Orthopedic Joint Replacement Market Size, Share & Industry Analysis, By Product (Knee, Hip, Shoulder, Ankle, and Others), By Procedure (Total, Partial, and Others), By End user (Hospitals & ASCs, Orthopedic Clinics, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

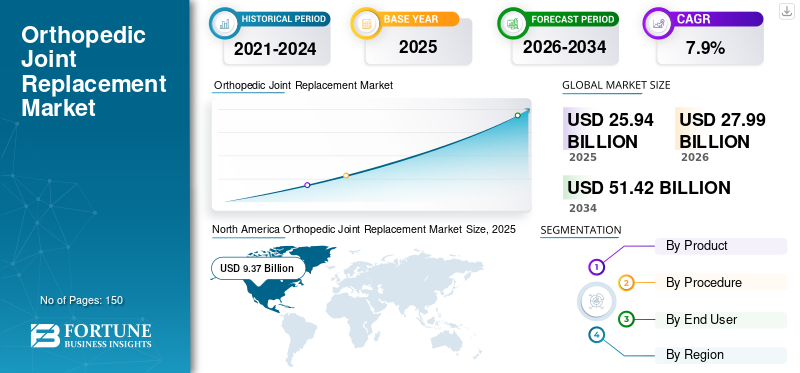

The global orthopedic joint replacement market size was estimated at USD 25.94 billion in 2025. The market is expected to rise from USD 27.99 billion in 2026 to USD 51.42 billion by 2034, expanding at a CAGR of 7.90% from 2026 to 2034. North America dominated the orthopedic joint replacement market with a market share of 36.13% in 2025.

Osteoarthritis is one of the most prevalent diseases among the geriatric population. Joint replacement has emerged as the most popular option for the treatment of osteoarthritis, which has resulted in a wider acceptance of joint implants among patients. A notable rise in the geriatric population is supplementing the orthopedic joint replacement market growth due to the increasing incidence of hip fractures in the elderly population. According to an article published in Agappe in November 2022, 260,000 to 300,000 individuals are estimated to be hospitalized each year for hip fractures in the U.S. By 2040, the number is estimated to reach 500,000.

With the introduction of robotic surgery and patient-specific 3D printed implants, the demand for orthopedic joint replacement implants has drastically increased, which is further augmented by support from regulatory bodies. For instance, in April 2023, Moximed received the marketing approval for its MISHA Knee System. This product is aimed at helping people effectively manage knee osteoarthritis. The market is also being favored by active government support and patient-friendly health reimbursement policies.

Download Free sample to learn more about this report.

Orthopedic Joint Replacement Market Key Takeaways

- 2025 Market Size: USD 25.94 billion

- 2026 Market Size: USD 27.99 billion

- 2034 Forecast Market Size: USD 51.42 billion

- CAGR: 7.90% (2026–2034)

- North America dominated the market with a 36.13% share in 2025.

- The knee segment is projected to lead the market with a 43.0% share in 2026.

- The partial replacement segment is anticipated to register a remarkable CAGR during the forecast period.

Asia Pacific

Asia Pacific is projected to register the highest CAGR during the forecast period, supported by a large patient pool.

North America

North America generated USD 9.37 billion in 2025 and is projected to reach USD 10.11 billion in 2026.

Europe

Europe is expected to witness steady growth, driven by the increasing prevalence of osteoarthritis, rising demand for orthopedic implants.

U.S.

U.S. market is projected to witness steady growth during the forecast period.

Japan

Japan is likely to witness sustained growth during the forecast period.

Read More

COVID-19 IMPACT

Decline in Orthopedic Surgeries amid COVID-19 Hindered Market Growth

Declines, delays, or cancellations in elective surgeries, such as those for orthopedic joint replacement had a huge impact on the global market growth. According to the CJRR Annual Report 2020-2021, the number of knee and hip replacement surgeries in Canada decreased by 26.4% and 12.9% respectively during 2020-21. This was mainly due to the cancellation of planned surgeries owing to COVID-19 related restrictions.

Moreover, according to GlobalSurg, the estimated volume of normal elective orthopedic surgeries during March 2020 – May 2020 should have been around 7.7 million. However, the pandemic led to an 82% cancellation of these surgeries during the peak period. Additionally, the U.K.’s National Health Service (NHS) had directed all hospitals in England to postpone non-urgent elective procedures for 3 months starting from April 15.

Due to the COVID-induced lockdowns, the pharma sector witnessed disruptions in supply chains due to the limitations on imports & exports, closure of flights, reduced production, and disturbed supply channels. The market was anticipated to witness a surge in 2021, and is expected to grow steadily during the forecast period.

ORTHOPEDIC JOINT REPLACEMENT MARKET TRENDS

Increasing Adoption of Online Tools to Gain Orthopedic Knowledge Will Open New Market Growth Avenues

With the rapid proliferation of the internet, patients have been referring to web-based tools and online resources to obtain information about specific diseases. Orthopedic joint replacement is one such area witnessing the introduction of a number of online tools guiding patients through their surgeries, connecting with the orthopedic surgeons, and providing post-surgery rehabilitation information.

- For instance, in January 2021, Ortoma AB introduced an Artificial Intelligence-based software platform to help in implant procedures by improving surgery accuracy. The product received approvals from both the U.S. and Europe.

Download Free sample to learn more about this report.

ORTHOPEDIC JOINT REPLACEMENT MARKET GROWTH FACTORS

Technological Innovations in Orthopedic Implants to Augment Market Growth

The market growth is expected to get a boost in the form of increasing demand for customized joint implants for both males and females. Since each patient has a unique anatomy, the concept of “one size fits all” is not applicable, and hence major medical device companies are striving to leverage advanced technologies to manufacture patient-specific orthopedic implants. For instance, in November 2022, ConforMIS Inc. introduced Imprint Knee System in the U.S. With this, the company also introduced a “Made-to-Measure” product category option for Total Knee Arthroplasty (TKA).

Furthermore, the introduction of 3D printing technology to manufacture orthopedic implants has resulted in a huge surge in demand for customized implants. Many orthopedic device companies are developing cutting-edge technologies that can be used to supply advanced joint implants, which is likely to favor the market growth during the projected timeframe.

Advancements in Robotic Surgeries to Boost Demand for Joint Replacement Devices

The adoption of surgical robots in the field of orthopedics has increased the efficiency of surgical procedures and thus, many hospitals are now offering robotic surgeries for the treatment of various orthopedic diseases. Several manufacturers are focusing on developing surgical robots that can be used in spinal fusion surgeries along with the company’s implants and navigation tools.

For instance, in November 2021, Smith+Nephew introduced CORI handheld robotics to assist in both total and partial knee arthroplasties. This advanced system is designed to enhance the skill sets of the orthopedic team. Additionally, in January 2019, Medtronic announced the launch of Mazor X Stealth Edition, a robotic system for spine surgery. The system can be used with the company’s spinal implants and navigation & 3D imaging tools, providing a comprehensive solution to healthcare professionals.

RESTRAINING FACTORS

Product Recalls and Lawsuits on Orthopedic Devices to Hamper Market Growth

The volume of orthopedic joint replacement surgeries is increasing exponentially. However, complications associated with the use of the implants are a major factor that is anticipated to hamper the growth of the market in the coming years.

Additionally, product recalls of knee and hip replacement devices by major players around the globe are also estimated to hinder the growth of the market. According to the U.S. Food and Drug Administration (FDA), from 2003 to 2019 there were more than 13,000 recalls of knee replacement components and systems. The highest number of recalls was recorded by Zimmer Biomet, followed by Johnson and Johnson Services Inc., and Smith & Nephew.

SEGMENTATION ANALYSIS

By Product Analysis

Knee Segment to Hold Dominating Position Owing to High Number of Procedures

On the basis of product, the market is categorized into knee, hip, shoulder, ankle, and others. The knee segment dominated the orthopedic joint replacement market share of 43.0% in 2026. Increase in the number of knee replacement procedures, which include total knee replacement procedures, robot-assisted knee replacement surgeries, and launch of products, such as ATTUNE Revision Knee System, Persona Partial Knee System, JOURNEY II XR Total Knee by key manufacturers are the factors responsible for the strong growth of the knee segment during the forecast period. For instance, in January 2022, Symbios Orthopédie S.A. launched the ORIGIN CR Total Knee System. This system allows surgeons to proceed with custom-made knee replacement surgery preserving the Posterior Cruciate Ligament (PCL).

To know how our report can help streamline your business, Speak to Analyst

Furthermore, the rapidly increasing prevalence of chronic knee-related diseases has boosted the number of knee replacement surgeries being performed across the world. For instance, according to the American Joint Replacement Registry 2022 Annual Report, the number of knee arthroplasty procedures between 2012 and 2021 had reached 1,495,965.

The shoulder segment is projected to register a strong growth rate owing to the shifting focus of manufacturers toward shoulder implants. Also, rapid increase in the number of shoulder replacement surgeries performed globally is anticipated to boost the sales of shoulder implants during the forecast period. For instance, according to a study published in the NCBI in November 2021, the number of primary shoulder replacement surgeries was estimated to grow significantly in the coming years, reaching at least 37,000 procedures per year.

By Procedure Analysis

Total Replacement Captured Majority Market Share Owing to High Number of Product Offerings

In terms of procedure, the market is categorized into total replacement, partial replacement, and others. The total replacement segment accounted for the maximum market share in 2022 owing to a higher number of product offerings for total orthopedic joint replacement procedures as compared to that for partial, reverse, or revision replacement.

The partial replacement segment is anticipated to report a remarkable CAGR, which can be attributed to the increased preference for partial replacement over total replacement among patients and healthcare providers.

By End User Analysis

High Procedure Volume in Hospitals & ASCs Resulted in Segment’s Dominance in the Market

On the basis of end user, the market has been segmented into hospitals & ASCs, orthopedic clinics, and others. Among these, the hospital & ASC segment dominated the global market in 2022. Factors, such as the growing number of hip implant surgeries within these facilities are contributing to the segment’s growth. Hospitals are generally equipped with the latest technologies and skilled healthcare professionals, which is further boosting the segment’s growth. For instance, in October 2023, Apollo Institute of Orthopedics completed 370 robotic knee replacement procedures over a period of 10 months since the launch of these surgeries in January 2022.

Furthermore, collaborations between hospitals and industry players to create advanced surgical procedures are also fostering the segment’s growth. According to the American Joint Replacement Registry’s 2021 annual report, the total number of joint replacement surgeries in ASCs increased by 55% in 2020. Such data indicates an increasing number of joint replacement surgeries being performed in ASCs.

The orthopedic clinics segment is also anticipated to register a considerable CAGR throughout the forecast period. This is attributed to the increasing number of orthopedic clinics in areas where access to medical facilities is limited.

REGIONAL ANALYSIS

North America

North America Orthopedic Joint Replacement Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a valuation of USD 9.37 billion in 2025 and USD 10.11 billion in 2026. Factors, such as growing awareness among the patient population regarding technologically advanced orthopedic implants and new treatment options available in the region are responsible for the region’s dominance in the global market. Furthermore, the increasing demand for hip replacement surgeries in the U.S. is contributing to the regional market growth. For example, according to the Agency for Healthcare Research and Quality, more than 450,000 total hip replacement procedures are performed each year in the U.S.

Europe

The growth of the market in Europe is attributed to the increasing prevalence of osteoarthritis, growing demand for orthopedic joint replacement implants, and rising day-care surgeries. For instance, according to an article published by NICE in October 2022, about 18% of the U.K. population aged over 45 years had sought treatment for knee-related osteoarthritis. This shows high prevalence of the disease in the country. Furthermore, an increase in healthcare expenditure by the European Commission is anticipated to fuel the growth of the market in the region.

Asia Pacific

The market in Asia Pacific is expected to record the highest CAGR during the forecast duration. Factors, such as a large patient pool and growing healthcare spending are supplementing the market growth in Asia Pacific. Moreover, increasing adoption of advanced products supplemented the market growth. For instance, in February 2023, Criticare Asia Hospital in Mumbai, India successfully completed the first partial knee replacement surgery using fully automated robotic arm technology.

Technological advancements, expansion of distribution networks of key players in emerging economies, and increasing healthcare spending are some of the primary factors augmenting the market growth in Latin America and the Middle East & Africa.

KEY INDUSTRY PLAYERS

Consolidated Market Structure to Enable Few Key Players to Hold Dominant Position

Zimmer Biomet, Stryker, Johnson & Johnson Services, Inc., and Smith & Nephew are the prominent players in the market and captured a considerable share of the global market in 2022. The dominance of these players can be attributed to their diversified portfolios of joint implants for both upper and lower extremities. These companies are actively engaged in new product launches to maintain their market dominance. For instance, in March 2023, Smith + Nephew showcased its Orthopedics Arthroplasty portfolio at the AAOS 2023 Annual Meeting. The company unveiled a franchise-level value proposition named “Precision in Motion” for its robust portfolio.

Furthermore, Johnson & Johnson Services, Inc. and Stryker, together with their knee and hip implant portfolios, hold a major position in the market. Other players operating in the market are B. Braun Melsungen AG, Bioimpianti, Conformis, MicroPort Scientific Corporation, and other players.

LIST OF KEY COMPANIES IN ORTHOPEDIC JOINT REPLACEMENT MARKET:

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Smith + Nephew (U.K.)

- Zimmer Biomet (U.S.)

- B. Braun Melsungen AG (Germany)

- Bioimpianti (Italy)

- Conformis (U.S.)

- MicroPort Scientific Corporation (China)

- Enovis (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2025 – Showcase of Next-Generation Mako SmartRobotics™

Stryker unveiled advancements in its Mako SmartRobotics™ system at the AAOS 2025 Annual Meeting, highlighting enhancements across hip, knee, spine, and shoulder procedures.

- March 2025 – $55 Billion U.S. Investment Over Four Years

Johnson & Johnson announced plans to invest over $55 billion in the U.S. over the next four years, including the construction of four new manufacturing facilities, starting with a $2 billion+ facility in North Carolina.

- March 2025 – Highlighting Breakthrough Sports Medicine Technologies

At AAOS 2025, Smith+Nephew showcased advanced sports medicine technologies, including the REGENETEN® Bioinductive Implant and the CORI® Surgical System, emphasizing innovations in joint repair. - August 2024 – 510(k) Clearance for CATALYSTEM Primary Hip System

The company received FDA 510(k) clearance for its CATALYSTEM Primary Hip System, designed to meet the evolving demands of primary hip surgery, with a commercial launch planned for the second half of 2024.

- 2025 – Cutting Edge in Hip & Knee Symposium

Zimmer Biomet announced its 2025 Cutting Edge Symposium, focusing on the future of orthopedic care with sessions on Total Knee Arthroplasty and Total Hip Arthroplasty, aiming to redefine medical education in musculoskeletal health.

- September 2024 – Introduction of Next-Generation Foot and Ankle Surgery Offerings

Enovis unveiled its Tarsoplasty Percutaneous Lapidus System and demonstrated the Better Step patient-focused platform at the AOFAS Annual Meeting, aiming to enhance surgical efficiency and patient outcomes in foot and ankle procedures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The market report provides qualitative and quantitative insights on the joint replacement industry and a detailed analysis of the market size and growth rate for all possible segments. Along with this, the report provides an elaborative analysis of the market dynamics and competitive landscape. Various key insights provided in the report are the number of joint replacement procedures performed in key countries, new product launches, regulatory scenario & overview of reimbursement policies in key countries, recent industry developments, such as mergers & acquisitions, and key industry trends.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.9% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product

|

|

By Procedure

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global orthopedic joint replacement market size stood at USD 27.99 billion in 2026 and is projected to reach USD 51.42 billion by 2034. Increasing number of total orthopedic replacement procedures among patients, growing launches for innovative orthopedic implants are some of the factors contributing to the growth of the market.

In 2025, the market value stood at USD 25.94 billion.

The market will exhibit a steady CAGR of 7.9% during the forecast period of 2026-2034.

The knee replacement segment is expected to be the leading segment in this market.

Technological innovations in orthopedic implants is a major factor driving the growth of the market.

Zimmer Biomet, Johnson and Johnson Services, Inc., and Stryker are the major players in the global market.

North America dominated the orthopedic joint replacement market with a market share of 36.13% in 2025.

Improvements in robotic surgeries are expected to drive the adoption of these devices.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us