Steel Billet Market Size, Share & Industry Analysis, By Type (Carbon Steel Billet, Alloy Steel Billet, and Stainless / Special Steel Billet), By Application (Construction, Wire Products, Engineering, Merchant Bars and Others), and Regional Forecast, 2026-2034

STEEL BILLET MARKET SIZE AND FUTURE OUTLOOK

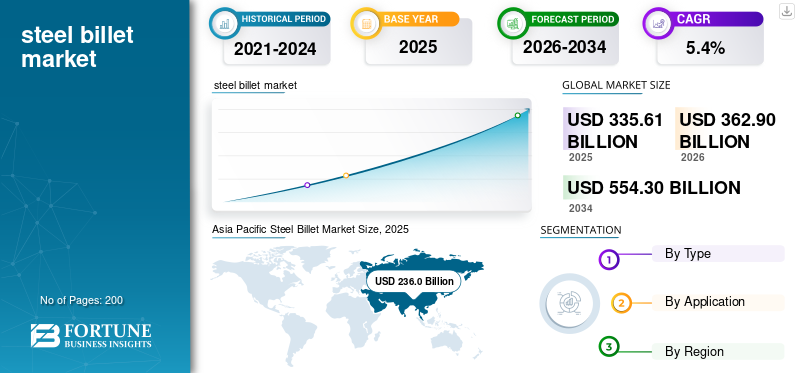

The steel billet market size was valued at USD 335.61 billion in 2025. The market is projected to grow from USD 362.90 billion in 2026 to USD 554.30 billion by 2034 at a CAGR of 5.4% during the forecast period. Asia Pacific dominated the steel billet market with a market share of 70.31% in 2025.

Steel billets are semi-finished steel products typically cast into square or rectangular cross-sections and used as raw materials for rolling mills. They are produced through continuous casting or ingot casting processes and serve as feedstock for manufacturing long steel products such as rebar, wire rods, merchant bars, and structural sections. Steel billets are categorized into carbon steel, alloy steel, and stainless or special steel billet based on composition and performance characteristics.

Carbon steel billets hold the leading share due to their extensive use in construction and general engineering applications. Rapid urbanization, infrastructure development and industrial expansion are key factors driving the product demand globally. Additionally, increasing investments in transportation, energy, and housing projects further stimulate consumption.

As global steel demand remains closely tied to economic growth and infrastructure spending, steel billet continue to play a critical role in the steel value chain, thus reinforcing market stability. The major key players operating in the market are ArcelorMittal S.A., China Baowu Steel Group Corporation Limited, Nippon Steel Corporation, and POSCO Holdings Inc.

Download Free sample to learn more about this report.

STEEL BILLET MARKET TRENDS

Investments and Capacity Modernization are Reshaping Production Patterns

The market is evolving due to rising infrastructure investments and modernization of steel production facilities. A key trend is the shift toward Electric Arc Furnace (EAF) technology, which enhances energy efficiency and reduces carbon emissions compared to traditional blast furnace routes. Additionally, increasing adoption of continuous casting technologies improves billet quality and reduces production costs. Developing economies are expanding domestic billet production capacity to reduce import dependence. Trade protection measures in various regions are also influencing global billet trade flows. Furthermore, growing demand for high-strength and corrosion-resistant steel grades is promoting alloy and special steel billet production. These structural changes in production technology and policy frameworks are reshaping market dynamics, thus influencing long-term growth patterns in the market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Construction Activity and Manufacturing Output Drives Market Expansion

The primary driver of the steel billet market growth is strong construction activity worldwide. Billets serve as essential raw materials for reinforcing bars and structural steel products used in residential, commercial, and infrastructure projects. Growing investments in highways, bridges, railways, and urban housing support steady demand. Additionally, expansion of industrial manufacturing and automotive production increases usage of billet-derived products. Government stimulus programs and infrastructure funding initiatives further strengthen market fundamentals. Rising steel consumption in emerging markets plays a crucial role in sustaining global demand. These construction and manufacturing-driven factors ensure consistent billet consumption, thus maintaining stable market growth.

MARKET RESTRAINTS

Raw Material Price Volatility and Trade Restrictions are Limiting Profit Margins

The market faces restraints primarily due to volatility in raw material prices such as iron ore and scrap metal. Fluctuations in energy costs and transportation expenses also impact production margins. Additionally, trade tariffs and protectionist policies disrupt global billet trade flows, affecting export-oriented producers. Environmental regulations aimed at reducing carbon emissions increase compliance costs, particularly for blast furnace-based producers. Overcapacity in certain regions further exerts downward pressure on prices. These cost and policy-related challenges limits profitability and investment flexibility, hence moderating the overall growth potential of the market.

MARKET OPPORTUNITIES

Urbanization and Industrial Expansion Create Long-Term Demand Potential

Urbanization and industrial expansion present significant growth opportunities for the market. Rapid population growth in emerging economies drives housing, transportation, and infrastructure development, increasing consumption of long steel products derived from billets. Additionally, renewable energy projects, including wind and solar installations, require structural steel components, supporting billet demand. Industrial machinery manufacturing and automotive production further create opportunities for higher-grade alloy and special steel billet. Expansion of domestic steelmaking capacity in developing countries also opens investment opportunities. As governments prioritize infrastructure and economic development, steel demand is expected to remain resilient. These structural economic drivers create sustained growth potential, therefore reinforcing long-term expansion prospects in the market.

MARKET CHALLENGES

Overcapacity and Sustainability Pressures Impacts Market Growth

A major challenge in the market is global overcapacity, particularly in regions with aggressive production expansion. Excess supply leads to price competition and margin pressure. Additionally, increasing sustainability requirements compel producers to adopt cleaner technologies and reduce carbon emissions, raising capital expenditure. Transitioning toward low-carbon steel production methods requires significant investment in EAF and renewable energy integration. Balancing environmental compliance with cost competitiveness remains complex. These structural and regulatory pressures shape industry competitiveness, therefore influencing long-term strategic positioning in the market.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D efforts focus on improving billet quality, enhancing alloy compositions, and adopting low-carbon steelmaking technologies. Investments in EAF technology and green steel initiatives aim to reduce emissions while maintaining strength and durability. These innovations support sustainable market growth.

SEGMENTATION ANALYSIS

By Type

Higher Mechanical Strength and Cost Effectiveness Drives Carbon Steel Billet Segment Growth

Based on type, the market is segmented into carbon steel billet, alloy steel billet, and stainless / special steel billet.

Carbon steel billet account for the largest steel billet market share due to their cost-effectiveness, mechanical strength, and versatility in construction applications. These billets are widely used to manufacture reinforcing bars, structural sections, and wire rods essential for residential, commercial, and infrastructure projects. Rapid urbanization, government-backed infrastructure development, and expanding housing demand significantly support consumption. Carbon steel offers a favorable balance between strength and affordability, making it suitable for mass-scale construction. Additionally, its compatibility with rolling mills enhances production efficiency. Strong demand from emerging economies ensures sustained volume growth, thus maintaining carbon steel billet as the dominant product segment.

Alloy steel billet contain additional elements such as chromium, nickel, or molybdenum to improve hardness, tensile strength, and resistance to wear. These enhanced properties make them suitable for automotive components, heavy machinery, and industrial equipment manufacturing. Growth in automotive production and capital goods industries supports steady demand for alloy steel billet. The segment is growing at a CAGR of 5.7% during the forecast period.

Stainless and special steel billet offer superior corrosion resistance, heat tolerance, and mechanical durability. These billets are used in energy, marine, aerospace, and chemical processing industries where environmental exposure is critical. Rising investments in oil & gas, renewable energy, and advanced industrial equipment support demand for corrosion-resistant materials. The segment is growing at a CAGR of 5.6% during the forecast period.

By Application

Rapid Urbanization Leads to Construction Segment Dominance

Based on application, the market is segmented into construction, wire products, engineering, merchant bars and others.

Construction segment held the highest market share in 2025, as billets are processed into reinforcing bars and structural steel products used in buildings, bridges, highways, and rail networks. Rapid urbanization, government infrastructure spending, and housing development programs significantly boost demand. Emerging economies particularly rely on billet-derived long steel products for large-scale projects.

To know how our report can help streamline your business, Speak to Analyst

The wire products segment is projected to grow at a CAGR of 5.2% from 2026 to 2034. Steel billets are rolled into wire rods that are further processed into fasteners, fencing wires, cables, and industrial wires. Growth in manufacturing, automotive assembly, and consumer goods production supports steady demand for wire products. Additionally, agricultural and infrastructure sectors utilize steel wires extensively. Industrial expansion in developing regions further reinforces consumption.

The engineering segment is expected to growth at the highest CAGR of 5.4% from 2026 to 2034. Engineering applications involve converting billets into bars and specialized components used in machinery, tools, and automotive systems. Growth in industrial machinery manufacturing and automotive production drives demand for high-quality billets. Alloy steel billet are particularly preferred in this segment for their strength and durability. Expanding capital investment in industrial equipment and transportation infrastructure supports incremental growth.

STEEL BILLET MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

Asia Pacific

Asia Pacific Steel Billet Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to large-scale infrastructure development and strong construction activity. China and India are major consumers and producers, supported by extensive urban housing projects, transportation networks, and industrial expansion. Rapid industrialization and government-backed infrastructure initiatives significantly increase demand for billet-derived long steel products. Additionally, strong domestic steelmaking capacity and integrated supply chains enhance regional competitiveness. Growing automotive and engineering industries further support alloy billet consumption.

China Steel Billet Market

China’s market is one of the largest worldwide, with 2025 revenues valued at USD 140.02 billion, representing 41.7% of global market sales. Growth is driven by large-scale infrastructure spending, strong domestic steel production capacity, and continued urban development projects.

To know how our report can help streamline your business, Speak to Analyst

India Steel Billet Market

The India market in 2025 was at USD 28.4 billion, accounting for 8.5% of global revenues. Expansion is supported by rapid urbanization, government infrastructure programs, and rising residential construction activity.

Japan Steel Billet Market

The Japan market in 2025 reached USD 32.4 billion, accounting for roughly 9.7% of global market revenues.

Europe

Europe’s market is shaped by environmental regulations and advanced engineering demand. Countries such as Germany, Italy, and France focus on high-quality alloy and special steel billet for automotive and machinery sectors. Infrastructure renovation and renewable energy projects support steady consumption. However, strict carbon emission regulations and energy cost volatility influence production economics. Increasing transition toward green steel initiatives and EAF-based production is reshaping the market landscape.

U.K. Steel Billet Market

The U.K. market in 2025 was at USD 7.40 billion, representing 2.2% of global market revenues. Growth is driven by infrastructure renovation projects and construction sector recovery.

Germany Steel Billet Market

Germany’s market reached USD 11.3 billion in 2025, equivalent to around 3.4% of global market sales. Demand is supported by advanced engineering industries and focus on high-grade alloy steel production.

North America

North America represents a mature but stable market for steel billet. The U.S. leads regional consumption due to infrastructure rehabilitation projects and industrial manufacturing output. Government investments in highways, bridges, and energy infrastructure drive demand for reinforcing bars and structural steel derived from billets. Additionally, automotive and machinery production support alloy billet usage. Adoption of EAF technology enhances production efficiency and sustainability.

U.S. Steel Billet Market

Based on North America’s strong contribution, the U.S. market was valued at USD 22.92 billion in 2025, accounting for roughly 6.8% of global sales. Growth is fueled by infrastructure modernization funding and steady industrial and automotive manufacturing output.

Latin America & Middle East & Africa

Latin America demonstrates gradual growth driven by infrastructure projects and automotive assembly operations, particularly in Brazil and Mexico. Construction of residential and commercial buildings supports demand for carbon steel billet. While local production exists, imports supplement supply in certain countries. Economic fluctuations may affect capital investment cycles; however, government-backed infrastructure programs provide medium-term growth potential. On the other hand, the Middle East & Africa region is witnessing incremental growth driven by large-scale construction projects and industrial diversification initiatives. GCC countries are investing in downstream steel production facilities to reduce import dependency. Infrastructure expansion, urban development, and energy projects support billet consumption.

GCC Steel Billet Market

The GCC market reached USD 8.32 billion in 2025, representing 2.5% of global market revenues. Growth is driven by large-scale urban development projects and investments in downstream steel manufacturing facilities.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Adopting Vertically Integrated Strategies to Sustain Market Competition

The market is highly competitive and moderately consolidated, with leading global steel producers dominating production through vertically integrated operations. Companies with integrated iron ore sourcing, EAF technology, and continuous casting facilities maintain cost advantages. Competition is driven by production scale, raw material access, energy efficiency, and regional trade positioning. Asian manufacturers, particularly in China and India, exert significant influence on global pricing and export flows. Additionally, sustainability initiatives and green steel investments are emerging as key competitive differentiators. High capital intensity and regulatory compliance requirements create entry barriers, therefore reinforcing the dominance of established steelmakers in the global market.

LIST OF KEY STEEL BILLET COMPANIES PROFILED

- ArcelorMittal S.A. (Luxembourg)

- China Baowu Steel Group Corporation Limited (China)

- Nippon Steel Corporation (Japan)

- POSCO Holdings Inc. (South Korea)

- Tata Steel Limited (India)

- JSW Steel Limited (India)

- Nucor Corporation (U.S.)

- Hyundai Steel Company (South Korea)

- Emirates Steel Arkan (United Arab Emirates)

- Jindal Steel & Power Limited (India)

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Additionally, it provides valuable insights into the market and current industry trends, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Million Ton) |

| Growth Rate | CAGR of 5.4% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 335.61 billion in 2025 and is projected to reach USD 554.30 billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By application the construction segment is leading the market.

Asia Pacific held the highest market share in 2025.

Construction activity and manufacturing output are driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us