Sustainable Films for Packaging Market Size, Share & Industry Analysis, By Material (Polylactic Acid (PLA), Recycled Polyethylene Terephthalate (rPET), Bio-Polyethylene (Bio-PE), Polypropylene (PP), and Others), By End Use (Food & Beverages, Pharmaceuticals, Consumer Goods, and Others), and Regional Forecast, 2026-2034

Sustainable Films for Packaging Market Size and Future Outlook

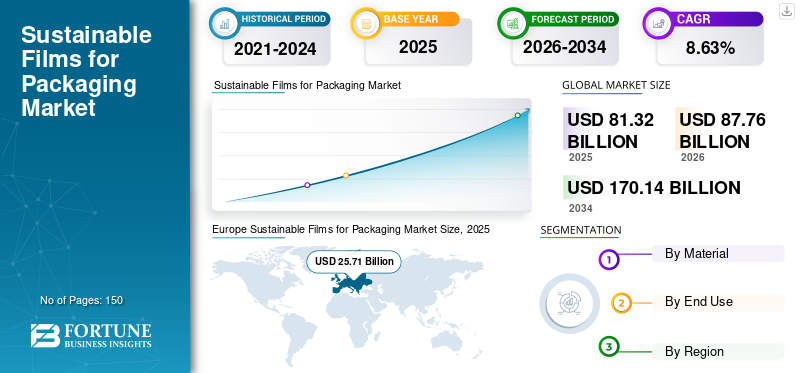

The global sustainable films for packaging market size was valued at USD 81.32 billion in 2025. The market is projected to grow from USD 87.76 billion in 2026 to USD 170.14 billion by 2034, exhibiting a CAGR of 8.63% during the forecast period. Europe dominated the sustainable films for packaging market with a market share of 31.62% in 2025.

The global market encompasses the sector dedicated to the creation, manufacturing, and marketing of environmentally friendly flexible film materials intended for packaging purposes. The increasing regulatory pressure regarding single use plastics, heightened consumer interest in eco-friendly packaging solutions, and corporate pledges toward achieving carbon neutrality and circular economy objectives are greatly propelling the global uptake of recyclable, biodegradable films, and bio based sustainable packaging films.

Furthermore, many key industry players, such as Amcor, Mondi, and Sealed Air, operating in the market, are focusing on developing innovative products and conducting R&D, and contributing to the global market share.

Download Free sample to learn more about this report.

SUSTAINABLE FILMS FOR PACKAGING MARKET TRENDS

Transition Toward Mono-Material Recyclable Structures is an Emerging Trend in Market

A significant trend in the worldwide sustainable films for packaging sector is the swift transition from multi-layer, hard-to-recycle laminates to mono-material recyclable film structures. Brand owners are progressively rethinking flexible packaging designs by utilizing polyethylene (PE) or polypropylene (PP) based mono-material solutions to meet circular economy objectives and comply with extended producer responsibility (EPR) regulations. Recent advancements in barrier coatings, compatibilizers, and high-performance resins now allow mono-material films to provide oxygen, moisture, and aroma barrier characteristics that are on par with traditional multilayer laminates. This shift is particularly noticeable in the packaging of food, personal care products, and e-commerce, where claims of recyclability significantly affect consumer purchasing choices. As recycling infrastructure continues to enhance globally, the demand for standardized, easily recyclable film solutions is steadily increasing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Push Against Conventional Plastics are Driving Market Growth

Stringent government regulations that limit single-use plastics and require recyclable or compostable packaging formats serve as a key driver for the sustainable films for packaging market growth. Regions including Europe, North America, and certain areas of Asia Pacific are enacting plastic taxes, mandates for minimum recycled content, and Extended Producer Responsibility (EPR) schemes that have a direct impact on the selection of packaging materials. These regulatory frameworks are urging Fast-Moving Consumer Goods (FMCG) companies and retailers to transition toward recyclable, bio-based, and compostable films in order to ensure compliance and avoid incurring financial penalties. Moreover, global sustainability commitments from multinational brands are further intensifying these regulatory pressures. As the timelines for compliance become more stringent, packaging converters and film manufacturers are hastening their investments in sustainable material innovations to align with the changing legislative requirements.

MARKET RESTRAINTS

Higher Production Costs Compared to Conventional Films Impedes Market Growth

One of the primary constraints in the sustainable films for packaging sector is the comparatively higher expense associated with bio-based polymers, recycled resins, and advanced recyclable structures when contrasted with traditional fossil-fuel-based plastics. Sustainable raw materials frequently encounter challenges in supply chains, reduced economies of scale, and increased processing complexity, which contribute to higher manufacturing costs. Furthermore, investments in research and development, certification, and performance testing add to the overall financial burden. In price-sensitive markets, especially in developing regions, this cost disparity can hinder adoption. Additionally, small and mid-sized packaging converters may find it difficult to meet the capital expenditure demands for new extrusion or recycling-compatible technologies, thereby restricting widespread market penetration in specific areas.

MARKET OPPORTUNITIES

Rising Demand from E-Commerce and Flexible Food Packaging Offers Impending Growth Opportunities

The growth of e-commerce and the consumption of packaged foods offers a significant opportunity for manufacturers of sustainable films. Lightweight and flexible films are favored for online retail packaging due to their durability, cost-effectiveness, and reduced transportation emissions when compared to rigid formats. Simultaneously, the rising demand for convenience foods, ready-to-eat meals, and portion-controlled packaging is driving the need for high-performance sustainable barrier films. Brands are actively pursuing recyclable and compostable flexible solutions to improve their sustainability credentials while ensuring product protection and shelf life are not compromised. Emerging economies with growing middle-class populations further enhance this opportunity, resulting in strong long-term growth prospects for innovative sustainable film technologies.

MARKET CHALLENGES

Performance Limitations and Recycling Infrastructure Gaps is a Major Challenge to Market Growth

Despite the strong demand, the sustainable films market continues to face considerable challenges due to performance limitations and insufficient recycling infrastructure. Certain bio-based and compostable films may not yet provide the same level of mechanical strength, heat resistance, or barrier performance as traditional multi-layer plastics in high-demand applications. Moreover, the lack of standardized recycling systems and composting facilities in numerous countries hampers effective end-of-life management. Even recyclable films can find their way to landfills owing to collection inefficiencies or consumer uncertainty about proper disposal methods. To ensure that sustainable film solutions deliver their intended environmental benefits, it is essential to harmonize material standards, enhance waste management infrastructure, and educate consumers.

Segmentation Analysis

By Material

PLA Segment Dominates Due to its Renewable Source and Industrial Production Capability

Based on the material, the market is divided into Polylactic Acid (PLA), Recycled Polyethylene Terephthalate (rPET), Bio-Polyethylene (Bio-PE), Polypropylene (PP), and others.

Polylactic Acid (PLA) segment is expected to account for the largest share of the market. PLA is the leading material in the sustainable packaging films market, mainly due to its renewable source, ability to be industrially composted, and its strong connection to global sustainability goals. Sourced from plant-derived materials such as corn starch and sugarcane, PLA greatly diminishes reliance on fossil fuels and reduces carbon emissions when compared to traditional plastics. The rising consumer demand for bio-based packaging, along with heightened investments in biopolymer manufacturing capabilities, further solidifies PLA's dominant role in the sustainable films sector.

The Recycled Polyethylene Terephthalate (rPET) segment is expected to grow at a CAGR of 8.65% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Food & Beverages Dominate Due to Heavy Dependence on Flexible Packaging

Based on the end use, the market is segmented into food & beverages, pharmaceuticals, consumer goods, and others.

The food & beverages segment is expected to hold a dominant sustainable films for packaging market share over the forecast period. The food and beverages sector leads the global market for sustainable packaging films, primarily due to its heavy dependence on flexible packaging for safeguarding products, ensuring preservation, and providing convenience. As the demand for ready-to-eat meals, snacks, frozen foods, and beverages continues to rise, the volume of packaging consumption in this sector remains notably high. Furthermore, food brands encounter significant regulatory oversight and consumer demand to implement recyclable, compostable, and bio-based materials. The commitment to corporate sustainability and the goals for reducing plastic usage among leading food manufacturers further drive the adoption of sustainable films within this sector.

The pharmaceuticals segment is projected to grow at a CAGR of 8.60% over the forecast period.

Sustainable Films for Packaging Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Sustainable Films for Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe is the dominant region and is projected to grow at 8.33% over the coming years and reach a valuation of USD 25.71 billion by 2025. The market in Europe is largely influenced by strict regulations set forth by the EU Green Deal and directives concerning packaging waste. A heightened awareness of environmental impact among consumers, coupled with a robust recycling infrastructure, fosters a growing demand for films that are either compostable or recyclable. Additionally, the imposition of mandatory recycled content requirements and plastic taxes acts as a catalyst for innovation and the substitution of materials.

U.K. Sustainable Films for Packaging Market

The U.K. market in 2025 was recorded at USD 4.82 billion, representing approximately 5.93% of global revenues.

Germany Sustainable Films for Packaging Market

Germany’s market reached approximately USD 5.63 billion in 2025, equivalent to around 6.92% of global sales.

Asia Pacific

Asia Pacific reached USD 20.66 billion in 2025 and secured the position of the second-largest region in the market. In the region, India and China are both reached USD 6.51 billion and USD 5.43 billion, respectively, in 2025. The growth in the Asia Pacific region is driven by an increase in urban populations, a rise in disposable income, and a surge in the consumption of packaged food. Governments in nations such as China and India are enacting bans on plastic, promoting the use of bio-based and recyclable alternatives. Additionally, the competitiveness of costs and the expansion of domestic biopolymer production further bolster regional growth.

Japan Sustainable Films for Packaging Market

The Japanese market in 2025 was valued to be around USD 3.45 billion, accounting for roughly 4.25% of global revenues. Japan's market is propelled by robust waste management systems, elevated recycling rates, and government-supported circular economy initiatives. Packaging manufacturers focus on producing lightweight, high-performance recyclable films.

China Sustainable Films for Packaging Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 6.51 billion, representing roughly 8.00% of global sales.

India Sustainable Films for Packaging Market

The Indian market in 2025 was valued at around USD 5.43 billion, accounting for roughly 6.68% of global markets.

North America

North America held the third-dominant share in 2024, valued at USD 15.09 billion, and maintained its third-leading position in 2025, with a value of USD 16.31 billion. In North America, growth is propelled by extended producer responsibility (EPR) regulations, mandates for recycled content, and sustainability initiatives led by retailers. Prominent FMCG and retail brands are allocating resources toward recyclable mono-material films and packaging based on post-consumer recycled (PCR) materials to achieve their ESG objectives. Additionally, technological innovations and robust research and development capabilities significantly enhance the pace of adoption.

U.S. Sustainable Films for Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market value approximated at around USD 12.76 billion in 2025, accounting for roughly 15.69% of global sales. In the U.S., the implementation of state-level plastic bans, mandates for recycled content, and robust corporate sustainability commitments serve as significant catalysts for growth. Furthermore, advancements in material innovation, the presence of international packaging firms, and investments in chemical recycling technologies facilitate the swift advancement of sustainable film solutions.

Latin America

The Latin America region is expected to witness moderate growth in this market space during the forecast period and reach a valuation of USD 10.31 billion in 2025. In Latin America, the growth of the market is steadily improving as a result of new restrictions on single-use plastics and voluntary commitments to sustainability from corporations. Multinational food and beverage firms are implementing recyclable flexible packaging to meet global standards. Nevertheless, the limitations of infrastructure affect the speed of this adoption.

Middle East & Africa

In the Middle East & Africa, South Africa reached USD 2.28 billion in 2025. The growth of the Middle East & Africa region is bolstered by initiatives aimed at economic diversification, especially within GCC nations, alongside a rising consciousness regarding the management of plastic waste. The demand for packaging is propelled by the modernization of retail and reliance on food imports. Nevertheless, the level of adoption differs significantly owing to variations in regulations and the development of recycling systems throughout the region.

Saudi Arabia Sustainable Films for Packaging Market

The Saudi Arabian market reached approximately USD 2.76 billion by 2025, accounting for roughly 3.39% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The global market demonstrates a semi-consolidated structure, with leading companies such as Amcor, Mondi, and Sealed Air. Their strong presence is largely driven by continuous strategic efforts, including partnerships, acquisitions, and product innovations aimed at strengthening research and expanding market reach.

- For example, in September 2024, Amcor announced the commercial launch of its next-generation recyclable high-barrier polyethylene (PE) film intended for dry food and home care applications. This new mono materials structure substitutes multi-layer laminates while preserving moisture and oxygen barrier performance. Engineered for store drop-off and advanced recycling processes, this innovation aids brand owners in achieving their recycled content and recyclability objectives.

In addition to these key players, companies such as Constantia Flexibles, ProAmpac, and Coveris also play a significant role in the global market. These organizations are expected to focus heavily on new product development, strategic partnerships, and collaborations to strengthen their global market shares in the coming years.

LIST OF KEY SUSTAINABLE FILMS FOR PACKAGING COMPANIES PROFILED

- Amcor (Switzerland)

- Mondi (U.K.)

- Sealed Air (U.S.)

- Constantia Flexibles (Austria)

- ProAmpac (U.S.)

- Coveris (Austria)

- UFlex Limited (India)

- Futamura Group (Japan)

- Cosmo Films (India)

- Winpak Ltd. (Canada)

- Dunmore (U.S.)

- Jindal Films (Luxembourg)

- Innovia Films (U.K.)

- ALMA Packaging AG (Switzerland)

- ePac Holdings, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2024: Mondi has broadened its sustainable flexible packaging range by introducing a recyclable paper-based and mono-PE barrier film solution tailored for food applications. The company has made investments in upgrading its extrusion and converting capacities at its European facilities to address the increasing demand for eco-designed packaging. This new solution provides excellent seal integrity and product protection, while also facilitating recyclability within current streams.

- May 2024: Sealed Air has launched a recyclable flexible film as part of its sustainability-oriented product range, aimed at packaging for protein and fresh food. This innovation substitutes conventional multi-material laminates with recycle-ready mono-material films that are suitable for polyethylene recycling streams. The company highlighted the advantages of a reduced carbon footprint and downgauging, which results in decreased plastic usage per package.

- March 2024: Constantia Flexibles expanded its EcoLam range of recyclable mono-material laminates designed for food and pharmaceutical The company enhanced barrier performance through advanced coating technologies, enabling wider replacement of conventional multi-layer structures.

- January 2024: ProAmpac has introduced a new range of curbside-recyclable flexible films made from polyethylene, specifically designed for snacks and frozen foods. This innovation incorporates high-barrier technology into a mono-material structure, enhancing recyclability while maintaining durability. ProAmpac has indicated that this product addresses the increasing Extended Producer Responsibility (EPR) policies in North America and Europe.

- November 2023: Coveris has introduced an innovative recyclable thermoforming film solution intended for fresh food packaging. This new film minimizes plastic weight while ensuring puncture resistance and clarity. It is engineered to be compatible with mechanical recycling processes, with the objective of assisting retailers in achieving their plastic reduction and recyclability targets.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segmentation included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, along with their prevalence by region. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.63% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, End Use, and Region |

| By Material |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 81.32 billion in 2025 and is projected to reach USD 170.14 billion by 2034.

In 2025, the market value stood at USD 25.71 billion.

The market is expected to grow at a CAGR of 8.63% over the forecast period.

By material, the Polylactic Acid (PLA) segment is expected to lead the market.

Regulatory push against conventional plastics are the key factors driving the market growth.

Amcor, Mondi, Sealed Air, Constantia Flexibles, ProAmpac, and Coveris are the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us