Tethered Drones Market Size, Share and Industry Analysis, By Solution (Tethered Drone and Tethered Stations), By Application (Search and Rescue, Telemetry and communication, Surveillance and Protection, and Commercial and Recreational), By Components (Sensors, Controller Systems, Cameras, and Batteries), By End-User (Commercial and Military), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

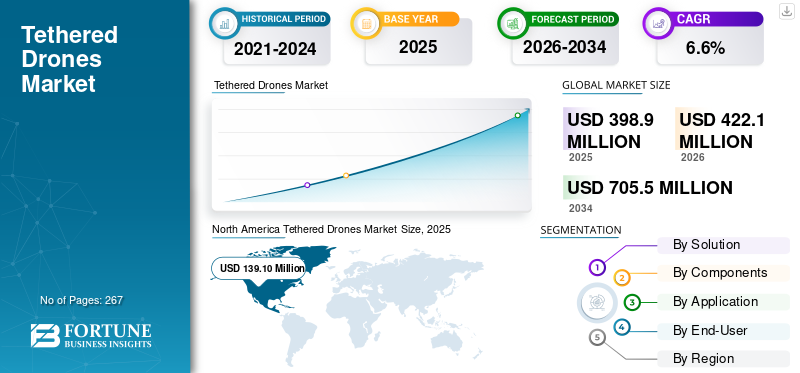

The global tethered drones market size was valued at USD 398.9 million in 2025 and is projected to grow from USD 422.1 million in 2026 to USD 705.5 million by 2034, exhibiting a CAGR of 6.6% during the forecast period. North America dominated the global market with a share of 34.87% in 2025.

The tethered drones market share is experiencing strong global growth, propelled by rising demands across defense, commercial surveillance, emergency management, infrastructure inspection, and telecommunications sectors. Unlike conventional UAVs, tethered drones are connected to a ground station via a robust cable, which supplies continuous power and secure data transmission. This configuration enables prolonged flight durations and reliable, real-time situational awareness, making them invaluable for critical operations such as border monitoring, crowd surveillance, disaster response, and persistent aerial observation. Technological innovations, including sophisticated payload integration, advanced energy management systems, and hybrid mobility designs, have further enhanced the versatility of these drones, driving higher adoption in both established and emerging markets. Tethered drones are preferred for missions requiring constant aerial coverage, uninterrupted surveillance, or rapid data collection, making them indispensable in national security, public safety, industrial inspection, and telecommunications.

The tethered drones market is shaped by a mix of telecom, defense, and specialist UAV players. COMSovereign Holding Corp. provides integrated tethered aerial platforms for communications and surveillance. Dragonfly Pictures Inc. and Hoverfly Technology Inc. focus on ISR and persistent overwatch solutions for military and security users. Elistair SAS, Novadem, and Flyfocus sp. z o.o deliver rugged tethered drone systems for border security, event protection, and industrial monitoring. Menet Aero LLC and Mistral Solutions Pvt. Ltd. expand adoption in defense and civil agencies, while Groupe Gorge and Perspective Robotics AG add robotics, automation, and advanced control technologies to the ecosystem.

Download Free sample to learn more about this report.

RUSSIA-UKRAINE WAR IMPACT

Russia-Ukraine War Accelerated Tethered-Drone Adoption, Supply Bottlenecks, and Doctrine-Level Integration Across Defense CONOPS

The conflict accelerated tethered drone adoption by stress-testing the value of persistent, elevated ISR and communication in contested environments. On the demand side, militaries prioritized rapid-deploy over watch for base defense, artillery spotting, convoy protection, and counter-UAS cuing. The ability to keep sensors aloft for hours, hard-tethered to assured power and data, proved attractive where GNSS is jammed and RF conditions are hostile. This has spilled over into procurement roadmaps beyond the immediate theater, with increased interest in vehicle-mounted, mast-compatible, and UGV-integrated configurations.

On the supply side, the war exposed bottlenecks in high-voltage ground power units, lightweight armored tethers, slip-rings, and EO/IR payload stacks, tightening lead times and nudging prices upward. It also accelerated doctrinal acceptance as tethered assets are now more frequently written into base-defense, border, and logistics-corridor concepts of operations alongside counter-battery radars and EW. Counter-UAS integration advanced as well, with tethered platforms hosting detection payloads and providing elevated nodes for RF sensing and jamming coordination.

Risks remain as export controls and sanctions reshape supply chains, component sourcing, and addressable markets. Electronic warfare keeps evolving, demanding better cable shielding, emissions control, and resilient datalinks. Urban deployments still face permitting and legal scrutiny. Yet the net effect is positive for the category as clearer mission value, stronger funding signals, faster product cycles, and broader interoperability with ground vehicles and command systems. In short, the war compressed years of experimentation into months of operational learning lifting near-term demand and setting a higher baseline for future growth.

MARKET DYNAMICS

MARKET DRIVERS

Reliability and Real-Time Data Transmission are Boosting Market Growth

A key driver for the tethered drones market growth is the requirement for reliable, real-time data transmission for surveillance, security, and industrial applications. The tether systems ensure ongoing aerial observation without battery constraints and provide a stable link for secure communications and high-resolution imagery. Defense agencies are deploying these solutions for continuous border monitoring and tactical command support, benefiting from their long operational endurance and minimal downtime. The commercial sector, including telecom, energy, and public safety, similarly values the ability to achieve uninterrupted aerial coverage for operations such as inspection and emergency management. Their enhanced data security and capacity for persistent monitoring meet critical needs in both government and private industries facing increasingly complex security and operational challenges.

MARKET RESTRAINTS

Mobility and Regulatory Complexity to Hamper Market Growth

Despite their advantages, tethered drones face notable restraints, most prominently their restricted operational radius due to physical tether limitations, which can make them less suitable for long-range missions or where high mobility is required. Handling and deploying the tether cables in dynamic or obstructive environments can increase operational complexity, necessitating skilled operators and robust systems to prevent entanglement or malfunction. Evolving airspace regulations, certification hurdles, and local flight restrictions can further impede large-scale deployment, especially in jurisdictions with strict UAV guidelines. The high upfront investment required for high-end, sophisticated tethered drone systems also limits market penetration among smaller users and organizations operating on constrained budgets.

TETHERED DRONES MARKET TRENDS

Prolonged and Persistent Operations Driving Rapid Expansion

The market trend is defined by a shift toward long-endurance, persistent aerial operations enabled by the continuous power and stable data connectivity that tethered drones offer. Growing defense budgets and heightened geopolitical tensions are prompting military and law enforcement agencies globally to depend on tethered drones for secure perimeter monitoring, border surveillance, and tactical awareness. In commercial sectors, the need for unceasing real-time data collection is driving usage in critical infrastructure inspection, telecommunications, crowd control, and emergency response. Recent innovations, such as automated tethered systems and integrated sensor payloads, have expanded the operational capabilities of these platforms, allowing them to provide high-definition video, thermal imaging, and advanced communication relays over sustained timeframes. The adoption of mobile and hybrid tethered drones is accelerating as public safety agencies and commercial users seek flexible systems that offer immediate deployment and extended mission versatility.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Expansion in Smart Infrastructure and Public Safety to Accentuate Market Growth

The most promising opportunity lies in expanding tethered drone applications in smart infrastructures, urban surveillance, and disaster management programs. Governments and private enterprises are investing in automated aerial monitoring solutions to secure borders, monitor crowds, inspect energy and telecom towers, and assess critical infrastructure. The Asia Pacific region presents remarkable opportunities owing to greenfield projects, rapid urbanization, and government-backed drone deployment for public safety. In addition, the commercial market is opening new avenues for tethered drones in agriculture, event management, and telecommunications offering immediate aerial oversight and resilient communications networks where traditional options are limited. The integration of advanced communication technologies, improved payload management, and automated tethering solutions will greatly expand use cases across these sectors, driving market growth and profitability for manufacturers and solution providers.

MARKET CHALLENGES

Cost, Environmental Factors, and Integration Are Major Challenges in Market

Major challenges include maintaining affordable acquisition and operational costs while delivering advanced features and reliability, especially as technological expectations rise. Tethered drones are sensitive to environmental factors such as extreme weather, wind, and temperature variations which can impact tether integrity and overall system performance. Integrating sophisticated payloads, managing tether deployment across complex terrains, and ensuring seamless connectivity in dynamic mission profiles demand ongoing innovation and engineering advances from manufacturers and operators. The need to balance mobility with endurance, comply with tightening regulations, and educate users on operational best practices continues to challenge broader industry adoption and the scaling of deployment in emerging markets.

SEGMENTATION ANALYSIS

By Solution

Due to Need of Continuous Power, Safer Airspace, and Quick Setup Tethered Stations are in Demand

By solution, the market is segmented into tethered drone and tethered stations.

The tethered stations segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 16.00% share. Ground power units, smart winches, and light tethers keep sensors aloft for hours without battery swaps, reducing sortie churn and operator workload. Hard links improve data assurance under jamming and simplify approvals in urban or sensitive airspace. Vehicle-mounted stations enable “on-the-move” ISR and rapid redeployment between sites.

The tethered drone segment is expected to grow at a CAGR of 7.0% over the forecast period.

By Components

Due to Multispectral Evidence, Day–Night Coverage, and Compliance, Cameras Are in Demand

The components segment is classified into sensors, controller systems, cameras, and batteries.

The cameras segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 10.14% share. EO/IR payloads deliver forensic-grade video, thermal anomaly detection, and target identification in low-light and obscurants. Stabilized gimbals reduce false alarms, while on-board storage and secure downlinks meet chain-of-custody rules. Upgrades (zoom, SWIR, low-SWaP) extend platform life, making camera refresh a recurring spend even with stable airframe fleets.

The sensors segment is expected to grow at a CAGR of 7.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application Type

Surveillance & Protection Are in Demand As it Can Reduce False Positives and Coordinate Ground Teams

The application segment is classified into search and rescue, telemetry and communication, surveillance and protection, and commercial and recreational.

The surveillance and protection segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 14.48% share. Critical sites airports, refineries, data centers, stadiums need continuous elevated viewpoints to close blind spots between fixed sensors. Tethered overwatch reduces false positives, accelerates response, and coordinates ground teams. Integrated analytics (object tracking, intrusion classification) convert video into actionable alerts, cutting OPEX while improving regulatory and insurer compliance.

The telemetry and communication segment is expected to grow at a CAGR of 7.6% over the forecast period.

By End-User

Military Segment is in Demand Due to Assured ISR under EW and Rugged Logistics

By end-user, the market is classified into commercial and military.

The military segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 19.30% share. In contested RF/GNSS environments, hard-tethered power and data safeguard uptime for base defense, convoy escort, and counter-UAS cueing. Vehicle/UGV integration supports rapid movement and concealment. Modular payloads (EO/IR, RF sensing, comms relay) let units tailor effects, while simplified training speeds deployment across dispersed formations.

The commercial segment is expected to grow at a CAGR of 6.9% over the forecast period.

TETHERED DRONES MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Tethered Drones Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 139.1 Million in 2025, capturing 34.90% of global revenue, and is estimated to reach USD 147.13 Million in 2026. The region’s growth is driven by security modernization initiatives, resilient communication systems, and increasing deployment of tethered drones across public safety, border security, and critical infrastructure applications. Growing adoption for disaster response, large-scale event monitoring, and military operations continues to support market expansion. The U.S. market is projected to reach USD 127.14 Million in 2026, driven by increasing use of tethered drones in homeland security, infrastructure surveillance, and communication networks.

Europe

The Europe market reached USD 112.3 Million in 2025, representing 28.20% of total market revenue, and is projected to reach USD 118.6 Million in 2026. Regional demand is supported by civil protection initiatives, border surveillance requirements, and growing investments in long-endurance intelligence, surveillance, and reconnaissance (ISR) capabilities. Wildfire monitoring, flood response, stadium security, and critical infrastructure protection are among the key applications driving adoption. The U.K. and Germany markets are projected to reach USD 22.49 Million and USD 28.35 Million in 2026, respectively.

Asia Pacific

The market in Asia Pacific was valued at USD 117.6 Million in 2025, accounting for 29.50% of the global market, and is projected to reach USD 125.0 Million in 2026. Growth is fueled by increasing investments in security modernization, disaster response capabilities, and border surveillance infrastructure. Rapid urbanization, expanding industrial facilities, and rising demand for continuous monitoring solutions are encouraging broader adoption of tethered drone systems. The China market is projected to reach USD 56.03 Million in 2026, while Japan and India are expected to reach USD 23.63 Million and USD 18.62 Million, respectively.

Rest of the World

The Rest of the World market accounted for USD 29.9 Million in 2025, representing 7.50% of the global industry, and is expected to reach USD 31.3 Million in 2026. Demand is supported by critical infrastructure protection, border security operations, and cost-effective aerial surveillance solutions across the Middle East, Africa, and Latin America. Increasing use of tethered drones for asset protection, event security, disaster assessment, and emergency communication support continues to create growth opportunities in these regions.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Growth Fueled by Innovation, Partnerships, and Urban Integration by Key Players

The tethered drones landscape features a diverse mix of defense-grade incumbents and agile specialists. COMSovereign Holding Corp. leverages telecom know-how to push persistent airborne communications, while Dragonfly Pictures Inc. brings naval and expeditionary endurance to ISR missions. Elistair Sas has become a reference for automated, long-endurance systems, complemented by Hoverfly Technology Inc., which focuses on rapid-deploy power-tether platforms for public safety. Europe adds depth as Groupe Gorge supports mission-critical robotics integration; Novadem supplies compact systems to security forces; and Perspective Robotics AG (Fotokite) scales public-safety deployments with firefighter-centric designs. In Central Europe, Flyfocus sp. Z o.o advances training and turnkey aerial services, and Menet Aero LLC. expands into energy and infrastructure monitoring with tethered capabilities. From India, Mistral Solutions Pvt. Ltd. integrates sensors, control, and local manufacturing for defense and homeland security customers. Together these players are shaping standards, expanding payload ecosystems, and meeting demand for persistent, low-risk aerial overwatch globally.

LIST OF KEY TETHERED DRONES COMPANIES PROFILED

- COMSovereign Holding Corp. (U.S.)

- Dragonfly Pictures Inc. (U.S.)

- Elistair Sas (France)

- Flyfocus sp. Z o.o (Poland)

- Groupe Gorge ( France)

- Hoverfly Technology Inc. (U.S.)

- Menet Aero LLC. (U.S.)

- Mistral Solutions Pvt. Ltd. (India)

- Novadem (France)

- Perspective Robotics AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- July 2025 - Garuda Aerospace has secured multiple deals to roll out AI-driven drone solutions across the mining sector, extending its work with Odisha Mining Corporation (OMC) and broadening its footprint in mining operations.

- July 2025 – COPTRZ, a U.K. provider of commercial drone solutions, has signed on as an authorized distributor of Elistair’s tethered drone platforms in the U.K.

- February 2025 - Elistair, a global leader in tethered UAS for ISR, announced a USD 3.5 million order from an allied military to deliver Khronos small tethered systems, including spares, training, and support won in collaboration with Milrem Robotics.

- January 2024 - Elistair has teamed with Rheinmetall Canada Inc. to offer an on-the-move ISR package that pairs the fully automated KHRONOS tethered drone with Rheinmetall’s Mission Master UGV family.

- August 2023 - The Indian Army has placed orders for 130 tethered drones and 19 tank-driving simulators under Emergency Procurement, with deliveries slated within 12 months.

REPORT COVERAGE

This report delivers a targeted deep dive into the tethered drone ecosystem profiling the leading infrastructure developers and operators, the key components (pads, charging, control systems, passenger processing), and the main use cases across urban air mobility and regional links. It charts current policy milestones, pilot programs, and network build-outs, and pinpoints the shifts shaping the next wave of deployments. Together, these insights explain the recent surge in activity and the forces set to drive the next phase of growth.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.6% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation

|

By Solution · Tethered Drone · Tethered Stations |

|

By Components · Sensors · Controller Systems · Cameras · Batteries |

|

|

By Application · Search and Rescue · Telemetry and communication · Surveillance and Protection · Commercial and Recreational |

|

|

By End-User · Commercial · Military |

|

|

By Region · North America (By Solution, Components, Application, and End-user) o U.S. (By End-User) o Canada (By End-User) · Europe (By Solution, Components, Application, and End-user) o U.K. (By End-User) o Germany (By End-User) o France (By End-User) o Russia (By End-User) o Rest of Europe (By End-User) · Asia Pacific (By Solution, Components, Application, and End-user) o China (By End-User) o Japan (By End-User) o India (By End-User) o Rest of Asia Pacific (By End-User) · Rest of the World (By Solution, Components, Application, and End-user) o Middle East and Africa (By End-User) o Latin America (By End-User) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 399.0 million in 2025 and is estimated to reach USD 705.6 million by 2034.

The market is growing at a CAGR of 6.60% during the projection period (2026-2034).

The tethered stations segment is estimated to be the leading segment in this market during the forecast period.

The military segment is estimated to be the leading segment in this market during the forecast period.

COMSovereign Holding Corp., Dragonfly Pictures Inc., Elistair Sas, Flyfocus sp. Z o.o, Groupe Gorge, Hoverfly Technology Inc. are some of the leading OEMs in the market.

North America is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 267

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us