Thoracic Catheters Market Size, Share & Industry Analysis, By Product Type (Chest Drainage Catheters, Pleural Drainage Catheters, Thoracic Suction Catheters, Thoracostomy Catheters, and Others), By Material (Silicone, Polyurethane, PVC, and Others), By Application (Pleural Effusion, Pneumothorax, Hemothorax, Empyema, Post-operative Thoracic Drainage, and Others), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Thoracic Catheters Market Size and Future Outlook

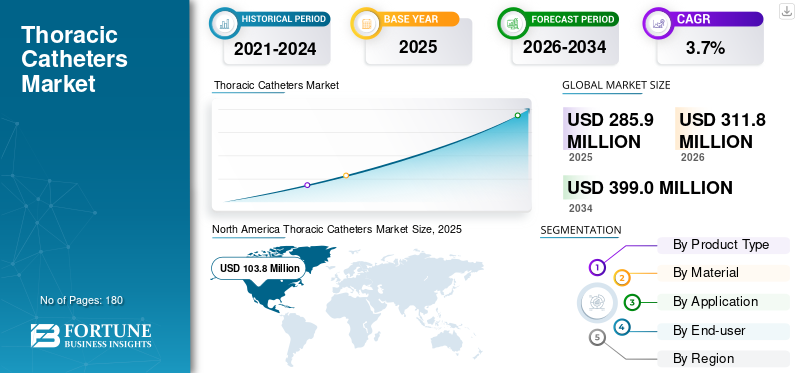

The global thoracic catheters market size was valued at USD 285.9 million in 2025. The market is projected to grow from USD 311.8 million in 2026 to USD 399.0 million by 2034, exhibiting a CAGR of 3.7% during the forecast period. North America dominated the thoracic catheters market with a market share of 36.31% in 2025.

Thoracic catheters are sterile, flexible tubes used to drain air, blood, or fluid from the pleural space and support lung re-expansion, typically after trauma, infection, malignancy-related effusions, or cardiothoracic surgery. They include conventional chest drainage catheters, pleural drainage catheters such as indwelling pleural catheters, and smaller-bore thoracostomy/pigtail options used in select cases. The market is growing as hospitals manage a steady stream of thoracic surgeries and emergency admissions. At the same time, clinicians increasingly favor reliable drainage solutions that are easier to place and compatible with modern post-operative pathways. The market growth is also supported by aging populations, higher cancer prevalence, and ongoing efforts to reduce complications and shorten the length of stay.

Furthermore, Teleflex Incorporated, Getinge AB, BD, and Cardinal Health held the largest market share in 2025, driven by increased investments and strategic initiatives, including new product launches and partnerships.

Download Free sample to learn more about this report.

Thoracic Catheters Market Key Takeaways

- 2025 Market Size: USD 285.9 million

- 2026 Market Size: USD 311.8 million

- 2034 Forecast Market Size: USD 399.0 million

- CAGR: 3.7% from 2026–2034

- North America dominated the market with a 36.31% share in 2025.

- Silicone segment is projected to hold a 70.1% share in 2026.

- Hospitals & ASCs segment is projected to hold an 89.8% share in 2026.

North America

The market reached USD 103.8 million in 2025, driven by high cardiothoracic surgery volumes and standardized post-operative care.

Asia Pacific

The market is projected to reach USD 63.8 million by 2026, supported by expanding surgical capacity and emergency care infrastructure.

Europe

The market is projected to reach USD 102.2 million by 2026, driven by stable surgical volumes and standardized drainage protocols.

U.S.

The market is projected to reach USD 99.0 million by 2026.

Japan

The market is projected to reach USD 8.5 million by 2026.

Read More

THORACIC CATHETERS MARKET TRENDS

Shift toward Smaller-Bore Options and Outpatient-Friendly Pleural Management

Across regions, clinicians are paying closer attention to the patient experience side of thoracic drainage, including discomfort, mobility limitations, and downstream impacts on recovery. This is encouraging the greater use of small-bore catheters and pigtail-style thoracostomy options for appropriate indications, particularly where imaging guidance and standardized placement are available.

Another notable trend is the continued shift in pleural effusion care toward approaches that support outpatient management when clinically feasible, which raises interest in pleural drainage catheters designed for longer-term use and home or clinic follow-up. At the same time, hospitals are refining post-operative protocols to reduce complications such as retained hemothorax or prolonged air leaks, which can influence catheter selection and stocking decisions. Operationally, supply reliability is becoming a bigger part of the purchasing conversation. Health systems increasingly value vendors with stable availability and consistent product quality across facilities. Taken together, the trend is toward more tailored catheter choices by indication and care setting, with an emphasis on comfort, consistency, and streamlined workflows.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Procedure Volume and Standardized Post-operative Care to Fuel the Market Growth

A significant factor driving thoracic catheters market growth is the predictable need for pleural and chest drainage across a wide set of clinical pathways. Cardiothoracic surgeries commonly require chest drainage as part of routine post-operative care and emergency care continues to see pneumothorax and hemothorax cases that need rapid intervention. As hospitals push for standardized recovery protocols, thoracic drainage becomes more protocol-driven, less dependent on individual preference, and more embedded in care bundles.

In parallel, pleural effusion management continues to generate the recurring demand for long-term drainage options, potentially shifting volumes toward specialized pleural drainage catheters. There is also a quality-of-care driver that prevents retained fluid, persistent air leaks, and associated infections, thereby reducing complications and readmissions. This makes clinicians and administrators more willing to use well-designed catheters that offer consistent performance, kink resistance, and patient comfort, especially in high-acuity settings. Overall, the driver is not a single factor. It is a reliable cadence of procedures, coupled with hospital priorities around safety, efficiency, and outcomes.

MARKET RESTRAINTS

Cost Pressure and Purchasing Consolidation Tighten Pricing to Limit Market Growth

Thoracic catheters sit in a category where hospitals expect strong reliability but also demand aggressive pricing, especially for high-volume chest drainage products. As group purchasing and centralized procurement expand, suppliers face tighter contract terms, more frequent rebids, and increasing requirements to justify premium features with measurable clinical value. In many facilities, purchasing decisions are made at the system level, which can reduce product diversity at the hospital level and slow the uptake of specialized variants unless they clearly reduce complications or length of stay. Budget constraints are often more pronounced in emerging markets, where access may be present but the preference leans toward cost-effective PVC or standard configurations.

Another restraint is variation in clinical practice, some sites lean toward small-bore solutions for select indications. In contrast, others make use of traditional chest tubes, making it harder for a single premium product approach to win broadly. Finally, training and workflow changes can be a barrier, even a better catheter may not be adopted quickly if it requires new placement routines or new stocking practices across the ED, ICU, and OR.

MARKET OPPORTUNITIES

Better Patient Pathways and Targeted Solutions Can Create Significant Growth Opportunities

A clear opportunity lies in aligning catheter selection with specific care pathways rather than treating all thoracic drainage as the same commodity. For example, pleural effusion management can benefit from products designed for longer dwell times, patient comfort, and outpatient follow-up. In this area, specialized pleural drainage catheters are growing faster than standard chest tubes.

Another opportunity is optimizing post-operative recovery. Hospitals are increasingly focused on early mobilization and faster discharge, which creates demand for drainage solutions that are easier to manage, less prone to clogging, and more comfortable for patients. Suppliers that support clinicians with practical education, proper sizing, placement technique, and troubleshooting can reduce complications and strengthen loyalty. Emerging markets offer additional upside as hospital capacity expands and more thoracic and cardiac procedures shift to higher-volume centers. Lastly, product line breadth can be a differentiator. Providers often prefer vendors who can reliably supply multiple catheter types and sizes, helping procurement reduce complexity while maintaining clinical flexibility.

MARKET CHALLENGES

Clinical Variability and Complications Associated with Products to Challenge Market Growth

Thoracic drainage can have several performance issues such as kinking, blockage, malposition, or inadequate drainage leading to complications, repeat procedures, or longer hospital stays. A major challenge is that outcomes depend on both device design and technique. Even a good catheter can underperform if size selection or placement practice varies widely across departments.

Hospitals also face practical constraints, such as stocking multiple sizes and types across ED, ICU, and OR, which can be difficult, and standardizing a limited formulary can create friction with clinician preferences. In some regions, access to imaging guidance or consistent training is uneven, which can affect the adoption of small-bore approaches for certain indications. The pricing pressure remains a constant challenge for suppliers. To win tenders for these products, they must be cost-effective, yet the market still expects reliability and patient-centered design.

Finally, quality requirements and documentation expectations continue to rise, placing greater pressure on manufacturers to ensure consistent materials, sterility, and traceability. Managing these challenges is essential as the market rewards reliability failures that are remembered.

Segmentation Analysis

By Product Type

Wide Adoption in Several Applications to Drive Chest Drainage Catheters Segment Growth

Based on product type, the market is segmented into chest drainage catheters, pleural drainage catheters, thoracic suction catheters, thoracostomy catheters, and others.

To know how our report can help streamline your business, Speak to Analyst

The chest drainage catheters segment holds the highest share as they are the default option across a broad range of high-volume scenarios, especially post-operative thoracic drainage and acute trauma/ED cases. After cardiothoracic surgery, drainage is part of standard recovery protocols, which creates a predictable baseline demand in hospitals. In emergencies such as pneumothorax and hemothorax, clinicians often choose a familiar, readily available chest tube to restore lung function quickly and manage ongoing drainage.

Additionally, the pleural drainage catheters segment is projected to grow at a CAGR of 6.7% during the forecast period.

By Material

Silicone Dominates as Comfort, Flexibility, and Biocompatibility Support Longer Dwell Time

By material, the market is classified into silicone, polyurethane, PVC, and others.

The silicone segment holds the largest thoracic catheters market share as it performs well in clinical situations where patient comfort, flexibility, and biocompatibility matter. Compared with more rigid materials, silicone can reduce irritation and is commonly preferred for longer dwell times, offering an advantage in pleural effusion management and for patients requiring extended drainage. It also tends to maintain flexibility across temperature changes and handling, which helps reduce kinking risk during placement and patient movement. Moreover, the segment is projected to hold a share of 70.1% in 2026.

Additionally, the polurethane segment is estimated to grow at a CAGR of 3.5% during the forecast period.

By Application

Post-operative Thoracic Drainage Leads as Surgery Protocols Require Routine, Repeatable Drainage

By application, the market is classified into pleural effusion, pneumothorax, hemothorax, empyema, post-operative thoracic drainage, and others.

The post-operative thoracic drainage segment holds the largest share as it is built into standard surgical practice. After many cardiothoracic procedures, drainage is not optional. It is part of routine management to remove air and fluid, monitor post-operative bleeding, and support lung re-expansion. The segment is projected to hold a share of 29.7% in 2026.

Additionally, the pleural effusion segment is estimated to grow at a CAGR of 6.2% during the forecast period.

By End-user

Hospitals and ASCs Dominate with High Thoracic Drainage in Surgery and High-Acuity Care

On the basis of end-user, the market is classified into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment accounts for the largest share as most thoracic catheter placements happen in settings equipped for surgery and high-acuity care. Chest drainage after cardiothoracic operations is typically managed in operating rooms and ICUs, while pneumothorax and hemothorax are often present in emergency departments and trauma pathways in hospitals. The segment is set to hold a share of 89.8% in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 8.7% during the forecast period.

Thoracic Catheters Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Thoracic Catheters Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share of USD 99.8 million in 2024 and also dominated in 2025, reaching a value of USD 103.8 million. North America’s growth is anchored in the region’s consistently high volume of cardiothoracic surgeries, trauma care, and ICU admissions, where chest drainage is a routine part of post-operative and emergency management. Hospitals continue to standardize recovery pathways after thoracic and cardiac procedures, which keeps the demand steady for reliable, easy-to-manage catheters across operating rooms and critical care units. At the same time, the region continues to see a sustained need for pleural drainage in recurrent pleural effusions, including oncology-linked cases, which supports the ongoing uptake of pleural drainage options alongside standard chest tubes.

U.S. Thoracic Catheters Market

In 2026, the U.S. market is forecasted to represent USD 99.0 million, capturing 33.1% of total global revenue.

Europe

Europe is expected to depict a CAGR of 2.8% over the forecast period, the second-highest globally, and is anticipated to reach a valuation of USD 102.2 million by 2026. The Europe market grows mainly due to stable surgical volumes and the region’s emphasis on hospital efficiency and complication reduction, where appropriate drainage management helps prevent prolonged stays and readmissions. Many European systems are reinforcing standardized post-operative protocols, which drives the recurring demand for chest drainage catheters as baseline consumables. In parallel, pleural effusion management remains a steady contributor, particularly in aging populations and in settings treating chronic respiratory disease and cancer-related complications.

U.K. Thoracic Catheters Market

The U.K. market is projected to reach USD 15.2 million by 2026, accounting for 5.1% of the global market revenue.

Germany Thoracic Catheters Market

The Germany market is estimated to reach about USD 18.3 million by 2026, representing roughly 6.1% of the global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 63.8 million, ranking as the third-largest globally. Asia Pacific is typically the fastest-growing region as it combines rising procedure access with expanding hospital capacity. As more patients gain access to advanced surgical care, especially in large urban centers, volumes of thoracic and cardiac procedures increase along with the routine need for post-operative drainage. Growth is also supported by improving emergency care systems and greater adoption of procedural best practices, which increases the number of cases treated with appropriate thoracic catheterization rather than conservative management.

Japan Thoracic Catheters Market

The Japan market is projected to generate approximately USD 8.5 million in revenue by 2026, contributing nearly 2.8% to the global market.

China Thoracic Catheters Market

The China market is estimated to reach approximately USD 22.7 million by 2026, contributing about 7.6% to global revenues.

India Thoracic Catheters Market

The India market is projected to hold a value of approximately USD 7.9 million by 2026, corresponding to about 2.6% of the global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa markets are anticipated to witness moderate growth, with Latin America expected to reach around USD 15.2 million by 2026. The Latin America market growth is driven by the gradual expansion of surgical capacity, the modernization of tertiary hospitals, and improved access to thoracic and cardiac interventions in major metropolitan areas. As health systems invest in ICU beds, trauma response, and surgical infrastructure, thoracic catheter usage rises as chest drainage is integral to managing post-operative and emergency cases. The Middle East and Africa market growth is supported by expanding hospital infrastructure and specialty care capacity, particularly in GCC countries and leading private/tertiary centers. As these systems scale up trauma services, critical care, and cardiothoracic programs, catheters are increasingly used as drainage is a standard requirement in many high-acuity pathways.

GCC Thoracic Catheters Market

By 2026, the GCC market is expected to generate approximately USD 3.8 million in the market, accounting for nearly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The thoracic catheters market is moderately consolidated at the top and highly fragmented in the long tail. A handful of global medtech companies dominate premium hospital accounts through broad portfolios, established chest drainage brands, and contracted supply relationships with large health systems. For example, Teleflex positions a dedicated chest drainage and thoracic catheter portfolio under its surgical/cardiovascular offering. In contrast, BD’s PleurX franchise anchors recurring pleural drainage use in chronic and oncology-linked effusions, both of which help reinforce share through clinical familiarity and repeat purchasing. Key players such as Teleflex Incorporated, Getinge AB, BD, and Cardinal Health held the largest market share.

Moreover, other key players, such as Cook Medical, B. Braun, Medela, and Vygon, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY THORACIC CATHETERS COMPANIES PROFILED

- Teleflex Incorporated (U.S.)

- Getinge AB (Sweden)

- BD (U.S.)

- Cardinal Health (U.S.)

- Cook Medical (U.S.)

- Braun (Germany)

- Medela (Switzerland)

- Vygon (France)

- Poly Medicure Ltd. (India)

- Redax S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Teleflex Incorporated, a leading global provider of medical technologies, completed the previously announced acquisition of substantially all of the Vascular Intervention business of BIOTRONIK SE & Co. KG.

- August 2024: Getinge announced that it had agreed to acquire Paragonix Technologies, Inc., a leading U.S. company in organ transport products and services.

- November 2023: Centese, Inc., announced the successful closing of its USD 15 million Series B funding round, led by Medical Technology Venture Partners with participation from existing and new investors. The round would advance clinical initiatives, fund commercialization efforts, and bolster the advanced product development of the Thoraguard Intelligent Chest Tube Management System.

- October 2023: Getinge completed the previously announced acquisition of 100% of the shares in High Purity New England, Inc., a leading U.S.-based company in the fast-growing areas of custom single-use solutions for bioprocessing applications.

- September 2023: Merit Medical Systems, Inc., a leading global manufacturer and marketer of healthcare technology, announced the U.S. commercial release of its Aspira Bottle. The new evacuated drainage bottle is the latest addition to Merit’s drainage portfolio.

- January 2022: ICU Medical Inc. completed its takeover of Smiths Medical from Smiths Group plc. The Smiths Medical business includes ambulatory infusion devices, syringe, vascular access, and vital care products.

- June 2021: BD, a leading global medical tech company, received 510(k) clearance from the U.S. FDA (Food and Drug Administration) for the PeritX Peritoneal Catheter System for the drainage of recurrent, symptomatic non-malignant ascites.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.7% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product Type,Material, Application, End-user, and Region |

| By Product Type |

|

| By Material |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 285.9 million in 2025 and is projected to reach USD 399.0 million by 2034.

In 2025, the market value stood at USD 103.8 million.

The market is expected to exhibit a CAGR of 3.7% during the forecast period of 2026-2034.

The chest drainage catheters segment leads the market by product type.

The key factors driving the market are the rising volume of procedures and standardized post-operative care.

Teleflex Incorporated, Getinge AB, BD, and Cardinal Health are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us