Steel Drums Market Size, Share & Industry Analysis, By Material (Carbon Steel and Stainless Steel), By Type (Tight Head and Open Head), By Capacity (Up to 10 Gallons, 10-30 Gallons, 31-50 Gallons, 51-80 Gallons, and Above 80 Gallons), By End-use Industry (Food & Beverages, Chemicals, Agriculture, Petroleum & Lubricants, Pharmaceuticals, Paints, Inks, & Dyes, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

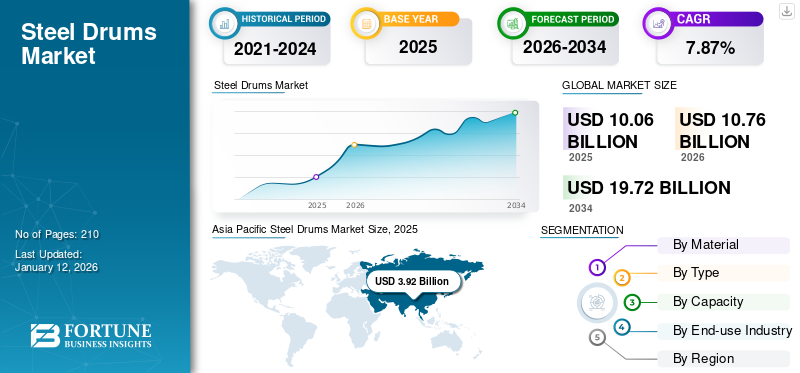

The global steel drums market size was valued at USD 10.06 billion in 2025. and It is projected to be worth USD 10.76 billion in 2026 and reach USD 19.72 billion by 2034, exhibiting a CAGR of 7.87% during the forecast period. Asia Pacific dominated the steel drums market with a market share of 35.76% in 2025.

Steel drums, commonly referred to as steel barrels, are crucial elements of industrial packaging, recognized for their resilience, sturdiness, and versatility. These cylindrical vessels, varying in capacity from 5 to 110 gallons, serve multiple functions, such as storage and transport of liquids, solids, and gases. Their robust design and durability against punctures, leaks, and outside damage render them perfect for managing hazardous materials. The market has experienced significant growth, driven by their widespread use in industries such as chemicals, petroleum, food and beverages, and pharmaceuticals. These durable and recyclable containers are essential for the safe storage and transportation of various materials.

The growing need for reliable and eco-friendly packaging options in sectors like chemicals, petroleum, paints, and pharmaceuticals is fueling the market growth because they are recyclable, and align with the global movement towards sustainable packaging methods.

Download Free sample to learn more about this report.

Global Steel Drums Market Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 10.06 billion

- 2026 Market Size: USD 10.76 billion

- 2034 Forecast Market Size: USD 19.72 billion

- CAGR: 7.87% from 2026–2034

Market Share:

- Asia Pacific dominated the Steel Drums Market with a 35.76% share in 2025, driven by rising chemical and lubricant sectors in China and India that require robust and safe storage solutions for industrial materials and hazardous substances.

- By material, carbon steel is expected to retain the largest market share in 2025, supported by its wide usage in sectors such as chemicals, petroleum, and food processing due to its adaptability, strength, and cost-effectiveness.

Key Country Highlights:

- United States: Petroleum and chemical industries drive market growth through high demand for durable and compliant packaging. Rising petroleum output and strict safety standards boost drum usage across national and international logistics.

- Europe: Growth is supported by strict EU regulations promoting durable and recyclable packaging. High recycling rates and investments in circular economy initiatives increase demand for premium drums across the region.

- China: Strong chemical and lubricant industries, paired with increasing oil production and industrial growth, make China a key driver of regional demand for steel drums, especially in bulk and hazardous goods handling.

- Latin America: Agriculture and beverage sectors demand durable and eco-friendly packaging solutions for fertilizers, chemicals, juices, and alcoholic drinks, supporting regional drum consumption.

- Middle East & Africa: The oil and gas sector fuels steel drum demand for storage and transport of crude oil, lubricants, and byproducts. Investments in manufacturing and logistics infrastructure further strengthen market growth.

MARKET DYNAMICS

MARKET DRIVERS

Market Growth Thrives Due to Durability, Secure Transport, and Rising Demand from Multiple Industries and Applications

The demand for strong storage and transport solutions significantly influences the market. These drums provide outstanding durability and resistance to impact, which makes them perfect for the secure transport of different materials, such as hazardous materials, liquids, and powders. Their sturdiness guarantees the secure handling of delicate substances by offering a tight seal and reliable closures that avert leaks and contamination. The drums are resilient to tough conditions and rough treatment, and their uniform sizes ease logistical processes across various sectors. Rising demand from sectors such as chemicals, pharmaceuticals, food and beverage, and oil and gas continues to boost the requirement for these drums for packaging and storage.

Demand from Chemical, Oil, and Gas Industries Propels the Demand for Safe, Durable, and Secure Storage

The global growth of the chemical, oil, and gas industries is a major factor propelling the growth of steel drum market. These sectors need dependable containers for the bulk storage and transport of hazardous substances, resulting in a higher demand for sturdy drums. These drums are preferred for their durability, corrosion resistance, and capability to securely hold chemicals, oils, solvents, and various petrochemical substances. Tight regulations and the requirement for secure drums enhance demand in these industries. The increase in chemical production and international trade demands strong packaging options, making drums a favored selection for secure and economical logistics.

MARKET RESTRAINTS

Rising Competition, Steel Prices, Transportation Costs, Recycling, and Regulations Limit the Market Growth

A limiting factor for the steel drum market is the rising competition from other packaging options like plastic drums and intermediate bulk containers (IBCs). The existence of alternatives, such as fiber drums, further limits product adoption. Variations in steel prices can influence production expenses and pricing approaches, impacting market stability. Elevated transportation expenses resulting from the heaviness of these drums may discourage certain clients, especially in areas with inadequate infrastructure. The expensive process of recycling these drums also poses a challenge, along with tighter rules on production and waste management can raise expenses and restrict output.

MARKET OPPORTUNITIES

Affordable, Durable, Sustainable, and Cost-effective is Driving Extensive Market Opportunities

Steel drums market present considerable potential because of their affordability and resilience. Their durable design guarantees a prolonged lifespan and the potential for repeated use, lowering long-term costs for industries. Reconditioning these drums boosts cost savings leading to establishing them as a sustainable and cost-effective choice. The resilience of drums reduces the chances of damage during shipping and storage, avoiding expensive leaks and spills. This durability, along with the possibility for repurposing and refurbishment, makes these drums a budget-friendly option compared to other packaging alternatives.

MARKET CHALLENGES

Variable Steel Prices Challenge Manufacturers, Which Leads to Affecting Competitiveness And Profitability

A significant challenge in the steel drum market is the variable prices of steel. Fluctuating costs of raw materials hinder manufacturers from keeping stable prices, which diminishes their competitiveness against substitute materials. Variable steel prices can greatly affect production expenses and profit margins for manufacturers. These variations can disturb market stability, influencing pricing strategies. Keeping prices stable for these drums is challenging, which may lower their competitiveness.

Download Free sample to learn more about this report.

STEEL DRUMS MARKET TRENDS

Sustainability, Emphasizing Durability, and Eco-friendly Packaging is Leading the Product Adoption

The increasing focus on sustainability and the circular economy presents a significant trend for the steel drum market. These drums are inherently sustainable due to their durability, reusability, and recyclability. Companies are adopting reuse, recycling, and repurposing practices to maximize the lifecycle of drums, yielding both environmental and economic benefits. Reconditioning and recycling drums conserves resources and minimizes waste. Furthermore, the rising demand for eco-friendly packaging in various industries, such as paints, inks, and coatings, drives the adoption of drums as a sustainable alternative to plastic containers.

IMPACT OF COVID-19

The COVID-19 pandemic first affected the steel drum market due to supply chain constraints and a lack of materials at production facilities. Lockdowns and trade limitations resulted in reduced demand and obstructed the production and distribution of drums. Nonetheless, the market started to bounce back in the later part of 2021 as nations reopened ports and international trade recommenced. Precautionary steps enabled ongoing operations while reducing risk and aiding sales in keeping pace with demand. The pandemic underscored the significance of strong supply chains, further propelling the steel market.

SEGMENTATION ANALYSIS

By Material

Carbon Steel Segment Dominates the Market Due to Usage Across Various Industries

Based on material, the market is segmented into carbon steel and stainless steel.

The carbon steel segment is dominating the market. Carbon drums are popular due to their adaptability, strength, and cost-effectiveness. They are frequently utilized in sectors such as chemicals, petroleum, and food processing to convey both hazardous and non-hazardous liquids, powders, and semi-solid substances. The segment is expected to dominate the market in 2026 with a share of 73.79%.

The second dominating segment is stainless steel. Rising demand for stainless drums in the agriculture sector will drive market expansion in several regions.

By Type

Tight Head Drums are Vital for Safely Storing Chemicals, Which Leads to Market Growth

Based on type, the market is segmented into tight head and open head.

The tight head segment is dominating the steel drums market share. The tight head type is expected to seize market value primarily due to its essential role in securely storing and transporting hazardous chemicals, oils, and petroleum lubricant products. These drums are designed to contain volatile materials and guarantee leak-proof sealing, which makes them essential for industries that must adhere to stringent environmental and safety regulations. The segment is expected to capture 70.82% of the market share in 2026.

The second dominating segment is the open head. Open head drums have a detachable lid that is fastened with bolts or clamps, providing convenient access for both filling and emptying. This is essential for sectors that need regular product dispensing, like those involved with chemicals, food products, and dangerous substances. The segment is likely to grow with a CAGR of 4.42% during the forecast period (2025-2032).

By Capacity

51-80 Gallons Segment Dominates the Market Due to Bulk Storage of Liquid

Based on capacity, the market is segmented into up to 10 gallons, 10-30 gallons, 31-50 gallons, 51-80 gallons, and above 80 gallons.

The 51-80 gallons segment is dominating the market, which is versatile and has been used in bulk storage and transportation of liquids, chemicals, and hazardous materials by many industries. It is most favored by the chemical, petroleum, and food industries because it complies with both domestic and international shipping regulations, thereby ideal for global logistics. This segment is expected to hold 43.22% of the market share in 2026.

The second dominating segment is 10-30 gallons in the market. This segment serves industries that need compact storage options such as chemicals, paints, or food items, where exact amounts are essential and the chance of spillage should be reduced. This segment is expected to register a substantial CAGR of 7.62% during the forecast period (2025-2032).

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Petroleum Segment Dominates the Market Due to the Transportation of Petroleum Products and Lubricants

Based on the end-use industry, the market is classified into food & beverages, chemicals, agriculture, petroleum & lubricants, pharmaceuticals, paints, inks, & dyes, and others.

The petroleum & lubricants segment is dominating the market of drums, as they are widely utilized for the storage and transportation of petroleum products and lubricants throughout the global supply chain. These drums provide excellent protection in high-temperature environments and maintain structural integrity in heat and flames without leaking or spilling. The segment is expected to capture 30.76% of the market share in 2026.

The second dominating end-use industry is chemical. The expansion of the chemical industries enhances the market for drums, as they are the ideal option for storing chemicals, lubricants, and various other substances. U.S. chemical production levels are projected to rise, leading to a greater demand for drums. This segment is poised to grow with a CAGR of 8.14% during the forecast period (2025-2032).

STEEL DRUMS MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. Asia pacific holds the largest share in the global market.

North America

Petroleum Segment Dominates the North American Market for Storage

The North America market was valued at USD 2.26 billion in 2025, capturing 22.74% of global revenue, and is estimated to reach USD 2.41 billion in 2026. The North American steel drum market is largely propelled by consistent demand from the chemical and petroleum industries, which necessitate safe and resilient packaging for hazardous substances. U.S. chemical production levels are anticipated to rise, leading to a higher demand for steel drums. Strict regulations and safety standards in U.S for chemical manufacturing require reliable and efficient packing solutions, leading to the increased use of these drums for chemical storage and transportation. The increase in global trade further enhances the demand for dependable bulk packaging. The U.S. market is set to be worth USD 1.63 billion in 2025.

- According to U.S. Energy Information Administration, it is estimated that the total world petroleum and other liquids supply will increase by about 0.6 million barrels per day (b/d) in 2024 and will increase by 1.9 million b/d in 2025 and 1.6 million b/d in 2026.

Europe

Stricter Regulations in Europe Promote the Demand for Durable and Recyclable Drums

In 2025, Europe held 20.01% of the global market, reaching a valuation of USD 2.51 billion, and is projected to grow to USD 2.67 billion in 2026. Strict environmental and safety regulations in Europe emphasizes the use of long-lasting and recyclable packaging materials, affecting the steel drum market. The transition to durable, high-quality packaging enables businesses to comply with the European Union's stringent regulations for the management, storage, and disposal of hazardous substances, fulfilling both safety standards and sustainability goals. Europe's market highlights its dedication to legal adherence, further boosting the need for premium and compliant drums. The growing emphasis on a circular economy encourages the use of reusable packaging solutions, which are a favored option for manufacturers. The U.K. market is anticipated to reach a market value of USD 0.34 billion in 2026.

- As per the European Steel Association AISBL (EUROFER), the large volumes of steel produced in Europe every year – 160 million tonnes – are made with large amounts of scrap steel. 56% of EU steel is made from scrap, with around 100 million tonnes of scrap steel recycled every year.

Germany is set to grow with a valuation of USD 0.64 billion in 2026, while France is projected to be valued at USD 0.53 billion in the same year.

Asia Pacific

Asia Pacific Market is Driven by Rising Chemical and Lubricant Sectors

Asia Pacific Steel Drums Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market with a valuation of USD 3.92 billion in 2025 and is projected to reach USD 4.25 billion in 2026. The strong chemical and lubricant sectors in China and India largely fuels the Asia Pacific market growth. These countries need robust packaging options for the secure storage and transport of chemicals, lubricants, and various industrial materials. The increase in lubricant and oil production, fueled by the automotive and machinery sectors, also enhances the use of these drums. China is estimated to stand at USD 1.69 billion in 2026.

- According to the International Council of Chemical Associations (ICCA), the chemical industry touches nearly every good-producing sector, making an estimated USD 5.7 trillion contribution to world Gross Domestic Product (GDP) through direct, indirect and induced impacts, equivalent to seven percent of the world’s GDP, and supporting 120 million jobs worldwide.

India is likely to reach a market value of USD 1.22 billion in 2026, while Japan is poised to reach USD 0.64 billion in the same year.

Latin America

Latin America’s Agriculture and Beverage Sectors Require Durable and Recyclable Drums

Latin America maintained a strong presence in the global market, reaching USD 0.71 billion in 2025, accounting for 10.39% share, and is expected to reach USD 0.74 billion in 2026. In this region, the rapidly expanding agricultural industry significantly influences the use of drums. Farmers and distributors prefer drums for the storage and transport of fertilizers, crop protectants, and various agricultural chemicals because of their durability and dependability. The expanding beverage sector further increases demand since drums are utilized for the bulk storage of juices and alcoholic drinks. The ability to recycle and reuse drums is particularly attractive to companies seeking economical and eco-friendly packaging options.

- As per the Latin American Steel Association, the production of rolled steel in Latin America should reach 55.3 Mt in 2022. If this projection materializes, the result will represent a decrease of 1.1% compared to 2021. The estimated consumption of rolled steel in the region will be reduced by 9.5% if the forecast of 67.8 Mt is confirmed.

Middle East & Africa

Middle East & Africa Market Thrives on Oil, Gas, and Packaging Needs

In 2025, the Middle East & Africa market stood at USD 0.65 billion, representing 11.11% of global demand, and is projected to grow to USD 0.69 billion in 2026. The steel drums market in the Middle East & Africa is strongly influenced by the region’s thriving oil and gas sectors, which need safe storage solutions for crude oil, lubricants, and chemical by products. The rise in investments in manufacturing capabilities and the expanding adoption of global quality standards also boost the need for drums in this region. The rising need for sturdy packaging in bulk liquid shipping is another factor contributing to this.

- As per the International Energy Agency, Crude oil production in the Middle East is Total 61 611 533 TJ in 2022. It accounts for the global share of 33% of the total in 2022.

Saudi Arabia is estimated to reach a valuation of USD 0.28 billion in 2025.

IMPACT OF TRADE PROTECTIONISM

Trade policies and tariffs can impact the drums market growth by affecting the cost of raw materials and finished products. Manufacturers must navigate these regulations to maintain competitiveness.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Participants in the Market is Witnessing Significant Growth Opportunities

The global market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major market players constantly focus on expanding their customer base across regions by innovating their existing wide range of products.

Major players in the industry include Mauser Group B.V., Greif, Inc., North Coast Container Corp, Rahway Steel Drum Co. Inc., General Steel Drum LLC, and others. Numerous other companies operating in the market are focused on market scenarios and delivering advanced packaging solutions.

List of the Key Companies Profiled in the Report:

- Metal Drum Co Ltd (U.K.)

- Mauser Packaging Solutions (U.S.)

- Greif, Inc. (U.S.)

- North Coast Container Corp (U.S.)

- Rahway Steel Drum Co Inc. (U.S.)

- General Steel Drum LLC (U.S.)

- Sicagen India Limited (India)

- Balmer Lawrie & Co. Limited (India)

- SCHÜTZ GmbH & Co. KGaA (Germany)

- Peninsula Drums CC (South Africa)

- Patrick J. Kelly Drums (U.S.)

- Nippon Steel Drums Co. Ltd. (Japan)

- PT Rheem Indonesia (Indonesia)

- INDONESIA RAYA (Indonesia)

- Pact Group (Australia)

KEY INDUSTRY DEVELOPMENTS

- In May 2024, Electra, a renewable energy-supported company backed by Bill Gates and Amazon, declared the launch of their green steel manufacturing facility in Colorado, USA. The plant aims to produce clean metallic iron from high-quality ores utilizing renewable energy, representing an essential advancement for sustainable steel production.

- In May 2024, Tosyali Algeria, part of Turkey's Tosyalı Holding, inaugurated a new flat-rolled steel mill in Algeria, expanding production capabilities in the area.

- In February 2024, Tata Steel declared the successful amalgamation of five essential enterprises such as Tata Steel Mining Limited, Tata Steel Long Products Limited, and The Tinplate Company of India Limited.

- In November 2023, The largest independent manufacturer of sustainable steel drums in North America is uniting its four companies under a new name, North Coast Container. The name change signals the start of a new era for the 106-year-old, family-owned business as it continues to expand as an industry leader in steel drum packaging.

- In May 2023, Global rigid container and life sciences packaging distributor Novvia Group (“Novvia”) acquired Rahway Steel Drum Company (“Rahway”), a New Jersey-based distributor of drums, pails, IBCs, and other rigid packaging solutions.

INVESTMENT ANALYSIS AND OPPORTUNITIES

In August 2024, JBDI Holdings, a Singapore-based supplier of new and reconditioned steel and plastic drums, raised USD 11.25 million by offering 2.25 million shares (22% secondary) at USD 5.00, the high end of the range of USD 4.00 to USD 5.00. JBDI Holdings has grown from a small reconditioning and recycling business to a comprehensive provider of revitalized, reconditioned, and recycled drums, comprising a diversified range of drums, including open-top drums, metal drums, plastic drums, plastic carboys, and intermediate bulk containers.

REPORT COVERAGE

The market research report provides a detailed market analysis. The market overview also focuses on key aspects, such as top key players, competitive landscape, product/service types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market intelligence & growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.87% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (Billion units) |

|

Segmentation |

By Material

|

|

By Type

|

|

|

By Capacity

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 10.06 billion in 2025.

The market is likely to grow at a CAGR of 7.87% over the forecast period.

The carbon steel segment leads the market.

The market size of Asia Pacific stood at USD 3.92 billion in 2025.

Steel drum market thrives due to durability, secure transport, and rising demand from multiple industries and applications.

Some of the top players in the market are Mauser Group B.V., Greif, Inc., North Coast Container Corp, Rahway Steel Drum Co Inc., General Steel Drum LLC, and others.

The global market size is expected to reach USD 19.72 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us