Transmission Fluids Market Size, Share & Industry Analysis, By Type (Automatic Transmission Fluid (ATF), Manual Transmission Fluid (MTF), and Others), By Base Oil (Mineral Oil, Semi-Synthetic Oil, and Synthetic Oil), By End user (On-Road Vehicles and Off-Road Vehicles), and Regional Forecast, 2026-2034

TRANSMISSION FLUIDS MARKET SIZE AND FUTURE OUTLOOK

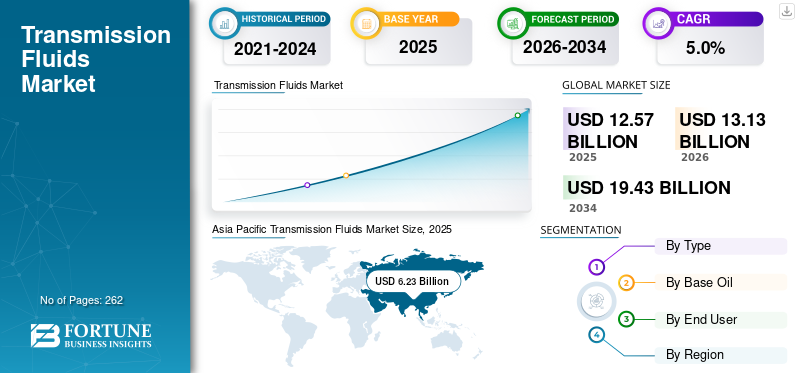

The global transmission fluids market size was valued at USD 12.57 billion in 2025. The market is projected to grow from USD 13.13 billion in 2026 to USD 19.43 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the transmission fluids market with a market share of 49.56% in 2025.

Transmission fluids are specialty lubricants used in automatic, manual, continuously variable, and dual-clutch transmissions, and increasingly in hybrid and selected electric driveline systems. In commercial terms, the market covers automatic transmission fluid (ATF), manual transmission fluid (MTF), and other transmission-related fluids, such as CVT, DCT, and hybrid/e-transmission fluids, sold into OEM factory-fill and aftermarket service-fill applications. The market is supported by the large global vehicle base and the technical necessity of these fluids in heat transfer, friction control, wear protection, hydraulic performance, and shift quality. Key players operating in the market include Shell plc, BP p.l.c., Exxon Mobil Corporation, and Chevron Corporation.

Download Free sample to learn more about this report.

TRANSMISSION FLUIDS MARKET TRENDS

Shift toward Low-Viscosity, OEM-Specific, and Electrified Driveline Fluids Emerges as a Key Market Trend

A major trend in the market is the shift away from broad, legacy transmission oils toward lower-viscosity, application-specific, and OEM-aligned fluid systems. Modern automatic transmission fluids are increasingly designed to support fuel economy, smooth shifting, sludge resistance, oxidation stability, and long fluid life across a broader operating window. Afton states that these automatic fluids are among the most sophisticated lubricant categories, while its current transmission fluid platforms are positioned to meet both OEM performance needs and a wide range of in-use vehicle requirements. This indicates that the market is increasingly driven by approval compatibility, fluid durability, and hardware fit rather than by standard lubrication performance alone.

A second important trend is the emergence of hybrid and electric driveline fluids as a distinct premium layer within the broader market. Shell highlights that hybrid and electric vehicles are creating new engineering demands for fluids, particularly in areas such as electrical compatibility, thermal management, and system protection. This does not eliminate conventional transmission fluid demand, but it shows that future market development will be shaped more by differentiated fluid categories and evolving driveline requirements than by traditional ATF and MTF demand alone.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Automatic, CVT, and Dual-Clutch Transmission Adoption to Drive Market Growth

One of the strongest drivers of transmission fluids market growth is the increasing penetration of automatic and other advanced transmission systems across the global vehicle fleet. Within the automated category, stepped automatics remain the largest segment, with CVTs and DCTs also representing considerable shares. As these systems require specialized fluids for friction control, hydraulic performance, heat management, and component protection, their rising adoption directly supports the demand for higher-performance transmission fluids.

The product demand is further reinforced as these fluids perform core operating functions rather than peripheral additive roles. They are essential to shift response, clutch durability, deposit control, anti-wear performance, and thermal stability in increasingly complex transmission systems. ATFs must perform across many different transmission and vehicle platforms, underscoring the centrality of fluid quality to drivetrain performance. Together with strong global vehicle production and a large installed vehicle parc, this creates a solid structural base for both OEM-fill and aftermarket transmission fluid demand.

MARKET RESTRAINTS

Surging Battery Electric Vehicle Adoption and Simpler Reduction Drive Systems May Restrain Market Growth

A major restraint for the market is the rise of battery-electric vehicles, which can reduce the need for conventional fluids of transmission in part of the future vehicle fleet. Traditional internal combustion vehicles generally rely on multi-speed automatic transmissions, manuals, CVTs, or dual-clutch systems that require dedicated transmission fluids for hydraulic function, shifting performance, and component protection. In contrast, many battery electric vehicles use simpler reduction drive systems with lower transmission complexity. Shell’s e-fluids positioning reflects that electrified mobility is changing fluid requirements significantly rather than carrying forward the same conventional transmission fluid architecture into all future vehicle platforms.

This restraint does not remove lubricant demand altogether, but it places structural pressure on conventional ATF and MTF volume growth over time. As more OEMs introduce dedicated EV platforms, part of future driveline demand shifts away from traditional transmission systems toward lubrication needs and consumption profiles that differ. In practical terms, this means that the market may continue to grow in value through premiumization and new fluid categories, while legacy transmission fluid segments may face comparatively slower volume expansion.

MARKET OPPORTUNITIES

Hybrid Drivetrains, Dedicated E-Fluids, and Premium Service-Fill Products to Create Growth Opportunities

One of the significant opportunities in the market lies in hybrid drivetrains and the development of dedicated e-fluids. Hybrid vehicles continue to use complex transmission-related systems and require fluids capable of balancing wear protection, durability, cooling performance, and compatibility with advanced materials and components. Shell states that hybrid and electric vehicles are bringing some of the biggest engineering and design changes in the mobility industry, creating the demand for new fluid technologies tailored to these systems. This opens attractive growth space for suppliers with strong formulation capabilities, additive expertise, and OEM development relationships.

Another major opportunity lies in premium service-fill products designed for installer and workshop markets. Afton’s multi-vehicle ATF technology shows that lubricant suppliers are increasingly focused on products that combine broad vehicle coverage with OEM certification and advanced performance. This supports the demand for higher-value synthetic and approval-backed transmission fluids that help simplify workshop inventories while maintaining technical credibility. As transmission diversity increases and end users place greater importance on shift quality, durability, and OEM-compliant servicing, premium service-fill fluids are expected to capture a larger share of market value.

MARKET CHALLENGES

OEM Approval Complexity, Transmission Diversity, and Misapplication Risk to Create Market Challenges

A major challenge in the transmission fluids market is the increasing diversity of transmission systems and the growing specificity of OEM fluid requirements. The market includes stepped automatic transmissions, manuals, CVTs, DCTs, hybrid driveline systems, and selected electrified architectures, each with distinct frictional, thermal, and material-compatibility requirements. Infineum’s transmission fluid framework itself separates multiple fluid families, showing that the market cannot be treated as a single, universal lubrication space. This increases formulation complexity, validation requirements, and technical barriers for suppliers.

The challenge is magnified in the aftermarket, where improper fluid selection can affect shift quality, clutch behavior, thermal performance, and OEM compliance. Afton’s transmission fluid positioning places strong emphasis on OEM certification and suitability across defined vehicle populations, underscoring the critical importance of application accuracy. This favors technically stronger suppliers and established brands, but it also raises the commercial burden around installer education, channel support, and precise product mapping, especially as the market becomes more specification-driven.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Research and development in the market is increasingly focused on friction durability, low-viscosity efficiency, oxidation resistance, and compatibility with more advanced driveline hardware. Afton’s driveline additive positioning shows that transmission fluid development is increasingly aimed at helping formulators deliver improved fuel economy, stable shift performance, sludge resistance, and longer fluid life in modern transmission systems. This suggests that product development is moving toward more tightly engineered, performance-specific formulations rather than broad, commodity-style transmission oils.

R&D is also becoming more closely tied to hybrid and electric driveline requirements. Shell’s e-fluids platform highlights the importance of electrical compatibility, thermal management, protection, and system efficiency in electrified mobility. This indicates that future transmission fluid innovation will increasingly depend on how well formulations can serve both conventional transmission needs and the emerging demand from electrified driveline systems. As transmission and driveline architectures continue to evolve, R&D is likely to remain focused on balancing conventional lubrication performance with new operating demands created by integrated and electrically sensitive systems.

SEGMENTATION ANALYSIS

By Type

Automatic Transmission Fluid (ATF) Segment Leads the Market due to Broad Use across Passenger Cars and SUVs

Based on type, the market is segmented into Automatic Transmission Fluid (ATF), Manual Transmission Fluid (MTF), and others.

Among these, Automatic Transmission Fluid (ATF) segment is expected to hold the dominant share of the global market. This dominance is primarily supported by the growing penetration of automatic transmissions across passenger cars and SUVs and a rising share of light commercial vehicles. Automatic transmissions remain the most widely adopted transmission format in major automotive markets such as North America, China, Japan, and several urbanizing economies where driving comfort, smoother gear shifting, and reduced driver fatigue are valued more strongly than manual operation. In addition, modern multi-speed automatic systems require highly engineered fluids for lubrication, hydraulic response, cooling, and friction control, which further reinforces the segment’s leadership in both volume and value terms.

The Manual Transmission Fluid (MTF) segment holds a significant share as manual vehicles still have a visible presence in price-sensitive markets and in selected fleet, utility, and commercial applications. Manual transmissions are generally associated with lower acquisition cost, easier mechanical familiarity, and continued use in regions where automatic penetration is still developing. However, the segment is gradually losing relative share as automatics, CVTs, and dual-clutch systems expand in global vehicle production. The segment is anticipated to expand at a CAGR of 4.5% during the forecast period.

The others segment includes CVT, DCT, and hybrid/e-transmission fluids. Although smaller in share, this segment remains commercially important as it reflects the market’s shift toward more specialized and higher-performance driveline fluid categories.

By Base Oil

Synthetic Oil Segment Leads the Market due to Rising Performance Requirements of Modern Transmissions

Based on base oil, the market is segmented into mineral oil, semi-synthetic oil, and synthetic oil.

Among these, the synthetic oil segment is expected to hold the leading share of the global market. This dominance is supported by the increasing performance requirements of modern transmissions, which operate under tighter thermal, frictional, and durability conditions than older driveline systems. Synthetic transmission fluids offer better oxidation stability, low-temperature flow properties, shear resistance, and extended service life, making them more suitable for automatic, CVT, DCT, and hybrid transmission applications. Their growing acceptance is also supported by OEMs' preference for higher-specification fluids that improve fuel economy, support smoother shifting, and help meet longer drain-interval expectations.

The semi-synthetic oil segment shows positive growth as it offers a practical balance between cost and performance. These products are widely used in markets and vehicle categories where end users want improved durability and better fluid performance than mineral oils can offer, but at a lower cost than fully synthetic products. Semi-synthetic fluids, therefore, remain attractive in a wide range of aftermarket and service-fill applications. The segment is poised to depict a CAGR of 4.6% during the forecast period.

The mineral oil segment is set to depict notable growth. It continues to serve older vehicle fleets, lower-cost servicing environments, and selected manual transmission applications. However, its relative position is under pressure from the industry-wide shift toward premium and OEM-approved fluid technologies.

By End User

On-Road Vehicles Segment Leads the Market due to Large Global Vehicle Parc

Based on end user, the market is segmented into on-road vehicles and off-road vehicles.

Among these, the on-road vehicles segment is expected to hold the dominant transmission fluids market share. This share is supported by a very large global parc of passenger cars, light commercial vehicles, and heavy commercial vehicles, all of which require transmission fluids during factory fill and throughout their operating life in service-fill applications. The recurring need for maintenance, fluid replacement, and transmission servicing across urban mobility, freight transport, ride-sharing, and personal vehicle ownership further strengthens demand. Since on-road vehicles represent the largest share of global automotive production and the largest installed vehicle base, they continue to form the core demand base for transmission fluids worldwide.

The off-road vehicles segment is expected to register a CAGR of 3.8% during the forecast period. This segment includes construction machinery, agricultural equipment, mining vehicles, and other heavy-duty off-highway systems that operate under demanding load and temperature conditions. These vehicles often require durable transmission and driveline fluids with strong anti-wear and thermal performance characteristics. Although the segment does not match the scale of on-road demand, it remains important in industrial and infrastructure-driven markets where equipment uptime, load-bearing capacity, and severe operating environments support consistent fluid consumption.

TRANSMISSION FLUIDS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Transmission Fluids Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region benefits from its very large vehicle production base, a vast installed vehicle parc, and a strong concentration of automotive manufacturing activity across China, Japan, India, South Korea, and Southeast Asia. Asia Pacific remains the most important region as it combines high OEM factory-fill demand with an expanding service-fill opportunity as the regional vehicle base continues to age and diversify. The region is especially important for automatic transmission fluid, CVT fluid, and other advanced driveline fluids, given the scale of passenger vehicle manufacturing and the broad presence of both mass-market and high-volume automotive production platforms.

China Transmission Fluids Market

The China market is one of the largest markets globally, with 2025 revenue at USD 3.17 billion, representing roughly 25.2% of the global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to register strong and steady demand during the forecast period. The region benefits from very high automatic transmission penetration, a large installed vehicle fleet, and a mature aftermarket service ecosystem. North America is one of the most important markets as automatic transmission systems dominate passenger and light truck platforms, creating strong structural demand for automatic fluids and premium synthetic service-fill products. The region also benefits from higher average fluid value realization, driven by the strong acceptance of synthetic and OEM-aligned formulations across professional workshops and retail aftermarket channels.

U.S. Transmission Fluids Market

In 2025, the U.S. market was valued at USD 2.53 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 20.2% of the global market sales.

Europe

The Europe market is expected to maintain a significant position in the market due to its large vehicle stock, well-established automotive industry, and growing emphasis on high-performance, OEM-compliant fluid systems. The region remains commercially important as it combines mature passenger vehicle ownership with strong demand for technically advanced lubricants, particularly in premium automotive markets. Europe is also significant as it has a broad mix of manual, automatic, DCT, and hybrid driveline platforms, which supports continued demand across several fluid categories rather than a single dominant product type.

Germany Transmission Fluids Market

The Germany market was valued at around USD 0.48 billion in 2025, representing roughly 3.9% of the global market revenues.

U.K. Transmission Fluids Market

The U.K. market was valued at around USD 0.29 billion in 2025, representing roughly 2.3% of the global market revenues.

Latin America

Latin America is a smaller but commercially relevant market. The region benefits from a sizable in-use vehicle fleet, continued dependence on internal combustion vehicles, and growing aftermarket service requirements across passenger and commercial vehicle categories. The market growth is expected to remain moderate, supported more by replacement demand and the maintenance of aging vehicles than by very high penetration of advanced transmission technologies.

Brazil Transmission Fluids Market

The Brazil market was valued at around USD 0.43 billion in 2025, representing roughly 3.4% of the global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively small, but has commercial potential due to its reliance on vehicle maintenance, premium imported lubricants, and fleet service demand across several core markets. The regional growth is likely to depend on vehicle ownership expansion, the durability requirements of passenger and commercial fleets, and the continued need for transmission servicing under demanding climatic and operating conditions.

GCC Transmission Fluids Market

The GCC market was valued at around USD 0.26 billion in 2025, representing roughly 2.1% of the global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Pivotal Companies Compete based on Distribution Networks and OEM Approvals to outpace their Rivals

Key players in the market compete based on OEM approvals, advanced formulations, multi-vehicle compatibility, synthetic low-viscosity technologies, and strong distribution networks. The market includes large integrated oil and lubricant majors such as Shell, bp/Castrol, ExxonMobil, Chevron, TotalEnergies, and Phillips 66, alongside lubricant-focused specialists such as FUCHS, Valvoline Global Operations, Idemitsu Kosan, ENEOS, Petro-Canada Lubricants, and LIQUI MOLY. Company product pages and corporate materials show a clear split between broad integrated energy players that compete on the basis of global supply, base oils, and large lubricant portfolios and specialist lubricant companies that compete through application fit, OEM alignment, and premium aftermarket positioning.

LIST OF KEY TRANSMISSION FLUIDS COMPANIES PROFILED

- Shell plc (U.K.)

- BP p.l.c. (U.K.)

- Exxon Mobil Corporation (U.S.)

- Chevron Corporation (U.S.)

- Valvoline Global Operations (U.S.)

- TotalEnergies SE (France)

- FUCHS SE (Germany)

- Phillips 66 Company (U.S.)

- Idemitsu Kosan Co., Ltd. (Japan)

- ENEOS Group (Japan)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Shell Lubricants Shell EV-Plus Thermal Fluid with PurePlus Technology helped enable an immersively cooled BEV powertrain architecture. Testing showed that the fluid could act as an all-in-one thermal management solution for the full BEV powertrain. This is important for the transmission fluids landscape as it shows how leading suppliers are extending beyond conventional ATF and MTF into electrified driveline and thermal-fluid platforms.

- August 2025: Castrol expanded its Castrol ON EV Transmission Fluids lineup with new products for wet e-motors, building on the earlier D1 and D2 transmission-fluid range for EV aftersales. The launch highlights how major lubricant brands are developing dedicated transmission-fluid products for electrified drivetrains rather than relying only on conventional driveline fluids.

- March 2025: ENEOS announced plans to accelerate AI-driven discovery and optimization of new lubricants and immersion cooling fluids with NVIDIA ALCHEMI and PFCC Matlantis. While broader than transmission fluids alone, the development signals faster innovation in formulation across advanced lubricant and future driveline-fluid categories.

REPORT COVERAGE

The transmission fluids market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and applications. In addition, it offers insights into the market and current industry trends and highlights key developments. In addition to the factors mentioned above, the report also covers several factors contributing to the growth of the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Million Liter) |

| Growth Rate | CAGR of 5.0% from 2026 to 2034 |

| Segmentation | By Type, Base Oil, End user, and Region |

| By Type |

|

| By Base Oil |

|

| By End user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 12.57 billion in 2025 and is projected to reach USD 19.43 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 5.0% during the forecast period of 2026-2034.

The on-road vehicles segment is expected to lead the market during the forecast period.

Asia Pacific holds the highest market share.

Rising automatic, CVT, and dual-clutch transmission adoption is a key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 262

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us