Telecom Managed Services Market Size, Share & Industry Analysis, By Service Type (Managed Data Center Services, Managed Security Services, Managed Network Services, Managed Mobility Services, Managed Infrastructure Services, and Others), By Deployment Type (On-Premise and Cloud-Based), By Organization Size (Large Enterprises and Small & Medium Enterprises (SMEs)), By End User (Telecom Operators, Healthcare, BFSI, and Others) and Regional Forecast, 2026-2034

TELECOM MANAGED SERVICES MARKET SIZE AND FUTURE OUTLOOK

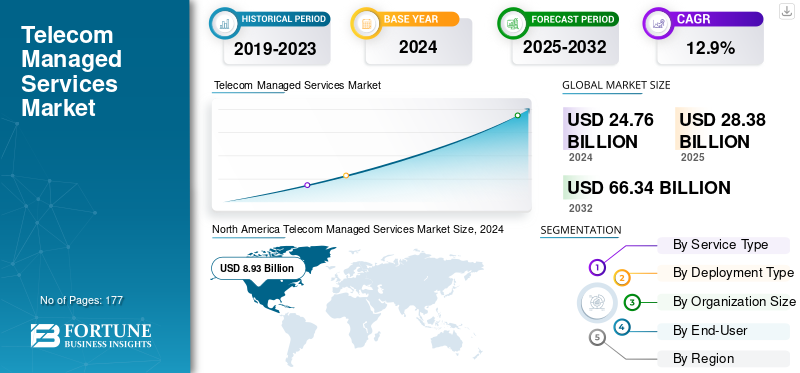

The global telecom managed services market size was valued at USD 28.38 billion in 2025. The market is projected to grow from USD 32.41 billion in 2026 to USD 82.01 billion by 2034, exhibiting a CAGR of 12.30% during the forecast period. North America dominated the global telecom managed services market with a market share of 36.00% in 2025.

Telecom managed services is referred to an outsourced infrastructure, network and operational aid solutions that allow telecom operators as well as enterprises to improve their efficiency, reduce the costs, and focus on core activities.

The market is noticing a prominent growth owing to increase in network complexities, expansion of 5G, cumulating data consumption, surging demand for cost-effective operations as well as the need for enhanced service quality and security. Additionally, cloud adoption and digital transformation also accelerates the overall market growth.

Key players operating in the market include AT&T Inc., Capgemini SE, Cisco Systems, Inc., Cognizant Technology Solutions Corporation, DXC Technology Company, Fujitsu Limited, HCL Technologies Limited, Huawei Technologies Co., Ltd., IBM Corporation (U.S.) and others. These companies are focusing on offering advanced end-to-end managed network, IT and security services to the global telecom providers.

Download Free sample to learn more about this report.

TELECOM MANAGED SERVICES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 28.38 billion

- 2026 Market Size: USD 32.41 billion

- 2034 Forecast Market Size: USD 82.01 billion

- CAGR: 12.30% from 2026–2034

- North America dominated the telecom managed services market with a 36.00% share in 2025.

- The managed data center services segment accounted for the largest market share in 2026.

- The cloud-based segment is projected to hold a 55.48% share in 2026.

North America

North America accounted for USD 10.24 billion in 2025 (36.00% share), supported by advanced telecom infrastructure and digital transformation.

Europe

Europe captured 20.40% of the global market in 2025, reaching USD 5.79 billion, driven by 5G rollout and cloud network adoption.

Asia Pacific

Asia Pacific reached USD 9.45 billion in 2025 and is projected to reach USD 10.86 billion in 2026, driven by 5G deployment and cloud-based managed services.

U.S.

The market is projected to reach USD 9.04 billion by 2026, fueled by digital transformation and cybersecurity investments.

Japan

The market is projected to reach USD 1.63 billion by 2026, supported by increasing 5G deployment and enterprise connectivity.

Read More

MARKET DYNAMICS

Market Drivers

Rising Demand for Efficient Network Management Drives the Market Development

The increase in demand for effective network management is a major factor driving telecom managed services market growth. As the telecom networks become highly complex due to IoT, 5G, cloud integration and increasing data traffic, different service providers find it difficult in managing operations internally. Outsourcing network management to a specialized vendor aids in ensuring a higher performance, faster resolution of issues, and lower downtime. Additionally, it also allows the operators to reduce operational costs, focus on innovation and improve the service quality as well as customer experience.

Market Restraints

Concerns Related to Data Privacy and Security Deters the Market Growth

Various concerns related to data privacy and security is a major restraint to the market. With operators outsourcing critical network functions to a third party providers, the risk of unauthorized access, cyberattacks and data breaches tend to increase. Handling these sensitive customer information across different platforms, global locations and cloud environment complicates the compliance with data protection regulations. Additionally, service providers are required to invest heavily in constant monitoring, robust security frameworks, and regulatory adherence which increases the cost and slower the service adoption.

Market Opportunities

Expansion of 5G Networks and Emerging Digital Ecosystems Offers Lucrative Growth Opportunities

The rise in new digital ecosystem and expansion of 5G networks create a major opportunity for the market. As operators move toward 5G, they demand sophisticated support for network planning, deployment, maintenance and optimization. The complexity of next-generation connectivity such as IoT, edge computing, cloud native architecture and network virtualization also drives the demand for expert managed service providers. These vendors aid telecom companies to accelerate the rollout, ensure higher performance, and reduce the operational challenges.

TELECOM MANAGED SERVICES MARKET TRENDS

Increasing Adoption of Cloud and Virtualized Network Solutions Has Emerged as a Prominent Market Trend

A major trend reshaping the market is increasing adoption of cloud based as well as virtualized network solutions. Telecom operators are increasingly embracing the software-defined networking and network function virtualization to replace the traditional hardware-based systems with a more scalable, flexible, and cost efficient architectures. Additionally, cloud managed platforms also enable quicker service deployment, improved resource utilization and automated network operations. This aids in growing data demand, enhances the service flexibility and allows providers to innovate effectively.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Service Type

Increasing Need for Effective Data Management Boosts Managed Data Center Services Segment Growth

Based on service type, the market is segmented into managed data center services, managed security services, managed network services, managed mobility services, managed infrastructure services and others. The Telecom Operators segment is projecteed to dominate the market with a share of 70.07% in 2026.

In 2026, managed data center services segment held the largest telecom managed services market share with a revenue of USD 7.9 billion. This dominance is driven by increasing need for effective data management, continuous monitoring, and storage optimization. Additionally, telecom companies are also increasingly relying on managed data centers to ensure network scalability, reliability and cost efficiency.

On the other hand, the managed security services segment held the highest CAGR of 13.8% in 2024. This growth is owing to the rising frequency of data breaches and cyber threats. With expansion in telecom networks, providers are focusing on advanced security frameworks to protect sensitive customers and enterprise data, thus fueling the need for outsourced security management.

By Deployment Type

Flexibility, Scalability and Cost-Effectiveness of Cloud-Based Segment Augments Its Growth

The market is divided into on premise and cloud-based, as per deployment type.

Among these, cloud-based segment dominates the market with a revenue share of USD 13.63 billion in 2024. The Cloud-Based segment is expected to lead the market, contributing 55.48% globally in 2026. This segmental growth is attributed to the its flexibility, scalability and cost-effectiveness. Additionally, telecom operators and enterprises are shifting toward a cloud infrastructure to improve the service agility and support rapid technological upgrades in the network operations. Increasing adoption of digital transformation initiatives also boosts the segment growth. Moreover, rising preference for virtualized network functions and cloud-native applications endures to quicken segment expansion.

By Organization Size

Established Infrastructure and High Investment Capacity of Large Enterprises Drives Segment Growth

Based on organization size, the market is segmented into large enterprises and Small & Medium Enterprises (SMEs).

Among these, the large enterprises segment dominated the market with a revenue share of USD 14.48 billion in 2024. This is benefiting from an established infrastructure and high investment capacity. Additionally, these organizations are growingly outsourcing telecom management functions to emphasis on strategic initiatives while maintaining the reliable communication networks. The Large Enterprises segment is projecteed to dominate the market with a share of 58.01% in 2026.

On the other hand, the small & medium enterprises segment also held highest CAGR of 13.5% in 2024. These firms are growingly adopting managed telecom services to reduce the operational complexities and IT costs. Moreover, the availability of cost-effective cloud solutions and remote management service is making these offerings highly accessible to a smaller business.

By End User

Increasing Reliance on Managed Services Drives Telecom Segment Growth

The market is segmented into telecom operators, healthcare, BFSI, and others, based on the end user.

In 2024, telecom operators segment dominated the market with a share of USD 17.33 billion. This growth is due to its extensive reliance on managed services to streamline network operations and improve the customer experience. Additionally, the need for effective management of complex network infrastructures and higher data traffic also supports their ongoing dominance.

Additionally, the BFSI sector held highest CAGR of 13.4% in 2024. This segmental growth is attributed to the growing need for uninterrupted and secure communication systems. Additionally, the increasing digital transaction and mobile banking activities are also prompting BFSI organizations to invest in managed telecom solutions.

To know how our report can help streamline your business, Speak to Analyst

TELECOM MANAGEMENT SERVICES MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America Telecom Managed Services Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 10.24 Billion in 2025, capturing 36.00% of the global market share, and is projected to reach USD 11.69 Billion in 2026. This regional growth is driven by advanced telecom infrastructure, early adoption of next generation technologies and strong presence of service providers across the region. Additionally, focus of the U.S. on digital transformation and cybersecurity also enhances regional market growth. The U.S. market is projected to reach USD 9.04 billion by 2026.

Europe

In 2025, Europe represented USD 5.79 Billion, accounting for 20.40% of the worldwide market, and is projected to grow to USD 6.58 Billion in 2026. This growth is due to stronger adoption of virtualized and cloud networks, rapid 5G deployment, and stringent regulatory frameworks that empower a high-quality and secure telecom operations. The UK market is projected to reach USD 1.00 billion by 2026. The Germany market is projected to reach USD 1.82 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 9.45 Billion in 2025, representing 33.30% of the global market landscape, and is expected to reach USD 10.86 Billion in 2026. This regional growth is attributed to growing network expansion, rising demand for cloud-based managed services and increase in mobile penetration across the region. Additionally, the growing investments in 5G deployment and enterprise connectivity are also propelling market growing across economies such as The Japan market is projected to reach USD 1.63 billion by 2026. The China market is projected to reach USD 5.31 billion by 2026. The India market is projected to reach USD 1.37 billion by 2026.

South America

The South America market is projected to reach USD 1.89 billion by 2025, driven by increasing investments in 5G and 4G infrastructure, expanding mobile penetration, and the growing pace of digital transformation across enterprises.

Middle East & Africa

Middle East & Africa accounted for USD 1.02 Billion in 2025, representing 3.60% of the global market share, and is projected to reach USD 1.14 Billion in 2026. supported by rising investments in telecommunications infrastructure, increasing mobile connectivity, and accelerating enterprise digitalization. The GCC countries market is projected to reach USD 0.52 billion by 2025.

Latin America

In 2025, Latin America held 6.70% of the global market, reaching a valuation of USD 1.89 Billion, and is projected to grow to USD 2.14 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Technological Innovation to Retain their Market Positions

The telecom managed services industry consists of various key players including AT&T Inc., Capgemini SE, Cisco Systems, Inc., Cognizant Technology Solutions Corporation, DXC Technology Company, Fujitsu Limited, HCL Technologies Limited, Huawei Technologies Co., Ltd., IBM Corporation (U.S.), and others. These companies are focusing on technological innovation, improving service quality, scalability and stronger partnerships with the telecom operators.

LIST OF KEY TELECOM MANAGED SERVICES COMPANIES PROFILED:

- AT&T Inc. (U.S.)

- Capgemini SE (France)

- Cisco Systems, Inc. (U.S.)

- Cognizant Technology Solutions Corporation (U.S.)

- DXC Technology Company (U.S.)

- Fujitsu Limited (Japan)

- HCL Technologies Limited (India)

- Huawei Technologies Co., Ltd. (China)

- IBM Corporation (U.S.)

- Tech Mahindra Limited (India)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Verizon Communications Inc. (U.S.)

- ZTE Corporation (China)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, Mobileum Inc. a leading global provider of analytics and network solutions, and NOHOLD, a pioneer in AI-powered automation solutions, announced the formation of a strategic alliance to redefine AI enablement across the telecom industry. This partnership marks a major step forward in building a scalable AI ecosystem that seamlessly blends into multi-vendor telecom operations, empowering operators to unlock the full value of their data.

- In August 2025, Xtelify, a fully-owned subsidiary of Bharti Airtel housing all of Airtel’s digital assets and capabilities, launched a sovereign, telco-grade cloud platform ‘Airtel Cloud’. Tailored to handle 140 crore transactions per minute for Airtel’s own use in India, this sovereign cloud platform is now being extended to meet the ever-evolving needs of businesses in India.

- In June 2025, Ericsson announced the launch of Ericsson On-Demand, a new solution delivering core network services as a true software-as-a-service (SaaS) platform to communications service providers (CSPs).

- In March 2025, Wipro Limited, a leading technology services and consulting company, launched TelcoAI360 to transform operations for telcos by leveraging AI. The AI-first Managed Services platform will empower telcos to roll out differentiated technology solutions at scale and speed, while delivering better customer experience at a fraction of the cost.

- In March 2025, The EY organization announced the launch of EY Telecom.ai agentic solution, a suite of artificial intelligence (AI) agents for telecommunication providers that will operate across the critical functions of finance, network, customer service and content life cycle management. Telecom.ai is an AI-powered solution that leverages the full-stack NVIDIA AI platform.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, service type, deployment type, organization size and end user of the product. Besides this, it offers insights into the telecom managed services market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Global Telecom Managed Services Market Scope |

|

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 12.30% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Service Type, Deployment Type, Organization Size, End User and Region |

|

By Service Type |

· Managed Data Center Services · Managed Security Services · Managed Network Services · Managed Mobility Services · Managed Infrastructure Services · Others |

|

By Deployment Type |

· On-Premise · Cloud-Based |

|

By Organization Size |

· Large Enterprises · Small & Medium Enterprises (SMEs) |

|

By End User |

· Telecom Operators · Healthcare · BFSI · Others |

|

By Region |

· North America (By Service Type, Deployment Type, Organization Size, End User and Region and Country/Sub-region) o U.S. (By End User) o Canada (By End User) o Mexico (By End User) · Europe (By Service Type, Deployment Type, Organization Size, End User and Country/Sub-region) o U.K. (By End User) o Germany (By End User) o France (By End User) o Italy (By End User) o Rest of Europe · Asia Pacific (By Service Type, Deployment Type, Organization Size, End User and Country/Sub-region) o China (By End User) o Japan (By End User) o India (By End User) o South Korea (By End User) o Rest of Asia Pacific · South America (By Service Type, Deployment Type, Organization Size, End User and Country/Sub-region) o Argentina (By End User) o Brazil (By End User) o Rest of South America · Middle East & Africa (By Service Type, Deployment Type, Organization Size, End User and Country/Sub-region) o GCC (By End User) o South Africa (By End User) o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 28.38 billion in 2025 and is projected to reach USD 82.01 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 12.30% during the forecast period.

Rising Demand for Efficient Network Management drives the market growth.

AT&T Inc., Capgemini SE, Cisco Systems, Inc., Cognizant Technology Solutions Corporation, DXC Technology Company, Fujitsu Limited, HCL Technologies Limited, Huawei Technologies Co., Ltd., IBM Corporation (U.S.) and others are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 10.24 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 177

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us