Spinal Fusion Devices Market Size, Share & Industry Analysis, By Product Type (Cervical Devices, Thoracolumbar Devices, Interbody Devices, and Biologics), By Disease Indication (Degenerative Disc Disease, Complex Deformity, Traumas & Fractures, and Others), By End User (Hospitals & Ambulatory Surgery Centers, Specialty Clinics and Others) and Regional Forecast, 2026-2034

Spinal Fusion Devices Market Size & Industry Overview

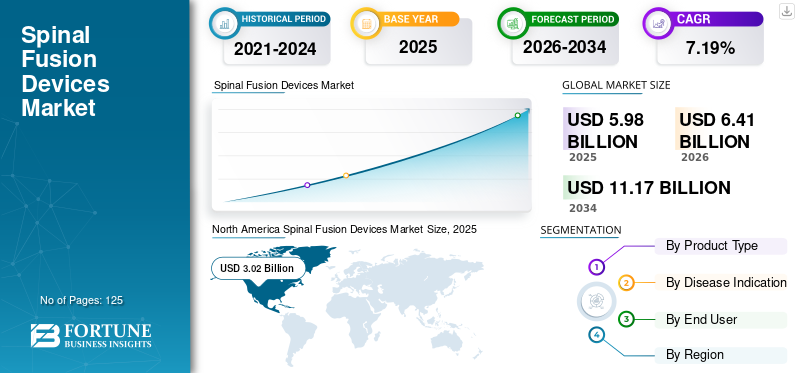

The global spinal fusion devices market size was valued at USD 5.98 billion in 2025. The market is projected to grow from USD 6.41 billion in 2026 to USD 11.17 billion by 2034, exhibiting a CAGR of 7.19% during the forecast period. North America dominated the spinal fusion devices market with a market share of 47.41% in 2025.

The number of spine fusion surgeries has gradually increased in recent years. Spinal fusion, also called as spinal arthrodesis, is a type of surgical procedure used to fuse two or more vertebral bodies in the vertebral column. Spinal fusion procedure is performed for the treatment of degenerative disc disease, abnormal spinal curvatures, spondylolisthesis, and others. Rising geriatric population and increase in number of spinal injuries have resulted in increasing the volume of spinal fusion procedures.

According to the Australian Bureau of Statistics 2017–18 National Health, approximately 16% of the population in Australia have back problems, which account for 4.0 Million people. This is projected to augment the market during the forecast period.

Spine fusion devices consist of cervical fixation devices, thoracolumbar fixation devices, interbody devices, and biologics. Rising demand for cervical and thoracolumbar devices and developments in interbody devices are the primary reasons which are poised to surge the market. In October 2019, Stryker received 510 (k) approval from the FDA for SAHARA Lateral 3D Expandable Interbody System, a 3D printed spine fusion implant. This is expected to positively impact the worldwide market for spinal arthrodesis devices.

Various technologies are being incorporated by major key manufacturers which is positively impacting the demand for spinal arthrodesis devices. Robotic-assisted spinal fusion surgery and minimally invasive spine fusion devices are emerging as game-changers for patients having spine diseases. Apart from this, increased research on biologics, especially Bone Morphogenetic Proteins (BMPs), is expected to favor the adoption of the spinal fusion implants.

Download Free sample to learn more about this report.

Spinal Fusion Devices Market Key Takeaways

- 2025 Market Size: USD 5.98 Billion

- 2026 Market Size: USD 6.41 Billion

- 2034 Forecast Market Size: USD 11.17 Billion

- CAGR: 7.19% from 2026–2034

- North America dominated the spinal fusion devices market with a market share of 47.41% in 2025.

- The thoracolumbar devices segment is estimated to hold a maximum share in the market.

- The hospitals & ambulatory surgery centers segment is estimated to dominate the market throughout the forecast period.

North America

North America generated a revenue of USD 3.02 Billion in 2025 and is projected to dominate the global spinal fusion devices market share throughout the forecast period.

Europe

In Europe, the market is expected to expand due to favorable health reimbursement, high demand for 3D printed medical devices in Germany and the U.K., and a gradual shift towards minimally invasive surgeries.

Asia Pacific

The region is expected to witness strong growth owing to improving reimbursement policies, increasing cases of degenerative spine disorders, and expanding healthcare infrastructure across emerging economies.

U.S.

The growing prevalence of chronic pain and increasing demand for advanced spinal fusion procedures are expected to drive market expansion throughout the forecast period.

Japan

Rising adoption of minimally invasive spine surgery technologies, coupled with an aging population and increasing incidence of degenerative spinal disorders, is expected to support steady market growth.

Read More

MARKET DRIVERS

“Emergence of Robotic Spine Fusion Surgeries to Fuel the Market”

Adoption of surgical robots in the spine industry is gradually increasing, with many hospitals offering robotic surgery for the treatment of various spinal diseases. Many manufacturers are focusing on developing surgical robots that can be used in spinal fusion surgeries along with the company’s implants and navigation tools. This has paved the way for many strategic collaborations and new product launches which is expected to drive the growth of the market.

In January 2019, Medtronic announced the launch of Mazor X Stealth Edition, a robotic system for spine surgery. The system can be used with the company’s spine implants, navigation and 3D imaging tools, providing a comprehensive solution to the healthcare professionals. Deeper penetration of such robotic system is expected to boost the spinal fusion devices market growth during the forecast period.

“New Product Launches to Drive the Adoption of Spine Fusion Devices”

The market for spinal arthrodesis devices is highly competitive, with key players constantly introducing new and advanced products in the market to maintain their position. Furthermore, minimally invasive surgeries are witnessing remarkable traction worldwide, compelling the players to launch devices especially for minimally invasive spinal fusion surgeries. For example, in July 2019, Alphatec Spine announced the commercial launch of InVictus, a spinal fixation platform designed for open, minimally invasive, or hybrid surgical procedures. Such innovations are anticipated to steer the spinal fusion devices market trends.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type Analysis

“Rising Prevalence of Lumbar Spine Degeneration to Boost the Thoracolumbar Devices Segment”

Based on product type, the market can be segmented into cervical devices, thoracolumbar devices, interbody devices, and biologics. The thoracolumbar devices segment is estimated to hold a maximum share in the market in 2018. Increasing availability of a variety of thoracolumbar fixation devices and rising prevalence of lumbar spine degeneration are the major factors attributed to the growth of this segment.

The cervical devices segment is anticipated to propel owing to the rapid adoption of spine navigation software and favorable health insurance coverage. Rapid adoption of expandable interbody devices and increasing demand for interbody spacer devices are the primary reasons attributable to the expansion of the interbody devices segment. Also, the launch of IdentiTi, an interbody implant system made of titanium for anterior lumbar interbody fusion procedures in July 2019 by Alphatec Spine is anticipated to foster the demand for interbody devices.

To know how our report can help streamline your business, Speak to Analyst

The biologics segment is anticipated to expand owing to the increased usage of demineralized bone matrix (DBM) and synthetic graft for spinal fusion.

By Disease Indication Analysis

“Degenerative Disc Disease Segment to Dominate the Market”

In terms of disease indication, the market is categorized into degenerative disc disease, complex deformity, traumas & fractures, and others. The degenerative disc disease is estimated to dominate the market throughout the forecast period. Spine fusion surgery has emerged as the standard treatment for degenerative disc disease, which is an important factor contributing to the expansion of the segment, says the spinal fusion devices market analysis.

The complex deformity segment is likely to propel owing to the significant increase in the number of births with deformities and active government support for awareness regarding the correction of deformities. The rising number of cases of spinal injuries and fractures, favorable reimbursement, and demand for minimally invasive surgeries are poised to surge the traumas & fractures and others segments during 2019-2026.

By End User Analysis

“Favorable Health Reimbursement to Drive the Growth of Hospitals & ASCs Segment”

On the basis of the end user, the market is classified into hospitals & ambulatory surgery centers, specialty clinics, and others. The hospitals & ambulatory surgery centers segment is estimated to dominate the market throughout the forecast period due to the rapid adoption of advanced spine surgery products and gradual rise in number of robotic spine surgery.

Also, spinal fusion procedures in ambulatory surgery centers are resulting in significant cost saving, which is projected to further propel the segment. According to an article published in Neurosurgery, spinal surgery in ambulatory surgery centers can result in saving USD 140 Million annually.

The specialty clinics segment is projected to witness remarkable growth during 2019-2026 owing to the gradual shift towards minimally invasive spine fusion procedures and increase in the number of spine surgeons. The others segment is anticipated to expand owing to the increased research on biologics and the use of artificial grafts for bone healing.

REGIONAL ANALYSIS

North America

North America Spinal Fusion Devices Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

North America generated a revenue of USD 3.02 Billion in 2025 and is projected to dominate the global spinal fusion devices market share throughout the forecast period. Significant rise in the number of spinal fusion procedures in ambulatory surgical centers and outpatient settings, rapid adoption of spine navigation tools, and surgical robots are factors that are expected to fuel the market in North America. According to the Centers for Disease Control and Prevention, over 20.4% of the U.S. adults were suffering from chronic pain and 8.0% of the U.S. adults had high-impact chronic pain in 2016. This is expected to augment the demand for spine fusion implants in the U.S during the forecast period.

Europe

In Europe, the market is expected to expand due to the favorable health reimbursement, high demand for 3D printed medical devices in Germany and the U.K, and gradual shift towards minimally invasive surgeries. Furthermore, increased government investment in biologics and spinal fusion implants is anticipated to accelerate the growth of the market in Europe.

Asia Pacific

In Asia Pacific, the demand for spinal arthrodesis devices is poised to surge during the forecast duration due to the improving reimbursement policies for spine surgeries and the increasing prevalence of degenerative diseases and spine fractures. In September 2019, the Australian Government announced changes in the Medicare Benefits Schedule (MBS) items for spine procedures which will provide appropriate reimbursement to the patients undergoing spinal surgery. This is expected to further fuel the market in Asia Pacific. Improving healthcare infrastructure, gradual shift towards minimally invasive spine solutions, and expansion of distribution network of key players in developing nations are primary factors augmenting the market in Latin America and the Middle East and Africa.

INDUSTRY KEY PLAYERS

“K2M Acquisition to Strengthen Stryker Market Position”

Medtronic accounted for the largest market share in the market mainly due to the company’s strong focus for core spine products and established distribution networks. The acquisition of Mazor Robotics and the launch of Mazor X Stealth Edition system to be used with the company’s spinal implants has positively impacted the company’s revenue. DePuy Synthes and Stryker also have a leading position in the worldwide market of spine arthrodesis devices. The market share of Stryker is estimated to increase in the forthcoming years owing to the acquisition of K2M in November 2018.

List Of Key Companies Covered:

- Medtronic

- Stryker

- Zimmer Biomet

- DePuy Synthes (Johnson & Johnson Services, Inc.)

- NuVasive, Inc

- RTI Surgical Holdings, Inc.

- Aesculap, Inc. (B. Braun Melsungen AG)

- Alphatec Spine, Inc.

KEY INDUSTRY DEVELOPMENTS:

- Integrity Implants Inc. and Fusion Robotics, LLC, announced that they have completed a merger and rebranded to increase the adoption of minimally invasive surgery for spinal care.

- Royal Biologics announced the completion of the acquisition of FIBRINET. This acquisition will create a strategic initiative to feature novel technologies to grow its portfolio of autologous and live cellular solutions to support orthopedic and spinal fusion. This system uses the patient's autologous blood to create a platelet-rich fibrin membrane (PRFM) and PRFM to help increase spinal fusions and provide surgeons with a new and novel biologic option.

- Zavation Medical announced the launch of the expandable anterior lumbar and lateral lumbar plates, designed to use the lumbar spine as supplemental fixation devices. These plates are add-ons to the company’s portfolio.

- WishBone Medical Inc. announced the acquisition of all Back 2 Basics Direct (B2B) and Orbbo Surgical assets. These two privately held medical device companies focus on research, development, and surgical instruments for spinal fusion. These acquisitions will augment the company's position within the pediatric orthopedic market, sterile packaged, spinal fusion product lines with greater revenues.

REPORT COVERAGE

Rising prevalence of cervical and lumbar disc degeneration and a gradual shift toward minimally invasive procedures has fueled the market. With the advent of robotic assisted spine surgery and spine navigation platforms, the demand for spine fusion devices is expected to increase drastically during the forecast horizon. The report provides qualitative and quantitative insights on the spinal fusion devices market trends and detailed analysis of the size & growth rate for all possible segments in the market.

Along with this, the report provides a detailed analysis of the dynamics and competitive landscape. Various key insights provided in the report include the prevalence of spinal diseases for key countries, the regulatory scenario for key countries, reimbursement scenario for key countries, new product launches, key industry developments such as mergers, acquisitions and partnerships, key industry trends, and company profiles.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Disease Indication

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

The value of the spinal fusion devices market was USD 5.98 Billion in 2025.

Fortune Business Insights says that the spinal fusion devices market is projected to reach USD 11.17 Billion by 2034.

The value of North America spinal fusion devices market was USD 3.02 Billion in 2025.

The spinal fusion devices market is projected to grow at a CAGR of 7.19% during the forecast period (2021-2034).

The thoracolumbar devices segment is the leading segment in this market during the forecast period.

Emergence of robotic spine fusion surgeries and new product launches are the key factors driving the spinal fusion implants market.

Medtronic, DePuy Synthes, and Stryker are the top players in the market.

North America is expected to hold the highest market share in the market.

Launch of 3D printed spinal fusion implants, use of spine navigation tools, and rapid adoption of robotic assisted spine fusion surgery are the key trends of the spinal fusion devices market.

- 2021-2034

- 2025

- 2021-2024

- 125

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us