Rigid Plastic Packaging Market Size, Share & Industry Analysis, By Material (Polyethylene (PE), {High density polyethylene (HDPE) and Low-density polyethylene (LDPE)}, Polyethylene terephthalate (PET), Polypropylene (PP), Polyvinyl Chloride (PVC), and Others), By Product Type (Bottles & Jars, Containers, Trays & Pallets, IBC's, Clamshell, Drums, Caps & Closures, and Others), By Application (Food & Beverage, Pharmaceutical, Personal Care & Cosmetics, Home Care, Industrial, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

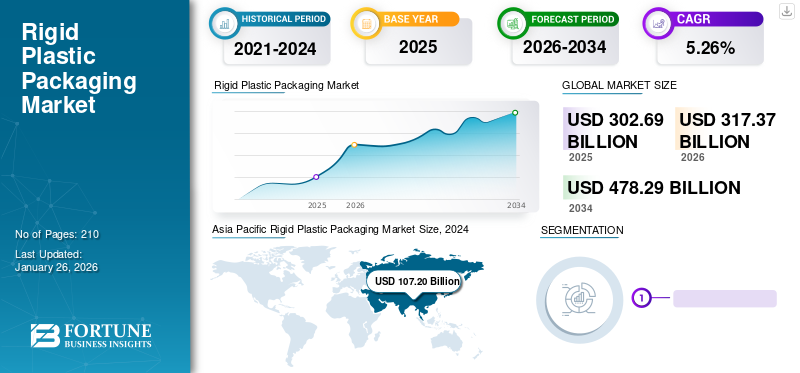

The global rigid plastic packaging market size was valued at USD 302.69 billion in 2025. The market is projected to grow from USD 317.37 billion in 2026 to USD 478.29 billion by 2034, exhibiting a CAGR of 5.26% during the forecast period. Asia Pacific dominated the rigid plastic packaging market with a market share of 37.34% in 2025. Moreover, the rigid plastic packaging market in the U.S. is projected to grow significantly, reaching an estimated value of USD 100.06 billion by 2032, driven by the increasing demand from the well-established pharmaceutical and medical sectors.

Rigid packaging is heavy and solid compared to normal packaging and protects products that require special handling. With the increasing trade of commodities globally, the need for the rigid plastic packaging industry is growing as it helps to transport products in bulk, thus driving market growth safely. The emerging economies of nations and growing demand for manufacturing and other industries worldwide are thriving market growth. The easy recyclability of plastic materials and their contribution to reducing carbon footprints is one of the primary reasons for accelerating market growth.

Download Free sample to learn more about this report.

COVID-19 IMPACT

Increased Growth in Food & Beverage Sector During Pandemic Accelerated Market Growth

The sudden outbreak of the pandemic negatively impacted the global market. The major hindrance for all industries, including packaging, was the shutdown of manufacturing units and stores and the shortage of raw materials. The pandemic positively impacted the pharmaceutical industry as there was increasing demand for medicines and vaccines. The rigid plastic packaging helped safely transport fragile medical equipment, consumer goods, and medicines. The food & beverage industry experienced moderate growth as retail stores were allowed to open for the necessary goods. All other major industries saw negative impacts. However, post-pandemic, the re-opening of the manufacturing units and other industries thrived in market growth.

Global Rigid Plastic Packaging Market Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 302.69 billion

- 2026 Market Size: USD 317.37 billion

- 2034 Forecast Market Size: USD 478.29 billion

- CAGR: 5.26% from 2026–2034

Market Share:

- Asia Pacific dominated the rigid plastic packaging market with a 37.34% share in 2025, driven by rising demand for food & beverage products in China and India, and rapid growth in the packaging sector supported by urbanization and industrial development.

- In the U.S., the market is projected to reach USD 100.06 billion by 2032 due to increasing demand from well-established pharmaceutical and medical sectors.

Key Country Highlights:

- United States: Strong growth driven by the pharmaceutical and medical sectors, with rigid plastic packaging supporting safe transport of fragile medical goods and medicines.

- India: Rapid expansion in food & beverage and pharmaceutical sectors is accelerating packaging demand, with the industry growing at 20–25% annually.

- China: Dominant role in regional demand due to large-scale consumption of packaged foods and industrial expansion.

- Europe: Growth supported by innovation and adoption of bioplastics in personal care and cosmetic packaging to meet sustainability goals.

Rigid Plastic Packaging Market Trends

Incorporation of Technologies in Packaging is Emerging as a Key Trend

Packaging is vital in handling the goods during transportation until they reach the end customer. Incorporating technologies in packaging, such as QR Codes, RFID, and sensors, enhances its performance. Smart packaging offers extended features to the packages and leads to benefits for customers and manufacturers. Integration of these technologies assists in controlling the temperature of the package and provides information about the inside environment of the products, thus extending the product’s shelf life. Moreover, these technologies help manufacturers with information about the location of products during transit. These features enhance the demand for smart packaging in rigid plastic packaging products and act as a key trend in the market.

Download Free sample to learn more about this report.

Rigid Plastic Packaging Market Growth Factors

Recyclability of Plastic Material Boosts Market Growth

Plastic is considered to be an unsustainable and non-environmental-friendly material. The governments of many nations have banned the use of plastic or advised to curb its usage and focus on more clean and low-impact packaging material. Innovation in the technologies and adoption of recyclable material is one of the primary factors contributing to market growth. According to research by the Organization for Economic Co-operation and Development, innovation for reusable plastic increased by 23% between 1970 and 2017. At the same time, innovation for repairing plastic has been raised by 12%.

Plastic takes hundreds of years to decompose completely, and according to the Environmental Protection Agency of the U.S., the municipal solid waste of PET in the U.S. in 2012 was 4.1 million tons, and only 31% was recycled. Due to these factors, the demand for bioplastic is increasing. Bioplastic is compostable plastic derived from natural materials or petroleum plastic products that are degradable. The augmenting demand for bio-based PE, PET, PP, and other materials is fueling the market growth.

Augmenting Demand for Bioplastic is Driving Market Growth

The increasing awareness among people using sustainable and low-impact products has led to a rise in the use of bioplastic as a material. Manufacturers have bioplastic alternatives for almost every conventional plastic material, such as bio-PP, biobased PE, and PET, among others. With the growing number of such materials and their application, the number of manufacturers and end-users is also rising, leading to market growth. For instance, in 2020, Coca-Cola planned to replace almost all petroplastic bottles with a bioplastic named PlantBottle using a resin named BioFormPX. For this launch, the company collaborated with other global companies to create a supply chain for the PlantBottle material.

The support from governments of several nations to drive bioplastic use by providing subsidies and other benefits to manufacturers and consumers is accelerating the rigid plastic packaging industry’s growth. For instance, the government of Thailand is considering a policy to fuel the growth of bioplastic demand from end-users by providing a 300% green tax credit.

RESTRAINING FACTORS

Accelerating Demand for Flexible Packaging is Hampering Market Growth

Flexible packaging refers to any packaging whose shape can be changed according to the product or content filled in it. It comprises materials that are much less dense and thicker than rigid packaging. It also bounces when it falls off vehicles during transportation without any damage, providing better product safety. The easy customizability and printability offered by flexible products, with other benefits over rigid plastic packaging, hamper market growth.

Rigid Plastic Packaging Market Segmentation Analysis

By Material Analysis

Polyethylene (PE) Segment Dominates Due to its Easy Recyclability and High Durability

Based on material, the market is classified into Polyethylene (PE), Polyethylene terephthalate (PET), Polypropylene (PP), Polyvinyl chloride (PVC), and others. The Polyethylene (PE) segment led the market accounting for 32.13% market share in 2026. Polyethylene (PE) is the dominating segment of the market. Polyethylene is a leakage-proof material that provides protection against water vapor and can be heat-sealed. It is extremely lightweight and economical. Furthermore, the easy recyclability and high durability with other features contribute to the segment's growth.

Polyethylene terephthalate (PET) is the second dominating region of this market. PET is one of the most transparent and sturdy materials, making it suitable for the packaging of water bottles and other clear packaging. It has lower gas permeability, thus protecting the products from outside gases and keeping the gases inside for cold drinks, hence enhancing the segment’s growth.

By Product Type Analysis

Bottles & Jars Segment Leads Due to its High Applications in End-Use Industries

Based on product type, the market is divided into bottles & jars, containers, trays & pallets, IBC’s, clamshell, drums, caps & closures, and others. Bottles & jars hold the largest market share. Bottles & jars have various applications in different growing end-use industries such as food & beverage, pharmaceutical, automotive, building & construction, and many others. Furthermore, plastic bottles and jars can take any shape, are lightweight, and resilient to damage. The easy recyclability and reusability of plastic bottles are driving the growth of this segment.

The Trays & pallets hold the second-largest segment is projected to dominate the market with a share of 26.64% in 2026. Trays & pallets hold the second-largest share of the rigid plastic packaging industry. The products packed in the trays and pallets can hold their weight without crushing the main product container. Furthermore, trays & pallets have lesser expenses to the shippers, and also increase the handling and visibility of the packed product, thus flourishing the growth of this segment.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Food & Beverage Segment Steers Growth Owing to Changing Preferences and Increasing Consumption of Packed Foods

Based on application, the market is divided into food & beverage, pharmaceutical, personal care & cosmetics, home care, industrial, and others. The food & beverage segment is dominating the market. The changing preferences of people and shifting trends toward the consumption of packed food are bolstering the growth of this segment. The increasing concern for health among all generations and the growing intake of healthy drinks such as protein shakes and milk products, among others, is one of the primary reasons for the growth of the food & beverage segment. The Food & Beverage segment led the market accounting for 28.21% market share in 2026.

Industrial is the second dominating segment of this market. Rapid industrialization and urbanization have led to a surged demand for industries throughout the world. The growing trade among countries and continuous development in developed and emerging nations have increased the demand for industrial products and their shipments, thus contributing to the growth of this segment.

REGIONAL INSIGHTS

The market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

The Asia Pacific market was valued at USD 113.03 billion in 2025, capturing 37.34% of global revenue, and is estimated to reach USD 119.45 billion in 2026. Asia Pacific is the leading region and held the largest rigid plastic packaging market share in 2024. The rising demand for food & beverage products in China and India is driving the growth of this region. According to the Packaging Industry Association of India, the Indian packaging industry is growing at 20-25% per annum, which is contributed by the food & beverage and pharmaceutical sectors.

Asia Pacific Rigid Plastic Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed 28.48% to the global market in 2025, with a valuation of USD 86.21 billion, and is projected to reach USD 90.47 billion in 2026. North America is the second largest leading region in the market. The well-established pharmaceutical and medical sector of the U.S. and the growing industrial sector of Canada is fueling the growth of the North American region.

Europe

Europe accounted for USD 72.27 billion in 2025, representing 23.88% of the global market share, and is projected to reach USD 75.27 billion in 2026. Europe is experiencing significant growth due to continuous innovation and technological advancements regarding the sustainability of plastic products and environmentally friendly alternatives such as bioplastic in the personal care and cosmetic packaging industries.

Latin America

In 2025, the Latin America market stood at USD 18.9 billion, representing 6.25% of global demand, and is projected to grow to USD 19.48 billion in 2026. Latin America is expected to show moderate growth. The growth potential mainly drives the manufacturers' investments in this region, and the emerging middle class is driving the growth of this region. Moreover, increasing food outlets and growing industries contribute to this region's growth.

Middle East & Africa

The market in Middle East & Africa reached USD 12.28 billion in 2025, representing 4.06% of total market revenue, and is projected to reach USD 12.71 billion in 2026.

List of Key Rigid Plastic Packaging Market Companies

Growing Key Market Players Focus on Customer Base Expansion to Drive Market Growth

The global rigid plastic packaging industry is highly fragmented and competitive. Regarding market share, the few major players dominate the market by offering innovative packaging in the packaging industry. They are constantly focusing on expanding their customer base across the regions by new product launches and technological innovations. Major players in the market include Amcor Plc, Berry Global, Silgan Holdings, Sonoco Product Company, and others. Numerous other players operating in the industry are focused on delivering advanced packaging solutions.

List of Key Companies Profiled:

- Amcor (Switzerland)

- Berry Global (U.S.)

- Silgan Holdings (U.S.)

- Sonoco Product Company (U.S.)

- Mauser Packaging Solutions (U.S.)

- Greif Inc. (U.S.)

- Schütz GmbH & Co. KGaA (Germany)

- Schoeller Allibert Services B.V. (Netherlands)

- Klöckner Pentaplast (U.K.)

- Time Technoplast Ltd. (India)

KEY INDUSTRY DEVELOPMENTS:

- February 2023 – Berry Global introduced child-resistant and tamper-evident PET bottles for pharmaceutical syrups and liquid medicines. The range of bottles includes 28mm neck PET bottles in sizes from 20ml to 1,000ml with various designs. These bottles are an attractive alternative to glass packaging.

- January 2023 – Tesco announced the launch of recycled plastic trays for the packaging of fresh fish products. The trays will contain at least 30% recycled coastal plastic content, which includes polyethylene, polypropylene, Polyethylene terephthalate (PET), and other types of plastic as material.

- September 2022 – Naeco, an Austrian manufacturer of plastic pallets, launched three types of plastic pallets named MASTER, FLAT, and MASTER MAX. The newly launched pallets are lightweight, monoblock, ideal for reuse, and suitable for various sectors. These pallets are made up of recycled polypropylene (rPP).

- September 2022 – Mars launched plastic jars with 15% recycled plastics for packaging candies in collaboration with Berry Global. The jars are available in 60, 81, and 87-ounce varieties and can eliminate 300 tons of virgin plastic annually.

- April 2022 – Encore Container announced that the company is diversifying its product portfolio by starting the production of 77-gallon plastic drums to serve new customers in the new market.

REPORT COVERAGE

The market research report provides a detailed market analysis and focuses on key aspects such as leading companies, material, product types, and leading applications of rigid plastic packaging. Moreover, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to market growth over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.26% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Product Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global rigid plastic packaging market size was valued at USD 302.69 billion in 2025 and is projected to grow from USD 317.37 billion in 2026 to USD 478.29 billion by 2034, exhibiting a CAGR of 5.26% during the forecast period.

The global market is projected to grow at a CAGR of 5.26% in the forecast period.

The market growth is primarily driven by the increasing demand for durable and recyclable packaging, especially in food & beverage and pharmaceutical sectors. The rise in bioplastic usage, global industrialization, and technological advancements in smart packaging also contribute significantly.

Asia Pacific dominates the market with a 37.34% share in 2025, led by rapid growth in China and India. Rising consumption of packaged foods and pharmaceutical products in these countries is a key contributor.

One of the key trends is the integration of smart technologies such as RFID, QR codes, and sensors into packaging. These technologies enhance product tracking, temperature control, and shelf life extension, creating new value for manufacturers and consumers.

Polyethylene (PE) leads the market due to its lightweight nature, durability, leakage resistance, and recyclability. PE is widely used in bottles, containers, and industrial packaging solutions.

The market faces challenges from the growing popularity of flexible packaging, which is lighter, more adaptable, and easier to customize. Additionally, environmental concerns and regulations against single-use plastics are restraining factors.

The food & beverage industry is the largest application segment, driven by changing consumer preferences, increasing demand for ready-to-eat foods, and rising consumption of bottled beverages.

Key companies include Amcor, Berry Global, Silgan Holdings, Sonoco Product Company, and Mauser Packaging Solutions. These players are focusing on recyclable materials, product innovation, and strategic expansions to strengthen their market presence.

- 2021-2034

- 2024

- 2021-2024

- 210

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us