Truck Bedliners Market Size, Share & Industry Analysis, By Product Type (Spray-On/Applied Bedliners, Drop-In/Molded Bedliners, and Bed Mats & Bed Rugs), By Material Type (Polyurea/Polyurethane, Plastics & Polymers, and Rubber & Composite Materials), By Truck Type (Light-Duty Pickup Trucks and Medium-Duty Pickup Trucks), By Application (OEM and Aftermarket), and Regional Forecast, 2026-2034

Truck Bedliners Market Size and Future Outlook

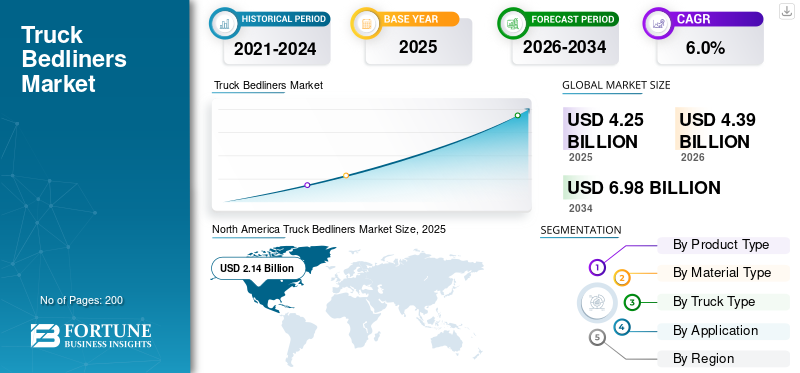

The global truck bedliners market size was valued at USD 4.25 billion in 2025. The market is projected to grow from USD 4.39 billion in 2026 to USD 6.98 billion by 2034, with a CAGR of 6.0% over the forecast period. North America dominated the truck bedliners market with a market share of 50.35% in 2025.

Truck bedliners are protective coatings or fitted inserts applied to pickup truck beds to prevent abrasion, dents, corrosion, moisture damage, and UV degradation. Offered as spray-on/applied, drop-in/molded liners, or bed mats/rugs, they improve durability, cargo grip, and resale value. Key drivers include rising pickup truck parc and commercial fleet usage, higher cargo-bed wear in construction, agriculture, and logistics, and increasing preference for durable protection that lowers repair costs and preserves resale value. OEMs also bundle liners as factory or dealer options. Growth in premium accessories and upgrades is accelerating the adoption of spray-on liners.

Major players include LINE-X, Rhino Linings, PPG, BASF, Axalta, Dow, and Sika, as well as molded and mat brands such as Husky Liners and BedRug. Trends include OEM-dealer packaging, growth of installer networks, premium spray-on systems (polyurea), faster-curing formulations, and wider product customization and warranty-backed offerings.

Download Free sample to learn more about this report.

TRUCK BEDLINERS MARKET TRENDS

Shift Toward Spray-On and Custom Coatings Boosts Market Evolution

The global market trends are evolving beyond simple drop-in liners as users increasingly value durability, seamless protection, and customization. Spray-on and polyurea/polyurethane coatings are gaining traction for their superior abrasion resistance compared to traditional liners, with manufacturers offering tailored textures, colors, and fitment options that appeal to both fleets and individual truck owners. These premium applications not only protect cargo beds but also enhance vehicle aesthetics and long-term value, supporting larger price positioning and aftermarket service margins. The trend reflects broader automotive customization, where accessories serve both functional and lifestyle purposes.

- In November 2024, LINE-X expanded its polyurea coating options with enhanced custom textures and colors, signaling rising consumer interest in performance and personalization.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Pickup Truck Sales and Fleet Expansion Fuel Bedliner Demand

Growing global sales of pickup trucks, coupled with expansion in commercial fleets such as construction, logistics, and utilities are directly driving demand market for truck bedliners. Increased ownership of light- and medium-duty pickups translates to higher initial installations and aftermarket upgrades, as buyers seek protection against abrasion, corrosion, and daily wear from heavy cargo. Fleet owners, especially, prioritize extended asset life, making bedliners a cost-effective solution to reduce maintenance costs and preserve resale value. As truck adoption spreads beyond traditional markets into emerging regions, this driver gains momentum.

MARKET RESTRAINTS

High Installation Costs and Price-Sensitive Alternatives Limit Uptake

One significant restraint in the market is the high cost of professional installation for premium spray-on liners, as well as competition from low-cost alternatives. Premium coatings require specialized equipment and trained technicians, raising the total cost compared with simpler drop-in liners or DIY solutions. In cost-sensitive regions or among price-conscious buyers, this can suppress demand for pickup trucks or shift purchases toward lower-price options with limited durability. Furthermore, where inexpensive plastic liners are widely available, the value proposition for higher-end products can be diluted, slowing broader market expansion. Although maintenance costs may be lower over time for premium options, upfront expense remains a barrier, particularly in emerging markets.

MARKET OPPORTUNITIES

Growth in Commercial Fleet Upfitting and OEM Partnerships to Augment Market Growth

A compelling opportunity in the truck bedliners market growth lies in commercial fleet upfitting and deeper OEM integration. As businesses expand logistics, delivery, and service fleets, bulk purchases of protective accessories including bedliners present scale opportunities for suppliers and service networks. OEMs also increasingly offer bedliners as factory options or bundled accessories, smoothing fitment issues and enhancing vehicle appeal at the point of sale. These dynamics open avenues for long-term contractual sales and stronger OEM supplier partnerships. Additionally, as modular electrician fleets and utility vehicles grow, demand for durable, warranty-backed bedliners rises, strengthening recurring revenue streams.

MARKET CHALLENGES

Material Performance Trade-Offs and Market Fragmentation to Restrict Market Growth

A persistent challenge for the market is balancing material performance with cost and application complexity. While polyurea and polyurethane coatings offer high durability, some formulations can perform poorly under extreme temperature swings or heavy impacts, leading to cracking, peeling, or UV degradation in certain climates. Achieving consistent performance across diverse environmental conditions requires continued material innovation. Additionally, the market is fragmented with numerous regional players and overlapping offerings, intensifying competition and compressing pricing power for manufacturers with a smaller scale. This fragmentation complicates brand differentiation and can confuse buyers about long-term performance expectations.

Segmentation Analysis

By Product Type

Preferred Choice for Commercial Fleets and High-Usage Pickup Owners Lead to Dominance of Spray-on/Applied Bedliners Segment

Based on product type, the market is segmented into spray-on/applied bedliners, drop-in/molded bedliners, and bed mats & bed rugs.

Spray-on/applied bedliners dominate the truck bedliners market share due to their seamless coverage, superior abrasion resistance, corrosion protection, and long service life. These characteristics make them the preferred choice for commercial fleets and high-usage pickup owners seeking reduced maintenance and higher resale value. Increasing pickup premiumization and OEM-dealer packaging further strengthen this segment’s position, especially in North America and the Asia Pacific. The spray-on/applied bedliners segment is projected to grow at a CAGR of 6.9% over the forecast period, reinforcing its dual status as the dominating and fastest-growing product type.

The bed mats & bed rugs segment’s growth is driven by rising demand for cost-effective, removable, and easy-to-install cargo protection solutions. Increasing light-duty pickup usage and aftermarket customization trends drive the segment’s steady 5.2% CAGR over the forecast period.

By Truck Type

Extensive Installed Base and Widespread Use Anchors Light-Duty Pickup Trucks Segmental Dominance

Based on truck type, the market is segmented into light-duty pickup trucks and medium-duty pickup trucks.

Light-duty pickup trucks dominate the market due to their extensive installed base and widespread use for personal, lifestyle, and light commercial purposes. High global production volumes and strong aftermarket customization demand consistently drive bedliner installations in this segment.

In contrast, heavier payload usage is reshaping demand patterns. The medium-duty pickup trucks segment is projected to grow at a CAGR of 7.0% over the forecast period, driven by rising fleet utilization across construction, logistics, agriculture, and infrastructure development.

By Material Type

Cost-Efficient Plastics Sustain Dominance Amid Performance-Driven Material Shifts

Based on material type, the market is segmented into polyurea/polyurethane, plastics & polymers, and rubber & composite materials.

The polyurea/polyurethane segment is dominant and fastest growing projected to grow at a CAGR of 6.9% over the forecast period, driven by increasing adoption of spray-on systems in commercial and heavy-duty applications.

Plastics & polymers is the second dominant global demand due to their cost efficiency, lightweight nature, and widespread use in drop-in liners supplied across mass-market pickups. These bedliner materials support high-volume OEM and aftermarket sales, particularly in cost-sensitive regions. However, durability and performance requirements are gradually shifting value toward advanced coatings. The segment is projected to grow at a CAGR of 4.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Factory-Installed Bedliner Integration Strengthens OEM Leadership

Based on application, the market is segregated into OEM and aftermarket.

OEM installations dominate the market as automakers increasingly integrate bedliners into factory or dealer-installed accessory packages. This approach improves quality consistency, warranty alignment, and customer convenience while boosting per-vehicle revenue. OEM dominance is extreme in mature pickup markets with high optional content penetration. Meanwhile, customization and retrofit demand continue to expand beyond factory channels.

The aftermarket segment is projected to grow at a CAGR of 7.0% over the forecast period, driven by fleet retrofits, pickup personalization trends, and expanding installer networks globally.

TRUCK BEDLINERS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

NORTH AMERICA

North America Truck Bedliners Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounts for the largest share of the global market, supported by a deeply entrenched pickup truck culture and high bedliner penetration across both OEM and aftermarket channels. Strong commercial fleet activity in construction, utilities, and logistics drives sustained replacement and upgrade demand. OEM bundling of spray-on liners and dealer-installed accessories continues to lift per-vehicle revenue. While the market is mature, steady growth is driven by premiumization, increased use of medium-duty pickups, and rising adoption of high-durability polyurea coatings across professional and fleet applications.

U.S. TRUCK BEDLINERS MARKET

The U.S. is set to account for USD 1.85 billion in 2026. The U.S. dominates regional demand due to the world’s largest pickup truck parc and high consumer willingness to invest in protective and premium accessories. Spray-on bedliners lead value share, driven by heavy-duty usage and resale value considerations. OEM-installed liners are gaining traction, while aftermarket demand remains strong, driven by customization culture and fleet retrofitting across construction, agriculture, and service industries.

EUROPE

Europe exhibits moderate yet consistent growth, driven primarily by commercial vehicle use rather than lifestyle pickups. Demand is concentrated in utility pickups, light commercial vehicles, and specialized fleet applications. Drop-in liners and plastic-based solutions remain prevalent due to cost efficiency, though spray-on coatings are gaining acceptance in premium and heavy-duty use cases. OEM accessory packaging, stricter durability expectations, and rising focus on vehicle lifecycle cost reduction across professional and municipal fleets further support growth.

U.K. TRUCK BEDLINERS MARKET

The U.K. market is set to account for USD 0.06 billion in 2026, is driven by construction, utilities, and agricultural pickup usage, where durability and corrosion resistance are key. Aftermarket installations dominate, supported by installer networks and retrofit demand. Spray-on liners are gradually expanding as fleets seek longer service life, while OEM uptake increases through dealer accessory programs tied to commercial pickup sales.

GERMANY TRUCK BEDLINERS MARKET

Germany’s market is supported by strong fleet discipline and emphasis on vehicle protection and residual value with share of 18.4% in 2025. Medium-duty pickup and commercial usage drive demand for higher-performance liners, particularly spray-on solutions. OEM integration and premium aftermarket installations are gaining momentum, aligned with Germany’s focus on engineered durability and total cost of ownership optimization.

ASIA PACIFIC

Asia Pacific is the fastest-growing region in the global markets, driven by the rising adoption of pickup trucks across logistics, infrastructure, agriculture, and rural transport. Expanding commercial fleets, improving road connectivity, and increasing awareness of cargo-bed protection are accelerating demand. Spray-on liners and polyurea materials are gaining share as durability requirements rise, while aftermarket installations dominate due to retrofit-heavy markets. Strong production bases and growing vehicle parc across multiple countries support sustained long-term growth.

CHINA TRUCK BEDLINERS MARKET

China is set to account for USD 0.47 billion in 2026. China leads Asia Pacific demand due to its large commercial vehicle parc and expanding pickup usage in logistics and rural mobility. In medium-duty applications, fleet operators increasingly adopt spray on bedliners to reduce maintenance costs. Aftermarket installations dominate, while OEM adoption is gradually increasing through standardized commercial vehicle packages.

JAPAN TRUCK BEDLINERS MARKET

Japan is set to account for USD 0.17 billion in 2026. Japan’s market is characterized by controlled growth, driven by utility pickups and light commercial vehicles rather than lifestyle usage. Demand emphasizes quality, fitment precision, and long-term durability. Spray-on liners are selectively adopted in professional applications, while drop-in solutions remain relevant due to structured fleet replacement cycles.

INDIA TRUCK BEDLINERS MARKET

India is emerging as one of the fastest-growing with CAGR of 10.1% over the forecast period, national markets, supported by the rapid expansion of small commercial pickups for last-mile delivery, agriculture, and infrastructure projects. Low penetration creates substantial headroom for growth, particularly in aftermarket installations. Demand is gradually shifting from basic mats toward durable spray-on and molded liners as awareness increases.

REST OF THE WORLD

The rest of the world region shows steady growth, driven by Latin America, the Middle East & Africa, where pickups are widely used for construction, mining, agriculture, and energy-related activities. Cost-sensitive markets favor drop-in liners and bed mats, but professional spray-on solutions are gaining traction among fleet operators seeking durability. Aftermarket channels dominate due to limited OEM bundling, while gradual infrastructure development and fleet modernization support long-term market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation, Installer Networks, and OEM Partnerships Shape Truck Bedliners' Competitiveness

The global truck bedliners market is shaped by continuous material innovation, expanding installer networks, and strengthening OEM supplier relationships. Leading players such as LINE-X, Rhino Linings, PPG, BASF, Axalta, Dow, Sika, and U-Pol compete through high-performance polyurea and polyurethane coatings, durable molded liners, and differentiated aftermarket solutions. Spray-on specialists focus on faster curing times, improved adhesion on steel and aluminum beds, and extended warranties, while chemical majors leverage formulation expertise and scale. Competitive advantage is increasingly built through certified installer networks, OEM and dealer-installed programs, and bundled accessory offerings that enhance per-vehicle revenue. Companies are also investing in low-VOC formulations, texture and color customization, and application efficiency to reduce labor time and costs. Strategic collaborations between coating suppliers, pickup OEMs, and dealership networks are intensifying to secure long-term volumes and aftermarket loyalty.

- In September 2024, LINE-X expanded its authorized installer network and introduced enhanced coating formulations, reinforcing its premium positioning and service-led competitive strategy in the market.

LIST OF KEY TRUCK BEDLINERS COMPANIES PROFILED IN REPORT

- Line-X LLC (U.S.)

- Rhino Linings Corporation (U.S.)

- PPG Industries Inc. (U.S.)

- BASF SE (Germany)

- Axalta Coating Systems Ltd. (U.S.)

- Dow Inc. (U.S.)

- Sika AG (Switzerland)

- U-Pol Ltd. (U.K.)

- SEM Products, Inc. (U.S.)

- Armorthane (U.S.)

- Speedliner (U.S.)

- KBS Coatings (U.S.)

- Raptor Coatings (U.K.)

- BedRug, Inc. (U.S.)

- Husky Liners, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: LINE-X announced it was entering 2026 after a strong 2025 marked by expanded partnerships and brand momentum. The update highlights partnerships aimed at strengthening franchise operations and scaling commercial upfitting, while continuing to anchor offerings around signature spray-on bedliners and related protective coatings.

- October 2025: RealTruck unveiled a record number of product showcases at SEMA 2025, including the Husky Liners EasyLock Bedliner and related protective accessories, signaling a broader product expansion strategy and reinforcing innovation momentum within the truck bedliners and truck accessories segment ahead of planned launches.

- September 2025: LEER announced it began offering WeatherTech’s truck/SUV accessories, explicitly including bed mats, ImpactLiner, and TechLiner bed protection products. This is a clear distribution expansion move, leveraging an established truck-cap/accessory storefront to expand market access for molded/thermoplastic bedliner alternatives to spray-in coatings.

- July 2025: RealTruck announced the acquisition of Husky Liners, integrating the well-known custom floor, cargo, and bed protection brand into its portfolio to expand product offerings and leverage RealTruck’s extensive distribution channels for future growth across multiple accessory categories, including truck bedliners and related protection solutions.

- February 2025: LINE-X stated it introduced an updated bedliner lineup (standard, premium, and MAX options) and expanded adjacent upfitting offerings via partnerships (e.g., window tint and towing equipment). The announcement also notes multi-location store expansion activity, reflecting how bedliner brands are bundling coatings with broader truck-accessory installation to raise ticket size.

REPORT COVERAGE

The global truck bedliners market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By Material Type, By Truck Type, By Application, and By Region |

| By Product Type |

|

| By Truck Type |

|

| By Material Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.25 billion in 2025 and is projected to reach USD 6.98 billion by 2034.

In 2025, the North Americas market value stood at USD 2.14 billion.

The market demand is expected to grow at a CAGR of 6.0% during the forecast period from 2026 to 2034.

The light-duty pickup trucks segment led the market.

Pickup truck sales and fleet expansion fuel bedliner demand, driving the market.

Top players in the market include LINE-X, Rhino Linings, PPG, BASF, Axalta, Dow, and Sika.

North America held the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us