- July 2022: Global Medikit Limited received FDA approval for its Medispine and Glospine spinal needle.

- January 2022: ICU Medical completed acquisition of Smiths Medical, a business unit of Smiths Medical Group plc. The strategic step was taken to consolidate its position in the syringe and ambulatory infusion devices, vascular access, and vital care products.

REPORT COVERAGE

The global spinal needles market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.2% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product Type, Gauge Size, Application, End-User, and Region |

| By Product Type |

|

| By Gauge Size |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 228.8 million in 2025 and is projected to reach USD 358.2 million by 2034.

In 2025, the market value stood at USD 102.5 million.

The market is expected to exhibit a CAGR of 5.2% during the forecast period.

By product type, the pencil-point needles segment is expected to lead the market.

The rising number of spinal procedures and increasing investment for new product developments are driving market expansion.

B. Braun Melsungen AG, BD, Teleflex Incorporated, Smiths Medical, Inc., and Vygon SAS are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us