Torque Vectoring Market Size, Share & Industry Analysis, By Technology Type (Brake-Based Torque Vectoring, Mechanical/Active Differential Torque Vectoring, and Electric Torque Vectoring), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Drivetrain Configuration (All-Wheel Drive (AWD/4WD), Front-Wheel Drive (FWD), and Rear-Wheel Drive (RWD)), By Component Type (Active Differentials, Electronic Control Units (ECUs), Clutches & Actuators, Sensors, and Software & Control Algorithms), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

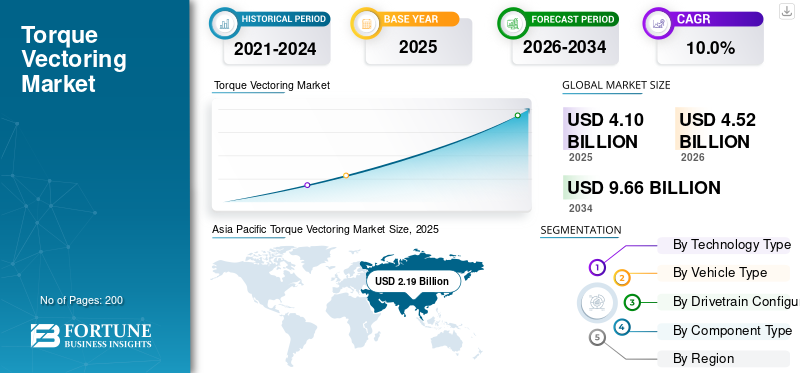

The global torque vectoring market size was valued at USD 4.10 billion in 2025. The market is projected to grow from USD 4.52 billion in 2026 to USD 9.66 billion by 2034, exhibiting a CAGR of 10.0% during the forecast period. Asia Pacific dominated the global market with a market share of 53.41% in 2025.

Automotive torque vectoring is a vehicle control technology that actively distributes drive torque between individual wheels or axles to enhance cornering performance, traction, stability, and safety under varying driving and road conditions. Key drivers of the global torque vectoring market include the rising demand for vehicle safety and performance, the growth of AWD and electric vehicles, stricter stability regulations, advancements in electronic control systems, and the increasing adoption in premium and performance-oriented vehicles.

Major players, including Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech, focus on advanced diagnostics, automation, and digital integration, supporting the development, calibration, and service efficiency of the active torque vectoring system, aligned with evolving safety and performance requirements.

Download Free sample to learn more about this report.

TORQUE VECTORING MARKET TRENDS

Stability Improvement and Supporting Drive Modes Boost New Market Trends

Electric torque vectoring is rapidly shifting from a halo performance feature into a scalable capability embedded in e-axles and multi-motor EV architectures. As OEMs pursue both fuel efficiency and driving feel, software-controlled wheel torque management is emerging as a differentiator in electric SUVs and premium EVs, enabling stability improvements without brake intervention and supporting selectable drive modes. This trend also increases the share of software and controls in the overall system value, as vehicle dynamics become increasingly software-defined and updatable across model years.

- In May 2024, BorgWarner announced it was supplying Polestar BEV SUVs with an electric Torque Vectoring and Disconnect system.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Integrated Vehicle Motion Control Accelerates Adoption of Advanced Torque Management

The broader integration of braking, steering, sensing, and motion software is driving the adoption of torque vectoring across more vehicle lines, as OEMs can deliver predictable handling, improved stability, and a consistent driver experience across trim levels with unified control logic. Rather than tuning subsystems in isolation, automakers and suppliers are combining actuators under centralized motion management, which makes it easier to deploy torque vectoring as part of a complete chassis-control package. This integration is especially valuable as vehicles gain higher power outputs and heavier batteries that increase the need for refined stability control.

- In January 2024, Bosch announced that its new Vehicle Motion organization was launched at the beginning of the year, unifying braking, steering, vehicle motion software, and sensors.

MARKET RESTRAINTS

Cost and Integration Burden Limits Penetration Beyond Premium and AWD-Heavy Segments

Despite clear performance benefits, torque vectoring faces restraints from system cost, calibration workload, and platform integration complexity, particularly for mechanical/active differentials and high-content electric solutions. OEMs must justify the added bill of materials and validation time in relation to the customer's willingness to pay. At the same time, suppliers face margin pressure that can slow aggressive feature rollouts into mid-segment vehicles. Brake-based approaches reduce hardware cost but can introduce brake wear and thermal constraints in demanding use. In parallel, electrification investments compete for the same budget, forcing tighter ROI scrutiny. These factors impede the torque vectoring market growth.

MARKET OPPORTUNITIES

Software-Defined Vehicles Create Upside via OTA Enhancements and Feature Monetization

Torque vectoring has a strong opportunity to expand through software-defined vehicle platforms that support rapid iteration, over-the-air (OTA) calibration refinements, and new driving-function packages delivered after sale. As OEMs separate software from hardware and standardize compute architectures, they can deploy torque vectoring control strategies more widely across platforms, improve performance in the field, and potentially monetize advanced dynamics modes. This also supports fleet learning and faster debugging, thereby reducing the need for long-cycle revalidation for incremental improvements. The result is a larger addressable market for software/control algorithms, as well as centralized motion controllers, beyond traditional performance nameplates.

- In June 2024, Stellantis said it delivered more than 94 million OTA updates in 2023 and outlined next-generation platforms expected for technology integration by the end of 2024.

MARKET CHALLENGE

Safety Validation and Fault Management Become Harder as Torque Control Becomes More Powerful

As torque vectoring shifts toward high-torque EV drivetrains and deeper software control, the challenge intensifies around functional safety, fault detection, and safe-state behavior under sensor errors, software defects, or actuator faults. Minor control anomalies can translate into driveline stress, unexpected propulsion loss, or unstable behavior, thereby raising validation demands across various scenarios, including those involving low-friction surfaces and mixed-traction events. OEMs and suppliers must demonstrate robustness across OTA updates, manage cybersecurity risks, and ensure that diagnostics can detect issues early. This increases test burden, compliance documentation, and recall risk if defects escape to production.

Segmentation Analysis

By Technology Type

Brake-Based Stability Control Integration Sustains High-Volume Adoption Across Mainstream Platforms

Based on technology type, the market is segmented into brake-based torque vectoring, mechanical/active differential torque vectoring, and electric torque vectoring (e-axle/multi-motor).

Brake-based torque vectoring dominate the torque vectoring market share because they leverage existing ESC/ABS hardware, keeping BOM and integration effort low while still improving turn-in and understeer control, ideal for mass-market platforms and high production volumes. As OEMs prioritize cost-effective safety and acceptable handling gains, brake-based calibration upgrades continue to expand across trims, even when hardware changes are limited.

The Electric Torque Vectoring (E-Axle/Multi-Motor) segment is projected to grow at a CAGR of 13.9% over the forecast period.

- In April 2025, Audi unveiled brake torque vectoring on the new A6 Avant as a wheel-selective braking function to improve cornering agility and counter understeer.

By Vehicle Type

Sedan and Hatchback Platforms Maintain Dominance Through Scale and Platform Standardization

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

Hatchback & sedan applications remain dominant because they represent large global nameplate volumes and benefit from standardized ESC-based control stacks that can include torque-vectoring logic with minimal incremental hardware requirements. Automakers also use consistent chassis-control signatures across sedan families to reduce calibration cost per unit, which supports broad deployment. While SUVs are growing, the installed base in compact and midsize sedans keeps demand steady for cost-optimized solutions.

The HCV segment is projected to grow at a CAGR of 12.1% over the forecast period.

By Drivetrain Configuration

FWD Segment Leads Owing to Faster Rollouts and Consistent Vehicle Feel

Based on drivetrain configuration, the market is segmented into AWD/4WD, FWD, and RWD.

Front wheel drive (FWD) remains the dominant installation base because it underpins most high-volume passenger car platforms globally, and it pairs well with cost-efficient, brake-assisted yaw control for everyday stability benefits compared to rear wheel drive RWD. OEMs can deploy software tuning changes across large fleets without redesigning rear driveline hardware, thereby supporting faster rollouts and a consistent vehicle feel. Meanwhile, electrification and performance positioning accelerate AWD growth through dual-motor layouts that facilitate easier implementation of torque distribution.

The All-Wheel Drive (AWD / 4WD) segment is projected to grow at a CAGR of 12.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component Type

High-Volume Sensing Content Underpins Adoption as Control Becomes More Data-Driven

Based on component type, the market is segmented into active differentials, ECUs, clutches & actuators, sensors, and software & control algorithms.

Sensors dominate because torque vectoring performance relies on continuous, accurate vehicle-state inputs (such as yaw rate, acceleration, wheel speed, and steering angle), and these sensing layers are scalable across nearly every vehicle architecture, including ICE, hybrid, and EV. As chassis control becomes more predictive and integrated with ADAS, sensor performance and robustness remain essential, sustaining high unit volumes even when actuation varies by segment.

The software & control algorithms segment is projected to grow at a CAGR of 12.4% over the forecast period.

- In November 2024, Bosch showcased high-performance MEMS sensors for occupant safety and driving dynamics at electronica 2024, underscoring its ongoing sensor innovation that supports vehicle control functions.

TORQUE VECTORING MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Torque Vectoring Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America’s torque vectoring services market is growing steadily due to the high penetration of SUVs, AWD vehicles, and increasing EV adoption. Advanced driver assistance systems, a premium vehicle mix, and a strong aftermarket diagnostics ecosystem support demand for calibration, software updates, and maintenance services. The region benefits from early adoption of software-defined vehicle architectures, enabling OTA-based torque vectoring optimization. Fleet electrification, particularly in delivery and utility vehicles, further drives service requirements related to system validation, diagnostics, and lifecycle support across both OEM and aftermarket channels.

U.S. Torque Vectoring Market

The U.S. dominates North America due to widespread SUV and pickup adoption, intense AWD penetration, and rapid growth of dual-motor EVs. OTA updates, ADAS integration, and high consumer demand for performance, safety, and personalized driving modes drive the adoption of torque vectoring services.

Europe

Europe represents a high-value market for torque vectoring services, driven by premium OEMs, stringent safety standards, and a strong emphasis on vehicle dynamics. High penetration of active differentials and advanced chassis systems increases demand for calibration, diagnostics, and software refinement services. Electrification policies and growing EV sales further accelerate electric torque vectoring service needs. Europe’s focus on driving precision, homologation compliance, and functional safety validation supports sustained demand for specialized engineering and aftermarket services.

U.K. Torque Vectoring Market

The UK market is supported by premium vehicle ownership, growing EV penetration, and strong motorsport and performance engineering expertise. Torque vectoring services focus on software calibration, diagnostics, and upgrades for premium sedans and electric SUVs, supported by a mature aftermarket and fleet electrification initiatives.

Germany Torque Vectoring Market

Germany leads Europe due to its concentration of premium OEMs and drivetrain technologies advance. High adoption of active differentials and electric AWD platforms drives strong demand for torque vectoring calibration, validation, and software services across development, production, and post-sale vehicle lifecycle stages.

Asia Pacific

Asia Pacific is the fastest-growing region, driven by massive vehicle production volumes, rapid EV adoption, and increasing SUV penetration. Electric torque vectoring services are expanding rapidly as multi-motor EVs and e-axles become more prevalent. OEMs focus on cost-efficient, software-driven vehicle dynamics, which boosts demand for diagnostics, OTA updates, and system optimization services. Growing local supplier ecosystems and government electrification initiatives further strengthen long-term service regional market growth across both developed and emerging economies.

China Torque Vectoring Market

China dominates the Asia Pacific due to large-scale EV production, high adoption of dual-motor electric SUVs, and software-centric vehicle platforms. OTA updates drive torque vectoring services, rapid model refresh cycles, and strong demand for system optimization across mass-market and premium EV brands.

Japan Torque Vectoring Market

Japan’s market is shaped by advanced vehicle control engineering, hybrid and EV adoption, and emphasis on reliability. Torque vectoring services focus on calibration precision, diagnostics, and integration with safety systems, particularly in compact cars and premium domestic models with sophisticated chassis control systems.

India Torque Vectoring Market

India shows strong growth potential driven by rising SUV sales and gradual EV adoption. Torque vectoring services remain limited but expanding, focused on diagnostics and software updates for higher-end SUVs and electric vehicles as safety regulations and feature penetration increase.

Rest of the World

The Rest of the World grows from a smaller base, driven by increasing SUV imports, gradual EV penetration, and the modernization of vehicle fleets. Torque vectoring services primarily expand through imported vehicles that are already equipped with advanced control systems. Growth is supported by improvements in service infrastructure, rising safety awareness, and electrification initiatives in Latin America, the Middle East, and certain parts of Africa.

COMPETITIVE LANDSCAPE

Key Industry Players

Electrification, Software Control, and Integrated Vehicle Dynamics Define Torque Vectoring Services Competition

The global torque vectoring market is shaped by the rising electrification of vehicles, software-defined vehicle architectures, and the increasing integration of vehicle motion control systems. Leading players, including Bosch, ZF, Continental, BorgWarner, GKN Automotive, Schaeffler, Hyundai Mobis, and Hitachi Astemo, compete through advanced calibration services, electric torque vectoring software, and lifecycle support for AWD and multi-motor platforms. Companies strengthen competitiveness by expanding vehicle dynamics software teams, offering OTA-enabled torque management updates, and supporting OEMs with validation, functional safety, and homologation services. Strategic collaborations with automakers and EV platform developers enable early integration of torque vectoring logic into centralized vehicle motion controllers. Suppliers also focus on modular service toolkits and data-driven diagnostics to reduce development time and costs. As electric SUVs and performance EVs scale globally, competition increasingly centers on software expertise, system integration capability, and the ability to deliver reliable, updatable torque vectoring performance across diverse vehicle architectures.

LIST OF KEY TORQUE VECTORING COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- BorgWarner Inc. (U.S.)

- Aisin Corporation (Japan)

- Schaeffler AG (Germany)

- GKN Automotive (Dowlais Group) (UK)

- Dana Incorporated (U.S.)

- Magna International Inc. (Canada)

- Valeo SA (France)

- Hyundai Mobis (South Korea)

- JTEKT Corporation (Japan)

- American Axle & Manufacturing (AAM) (U.S.)

- Schaeffler Vehicle Lifetime Solutions (Germany)

- Hitachi Astemo Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Audi announced model year updates across key series and highlighted dynamic plus driving behavior enabled by brake torque vectoring and (for specific variants) the quattro sport differential. Audi positioned these changes as both software- and hardware-led improvements that raise lateral dynamics while retaining everyday drivability.

- In October 2025, Alpine developed a torque vectoring system for its A390 all-electric fastback, which can distribute torque between 0% and 100% across the two rear wheels. The system, developed over a five-year period, utilizes the A390’s three-motor architecture to control each rear wheel independently. One motor powers the front axle while two rear motors each drive a single wheel, enabling precise torque management that responds in milliseconds to steering angle and vehicle speed.

- In October 2025, Porsche launched the first all-electric Macan GTS and confirmed Porsche Torque Vectoring Plus (PTV Plus) as standard equipment. Porsche linked the system with fast-reacting AWD control to enhance agility, traction, and stability, reinforcing the role of torque vectoring as a mainstream performance feature in sporty EV SUVs.

- In June 2025, Bugatti published an engineering-focused update on the Tourbillon’s hybrid powertrain, explicitly noting clutch actuation type and an eight-speed dual-clutch transmission paired with a torque-vectoring differential. Bugatti framed the system as enabling both emotional high-rev performance and modern precision control, with rapid torque delivery used to enhance responsiveness.

- In June 2024, Volkswagen premiered the new Golf R, emphasizing track-focused handling via R-Performance Torque Vectoring, which actively distributes drive across the rear axle to enhance turn-in, reduce understeer, and improve exit traction. VW positioned the system as a core differentiator for repeatable performance driving rather than only occasional stability intervention.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology Type, By Vehicle Type, By Drivetrain Configuration, By Component Type, and By Region. |

|

By Technology Type |

· Brake-Based Torque Vectoring · Mechanical / Active Differential Torque Vectoring · Electric Torque Vectoring (E-Axle / Multi-Motor) |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Drivetrain Configuration |

· All-Wheel Drive (AWD / 4WD) · Front-Wheel Drive (FWD) · Rear-Wheel Drive (RWD) |

|

By Component Type |

· Active Differentials · Electronic Control Units (ECUs) · Clutches & Actuators · Sensors · Software & Control Algorithms |

|

By Region |

· North America (By Technology Type, By Vehicle Type, By Drivetrain Configuration, By Component Type, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Technology Type, By Vehicle Type, By Drivetrain Configuration, By Component Type, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Technology Type, By Vehicle Type, By Drivetrain Configuration, By Component Type, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Technology Type, By Vehicle Type, By Drivetrain Configuration, and By Component Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.10 Billion in 2025 and is projected to reach USD 9.66 Billion by 2034.

In 2025, the market value stood at USD 2.19 billion.

The Torque Vectoring market demand is expected to grow at a CAGR of 10.0% during the forecast period from 2026 to 2034.

The Front-Wheel Drive (FWD) segment led the Torque Vectoring Market share in the Drivetrain Configuration segment.

Integrated vehicle motion control accelerates the adoption of advanced torque management.

Key market players in the market include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, BorgWarner Inc., and Aisin Corporation.

Asia Pacific accounted for the largest share in the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us