Sustainable Automotive Manufacturing Market Size, Share & Industry Analysis, By Propulsion Type (Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and others), By Sustainable Material Type (Recycled Metals, Recycled Plastics, Bio-based Plastics & Polymers, and Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers & Three-Wheelers, and Others), By Application Area (Carbon Emission Reduction, Waste Management & Recycling, and Others), By Manufacturing Technology (Energy-efficient Manufacturing Systems, and Others), and Regional Forecast, 2026-2034

Sustainable Automotive Manufacturing Market Size and Future Outlook

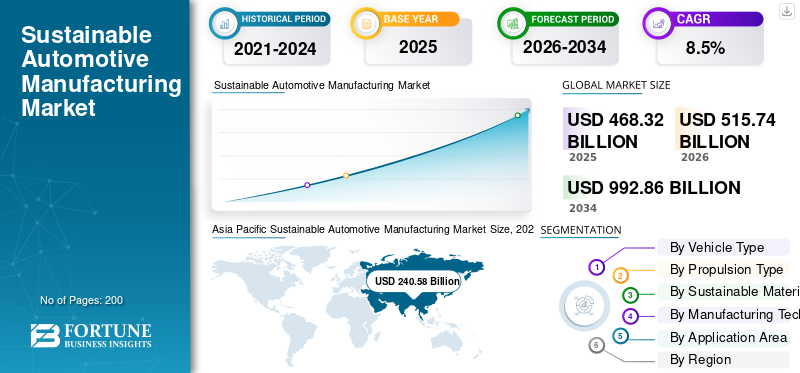

The global sustainable automotive manufacturing market size was valued at USD 468.32 billion in 2025. The market is projected to grow from USD 515.74 billion in 2026 to USD 992.86 billion by 2034, exhibiting a CAGR of 8.5% over the forecast period. Asia Pacific dominated the sustainable automotive manufacturing market with a market share of 51.37% in 2025.

Sustainable automotive manufacturing refers to the production of vehicles, components, and materials through low-emission, resource-efficient, and socially responsible methods. It includes renewable-energy factories, recycled and bio based materials, smart production systems, water and waste reduction, battery recycling, ethical sourcing, and lifecycle-focused design for reduced environmental impact across the automotive value chain. Stricter emission regulations, EV production expansion, OEM net-zero targets, rising adoption of recycled materials, battery circularity, and factory energy-efficiency programs drive growth. Automakers are shifting toward renewable electricity, low-carbon steel and aluminum, water reuse, and digital manufacturing to reduce cost, comply with climate rules, and meet consumer sustainability expectations.

Major players include Toyota, Tesla, BYD, Volkswagen, BMW, Mercedes-Benz, Hyundai, General Motors, Ford, Stellantis, Honda, Nissan, Volvo Cars, and Renault. These players are showing an incline toward EV-focused production, renewable-powered plants, battery recycling, supplier decarbonization, recycled materials, circular-economy models, and smart-factory modernization.

Download Free sample to learn more about this report.

SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET TRENDS

Circular Manufacturing and Low-Carbon Factories to Reshape Automotive Production

Automakers are moving from simple energy-saving initiatives to circular, low-carbon production systems that combine renewable power, recycled materials, battery reuse, and digital factory monitoring. This trend is visible in premium and mass-market manufacturing networks, where companies are redesigning production sites to reduce Scope 1 and Scope 2 emissions while also cutting upstream material emissions. Recycled aluminum, low-carbon steel, renewable electricity, and closed-loop battery material recovery are becoming central to factory planning. In 2024, Volkswagen reported that its decarbonization levers include e-mobility, energy supply conversion, energy efficiency, and value-chain decarbonization, while targeting net CO₂e neutrality at production sites by 2040. In December 2025, BMW commissioned its Cell Recycling Competence Center in Salching for the direct recycling of battery materials.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

EV Expansion and Net-Zero Commitments to Accelerate Sustainable Manufacturing Demand

The electric vehicle growth is pushing automakers to redesign factories, source cleaner materials, and localize battery manufacturing. BEV and hybrid production require new assembly systems, battery packs, thermal management systems, electronics, and recycling processes, thereby increasing the demand for sustainable manufacturing technologies. OEM net-zero targets also create pressure to decarbonize suppliers, use renewable electricity, and improve plant energy efficiency. The rising vehicle electrification and the need to lower each vehicle's lifecycle footprint are significant factors driving sustainable automotive manufacturing market growth.

- In 2024, the International Energy Agency (IEA) reported that electric car sales exceeded 17 million units, with China accounting for more than 11 million. Furthermore, during the same year, Volkswagen stated that BEVs were manufactured at 18 sites across Europe, China, and the U.S.

MARKET RESTRAINTS

High Capital Costs and Supply Chain Complexity May Limit Faster Adoption

Sustainable automotive manufacturing requires large upfront investment in renewable energy systems, energy-efficient equipment, battery recycling, digital factories, and low-carbon materials. These investments can be difficult for smaller suppliers, especially where margins are tight, and electricity, battery materials, or recycling infrastructure remain costly. Another restraint is supplier complexity. Automakers depend on steel, aluminum, plastics, batteries, semiconductors, logistics, and mining networks, which slow full lifecycle decarbonization. Sustainability targets also require verification, traceability, and reporting systems, which add to the administrative burden. In 2024, Volkswagen reported that value-chain decarbonization covers raw material extraction, material manufacturing, supplier processes, own production, use phase, and end-of-life dismantling, showing the breadth of the challenge. In 2024, Mercedes-Benz highlighted battery cells, steel, and aluminum as CO₂-intensive supplier focus areas.

MARKET OPPORTUNITIES

Battery Recycling and Secondary Materials to Create New Growth Pathways

Battery recycling, remanufacturing, and the use of secondary materials offer significant opportunities as EV growth increases the demand for lithium, nickel, cobalt, graphite, aluminum, and copper. Recycling reduces dependence on mined raw materials, supports domestic supply chains, and lowers manufacturing emissions. Automakers can also reduce geopolitical risk by designing vehicles for disassembly, reduce waste by material recovery, and reuse. Opportunities are especially strong in battery hubs, EV plants, and regions that support circular-economy regulation. In September 2024, the U.S. Department of Energy announced more than USD 3 billion for 25 battery manufacturing and recycling projects across 14 states to support domestic battery supply chains. In December 2025, BMW launched direct recycling to feed recovered battery materials back into cell production.

MARKET CHALLENGES

Measuring True Sustainability across the Full Vehicle Lifecycle Remains Difficult, Creating Challenges for Market Expansion

The main challenge is proving that manufacturing involves genuinely sustainable materials across the full vehicle lifecycle, not only at the final assembly plant. A vehicle may be built in a renewable-powered factory but still carry high embedded emissions from battery cells, steel, aluminum, plastics, mining, and transport. Companies must, therefore, measure supplier emissions, material origins, recycling rates, factory energy use, water use, and end-of-life recovery using consistent methods. This is difficult across global supplier networks and different regulatory systems. In 2024, Volkswagen described its decarbonization index as a lifecycle measure covering regions including Europe, China, and the U.S. In 2024, Mercedes-Benz said that suppliers representing around 90% of its annual purchasing volume had signed an Ambition Letter committing to net carbon-neutral production materials by 2039.

Segmentation Analysis

By Propulsion Type

Established Manufacturing Infrastructure to Impel ICE Vehicles Segment Leadership

Based on propulsion type, the market is segmented into Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), Fuel Cell Electric Vehicles (FCEVs), and ICE vehicles.

The ICE vehicles segment dominates the global sustainable automotive manufacturing market share as conventional vehicle platforms still account for the largest share of worldwide automotive production and supplier ecosystems. Automakers continue to integrate sustainable manufacturing sustainable practices such as renewable-powered plants, recycled metals, low-carbon steel, and energy-efficient assembly systems, into ICE vehicle production lines as they gradually transition toward electrification. Large-scale manufacturing capacity, mature component supply chains, and widespread consumer demand support the segment’s continued leadership, especially in emerging economies where EV adoption remains comparatively slower.

The Battery Electric Vehicles (BEVs) segment is projected to grow at a CAGR of 16.4% over the forecast period. In October 2024, Toyota announced expanded low-carbon manufacturing initiatives across its global vehicle production operations, including emissions-reduction and renewable-energy integration initiatives.

By Sustainable Material Type

Circular Metal Recovery and Lightweight Vehicle Production to Bolster Recycled Metals Segment Growth

Based on sustainable material type, the market is segmented into recycled metals, recycled plastics, bio-based plastics & polymers, natural fiber composites, and eco-friendly interior materials.

The recycled metals segment dominates the market given that steel and aluminum remain the primary structural materials used in the automotive sector manufacturing worldwide. Automakers increasingly use recycled aluminum and steel to reduce production emissions, improve material efficiency, and support circular-economy objectives without compromising structural performance. Growing pressure to lower embedded carbon emissions in vehicle manufacturing has accelerated the adoption of secondary metals across EV and conventional vehicle production. Recycled metals also help manufacturers reduce their reliance on raw materials and the energy consumption associated with primary metal extraction.

The bio-based plastics & polymers segment is projected to grow at a CAGR of 11.3% over the forecast period. In April 2024, Mercedes-Benz expanded the use of secondary raw materials and low-CO₂ aluminum within vehicle manufacturing operations as part of its Ambition 2039 strategy.

By Vehicle Type

Large-Scale Manufacturing and Deployment to Propel Passenger Cars Segment Growth

Based on vehicle type, the market is segmented into passenger cars, commercial vehicles, two-wheelers & three-wheelers, and off-highway vehicles.

The passenger cars dominates the global market given that these cars account for the largest share of worldwide automotive production and EV deployment. Automakers are heavily investing in low-emission assembly plants, renewable-powered manufacturing facilities, lightweight materials, and battery-integrated production systems primarily for passenger vehicle platforms. Sustainability-focused innovations, such as recycled interiors, smart manufacturing technologies, and energy-efficient paint shops, are widely implemented first in passenger vehicle production due to higher manufacturing volumes and faster consumer adoption. Strong EV penetration across Europe, China, and North America further supports segment dominance.

The two-wheelers & three-wheelers segment is projected to grow at a CAGR of 11.8% over the forecast period. In March 2024, BMW Group stated that its global production network continued expanding low-carbon manufacturing practices for next-generation passenger vehicle production facilities.

To know how our report can help streamline your business, Speak to Analyst

By Application Area

Industrial Decarbonization Programs to Accelerate Carbon Emission Reduction Segment Growth

Based on the application area, the market is segmented into carbon emission reduction, waste management & recycling, water conservation, sustainable supply chain management, and battery recycling & remanufacturing.

The carbon emission reduction segment dominates the market as governments, investors, and automotive OEMs are prioritizing factory decarbonization and lifecycle emission reduction strategies. Manufacturers are increasingly deploying renewable electricity, low-carbon materials, energy-efficient production systems, and digital energy management tools to reduce operational emissions across assembly plants and supplier networks. Net-zero commitments and tightening global climate and strict environmental regulations continue to drive investment toward emissions-focused manufacturing upgrades. Automotive companies are also targeting reductions in Scope 1, Scope 2, and Scope 3 emissions across their production ecosystems.

The battery recycling & remanufacturing segment is projected to grow at a CAGR of 13.9% over the forecast period. In July 2024, Volvo Cars announced expanded use of renewable energy and climate-neutral production initiatives aligned with its long-term net-zero manufacturing roadmap.

By Manufacturing Technology

Factory Energy Optimization Systems to Push Energy-Efficient Manufacturing Segment Growth

Based on manufacturing technology, the market is segmented into energy-efficient manufacturing systems, smart manufacturing/Industry 4.0, green robotics & automation, additive manufacturing (3D printing), and closed-loop manufacturing systems.

The energy-efficient manufacturing systems segment dominates the market given that automotive manufacturers prioritize reducing factory operating costs, electricity consumption, and production-related emissions. Technologies such as energy-efficient HVAC systems, waste heat recovery, smart lighting, renewable energy integration, and intelligent process optimization are widely deployed across automotive plants globally. These systems help manufacturers comply with sustainability regulations while improving long-term production efficiency and profitability. Energy-efficient manufacturing also supports corporate net-zero targets and ESG performance improvement initiatives.

The smart manufacturing/Industry 4.0 segment is projected to grow at a CAGR of 10.4% over the forecast period. In June 2024, Ford highlighted AI-enabled manufacturing efficiency and energy-optimization programs as part of its sustainable production modernization initiatives.

SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

NORTH AMERICA

Asia Pacific Sustainable Automotive Manufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintains a strong position in the global market due to advanced automotive industrial automation, EV manufacturing expansion, battery localization initiatives, and large-scale factory modernization investments. The region benefits from strict emission regulations, renewable-energy integration across manufacturing plants, and growing investment in sustainable supply chains. The U.S. and Mexico continue attracting EV and battery production projects, while Canada strengthens low-carbon automotive component manufacturing. The rising deployment of smart manufacturing technologies, recycled materials, and energy-efficient assembly systems further supports regional growth. Expanding battery recycling infrastructure and increasing corporate net-zero commitments are also accelerating the adoption of sustainable manufacturing across the North American automotive ecosystem.

U.S. SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

The U.S. dominates the North America market and is expected to reach USD 64.68 billion in 2026. Growth is supported by EV manufacturing expansion, battery gigafactory investments, renewable-powered production facilities, and increasing adoption of Industry 4.0 technologies. Federal clean-energy incentives, supplier decarbonization programs, and automotive recycling investments continue strengthening the country’s sustainable manufacturing ecosystem.

EUROPE

Europe is one of the most sustainability-focused automotive manufacturing regions globally, driven by strict carbon regulations, circular-economy initiatives, and advanced green manufacturing technologies. Automakers across the region are increasingly investing in renewable-powered production plants, low-carbon materials, battery recycling systems, and digital manufacturing optimization. Strong EV production growth, supplier decarbonization requirements, and sustainable supply chain regulations continue accelerating industrial transformation. Germany, France, and the U.K. remain major contributors to regional growth, while Eastern Europe is emerging as a cost-efficient hub for EV manufacturing and battery components. Europe also leads in the adoption of recycled metals, lightweight materials, and lifecycle-based sustainability frameworks.

U.K. SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

The U.K. market is projected to reach USD 12.76 billion in 2026, supported by EV assembly investments, battery gigafactory expansions, and the adoption of advanced smart manufacturing. Government net-zero initiatives, renewable energy integration, and sustainable supply chain programs continue accelerating industrial modernization. Increasing localization of battery materials and digital manufacturing technologies further strengthens long-term market growth potential.

GERMANY SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

Germany accounted for nearly 27.6% share of the European market due to its strong automotive production ecosystem, premium vehicle manufacturing leadership, and extensive factory automation infrastructure. Large-scale EV investments, renewable-powered production facilities, the adoption of low-carbon steel, and advanced recycling technologies continue to support market dominance. Strong supplier networks and industrial innovation capabilities further reinforce Germany’s leadership position.

ASIA PACIFIC

Asia Pacific dominates the global market due to its massive automotive production base, rapid expansion of EV manufacturing, concentration of battery supply chains, and extensive industrial infrastructure. China, Japan, India, and South Korea collectively account for the majority of global EV and automotive component production. Government incentives supporting clean manufacturing, renewable energy integration, localized battery production, and sustainable supply chain development continue to accelerate market growth. The region also benefits from the rising adoption of smart factories, recycled materials, energy-efficient production systems, and battery recycling technologies. Increasing two-wheeler electrification and large-scale passenger vehicle production further strengthen Asia Pacific’s market leadership.

CHINA SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

China dominates the Asia Pacific market with nearly 60.0% regional share due to its unmatched EV production scale, battery manufacturing leadership, and large automotive supplier ecosystem. Strong government support for green manufacturing, renewable-powered factories, battery recycling, and industrial electrification continue driving market expansion. China’s leadership in low-carbon automotive production and advanced manufacturing technologies further strengthens its dominant regional position.

INDIA SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

In Asia Pacific, the India market is projected to register the highest CAGR of 13.0% over the analysis period. Growth is supported by rapid two-wheeler electrification, expanding automotive production capacity, increasing renewable-energy integration, and government incentives promoting local EV manufacturing. Rising investments in battery assembly, smart manufacturing systems, and sustainable supply chains are accelerating the country’s industrial transformation.

JAPAN SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

The Japan market is projected to reach USD 29.86 billion in 2026, supported by advanced hybrid and EV manufacturing technologies, leadership in industrial automation, and a strong recycling infrastructure. The country continues investing in hydrogen mobility, low-carbon materials, and energy-efficient production systems. Strong OEM sustainability targets and high adoption of smart manufacturing technologies continue supporting long-term market growth.

SOUTH AMERICA

South America is gradually strengthening its position in the market through increased industrial modernization, biofuel integration, expanded EV assembly, and the adoption of recycled materials. Brazil and Argentina remain the region’s primary automotive production centers, while Chile supports the development of the battery-material supply chain. Automakers are increasingly investing in energy-efficient factories, integrating renewable electricity, and developing sustainable logistics systems to improve competitiveness and meet global sustainability expectations. The rising demand for affordable electric mobility, especially in urban transportation and two-wheelers, is further supporting the regional market growth. Expanding circular-economy initiatives and sustainable material use continue to drive long-term industry transformation across South America.

BRAZIL SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

Brazil dominates the South America market growth with nearly 59.9% regional share, driven by its large automotive production base, leadership in biofuel integration, and expanding EV assembly operations. Strong industrial infrastructure, the increasing use of recycled materials, and the adoption of renewable energy across automotive manufacturing facilities continue to support market growth. Government industrial modernization initiatives further strengthen Brazil’s dominant regional position.

MIDDLE EAST & AFRICA

The Middle East & Africa market is expanding steadily due to increasing industrial diversification, renewable energy investments, and the gradual development of the EV ecosystem. Countries across the region are modernizing manufacturing infrastructure, improving industrial sustainability standards, and investing in localized automotive assembly capabilities. The UAE, Saudi Arabia, and South Africa are emerging as major regional growth centers due to rising smart manufacturing adoption, industrial automation, and low-carbon mobility initiatives. Growing interest in battery recycling, renewable-powered production facilities, and sustainable logistics systems is also supporting market development. Government economic diversification strategies continue to encourage long-term investment in advanced automotive manufacturing technologies.

UAE SUSTAINABLE AUTOMOTIVE MANUFACTURING MARKET

The UAE market is projected to grow at a CAGR of 16.2% during the forecast period, driven by the rapid adoption of smart manufacturing, the integration of renewable energy, and industrial diversification initiatives. Investments in EV infrastructure, clean mobility ecosystems, and sustainable logistics systems continue to support market expansion. A strong government focuses on low-carbon industrial transformation, and advanced manufacturing technologies further accelerate long-term, sustainable growth in automotive manufacturing.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Deploying Smart Manufacturing Technologies and Closed-loop Recycling Systems to strengthen their Standing

The global market is moderately consolidated, with market trends driven by large automotive OEMs, industrial automation providers, battery manufacturers, and sustainable material suppliers. Major players, including Toyota, Volkswagen Group, Tesla, BYD, BMW Group, Hyundai Motor Group, Mercedes-Benz Group, Magna International, Bosch, and Stellantis, compete through EV-focused manufacturing expansion, renewable-powered factories, battery recycling systems, and digitalized production ecosystems. Companies are strengthening their competitive positioning by integrating smart manufacturing technologies, low-carbon materials, closed-loop recycling systems, and AI-driven factory-optimization tools into automotive production networks.

Strategic partnerships with battery suppliers, renewable-energy providers, and recycling firms are increasingly used to secure sustainable supply chains and reduce lifecycle emissions. Localized EV manufacturing, supplier decarbonization initiatives, and investments in circular economy infrastructure are also becoming major competitive differentiators across developed and emerging automotive markets.

LIST OF KEY SUSTAINABLE AUTOMOTIVE MANUFACTURING COMPANIES PROFILED

- Toyota Motor Corporation (Japan)

- Tesla, Inc. (U.S.)

- BYD Company Ltd. (China)

- Volkswagen AG (Germany)

- BMW Group (Germany)

- Mercedes-Benz Group AG (Germany)

- Ford Motor Company (U.S.)

- General Motors Company (U.S.)

- Hyundai Motor Company (South Korea)

- Kia Corporation (South Korea)

- Volvo Car Corporation (Sweden)

- Stellantis N.V. (Netherlands)

- Nissan Motor Co., Ltd. (Japan)

- Honda Motor Co., Ltd. (Japan)

- Renault Group (France)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Stellantis launched its Circular Economy Dismantling Center in Casablanca, Morocco, the company’s first such facility in the Middle East and Africa and third worldwide. Operated under SUSTAINera, the site supports vehicle dismantling, the recovery of reusable components, parts reuse, recycling, and the development of Morocco’s sustainable automotive ecosystem.

- May 2026: Toyota’s Tahara plant in Japan achieved carbon neutrality, becoming Toyota’s first carbon-neutral facility. The site uses renewable energy, including wind turbines and solar panels, and supports Toyota’s broader sustainable manufacturing goal, while its European operations aim to achieve carbon-neutral owned facilities by 2030.

- April 2026: Scottish Leather Group opened a 75,000 sq. ft Glasgow facility to manufacture BioPRO, a protein-based, recoverable molded foam for automotive seating and other transport interiors. The site strengthens Bridge of Weir Leather’s ability to scale sustainable seating materials for global carmakers and reduce fossil-based content.

- April 2026: Mercedes-Benz Trucks unveiled the reECONIC concept with 32 partners, demonstrating a battery-electric waste-collection vehicle made partly from recycled, natural, and bio-based materials. The initiative demonstrated the feasibility of circular manufacturing and indicated that recycled-content production could theoretically reduce CO₂-equivalent emissions across truck components and manufacturing processes.

- February 2026: Aqua Metals and American Battery Factory signed a non-binding MOU to evaluate co-locating lithium-ion battery recycling beside ABF’s planned Tucson cell operations. The collaboration would recycle manufacturing scrap and return battery-grade lithium carbonate for U.S. battery production, supporting circular supply, lower waste, and localized sustainable manufacturing.

REPORT COVERAGE

The global sustainable automotive manufacturing market analysis provides an in-depth study of the market size and forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on rapid technological advancements, new product launches, key industry developments, strategic partnerships, mergers, and acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market shares, emerging opportunities, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Propulsion Type, By Sustainable Material Type, By Manufacturing Technology, By Application Area, and By Region |

| By Propulsion Type |

|

| By Sustainable Material Type |

|

| By Vehicle Type |

|

| By Application Area |

|

| By Manufacturing Technology |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 468.32 billion in 2025 and is projected to reach USD 992.86 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 240.58 billion.

The market is expected to grow at a CAGR of 8.5% over 2026 to 2034.

The passenger cars segment leads the market share by vehicle type.

Stricter emission regulations, EV production expansion, OEM net-zero targets, rising adoption of recycled materials, and battery circularity are key factors driving the market.

Key market players include Toyota, Tesla, BYD, Volkswagen, BMW, Mercedes-Benz, Hyundai, General Motors, Ford, and Stellantis.

The Asia Pacific region accounts for the largest share of the market.

North America, Europe, Asia Pacific, South America, and the Middle East & Africa have been considered in the market report.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us