Truck Refrigeration Unit Market Size, Share & Industry Analysis, By System Type (Diesel-engine TRUs, Electric TRUs (eTRUs), and Hybrid TRU), By Sales Channel (Factory-fit and Retrofits), By Vehicle Type (LCV, MCV, and HCV), By Mount Location (Front-mount, Roof-mount, and Under-mount), By End-User Industry (Food & Beverage Logistics, Pharmaceutical & Healthcare, Chemicals, Floriculture & Agricultural Exports, and Retail & E-commerce Grocery), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

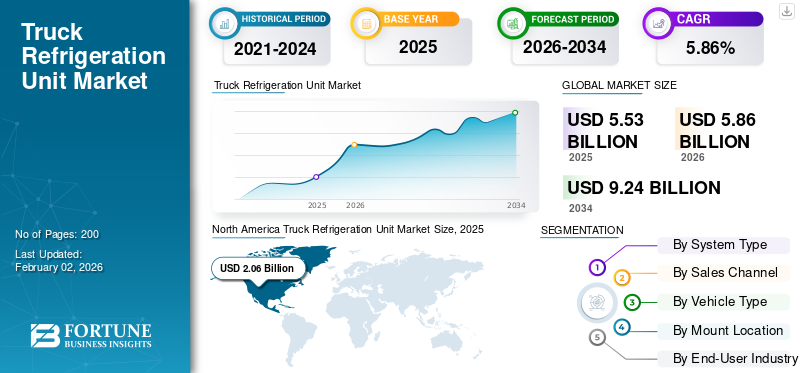

The global truck refrigeration unit market size was valued at USD 5.53 billion in 2025 and is projected to grow from USD 5.86 billion in 2026 to USD 9.24 billion by 2034, exhibiting a CAGR of 5.86% during the forecast period. North America dominated the truck refrigeration unit market with a market share of 37.25% in 2025.

Truck Refrigeration Units (TRUs) are specialized cooling systems installed on trucks and trailers to maintain controlled temperatures during the transportation of perishable goods. These units typically operate using diesel engines, electric power, or hybrid systems, and they ensure consistent cooling across short-haul and long-haul routes. TRUs are widely applied in industries such as food and beverage, pharmaceuticals, agriculture, chemicals, and e-commerce grocery logistics. They come in different mount configurations depending on vehicle size and cargo requirements. Their role is critical in securing supply chain integrity and meeting stringent safety and quality standards for temperature-sensitive goods.

The growth of the global truck refrigeration unit market is evolving rapidly, driven by rising demand for cold-chain logistics, urbanization, and growth in temperature-sensitive industries. Adoption of electric TRUs and hybrid technologies is accelerating as manufacturers and fleet operators respond to stricter emission norms and the push for sustainable logistics. Light commercial vehicles (LCVs) dominate urban last-mile delivery, while medium and heavy commercial vehicles (MCVs/HCVs) serve regional and long-haul transport. Food and beverage logistics remain the largest end-user, followed by pharmaceuticals and agriculture.

Major global players include Carrier Transicold, Thermo King/Ingersoll Rand, Daikin/Thermo King Japan, and Zanotti, each innovating in efficiency, durability, and low-emission technologies.

U.S. tariffs on imported components and finished refrigeration units have had a mixed influence on the global truck refrigerated unit market share. On one hand, higher tariffs on steel, aluminum, and certain electronics have increased input costs for U.S.-based manufacturers, prompting them to localize production and strengthen domestic supply chains. On the other hand, tariffs on imports from regions such as China have encouraged North American players such as Carrier Transicold and Thermo King to expand capacity within the U.S. This shift has created short-term price pressures but also stimulated regional manufacturing competitiveness and technological self-reliance in advanced TRU systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Temperature-Sensitive Freight to Drive Market Growth

Rapid expansion of temperature-sensitive freight, driven by growing fresh-food trade, perishable exports, pharmaceuticals (including cold-chain vaccines), and e-commerce grocery, is the primary engine for TRUs. Regulatory pressure to reduce local air pollution and greenhouse-gas emissions is forcing fleets and ports to replace diesel TRUs with electrified or zero-emission alternatives. California’s CARB has formal TRU reporting and is actively developing zero-emission TRU requirements, underpinning faster adoption in regulated markets.

Manufacturer investment and product launches, exemplified by major suppliers rolling out all-electric driven transport refrigeration unit lines and expanded connected solutions. Carrier Transicold’s Vector/eDrive updates and Thermo King’s all-electric program and partnerships are accelerating technology availability and commercial acceptance.

Economic and operational drivers also favor electrification: grid-powered operation reduces onsite NOx/PM exposure and can lower total cost of ownership where electricity/charging is economical, a trade-off quantified in EPA TRU emissions/economics guidance. Sustainability imperatives, cold chains account for a meaningful share of global food-system emissions, are prompting shippers and retailers to prioritize low-emission TRUs, creating OEM and fleet demand for efficient electric and hybrid TRU platforms.

MARKET RESTRAINTS

High Infrastructure and Energy Demands by Electric & Hybrid Refrigerated Systems Hampers Market Expansion

One of the crucial restraining factors for the global Truck Refrigeration Unit (TRU) market is the high infrastructure and energy demand required to support electric or hybrid refrigerated systems, especially for heavy-duty and long-haul operations. Electrified TRUs need reliable charging stations with enough power capacity, yet many major freight corridors lack sufficient high-capacity DC fast-charging infrastructure. For example, a 2023 study showed that only about 12% of public charging stations across key North American freight routes support outputs over 150 kW, forcing fleets to rely heavily on depot-charging and increase upfront capital costs.

Added weight, higher energy consumption, and cost penalties associated with electrification and higher cooling loads also add to the restraints. Some new technologies (such as multi-temperature TRUs or extreme cold-chain requirements) require significantly more power; diesel units remain more reliable in very cold environments. Additionally, grid upgrades are often necessary at facilities. A survey of cold chain operators revealed that 68% of U.S. facilities would need electrical upgrades costing between USD 250,000 and USD 800,000 per facility to fully support electrified TRU deployments. These combined factors, capital cost, operating complexity, and energy/grid constraints, limit adoption speed in many regions, particularly in less developed markets or areas with weak electricity reliability.

MARKET OPPORTUNITIES

Accelerating Electrification and Modernization of Cold-Chain Logistics to Create Lucrative Growth Opportunities

A major opportunity for the TRU market lies in the accelerating electrification and modernization of cold-chain logistics, driven by the rapid expansion of refrigerated storage and tighter emissions rules. Growing demand for temperature-controlled distribution from fresh food and seafood to vaccines and biologics is expanding warehouse and trailer electrification use cases. Public refrigerated warehouse capacity in the U.S. alone reached 2.51 billion gross cubic feet in 2023, indicating larger, more integrated cold-chain networks that require flexible, low-emission TRU solutions. Manufacturers are commercializing high-capacity engineless eTRUs capable of on-site grid operation and telematics integration (new models deliver up to 58,000 BTU/hr while supporting two-way fleet controls), enabling fleets to shift from diesel gensets to grid or battery power and lower operating costs. Regulatory programs and inventory reporting are encouraging fleet electrification pilots and depot-charging investments, creating a virtuous cycle of demand for electric TRUs, retrofit solutions, and facility upgrades. Combined with industry telematics and predictive maintenance, these trends open opportunities for suppliers to sell higher-value hardware plus software services (remote monitoring, energy-optimizing controls, and warranty/servicing contracts), transforming TRUs from commodity units into integrated fleet systems that reduce emissions, improve uptime, and lower total cost of ownership over the lifecycle.

TRUCK REFRIGERATION UNIT MARKET TRENDS

Adoption of Telemetry, Remote Diagnostics, and Real-Time Monitoring is One of the Significant Market Trends

One major trend in the TRU market is the rising integration of telemetry, remote diagnostics, and real-time monitoring into refrigeration units. Manufacturers are embedding sophisticated sensor networks, API-capable modules, and cloud-connected platforms to track performance, temperature stability, door metrics, engine run hours, fuel or battery states, and fault indicators. For example, Carrier Transicold’s Lynx Fleet telematics platform now supports up to five temperature sensors per multizone unit, dual satellite-cellular / cellular comms, with battery-backed reporting up to 10 days without vehicle power. Another advancement is the use of TRU Health dashboards, which shift service scheduling from calendar-based to performance-based maintenance, reducing downtime and wastage. These capabilities are critical for cold-chain compliance: fleets moving food or pharmaceuticals need strict monitoring and traceability, since even minor temperature excursions can invalidate high-sensitivity loads.

Meanwhile, cold-chain demand is expanding. In North America alone, cold-chain logistics infrastructure and refrigerated transportation are growing in response to rising demand for fresh, frozen, and processed food (with multiple policies and food safety mandates supporting it). The telematics trend allows operators to optimize fuel usage (or battery/diesel consumption), reduce spoilage, improve route planning, and ensure regulatory and customer compliance. As digital and IoT platforms mature, they are becoming a differentiating factor among TRU OEMs, driving the shift toward software + service business models beyond hardware alone.

Download Free sample to learn more about this report.

Segmentation Analysis

By System Type

Reliability and Independence from Vehicle Power Systems Drive the Diesel-engine TRUs Segment Growth

On the basis of system type, the market is classified into Diesel-engine TRUs, Electric TRUs (eTRUs), and Hybrid TRU.

The diesel-engine truck refrigeration units (TRUs) segment is projected to dominate the market, accounting for 73.52% of the global market share in 2026. Diesel-engine TRUs remain the most dominant system type due to their proven reliability and independence from vehicle power systems. They are critical for long-haul and cross-border transport where charging infrastructure for eTRUs is limited. Diesel TRUs offer high cooling capacity suitable for multi-temperature trailers, ensuring compliance with food safety standards and pharmaceutical cold-chain regulations. Despite emission concerns, demand persists, as evidenced by the California Air Resources Board estimating that over 70% of in-use TRUs in 2022 were diesel-powered. Manufacturers are upgrading diesel TRUs with cleaner engines, improved after treatment systems, and telematics integration to reduce emissions and improve efficiency. For instance, Thermo King recently launched ultra-low-emission models meeting stringent U.S. EPA Tier 4 standards. These advancements ensure diesel TRUs continue dominating while gradually transitioning fleets toward hybrid and electric-ready architectures.

By Sales Channel type

Constant Preference for Integrated, Warranty-Backed Systems Fuels Factory-Fit Segment Demand

In terms of sales channel type, the market is categorized into factory-fit and retrofits.

The factory-fit segment is expected to lead by sales channel, contributing 74.02% globally in 2026. This segment dominates the TRU sales channel as OEMs and fleet operators increasingly prefer integrated, warranty-backed systems over aftermarket retrofits. Factory-fitted TRUs provide better design compatibility, improved reliability, and seamless integration with truck electronics and telematics. This preference is further strengthened by regulations that require emission-compliant TRUs to be installed during new truck purchases. Industry updates show rising OEM partnerships with TRU manufacturers; for example, Carrier Transicold and major truck OEMs now offer factory-integrated engineless TRU options as standard on select electric and hybrid trucks. Moreover, European truck manufacturing data shows that nearly 65% of refrigerated vehicle registrations in 2023 were delivered with factory-fitted TRUs, underscoring OEM dominance. Factory-fit channels also support regulatory certification and global standardization, ensuring fleets comply with cross-regional mandates. This dominance is further reinforced by telematics-enabled OEM packages, which reduce lifecycle costs and enhance cold-chain visibility.

By Vehicle Type

Rising Urbanization and Commuter Transit Expansion Drive the Segment Growth

Based on vehicle type, the market is segmented into LCV, MCV, and HCV.

Heavy Commercial Vehicles (HCVs) segment is projected to remain dominant by vehicle type, accounting for 36.83% of the global market share in 2026 due to their critical role in bulk and long-haul cold-chain logistics. HCVs are essential for transporting large food and pharmaceutical shipments across intercity and international corridors, requiring robust TRUs with high cooling capacity. In North America, the Federal Highway Administration reports that over 45% of refrigerated freight ton-miles are moved by heavy trucks, highlighting their dominance. Additionally, HCVs are increasingly adopting multi-temperature TRUs to handle diverse loads in a single trip, such as frozen goods and fresh produce. Major OEMs such as Daimler and Volvo Trucks are working with TRU manufacturers to integrate hybrid-ready and electric-capable TRUs into HCV fleets, ensuring compliance with zero-emission regulations in California and the EU. This combination of payload capacity, route flexibility, and technological upgrades ensures that HCVs remain the backbone of refrigerated transport.

To know how our report can help streamline your business, Speak to Analyst

By Mount Location

Superior Cooling Capacity of the Roof Mount Segment Drives its Segmental Growth

Based on mount location, the market is classified into front-mount, roof-mount, and under-mount.

The roof-mount segment dominates the market due to its superior cooling capacity, making it ideal for large trailers and intercity or international cold-chain distribution. Positioned at the trailer’s top, these units can deliver consistent airflow and support multi-zone configurations, which are essential for transporting different categories of perishables simultaneously. Leading manufacturers such as Thermo King and Carrier Transicold continue to invest in roof and front-mount units with advanced telematics, fuel-saving technologies, and hybrid-ready systems. For example, Carrier’s Vector series offers up to 58,000 BTU/hr cooling capacity, supporting demanding pharmaceutical and frozen food shipments. The ability to handle larger volumes, integrate with remote monitoring platforms, and comply with regulatory standards ensures that roof-mount TRUs remain the preferred choice for fleet operators globally.

By End-User Industry

Strict Global Regulations on Food Safety and the Rising Demand for Fresh, Frozen, and Processed Foods Drive the Food & Beverage Logistics Segment Growth

Based on end-user industry, the market is segregated into food & beverage logistics, pharmaceutical & healthcare, chemicals, floriculture & agricultural exports, and retail & e-commerce grocery.

The Food & beverage segment is expected to lead by end-user industry, holding 41.86% of the global market share in 2026. This dominance stems from strict global regulations on food safety and the rising demand for fresh, frozen, and processed foods across international trade routes. The U.S. Department of Agriculture reported that in 2023, over 50% of U.S. agricultural exports required temperature-controlled shipping, highlighting TRUs’ critical role.

European logistics data indicates that food accounts for nearly two-thirds of all refrigerated vehicle activity. OEMs are responding by designing multi-temperature TRUs that can carry frozen, chilled, and ambient products in a single load, reducing costs and boosting efficiency. Growth in quick-service restaurants, e-commerce grocery, and urban cold storage further fuels TRU demand in this sector. With continuous expansion in perishable trade and consumer demand for fresh produce, food, and beverage logistics will remain the key driver of TRU adoption.

TRUCK REFRIGERATION UNIT MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Truck Refrigeration Unit Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 2.06 billion, contributing 37.25% to global market revenue, and is projected to grow to USD 2.17 billion in 2026. North America’s TRU market is anchored by a very large, mature cold-chain ecosystem where refrigerated warehousing, long-haul fleet operations, and regulatory scrutiny converge to sustain demand. Large public and private cold-storage networks support year-round food distribution and export logistics; U.S. public warehouse refrigerated storage totaled 2.51 billion gross cubic feet in 2023, underpinning the use of heavy truck-and-trailer reefers for regional and national routes. Fleet modernization programs and state rules (notably California’s TRU programs) are pushing owners toward cleaner, telematics-enabled units and depot-electrification pilots. At the same time, large logistics integrators concentrate buying power, with major cold-storage operators managing billions of cubic feet of temperature-controlled space across North America. These combined factors big installed cold storage, stringent emissions reporting, and fleet consolidation, keep North America the dominant TRU market and a testing ground for new eTRU and hybrid solutions. The U.S. market is projected to reach USD 1.53 billion by 2026.

Europe

The Europe market accounted for USD 1.68 billion in 2025, representing 30.38% of the global industry, and is expected to reach USD 1.79 billion in 2026. Europe’s TRU demand is driven by dense intra-EU food movement, cross-border trade, and a strong regulatory emphasis on food safety and emissions. Road freight statistics show that food products, beverages, and tobacco are the single largest goods group by tonne-kilometres, exceeding 312.2 billion tkm, which translates into a sustained need for refrigerated trailers and trucks across national borders. EU member states are investing in last-mile cold logistics and upgrading regional depots to support multi-temperature loads and stricter traceability. OEMs and TRU makers increasingly offer factory-integrated, telematics-enabled units tailored for EU type-approval and emissions targets. the UK market is projected to reach USD 0.26 billion by 2026 and the Germany market is projected to reach USD 0.47 billion by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 1.5 billion in 2025, capturing 27.21% of the global market share, and is projected to reach USD 1.61 billion in 2026. Asia Pacific’s rapid urbanization, growing perishable trade, and major cold-storage investments are accelerating TRU demand faster than other regions. China’s refrigerated warehouse and logistics build-out expanded materially (reported warehouse capacity rose to around 228 million cubic metres of cold storage). In contrast, new-energy refrigerated truck registrations in China surged in early 2024 as fleets trial low-emission reefers. India’s nationwide cold-chain expansion (tens of millions of tonnes of storage capacity) and government programmes to fund integrated cold-chain projects are pulling fleets toward modern TRUs, retrofits, and depot electrification. High population densities, expanding retail cold-chain, and stronger pharma cold-logistics are creating large incremental annual demand, making the Asia Pacific the fastest-growing TRU region. The Japan market is projected to reach USD 0.18 billion by 2026, the China market is projected to reach USD 0.93 billion by 2026, and the India market is projected to reach USD 0.30 billion by 2026.

Rest of the World

The Rest of the World market was valued at USD 0.29 billion in 2025, capturing 5.16% of global revenue, and is estimated to reach USD 0.29 billion in 2026. In many developing regions, such as Latin America, Africa, and parts of the Middle East, TRU growth is uneven, yet it presents major upside as cold-chain coverage is incomplete and post-harvest loss rates remain high. Governments and multilateral programs are funding hub-and-spoke cold-chain projects, airport perishables terminals, and corridor upgrades, while private logistics operators are expanding reefers and refrigerated services to reduce spoilage and tap export markets. As infrastructure investments and policy support rise, these regions offer significant long-term TRU market expansion potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Leadership, Strong Service Networks, and Continuous Innovation by Key Players Drive Competitive Edge

Carrier Transicold is widely regarded as the leading global manufacturer of truck refrigeration units, a position built on decades of technological leadership, strong service networks, and continuous innovation. Its dominance stems from early adoption of high-capacity, energy-efficient TRUs and pioneering electric and hybrid-ready refrigeration systems. Carrier’s global distribution and after-sales service reach allow it to support fleets in over 150 countries, strengthening reliability and brand trust. Its TRU portfolio spans engineless electric Vector series, diesel-powered Supra and X4 units, and hybrid-ready models. Integration of telematics through Lynx Fleet further positions Carrier as a first-choice partner for modern cold-chain fleets.

Thermo King is also among the major global TRU manufacturers, closely competing with Carrier through strong brand heritage, continuous R&D, and integration with parent company Ingersoll Rand’s global resources. Its leadership is tied to innovation in sustainable refrigeration, notably with the Advancer series, which delivers improved fuel efficiency and lower emissions. Thermo King’s TRU portfolio includes diesel-powered T-Series and Precedent units, fully electric E-Series, and hybrid solutions tailored for both light and heavy commercial vehicles. Its investments in zero-emission refrigerated trailers and smart monitoring solutions make it a key player, solidifying its position as the second leading global supplier.

LIST OF KEY TRUCK REFRIGERATION UNIT COMPANIES PROFILED

- Thermo King (U.S.)

- Carrier Transicold (U.S.)

- Daikin Industries (Japan)

- Zanotti (Italy)

- DENSO Corporation (Japan)

- Mitsubishi Heavy Industries Thermal Systems (Japan)

- Webasto Group (Germany)

- FRIGOBLOCK GmbH (Germany)

- Sanden Corporation (Japan)

- Subros Limited (India)

- Kingtec Group (China)

- Guchen (China)

- Glen Refrigeration (China)

- Advanced Temperature Control (ATC) (Canada)

- Klinge Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Thermaxx and Thermo King partnered to combine Transport Refrigeration Services’ (TRS) Thermaxx refrigerated bodies with Thermo King units to deliver improved performance for operators. This combination is designed to give operators reliable temperature control, reduced fuel consumption, and bodies that continue performing year after year. Thermaxx’s advanced panel technology delivers exceptional insulation and structural integrity, ensuring consistent performance even under demanding conditions.

- In July 2025, Carrier Transicold expanded its line of Supra High Efficiency (HE) truck-mounted refrigeration units by launching the Supra HE 11 Multi-Temperature (MT) and HE 13 MT. Available in standard and silent versions, the Supra HE 11 MT and HE 13 MT units support a wide range of refrigerated transport needs, supporting various configurations, including a double double-compartment setup for the Supra HE 11 and the option of either a double or triple-compartment setup for the Supra HE 13 MT.

- In April 2025, Thermo King recently launched the Legend series with the first Asian-made transport refrigeration unit production line at its plant in Wujiang, China, set to serve the entire Asia Pacific market. In line with the company's “Future Factory” initiative, the new production line boosts Legend's supply chain localization by 60%, enhancing delivery speed, stability, and flexibility to drive the cold chain logistics towards a more efficient, intelligent, and sustainable future.

- In November 2024, Carrier Refrigeration launched Transform Line, a range of modernization and retrofit solutions for truck, trailer, rail, and container refrigeration systems worldwide. Transform Line would help transport refrigeration customers meet future operational and regulatory demands, while maximizing the return on their investments from their existing fleets.

- In August 2024, Carrier Transicold introduced a new maintenance dashboard for its Lynx Fleet telematics platform. The dashboard allows users to create customized preventive maintenance schedules for transport refrigeration units (TRUs) based on performance data collected and communicated in real time.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.86% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By System Type, By Sales Channel, By Vehicle Type, By Mount Location, By End-User Industry, and Region |

|

By System Type |

· Diesel-engine TRUs · Electric TRUs (eTRUs) · Hybrid TRU |

|

By Sales Channel |

· Factory-fit · Retrofits |

|

By vehicle Type |

· LCV · MCV · HCV |

|

By Mount Location |

· Front-mount · Roof-mount · Under-mount |

|

By End-User Industry |

· Food & Beverage Logistics · Pharmaceutical & Healthcare · Chemicals · Floriculture & Agricultural Exports · Retail & E-commerce Grocery |

|

By Geography |

· North America (By System Type, By Sales Channel, By Vehicle Type, By Mount Location, By End-User Industry, and By Country) o U.S. o Canada o Mexico · Europe (By System Type, By Sales Channel, By Vehicle Type, By Mount Location, By End-User Industry, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By System Type, By Sales Channel, By Vehicle Type, By Mount Location, By End-User Industry, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World ( By System Type, By Sales Channel, By vehicle Type, By Mount Location, By End-User Industry , and By Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 5.86 billion in 2026 to USD 9.24 billion by 2034

The truck refrigeration unit market trend is expected to exhibit a CAGR of 5.86% during the forecast period (2026-2034).

The diesel-engine TRUs segment leads the market by system type.

Expansion of temperature-sensitive freight is the key factor driving the market.

Top players in the truck refrigeration unit industry include Carrier Transicold (U.S.), Thermo King/Ingersoll Rand (U.S.), Daikin/Thermo King Japan (Japan), Zanotti (Italy), and Songz Automobile Air Conditioning (China).

North America dominates the market.

Major factors favoring that are expected to favor product adoption is the rising demand for fresh, frozen, and processed foods drives demand for cold logistics.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us