Strontium Carbonate Market Size, Share & Industry Analysis, By Form (Powder, Granular, and Others), By Grade (Electronic Grade, Industrial Grade, and Others), By Application (Glass & Ceramics, Pyrotechnics & Fireworks, Electronics & Magnetic Materials, Medical, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

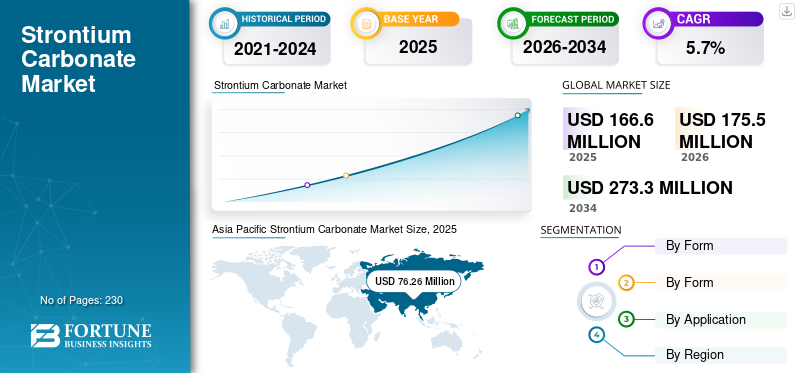

The global strontium carbonate market size was valued at USD 166.6 million in 2025. The market is projected to grow from USD 175.5 million in 2026 to USD 273.3 million by 2034 at a CAGR of 5.7% during the forecast period. Asia Pacific dominated the global strontium carbonate market with a market share of 45.77% in 2025.

Strontium carbonate is an inorganic compound with the chemical formula SrCO3. It appears as a white, odorless, and tasteless powder with an orthorhombic crystal structure. The compound is practically insoluble in water but dissolves in dilute acids, releasing carbon dioxide. The growth factors driving the market include the expanding demand from the electronics industry, particularly for high-purity electronic grade material used in Multilayer Ceramic Capacitors (MLCCs), OLED displays, and ferrite magnets for electric vehicles and renewable energy systems. Rapid industrialization and urbanization in the Asia Pacific, particularly in China and India, drive increased the consumption of ceramics, glass, and pyrotechnics. Additionally, the push toward sustainable and energy-efficient technologies fosters R&D in thermochemical energy storage and magnetic materials, creating new applications for strontium carbonate. Hebei Xinji Chemical Group Co. Ltd., Kandelium GmbH, Solvay SA, Joyieng Chemical Limited, and JAM Group Co. are the key players operating in the market.

Download Free sample to learn more about this report.

STRONTIUM CARBONATE MARKET TRENDS

Shift toward Ultra-Low Impurity Carbonates to Meet Electronics-Grade Standards is a Market Trend

The strontium carbonate market is undergoing a significant shift toward ultra-low impurity variants to align with stringent electronics-grade standards, driven by the electronics industry's demand for high-performance components such as multilayer ceramic capacitors (MLCCs), OLED displays, and luminescent materials. Additionally, trace impurities such as iron, sodium, or chloride ions below 10 ppm can cause wafer defects, optical distortions, or reduced luminance efficiency in advanced applications such as 5G infrastructure and high-definition panels.

The market growth for high-purity strontium carbonate is projected robustly, fueled by electronics expansion and emerging uses in solid-state batteries, where strontium doping enhances ionic conductivity. This evolution enhances product reliability while also supporting regulatory compliance, such as EU heavy metal limits, positioning ultra-low impurity carbonates as a key growth driver in the strontium carbonate sector.

MARKET DYNAMICS

MARKET DRIVERS

Rising Product Consumption in Ceramic Glazes and Frits Boosts Material Demand

Strontium carbonate acts as an effective flux in ceramic glazes, helping raw materials melt and fuse more effectively during firing. It enhances the durability of ceramic products by improving resistance to crazing (fine surface cracks) and scratching, which increases the longevity and aesthetic quality of ceramic pieces. Additionally, this product is considered a safer and environmentally friendlier alternative to barium carbonate, making it increasingly popular in industrial and artistic ceramic applications. The growing preference for improved glaze performance and sustainability is fueling the demand for this material in the ceramics sector.

Furthermore, the role of this material in frit production also drives market growth. Frits, which are pre-melted raw materials that become glassy when fired, help reduce bubble formation and surface defects in ceramics, especially in high-temperature and fast-cycle firing processes. By incorporating this material into frit formulations, manufacturers achieve improved glaze smoothness, gloss, and color development, meeting the rising consumer demand for high-quality sanitary and daily-use ceramic products. This extended functionality in boosting glaze quality, combined with its application in lead-free, environmentally compliant ceramic products, positions SrCO3 as a key material, contributing to the global strontium carbonate market growth.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Limited Availability of High-Grade Celestine Ore to Hamper Market Growth

The limited availability of high-grade celestine ore, the primary raw material for strontium carbonate production, acts as a key restraining factor for the market by undermining conversion efficiency and escalating costs. Celestine (SrSO4) ore typically requires high strontium content for optimal yields in dominant processes such as black ash reduction or double decomposition with sodium/ammonium carbonate. Impurities such as iron, calcium sulfate, and barium sulfate form ferrites or insoluble complexes that clog equipment and reduce purity to below 98-99% without extensive purification.

MARKET OPPORTUNITIES

Expansion of Renewable Energy Storage and Magnetic Applications to Offer Growth Opportunities

The expansion of renewable energy storage, particularly in Concentrating Solar Power (CSP) plants, presents a compelling opportunity for the market through its role in advanced Thermochemical Energy Storage (TCES) systems. Strontium carbonate (SrCO3) enables reversible calcination-carbonation reactions, where high-temperature solar input (up to 1300°C) decomposes it into Strontium Oxide (SrO) and CO2, storing energy at densities exceeding 1.8 GJ/m³, far surpassing those of molten salts. The exothermic recombination releases heat above 1000°C for efficient power generation during off-sun periods. This addresses solar intermittency, supporting CSP scalability amid global renewable targets, with research demonstrating cycle stability over 2000 iterations through pore-enhanced composites.

The push for rare-earth-free magnets, driven by supply chain vulnerabilities and cost pressures, leverages strontium's abundance to boost magnetic performance in renewable systems, with demand rising alongside offshore wind and EV adoption. These dual opportunities in storage and magnetics position strontium carbonate for sustained growth, fostering innovation in composites that enhance reaction kinetics and durability.

MARKET CHALLENGES

High Cost and Volatility of Upstream Mining and Processing to Hinder Market Growth

High costs and volatility in upstream mining and processing pose a major challenge for the market, primarily due to the energy-intensive extraction and conversion of celestine ore (SrSO4), which dominates global supply. Processes such as the black ash method require high-temperature reduction (over 950°C) with coke to produce strontium sulfide, followed by leaching and carbonation. This approach incurs substantial raw material, utility, and capital expenses often exceeding USD 1,500 to 2,500 per metric ton for plant setup and operations, as detailed in comprehensive cost analyses. Limited high-grade ore reserves, concentrated in China and Mexico, amplify mining costs amid depleting deposits and regulatory hurdles, while fluctuating coke, energy, and labor prices exacerbate financial pressures on producers.

Regulatory Compliance May Create Hurdles for Market Expansion

Regulatory compliance presents a significant hurdle for the market, primarily due to stringent environmental and safety standards that elevate production costs and operational complexity. Regulations such as REACH in the EU and TSCA in the U.S. mandate rigorous registration, risk assessments, and emission controls for strontium compounds, given their mining impacts, including habitat disruption and potential aquatic toxicity evidenced by Canada's Federal Water Quality Guidelines, which limit strontium to protect freshwater ecosystems. These requirements necessitate costly upgrades in waste management, monitoring, and purification, which strain smaller producers and contribute to market consolidation amid global sustainability mandates.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions significantly impact the market, primarily due to its concentrated supply chain, which is dominated by China (accounting for over 70% of global production) and Mexico, making it vulnerable to export restrictions, tariffs, and policy shifts. China's strategic classification of strontium compounds as critical materials enables potential export controls. Meanwhile, the U.S. tariffs and reciprocal measures disrupt imports from key suppliers, elevating costs and causing shortages for downstream industries such as electronics and ceramics. Mexico's celestine exports face similar trade barriers, with global flows, such as Germany's leading role and U.S. reliance.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Research and Development (R&D) trends in the market are heavily focused on improving product purity, enhancing process efficiency, and expanding high-value applications. Innovations emphasize achieving ultra-low impurity grades required for electronics and display technologies, where precise material properties impact performance in multilayer capacitors, OLED screens, and ferrite magnets.

R&D efforts are also targeting scalable, energy-efficient purification methods to address the challenges posed by the limited availability of high-grade celestine ore. Researchers explore mechanochemical synthesis and membrane filtration to reduce contaminants and enhance strontium carbonate reactivity and stability, which are crucial for thermochemical energy storage and battery materials development.

SEGMENTATION ANALYSIS

By Form

Powder Segment Dominated the Market Due to Its Fine Particle and Widespread Use

Based on form, the market is segmented into powder, granular, and others.

The powder segment held the largest market share in 2025. The powder form is a fine, white, odorless, and tasteless particulate, prized for its high reactivity, uniform dispersion, and rapid dissolution in acids, making it ideal for precision applications. This form excels in electronics-grade applications, such as Multilayer Ceramic Capacitors (MLCCs) and OLED phosphors, where sub-ppm purity prevents defects. It is also suitable for ceramics, where it enhances thermal stability and craze resistance by fluxing glazes and frits. Its versatility extends to pyrotechnics for red flame effects, electromagnets, and battery additives, with high-purity variants supporting miniaturization trends despite higher processing costs.

Granular material features larger, aggregated particles designed for superior flowability, reduced dust generation, and easier handling in bulk industrial processes. It appears as white, crystalline granules with a controlled size distribution, ensuring consistent dosing. Producers favor granules for pyrotechnics and glassmaking to reduce airborne particulates and enhance safety, although they command a premium price over powder due to the additional granulation steps.

The others category encompasses specialized strontium carbonate variants, such as crystals, custom agglomerates, or nano-structured powders tailored for niche high-tech applications beyond standard powder or granular needs. These include ultra-fine crystalline forms for advanced thermochemical energy storage in renewables, where enhanced surface area boosts carbonation kinetics, or doped composites for solid-state batteries and magnetic ferrites in EVs.

By Grade

Industrial Grade Segment Dominated the Market due to Broad Applicability across Various Applications

Based on grade, the market is segmented into electronic grade, industrial grade, and others.

The industrial grade segment dominated the market by volume in 2025. The segment dominated by volume due to its extensive use in high-consumption sectors such as construction and pyrotechnics. The growth is driven by cost-effectiveness and bulk availability.

In contrast, electronic grade leads by value owing to premium pricing from ultra-high purity (≥99.995%) requirements, supporting advanced miniaturization in semiconductors and displays amid rising electronics demand.

The others category includes pharmaceutical, food, and specialty grades, occupying a smaller but growing niche with tailored purities. Pharmaceutical variants support ranelate treatments for osteoporosis, while food grades meet safety thresholds for limited uses, although regulatory hurdles limit their scale. These grades command moderate value premiums for compliance testing and traceability, with potential applications in emerging biomedical fields, such as nanoparticles. However, they trail the industrial and electronic segments in both volume and revenue due to their narrower adoption.

By Application

To know how our report can help streamline your business, Speak to Analyst

Electronics & Magnetic Materials Segment Led the Market Due to its Utilization as a Flux in Ceramic Glazes and Frits

Based on application, the market is segmented into glass & ceramics, pyrotechnics & fireworks, electronics & magnetic materials, medical, and others.

The electronics & magnetic materials segment commands the dominating share, driven by premium pricing for ultra-high purity electronic-grade material essential in Multilayer Ceramic Capacitors (MLCCs), OLED phosphors, and strontium ferrite permanent magnets. This segment benefits from robust growth in consumer electronics, 5G infrastructure, electric vehicles (EVs), and renewable energy systems.

The glass & ceramics segment accounted for the second-largest share in the market in 2025. Strontium carbonate is extensively used as a flux in ceramic glazes and frits, improving durability, hardness, and reducing crazing or bubbles during firing. It enhances color vibrancy and finish quality in tiles, pottery, and technical ceramics. In glassmaking, it improves hardness, scratch resistance, brightness, and reduces micro-cracking in optical, pharmaceutical, and display glasses such as LCD substrates, supporting lightweight and durable glass technologies.

The pyrotechnics & fireworks segment is set to experience significant growth during the forecast period. This segment harnesses strontium carbonate’s ability to produce bright red flames, making it a key colorant in fireworks and signaling flares. Its stability and combustion characteristics enable vibrant color effects while serving as a safer substitute for toxic barium compounds. Consistency in particle size and purity is critical in this application to achieve the desired luminosity and safety standards.

The others category includes specialty applications such as metallurgical refining, chemical precursors for strontium compounds such as strontium chromate and nitrate used in corrosion-resistant paints, and limited use in food-grade additives. These applications capitalize on SrCO3’s chemical stability and ability to improve product performance in diverse industrial contexts.

STRONTIUM CARBONATE MARKET REGIONAL OUTLOOK

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Strontium Carbonate Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted led the global strontium carbonate market share in 2025. The region dominates the market in volume and value, driven by rapid industrialization, urbanization, and the expansion of electronics, ceramics, and automotive industries in countries such as China, India, Japan, and South Korea. Strong economic growth, robust demand for consumer electronics, and supportive government policies in the Asia Pacific region significantly contribute to its leading market share and the fastest growth rate during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

North America

North America maintains a substantial market share through advanced manufacturing in electronics, automotive, and healthcare, with steady demand for high-purity electronic-grade strontium carbonate in MLCCs, EVs, and medical applications. The U.S. relies heavily on imports from China and Mexico, facing challenges from trade tariffs and supply chain volatility, yet benefits from robust R&D and regulatory frameworks that promote sustainability.

Europe

Europe exhibits steady market growth underpinned by stringent quality standards, sustainability initiatives, and strong bases in ceramics, glass, and electronics manufacturing across Germany, the U.K., and Spain. The market is set for modest but steady growth, leveraging its strong industrial base in glass, electronics, and coatings, with innovation and strategic investments likely the key to capturing opportunities in the evolving landscape.

Latin America

Latin America emerges as a promising market, fueled by infrastructure development, mining activities, and rising industrial demand, particularly in Mexico, a key celestine exporter, and Brazil with growing ceramics and construction sectors. Opportunities arise from the expanding middle-class consumption of paints, glass, and consumer goods. However, challenges such as political instability, currency fluctuations, and logistical hurdles limit the scale.

Middle East & Africa

The Middle East & Africa represent nascent markets with substantial upside from infrastructure projects, urbanization, and the adoption of emerging electronics, though constrained by political risks, limited local production, and heavy reliance on imports.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Manufacturers to Direct their Capital toward Product Quality Enhancement

Major investments are underway in the market as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers such as Hebei Xinji Chemical Group, Kandelium GmbH, Solvay SA, Joyieng Chemical Limited, and JAM Group are directing their capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly centered on improving purity consistency, reducing environmental footprint, and developing grades suited for advanced ceramics, electronics, and specialty glass applications.

LIST OF KEY STRONTIUM CARBONATE COMPANIES PROFILED

- Central Drug House (CDH) Fine Chemicals (India)

- Divjyot Chemicals Pvt Ltd (India)

- Jam Group Co. (Iran)

- Kandelium GmbH (Germany)

- Solvay (Belgium)

- Star Earth Minerals Pvt Ltd (India)

- Suvchem (India)

- Vishnu Priya Chemicals Pvt Ltd (India)

- Joyieng Chemical Limited (China)

- Hebei Xinji Chemical Group Co Ltd (China)

KEY INDUSTRY DEVELOPMENTS

- August 2025 – Vishnu Chemicals Limited announced that its fully-owned subsidiary, Vishnu Strontium Private Limited, commenced the commercial production of strontium carbonate at its manufacturing facility in Atchutapuram, Visakhapatnam, Andhra Pradesh. The company informed the exchanges that the commencement of production marks an important milestone in its specialty chemicals business.

- July 2025 – Vishnu Priya Chemicals Pvt Ltd, a leading manufacturer of high-performance specialty chemicals, announced its acquisition of Jayansree Pharma Private Limited (JPPL). This acquisition, finalized through a Share Purchase Agreement on August 19, 2025, represents a significant strategic expansion for Vishnu Chemicals, reinforcing its market position and operational capabilities.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, form, grade, type, and application. Besides this, it provides valuable insights into the market and current industry trends as well as highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several other factors that contribute to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.7% from 2025 to 2034 |

|

Segmentation |

By Form, By Grade, By Application, By Region |

|

By Form |

· Powder · Granular · Others |

|

By Grade |

· Electronic Grade · Industrial Grade · Others |

|

By Application |

· Glass & Ceramics · Pyrotechnics & Fireworks · Electronics & Magnetic Materials · Medical · Others |

|

By Region |

· North America (By Form, By Grade, By Application, By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Form, By Grade, By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Form, By Grade, By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Form, By Grade, By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Form, By Grade, By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 166.6 million in 2025 and is projected to reach USD 273.3 million by 2034.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The powder segment led the market by form in 2025.

Asia Pacific held the highest market share in 2025.

A key factor driving the market growth is the rising consumption of strontium carbonate in ceramic glazes and frits.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us