Superalloys Market Size, Share & Industry Analysis, By Type (Nickel-Based, Cobalt-Based, Iron-Based, and Others), By Application (Aerospace, Automotive, Oil & Gas, Chemical Processing, Medical Devices, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

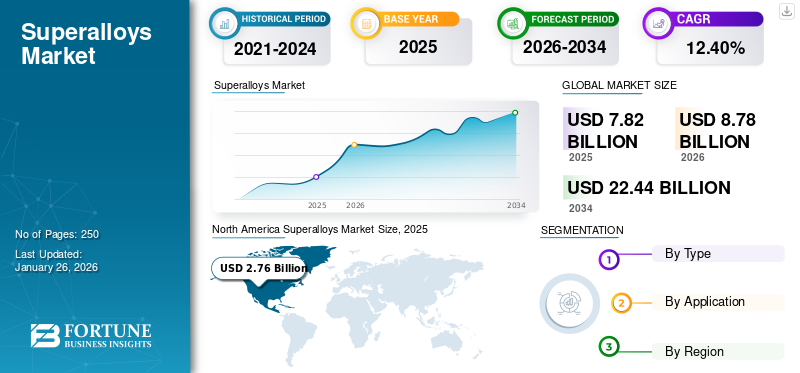

The global superalloys market size was valued at USD 7.82 billion in 2025. The market is projected to grow from USD 8.78 billion in 2026 to USD 22.44 billion by 2034 at a CAGR of 12.40% during the forecast period. North America dominated the superalloys market with a market share of 35% in 2025.

Superalloys, also known as high-performance alloys, are a group of metallic materials engineered to exhibit exceptional mechanical strength, resistance to thermal creep deformation, surface stability, and corrosion or oxidation resistance, particularly at high temperatures. These materials comprise nickel, cobalt, or iron-based matrices, often enhanced with significant amounts of chromium, aluminum, titanium, and other refractory metals such as tungsten, molybdenum, and tantalum. The unique combination of these elements imparts their remarkable properties, making them indispensable in applications where materials are subjected to extreme stress, high temperatures, and aggressive environments. These are characterized by their ability to retain structural integrity and performance under conditions that would cause conventional alloys to fail, such as in jet engines, gas turbines, nuclear reactors, and industrial gas turbines.

The market is driven by several key factors, including the rising demand for high-performance materials in the aerospace, power generation, automotive, and industrial sectors. It is primarily composed of nickel, cobalt, and iron-based alloys. They offer exceptional mechanical strength, corrosion resistance, and high-temperature stability, making them indispensable for applications demanding durability and efficiency in extreme conditions. The market's growth is associated with increasing commercial and military aircraft production, which is extensively used in jet engines, turbine blades, exhaust systems, and other critical components that demand superior thermal resistance and mechanical strength. With the rise in demand for air travel, airline operators and aircraft manufacturers such as Boeing and Airbus are expanding their fleets, further boosting the demand.

Furthermore, government investments and initiatives to strengthen defense and space exploration programs have significantly contributed to market growth. They are widely used in military aircraft, missiles, naval vessels, and space propulsion systems due to their exceptional durability and resistance to harsh environments. As global defense budgets increase and space agencies invest in next-generation space exploration missions, the demand for the product is expected to rise.

Download Free sample to learn more about this report.

Superalloys Market Key Takeaways

- 2025 Market Size: USD 7.82 billion

- 2026 Market Size: USD 8.78 billion

- 2034 Forecast Market Size: USD 22.44 billion

- CAGR: 12.40% from 2026–2034

- North America dominated the superalloys market with a 35.00% share in 2025.

- The nickel-based segment is projected to hold the largest market share of 49.77% in 2026.

- The aerospace segment is expected to account for 65.38% of the market in 2026.

North America

North America accounted for 35.00% of the global market in 2025, reaching USD 2.76 billion, and is projected to grow to USD 3.13 billion in 2026.

Asia Pacific

Asia Pacific generated USD 2.26 billion in 2025, representing 29.00% of the global market, and is expected to reach USD 2.53 billion in 2026.

Europe

Europe contributed USD 1.81 billion in 2025, accounting for 23.00% of global revenue, and is projected to reach USD 2.02 billion in 2026.

U.S.

U.S. The market is projected to reach USD 2.48 billion by 2026.

Japan

Japan The market is projected to reach USD 0.53 billion by 2026.

Read More

SUPERALLOYS MARKET TRENDS

Integration of Additive Manufacturing (AM) Boosts the Market Growth

Traditionally, superalloy manufacturing relied on casting, forging, and machining, often resulting in high material waste and extended production times. However, AM has revolutionized this process by allowing manufacturers to build intricate parts layer by layer, significantly reducing material waste while enhancing its design flexibility. Industries such as aerospace, automotive, and power generation are at the forefront of adopting AM to produce lightweight, high-performance components that meet stringent specifications. For instance, in aerospace, turbine blades, fuel nozzles, and structural components can now be customized and optimized for weight reduction and improved efficiency. Similarly, in the automotive sector, AM enables the production of turbochargers, exhaust valves, and other high-temperature components with enhanced durability and performance. The integration of AM in superalloy production depicts its ability to manufacture parts with complex geometries that were previously impossible or too expensive to achieve using traditional methods. This innovation has significantly improved the mechanical properties, thermal resistance, and overall performance of alloy components, making them more suitable for extreme environments.

Additionally, advancements in AM technologies, such as laser powder bed fusion (LPBF), electron beam melting (EBM), and direct energy deposition (DED), have improved the precision and cost-effectiveness of manufacturing processes, making production more scalable and efficient. The growing adoption of AM production also reduces lead times and enables rapid prototyping, which benefits industries that look for frequent design modifications and high-performance components. For instance, in the power generation sector, AM allows for the quick production of gas turbine components that enhance efficiency and reduce downtime.

MARKET DYNAMICS

MARKET DRIVERS

Emphasis on Recycling and Sustainability to Aid Market Growth

The increasing emphasis on recycling and sustainability drives superalloys market growth as industries face growing environmental concerns and stricter regulatory compliance. Superalloys composed of nickel, cobalt, and chromium are highly valuable due to their exceptional strength, corrosion resistance, and high-temperature performance. Recycling involves reclaiming and refining used or scrap components from aerospace, power generation, and automotive industries, which are extensively used in turbines, jet engines, and exhaust systems. The process helps conserve natural resources and reduces greenhouse gas emissions associated with mining and refining new metals. Additionally, recycling retains superior mechanical properties, making it a cost-effective and sustainable alternative to newly produced alloys. With governments and environmental agencies imposing stricter regulations on waste management and carbon emissions, companies are investing in advanced recycling technologies to improve efficiency, quality, and material recovery rates. Industries are also exploring closed-loop recycling systems, where end-of-life components are collected, processed, and reintroduced into the manufacturing cycle. This approach minimizes waste and aligns with circular economy principles, ensuring that valuable materials are continuously reused rather than discarded. Moreover, advancements in separation and purification technologies enable high-purity metal recovery, further enhancing the viability of recycled materials in critical applications.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Volatility in Raw Material Prices May Hamper the Market Growth

Superalloys rely on high-value metals such as nickel, cobalt, chromium, and molybdenum, which are essential for their exceptional strength, corrosion resistance, and high-temperature performance. However, the prices of these raw materials are highly susceptible to market fluctuations, driven by factors such as geopolitical tensions, supply chain disruptions, mining regulations, and fluctuating demand from key industries, including aerospace, energy, and automotive. The limited supply and geopolitical risks are associated with few critical metals. For example, cobalt, a key component in many nickel-based industries, is predominantly mined in the Democratic Republic of the Congo (DRC), a region often impacted by political instability, labor disputes, and ethical concerns regarding mining practices. Any disruption in supply from these regions can lead to price increases, making it costly for manufacturers to procure essential materials. Similarly, nickel, another crucial element, has experienced price volatility due to regulatory changes in major producing countries, including Indonesia and the Philippines, where export restrictions and environmental policies can impact product availability.

MARKET OPPORTUNITIES

Increasing Demand for High-Temperature Alloys in Next-Generation Aerospace and Energy Applications to Boost Market Growth

The demand for high-temperature resistance is rising, driven by advancements in aerospace, power generation, and space exploration technologies. Modern aircraft, spacecraft, and gas turbines operate under extreme thermal and mechanical stress, requiring materials that can withstand prolonged exposure to high temperatures without compromising structural integrity or performance. In the aerospace sector, next-generation aircraft and supersonic/hypersonic vehicles are being developed to operate at higher speeds and altitudes, necessitating superior thermal stability and oxidation resistance. Military aircraft and space exploration programs also incorporate advanced jet engines, propulsion systems, and spacecraft components, enabling longer operational lifespans and better fuel efficiency. Similarly, the demand for more efficient and cleaner power generation in the energy sector is driving high-temperature adoption in gas turbines, nuclear reactors, and renewable energy applications. Developing ultra-supercritical (USC) coal-fired power plants and next-generation gas turbines requires alloys that can withstand extreme pressure and heat conditions to improve efficiency and reduce emissions. As a result, research and development efforts focus on enhancing alloy compositions by incorporating elements such as rhenium, hafnium, and tantalum, further improving thermal stability, corrosion resistance, and mechanical strength.

MARKET CHALLENGES

High Production Costs and Complex Manufacturing Processes Hampers the Growth

The high cost of raw materials, such as nickel, cobalt, and chromium, poses different challenges for the market growth. Many of these metals are sourced from geopolitically unstable regions, making their supply vulnerable to price fluctuations, export restrictions, and supply chain disruptions. Manufacturers must carefully manage procurement strategies to mitigate cost variations, which can impact profitability. Furthermore, waste management and material efficiency pose additional cost concerns, as intricate production methods often lead to significant material loss. To address these issues, companies invest in advanced manufacturing technologies, such as additive manufacturing (3D printing) and automated production systems, to improve material efficiency, reduce lead times, and lower costs.

Additionally, there are ongoing efforts to develop alternative alloy compositions with lower-cost elements. However, widespread adoption remains limited due to the need for adherence to stringent regulations in aerospace and power generation industries. Despite these advancements, the high cost and complexity of alloy manufacturing continue to pose a significant barrier to market growth.

IMPACT OF COVID-19

The COVID-19 pandemic significantly impacted the global market due to disruptions in supply chains, manufacturing activities, and end-user industries such as aerospace, power generation, automotive, and industrial sectors. The pandemic led to nationwide lockdowns, travel restrictions, labor shortages, and reduced industrial output, severely affecting demand and production. One of the widely hampered sectors was aerospace, a major consumer of superalloys, as the aviation industry experienced a drastic decline in air travel, leading to reduced aircraft production and maintenance. Airlines' delays or cancelation of new aircraft orders during the pandemic directly impacted the jet engine manufacturers' demand for high-performance alloy components. The global supply chain faced significant disruptions due to restricted transportation, plant shutdowns, and raw material shortages. Critical metals such as nickel, cobalt, and chromium are often sourced from geopolitically sensitive regions, causing delays in mining operations and metal refining activities and resulting in price fluctuations and material shortages. Additionally, export restrictions imposed by some countries to safeguard domestic supplies further exacerbated the issue, leading to increased production costs and supply bottlenecks for alloy manufacturers.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Geopolitical Tensions in Countries Involved in Mining Activities Might Affect the Market Significantly

The global market is highly sensitive to trade protectionism and geopolitical tensions, as these advanced materials rely on critical raw materials such as nickel, cobalt, chromium, and molybdenum, which are mined and processed in a few key regions. Superalloys are essential in aerospace, power generation, automotive, and defense industries. They are associated with strategic trade policies, tariffs, export restrictions, and international conflicts that can disrupt supply chains and inflate production costs. One of the biggest challenges in the market is the geopolitical concentration of crucial raw materials. For instance, over 70% of the world’s cobalt supply comes from the Democratic Republic of the Congo (DRC), a nation plagued by political instability, labor disputes, and ethical concerns regarding mining practices. Similarly, Indonesia and the Philippines dominate global nickel production, with both countries having imposed export restrictions at different times to prioritize domestic industries. When major producing nations enact trade barriers, export duties, or outright bans, global supply chains suffer, leading to material shortages, price spikes, and uncertainty for manufacturers.

In addition, rising trade tensions between major economies—such as the U.S. and China or the European Union and Russia have further complicated the global market. For example, the U.S.-China trade war led to tariffs on raw materials, semi-finished products, and industrial components, increasing costs for product manufacturers who depend on imported materials and specialized processing technologies. Trade restrictions on high-tech exports, such as aerospace components and turbine materials, have limited market growth and technology-sharing opportunities, forcing companies to find alternative suppliers or invest in domestic production capabilities.

Furthermore, the Russia-Ukraine conflict has had significant implications for the market, as Russia is a major supplier of nickel and other essential metals. Economic sanctions imposed on Russia by Western nations have disrupted the global nickel supply chain, leading to market volatility, price fluctuations, and sourcing challenges for producers. As sanctions limit trade with Russian suppliers, industries such as aerospace, defense, and power generation that rely on superalloys have been forced to seek alternative supply routes and establish new partnerships, often at higher costs.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

The global market is witnessing significant advancements in research and development (R&D) as industries seek to enhance material performance, improve manufacturing processes, and address sustainability challenges. The R&D trends such as development of next-generation with enhanced strength, higher thermal resistance, and improved corrosion resistance are expected to support market growth. Researchers are exploring novel alloy compositions, including high-entropy alloys (HEAs) and oxide dispersion-strengthened (ODS) superalloys, which offer superior mechanical properties and extended operational life for applications in aerospace, power generation, and defense. Another primary R&D focus is the integration of additive manufacturing (AM) or 3D printing in alloy production. Traditional manufacturing methods, such as casting and forging, are often costly and time-consuming. AM allows for the precise fabrication of complex alloy components, reducing material waste and production costs while improving design flexibility. Advancements in laser powder bed fusion (LPBF) and electron beam melting (EBM) are making it possible to produce high-performance turbine blades, jet engine parts, and automotive components with enhanced efficiency. Sustainability is also a growing area of R&D in the market. With increasing environmental concerns and regulatory pressures, companies invest in recycling technologies to recover nickel, cobalt, and chromium from end-of-life alloy components. Closed-loop recycling systems are being developed to ensure these valuable metals can be reused without compromising material integrity, reducing dependence on raw materials and minimizing environmental impact.

SEGMENTATION ANALYSIS

By Type

Nickel-Based Segment Dominated the Market Owing to its Versatile Properties

Based on Type, the market is segmented into nickel-based, cobalt-based, iron-based, and others.

In 2026, the nickel-based segment is projected to lead the market with a 49.77% share. The segment's growth is associated with its exceptional high-temperature strength, oxidation, and corrosion resistance. These properties make them indispensable in aerospace, gas turbines, and power generation industries, where components such as turbine blades, combustors, and exhaust systems must withstand extreme conditions. The growing demand for fuel-efficient aircraft and the rising adoption of renewable energy sources, including high-performance gas turbines is driving the segment growth.

The cobalt-based segment is expected to grow significantly during the forecast period. Its superior thermal stability, wear, and corrosion resistance drive the demand, making it ideal for medical implants, industrial gas turbines, and aerospace applications. Due to the aging global population, the increasing demand for biomedical devices, such as hip and knee implants, significantly fuels market expansion.

The growth of the iron-based segment is attributed to the expanding energy infrastructure, including coal-fired and nuclear power plants, where high-temperature strength and corrosion resistance are essential. Additionally, increasing research into improving iron-based performance through alloying and manufacturing advancements expands their market potential.

By Application

To know how our report can help streamline your business, Speak to Analyst

Aerospace Accounted for Leading Share Owing to Products' Growing Use

Based on application, the market is segmented into aerospace, automotive, oil & gas, chemical processing, medical devices, and others.

The aerospace segment is expected to account for 65.38% of the market in 2026. This growth is fueled by the demand for high-performance materials that can withstand extreme conditions. With the growing demand for fuel-efficient and lightweight aircraft, manufacturers increasingly use advanced alloys to improve engine efficiency and reduce emissions. Additionally, the rise of the commercial aviation sector, driven by increasing air travel demand and advancements in military and defense aviation, has further fueled the demand.

The automotive segment is set to witness significant growth during the forecast period. The growth is driven by the increasing trend toward lightweight and fuel-efficient vehicles, leading automakers to explore alloy-based components that can withstand higher temperatures and mechanical stress while reducing overall vehicle weight.

The growth of the oil & gas segment is associated with the extensive use of downhole drilling tools, valves, tubing, and components in gas turbines used for power generation in refineries. Nickel-based is vital in ensuring the durability and longevity of equipment exposed to harsh offshore and onshore conditions, where corrosion resistance and mechanical strength are crucial for operational safety and efficiency. The increasing demand for deepwater and ultra-deepwater exploration, coupled with the need for high-performance materials in refining and processing operations, has driven the oil & gas sector adoption.

SUPERALLOYS MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Asia Pacific, Europe, Latin America, and Middle East & Africa.

North America

North America Superalloys Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 2.76 billion in 2025, accounting for 35.00% share, and is expected to reach USD 3.13 billion in 2026. The growth is driven by the strong presence of aerospace, defense, automotive, and power generation industries. The U.S. is a key contributor and home to major aircraft manufacturers, including Boeing, Lockheed Martin, and General Electric (GE Aviation), which require high-performance superalloys for jet engines, turbine blades, and structural components. Additionally, the region has a well-established additive manufacturing (AM) sector, enabling advanced product production. The renewable energy and gas turbine industry also contribute to market growth, with increasing investments in clean energy and high-efficiency power plants. The U.S. market is valued at USD 2.48 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The Asia Pacific market accounted for USD 2.26 billion in 2025, representing 29.00% of the global industry, and is expected to reach USD 2.53 billion in 2026. Asia Pacific is expected to grow significantly over the forecast period, driven by the expanding aerospace, automotive, and energy sectors. Countries such as China, India, and Japan are making substantial investments in indigenous aircraft production, space exploration, and high-speed rail—all of which require superalloys. China is ramping up its defense and aerospace capabilities, increasing demand for nickel-based and cobalt-based. The region also has a booming automotive industry, with rising production of electric vehicles (EVs) and hybrid cars, where alloys are used in battery components and thermal management systems. Additionally, the growing energy demand in the Asia Pacific is driving investments in advanced gas turbines and nuclear reactors, further boosting product consumption in the region. The Japan market is valued at USD 0.53 billion by 2026. The China market is valued at USD 0.75 billion by 2026. The India market is valued at USD 0.55 billion by 2026.

Europe

In 2025, Europe generated USD 1.81 billion, contributing 23.00% to global market revenue, and is projected to grow to USD 2.02 billion in 2026. The region is at the forefront of sustainable aviation initiatives, promoting research into lighter, fuel-efficient aircraft engines that rely on advanced alloys. The automotive industry is crucial, especially in Germany, France, and the U.K., as they are used in high-performance engines and turbochargers. The region’s strict environmental regulations encourage the development of recyclable and eco-friendly solutions to reduce carbon emissions and promote circular economy practices. The UK market is valued at USD 0.43 billion by 2026. The Germany market is valued at USD 0.7 billion by 2026.

Latin America

Latin America contributed 7.60% to the global market in 2025, with a valuation of USD 0.59 billion, and is projected to reach USD 0.66 billion in 2026. In Latin America, the growing demand for the product is driven by the aerospace, energy, and mining industries. Brazil and Mexico are key contributors, with Boeing and Embraer maintaining aerospace operations in the region. The power generation industry, including hydropower and thermal energy plants, also relies on superalloys for turbines and heat exchangers.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.4 billion, accounting for 5.00% of the worldwide market, and is projected to grow to USD 0.44 billion in 2026. The Middle East & Africa region is witnessing steady demand due to energy, aviation, and industrial infrastructure investments. The region’s oil and gas sector relies upon high-temperature and corrosion-resistant components used in drilling and refining operations. Additionally, Gulf countries, including the UAE and Saudi Arabia, invest in aerospace and defense manufacturing, thus increasing demand for aircraft engines and military applications.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Adopting Various Business Expansion Strategies to Maintain their Market Positions

Mishra Dhatu Nigam Limited, Sunflag Iron & Steel Co. Ltd, Doncasters Group, and Cannon Muskegon are a few key players in the market. These players mainly operate based on the product's pricing and application features. Companies are entering into partnerships to enhance product portfolios, increase their market share, and gain a competitive edge.

LIST OF KEY SUPERALLOY COMPANIES PROFILED

- Mishra Dhatu Nigam Limited (India)

- Sunflag Iron & Steel Co. Ltd (India)

- Doncasters Group (U.K.)

- Cannon Muskegon (U.S.)

- Precision Castparts Corp. (U.S.)

- Nippon Yakin Kogyo Co., Ltd. (Japan)

- VDM Metals (Germany)

- ATI (U.S.)

- HAYNES INTERNATIONAL (U.S.)

- CRS Holdings, LLC (U.S.)

- AMG Chrome Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2024: EOS has expanded its AM material portfolio with nickel-based EOS IN738 and EOS K500 powders (Courtesy EOS). Two nickel-based super alloy powders were added to its Laser Beam Powder Bed Fusion (PBF-LB) additive manufacturing machines. EOS Nickel Alloy IN738 and EOS Nickel Alloy K500 were commercially available for the EOS M 290 family of machines from December 2024 and available for the EOS M 400-4 in the first half of 2025.

- October 2023: Mitsubishi Materials Co., Ltd. has launched a new grade, MV9005, for turning heat-resistant superalloys. For machining Ni-based heat-resistant alloys for the aviation industry, coated inserts are widely used in the medium finishing area where the tool life for machining large parts with only one corner is required.

- December 2021: Aperam acquired ELG, a stainless steel and super alloys recycling company. Both companies will work toward a closed-loop economy in the stainless steel and super alloys industry.

- October 2021: BEAMIT Group developed a printing process for a new superalloy, René 80-RAM1, featuring a high melting point and excellent oxidation resistance at high temperatures.

- June 2020: Protolabs launched a new cobalt chrome superalloy for its metal laser sintering process, targeting the oil & gas sector due to its heat, wear, and corrosion-resistant properties.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, sources, and product applications. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 12.40% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 7.82 billion in 2025 and is projected to reach USD 22.44 billion by 2034.

Recording a CAGR of 12.40%, the market is slated to exhibit steady growth during the forecast period.

The aerospace application segment led in 2025.

In 2025, the North America market size stood at USD 2.76 billion.

Increasing demand for high-temperature alloys in next-generation aerospace and energy applications will aid market growth.

Rising demand from the aerospace industry is anticipated to drive product adoption.

Mishra Dhatu Nigam Limited, Sunflag Iron & Steel Co. Ltd, Doncasters Group, and Cannon Muskegon are major players in the global market.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us