Stockbroking Market Size, Share & Industry Analysis, By Broker Type (Full-Service Brokers, Discount Brokers and Hybrid Brokers), By Service Offering (Execution Services, Advisory Services and Value-Added Services), By Client Type (Retail Investors, High Net Worth Individuals (HNIs) and Institutional Investors) and Regional Forecast, 2026-2034

Stockbroking Market Size and Future Outlook

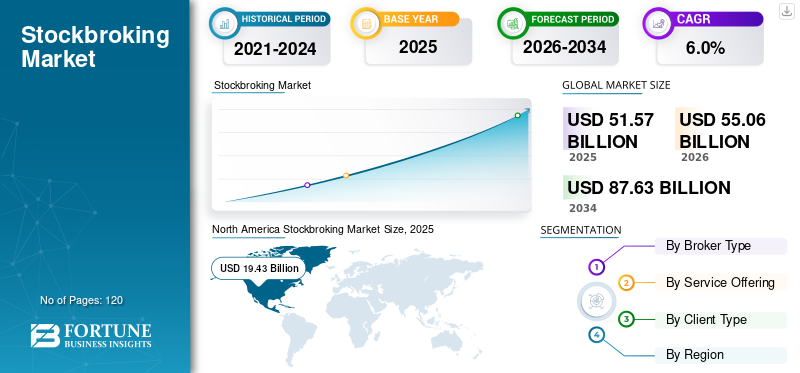

The stockbroking market size was valued at USD 51.57 billion in 2025. The market is projected to grow from USD 55.06 billion in 2026 to USD 87.63 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. North America dominated the stockbroking market with a market share of 37.68% in 2025.

The market comprises firms and digital platforms that facilitate buying and selling of equities, derivatives, Exchange-Traded Funds (ETFs), bonds and other securities on behalf of retail and institutional investors. Stockbrokers generate revenue through commissions, spreads, margin financing, advisory fees and value-added services such as portfolio analytics and wealth management tools.

The market continues to expand due to rising retail participation in equity sectors, increasing financial literacy, and rapid adoption of mobile-based trading platforms. Technological innovation, including AI-driven advisory tools and low-cost brokerage models, has reshaped competitive dynamics. Additionally, high trading volumes across derivatives and ETFs have strengthened brokerage revenues globally.

Major market participants including Charles Schwab Corporation, Fidelity Investments, Morgan Stanley, Robinhood Markets, Inc., Interactive Brokers Group, Inc., and E*TRADE (Morgan Stanley) continue to expand digital brokerage capabilities and diversify revenue streams through advisory and value-added solutions.

- For instance, in November 2023, Charles Schwab Corporation completed the integration of TD Ameritrade, significantly expanding its brokerage client base and strengthening its retail and advisory capabilities.

Download Free sample to learn more about this report.

STOCKBROKING MARKET TRENDS

Digital Brokerage Platforms and Commission Compression Reshapes Market Growth

A key trend shaping the market is the rapid growth of digital-first brokerage platforms offering commission-free trading models. Discount brokers have attracted millions of retail investors through intuitive mobile interfaces, real-time analytics and fractional investing features.

At the same time, full-service brokers are expanding value-added services such as portfolio advisory, retirement planning and ESG investing tools to maintain differentiation. Increased automation and AI-based investment insights are transforming service delivery models.

- For instance, in 2024, Robinhood expanded its retirement account offerings, enhancing long-term investment tools beyond traditional commission-free trading.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Retail Investor Participation Drives Market Growth

The stockbroking industry is primarily driven by rising retail investor participation across global equity sectors. Lower transaction costs, digital access to trading platforms and increased financial awareness have significantly expanded the investor base. Retail trading volumes now account for a substantial share of daily exchange activity in developed and emerging markets.

Additionally, volatile market conditions have increased demand for derivatives and active trading strategies, further driving stockbroking market growth.

- For instance, in 2024, Interactive Brokers Group, Inc., reported strong growth in new retail accounts, reflecting continued expansion in global retail participation.

MARKET RESTRAINTS

Regulatory Scrutiny and Margin Pressure Restricts Market Expansion

Increasing regulatory oversight on investor protection, margin trading and order execution transparency poses operational challenges for brokers. Compliance costs continue to rise, particularly in highly regulated markets such as North America and Europe.

Moreover, commission compression and competitive pricing among discount brokers reduce margins, forcing firms to diversify into advisory and value-added services to sustain profitability.

- For instance, in 2024, several U.S. brokerage firms enhanced compliance reporting systems in response to evolving SEC transparency requirement.

MARKET OPPORTUNITIES

Expansion of Value-Added Services and Wealth Platforms Creating Growth Opportunities

Stockbrokers are increasingly expanding into value-added services such as robo-advisory, retirement accounts, tax optimization tools and alternative investment access. These services create recurring revenue streams beyond transaction-based commissions. Growing demand for personalized portfolio insights and ESG-aligned investments is further encouraging brokers to invest in analytics-driven platforms and advisory ecosystems.

- For instance, in 2024, Fidelity Investments enhanced its digital wealth advisory platform, expanding AI-based portfolio management tools for retail investors.

Segmentation Analysis

By Broker Type

Full-Service Brokers Dominates Due to Comprehensive Advisory Capabilities

Based on broker type, the market is segmented into full-service brokers, discount brokers and hybrid brokers.

The full-service brokers segment holds the highest stockbroking market share, driven by comprehensive advisory services, wealth management integration and strong institutional relationships. These brokers generate diversified revenues through advisory fees, managed portfolios and financial planning services.

- For instance, Morgan Stanley’s wealth management division continued expanding advisory-led brokerage services in 2024, reinforcing full-service dominance.

The discount brokers segment is expected to register the highest CAGR of 7.0%, supported by rapid retail adoption of low-cost digital trading platforms.

To know how our report can help streamline your business, Speak to Analyst

By Service Offering

Execution Services Lead Due to High Trading Volumes

Based on service offering, the market is segmented into execution services, advisory services, and value-added services.

The execution services segment holds the highest market share, as trade execution remains the core function of stockbrokers, generating substantial transaction-based revenue from equities and derivatives trading.

- For instance, in 2024, Charles SchwabCcorporation reported strong equity and ETF trading volumes, highlighting continued reliance on execution services.

The value-added services segment is projected to grow at the highest CAGR of 7.2% due to increasing demand for robo-advisory and financial planning tools.

By Client Type

Retail Investors Dominate Due to Expanding Individual Participation

Based on client type, the market is segmented into retail investors, high net worth individuals (HNIs) and institutional investors.

The retail investors segment holds the highest market share, driven by app-based trading growth and commission-free brokerage models. Retail trading activity has expanded significantly across developed and emerging markets.

- For instance, Robinhood reported continued growth in funded retail accounts in 2024, reflecting sustained participation levels.

The retail investors segment is also expected to register the highest CAGR of 6.8%, supported by rising financial literacy and digital adoption.

Stockbroking Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and Middle East & Africa.

North America

North America Stockbroking Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share, supported by deep capital markets, advanced trading infrastructure and high retail participation. The region benefits from established brokerage giants, diversified revenue streams and strong derivatives activity. Digital brokerage innovation and strong ETF penetration further strengthen revenue generation across U.S. and Canadian markets.

U.S. Stockbroking Market

The U.S. market in 2026 is estimated at around USD 17.42 billion, representing approximately 31.6% of global revenues. High retail participation, strong derivatives trading and diversified brokerage models drive market dominance. Advanced digital platforms and wealth management integration further reinforce market leadership.

Europe

Europe represents a mature market supported by diversified investor bases and strong regulatory oversight. Increasing adoption of digital trading platforms and ESG-focused investments supports brokerage expansion. Cross-border brokerage operations across EU markets enhance liquidity and competition.

U.K. Stockbroking Market

The U.K. market in 2026 is estimated at around USD 4.13 billion, representing approximately 7.5% of global revenues. London remains a major financial hub with high equity and derivatives trading volumes. Strong HNI participation and advisory services drive brokerage revenues.

Germany Stockbroking Market

Germany’s market in 2026 is estimated at around USD 2.75 billion, representing approximately 5.0% of global revenues. Strong retail and institutional trading participation supports market stability. Digital brokerage adoption continues to expand across younger investors.

Asia Pacific

Asia Pacific is expected to register the highest CAGR, driven by rapid retail investor expansion, financial market reforms and increasing IPO activity. Digital brokerage platforms are gaining significant traction across India, China and Southeast Asia. Rising middle-class participation and government-backed capital sectors reforms accelerate brokerage demand.

Japan Stockbroking Market

Japan’s market in 2026 is estimated at around USD 3.11 billion, representing approximately 5.6% of global revenues. Advanced trading infrastructure and institutional participation drive stable revenues. Retail trading activity has expanded through digital platforms.

China Stockbroking Market

China’s market in 2026 is estimated at around USD 5.52 billion, representing approximately 10.0% of global revenues. High domestic trading volumes and retail & institutional investor activity support brokerage expansion. Regulatory reforms continue to strengthen capital sector depth.

India Stockbroking Market

India’s market in 2026 is estimated at around USD 3.27 billion, representing approximately 5.9% of global revenues. Rapid growth in retail demat accounts and discount brokerage platforms drives market acceleration. Strong IPO pipelines and derivatives volumes further support expansion.

South America and Middle East & Africa

The Middle East & Africa region represents an emerging but steadily expanding market, supported by financial sector liberalization, privatization initiatives and capital market modernization programs. Governments across the GCC and selected African economies are actively strengthening exchange infrastructure, enhancing regulatory transparency and encouraging foreign investor participation to deepen market liquidity. Increasing IPO activity in energy, infrastructure and financial services sectors is gradually strengthening brokerage revenues across the region.

Furthermore, digital brokerage adoption is expanding, particularly in the GCC and South Africa, as retail participation rises and online trading platforms gain traction. Regulatory reforms aimed at improving investor protection and cross-border capital flows are expected to further support market development across the Middle East & Africa region during the forecast period

GCC Stockbroking Market

The GCC market in 2026 is estimated at around USD 1.51 billion, representing approximately 2.7% of global revenues. Energy-sector listings and government privatization initiatives support brokerage activity. Foreign investor participation continues to increase across regional exchanges.

COMPETITIVE LANDSCAPE

Key Industry Players

Digital Expansion and Wealth Platform Integration Strengthening Market Positioning

The global stockbroking market is moderately consolidated, with leading firms competing across execution services, advisory solutions, and digital wealth management platforms. Major brokerage firms are increasingly investing in AI-driven trading tools, integrated wealth ecosystems, and commission-optimized pricing models to retain retail and institutional clients.

Full-service brokers continue expanding advisory-led revenue streams, while discount brokers focus on scale, mobile-first platforms, and value-added digital services. Strategic acquisitions, platform upgrades, and international expansion remain central to competitive differentiation.

- For instance, in May 2024, Nasdaq completed its USD 10.5 billion acquisition of Adenza, enhancing its capital markets software and risk management technology portfolio.

LIST OF KEY STOCKBROKING PLAYERS PROFILED

- Charles Schwab Corporation (U.S.)

- Fidelity Investments (U.S.)

- Morgan Stanley (U.S.)

- Interactive Brokers Group, Inc. (U.S.)

- Robinhood Markets, Inc. (U.S.)

- E*TRADE (Morgan Stanley) (U.S.)

- TD Ameritrade (U.S.)

- Hargreaves Lansdown plc (U.K.)

- Zerodha Broking Ltd. (India)

- Saxo Bank A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Morgan Stanley completed the full operational integration of E*TRADE’s brokerage infrastructure into its wealth management division, enhancing cross-selling of advisory and digital trading services to retail and HNI clients.

- December 2024: Robinhood Markets, Inc. launched commission-free trading for select international equities in the U.K., expanding its retail brokerage footprint beyond the U.S. market.

- July 2024: Interactive Brokers Group, Inc., announced expansion of overnight trading hours for U.S. stocks and ETFs, extending trading accessibility for global retail and institutional investors.

- March 2024: Fidelity Investments expanded zero-expense-ratio index fund offerings and enhanced its digital brokerage tools to strengthen retail client acquisition and long-term asset retention.

- November 2023: Charles Schwab Corporation completed the integration of TD Ameritrade client accounts onto Schwab’s brokerage platform, significantly increasing its retail investor base and execution scale.

REPORT COVERAGE

The global stockbroking market analysis includes a comprehensive study of market size & forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence market growth over the forecast period The report also covers technological advancements in digital identity and verification platforms, compliance considerations, and key strategic developments including partnerships and M&A activity, alongside regional insights and competitive landscape analysis. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Broker Type, Service Offering, Client Type, and Region |

| By Broker Type |

|

| By Service Offering |

|

| By Client Type |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 51.57 billion in 2025 and is projected to reach USD 87.63 billion by 2034.

In 2025, North Americas market value stood at USD 19.43 billion.

The market is expected to exhibit a CAGR of 6.0% during the forecast period of 2026-2034.

By client type, the retail investors segment is expected to lead the market.

Rising retail investor participation is the key factor driving the market growth.

Charles Schwab Corporation, Fidelity Investments, Morgan Stanley, Interactive Brokers Group, Inc., and Robinhood Markets, Inc. are among the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us