Turret System Market Size, Share, Industry & Russia-Ukraine War Analysis, By Platform (Land, Naval, and Airborne), By Technology (Hydraulic, Electric/Electro-mechanical, Hybrid, and Sensor tech class (optical, IR, radar, lidar)), By Deployment Mode (Vehicle-mounted, Naval hull, Stationary, and Drone-mounted), By Weapon (Small-caliber (≤ 30 mm), Medium-caliber (30–50 mm), Large-caliber, and Missile/Rocket integrated), By Component (Turret Drive (motors, gearboxes), Turret Control/Fire Control Electronics, Stabilization/Gimbals, and Others), and Regional Forecast, 2026-2034

turret system market Overview

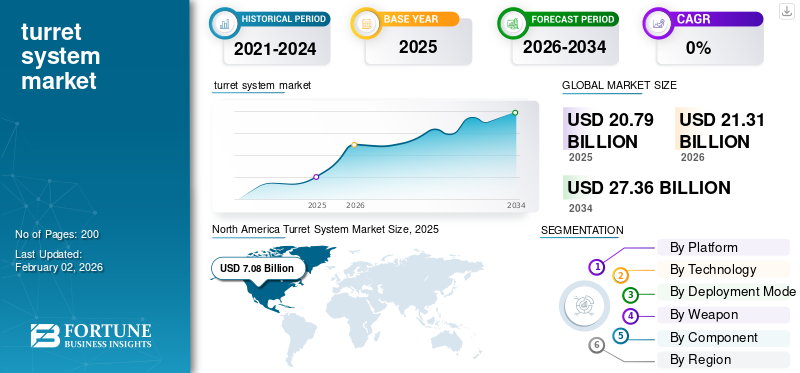

The global turret system market size was valued at USD 20.79 billion in 2025. The market is projected to grow from USD 21.31 billion in 2026 to USD 27.36 billion by 2034, exhibiting a CAGR of 3.17% during the forecast period. North America dominated the global market with a share of 34.06% in 2025.

The global turret system market is undergoing a steady transformation driven by modernization, autonomy, and modularity. Turret systems encompassing weapon mounts, remote stations, and sensor platforms are critical for enhancing precision, protection, and situational awareness across land, naval, and airborne domains. The market is expanding as countries replace hydraulic and manually operated turrets with electro-mechanical, AI-assisted, and stabilized systems capable of engaging diverse threats, including drones and armored targets. Rising geopolitical tensions, particularly in Europe and Asia Pacific, are fueling defense procurement and joint production initiatives. Concurrently, technological advances in electric drives, fire-control software, and sensor fusion are redefining turret functionality. The convergence of these trends positions turret systems as an indispensable subsystem in modern warfare and defense modernization programs.

The turret system landscape is led by a mix of established defense primes and emerging innovators. Major contributors include BAE Systems (U.K.), Rheinmetall AG (Germany), Leonardo S.p.A. (Italy), Elbit Systems (Israel), and General Dynamics (U.S.), all offering comprehensive land and naval turret solutions. Supporting firms such as Northrop Grumman, Moog, FN Herstal, Thales, and Denel specialize in actuation, control, and stabilization technologies. Additionally, Asian defense manufacturers in India, South Korea, and China are rapidly expanding indigenous turret capabilities, intensifying global competition and diversifying the supply base for both manned and unmanned systems.

Download Free sample to learn more about this report.

Turret System Market KEY TAKEAWAYS

- 2025 Market Size: USD 20.79 billion

- 2026 Market Size: USD 21.31 billion

- 2034 Forecast Market Size: USD 27.36 billion

- CAGR: 3.17% from 2026–2034

- North America dominated the global turret system market with a 34.06% share in 2025.

- The land segment is projected to hold a 62.93% share in 2026.

- The vehicle-mounted segment is expected to account for a 58.19% share in 2026.

North America

North America USD 7.26 billion in 2026. Strong demand from military fleet modernization, AI-assisted fire control systems, and advanced naval and armored upgrades.

Europe

Europe USD 6.32 billion in 2026. Rising defense spending and post-conflict rearmament programs driving upgrades of vehicle and naval turret systems.

Asia Pacific

Asia Pacific USD 5.97 billion in 2026. Rapid growth driven by indigenous defense modernization, border security needs, and unmanned turret system adoption.

U.S.

U.S. USD 6.29 billion in 2026. Continuous R&D in autonomous and electric turret systems supporting long-term defense modernization.

Japan

Japan USD 0.76 billion in 2026. Increasing focus on domestic defense production and advanced turret system integration.

Read More

RUSSIA-UKRAINE WAR IMPACT

Russia-Ukraine Conflict-Induced Acceleration in Defense Modernization

The Russia–Ukraine war has profoundly reshaped the global turret system market, driving acceleration in procurement and modernization cycles. The conflict has demonstrated the renewed importance of armored vehicles, remote weapon stations, and stabilized turret systems in high-intensity, drone-saturated warfare. Ukrainian and Russian forces have relied heavily on turret-equipped platforms for both offensive and defensive operations, proving that mobility, survivability, and rapid target engagement remain decisive on the modern battlefield. NATO member states and European allies have consequently boosted defense budgets, fast-tracked vehicle replacement programs, and reactivated dormant manufacturing lines for armored and naval turret systems.

The U.S., Germany, Poland, the U.K., and South Korea witnessed surging orders for remote-controlled, electric, and modular turret systems to replenish stockpiles and upgrade fleets. At the same time, global supply chains have tightened, particularly for optics, gyroscopes, and electro-mechanical actuators, causing production bottlenecks. The war has also validated the demand for unmanned turrets and autonomous fire-control systems capable of engaging drones and loitering munitions. As a result, the conflict has effectively reset global defense priorities, ensuring the turret system market growth remains on an elevated, war-driven growth trajectory.

TURRET SYSTEM MARKET TRENDS

Electrification, Autonomy, and Modular Integration are the Leading Market Trends

The overarching trend in the turret system market is the shift toward electrified, intelligent, and modular architectures across land, naval, and airborne platforms. Traditional hydraulic turrets are being rapidly replaced by electric and electro-mechanical drives, which offer higher reliability, reduced maintenance, and easier integration with digital fire-control systems. The adoption of AI-enabled targeting, sensor fusion, and stabilized optics is transforming turrets from simple weapon mounts into sophisticated, networked combat subsystems. Across NATO and allied nations, modular turret designs allow for quick reconfiguration between gun, missile, or surveillance roles, extending platform lifespans and reducing lifecycle costs. On the airborne side, lightweight gimbal turrets are integrating multi-sensor packages for ISR (Intelligence, Surveillance, and Reconnaissance) missions, at the same time naval systems increasingly use automated fire-control algorithms for close-in defense. Another dominant trend is the proliferation of remote and unmanned turrets, particularly for armored vehicles and UAVs, enhancing crew survivability. Cybersecurity and digital standardization are becoming integral to turret system design as defense forces transition to network-centric warfare. Overall, the market is pivoting toward electrified, autonomous, and software-defined turret ecosystems, blending mechanical precision with digital intelligence.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Defense Modernization and Rising Cross-Border Tensions to Boost Market Growth

The primary driver for turret system demand is the global wave of defense modernization triggered by rising geopolitical tensions and the re-emergence of conventional warfare. Countries across Europe, Asia, and the Middle East are actively replacing legacy hydraulic turrets with digital, electric, and stabilized systems capable of operating in electronic warfare environments. The steady increase in defense budgets particularly in the U.S., Germany, India, and China is fueling procurement of next-generation armored vehicles, naval guns, and UAV-mounted turret platforms. The operational emphasis on crew protection and precision lethality underpins the adoption of remote weapon stations and unmanned turrets. Additionally, advancements in AI, fire-control computing, and sensor fusion have made modern turret systems critical to multi-domain command networks. In Asia Pacific and Eastern Europe, border tensions and modernization programs are sustaining continuous demand for lightweight and modular turret solutions. Collectively, these trends ensure that defense modernization and geopolitical competition remain persistent growth drivers of the turret system market share.

MARKET RESTRAINTS

Cost, Complexity, and Export Control Barriers to Hamper Market Growth

Despite robust demand, the turret system market faces structural restraints centered on high system cost, integration complexity, and export restrictions. Modern turrets are expensive to design, test, and qualify those with AI-assisted fire control, electro-mechanical actuation, and advanced stabilization. Smaller defense budgets, particularly in emerging countries, often delay procurement or limit scope to retrofits rather than new builds. Complex integration requirements with vehicle and ship subsystems (power, recoil, communication) further increase time and cost. Supply chain dependence on specialized components such as precision bearings, servo motors, and optical sensors introduces vulnerability to global shortages. Moreover, export control laws (e.g., ITAR, EU defense restrictions) can hinder cross-border collaboration and sales, fragmenting the global supply base. Another constraint is maintenance burden: electric turrets demand highly trained technical personnel and specialized parts. These challenges collectively limit market scalability in cost-sensitive regions, moderating growth rates despite rising defense budgets.

MARKET OPPORTUNITIES

Rise of Unmanned, Export, and Retrofit Segments to Create Market Opportunities

Significant opportunities exist in unmanned and retrofit turret systems, alongside export potential to developing defense markets. As global militaries prioritize crew safety and precision engagement, unmanned turrets remotely operated or AI-assisted are in rising demand for both land and naval platforms. Retrofitting older armored vehicles and patrol ships with modern electric or sensor-fused turrets is a cost-effective alternative to full platform replacement, creating a large upgrade market across Europe, Asia, and the Middle East. Emerging defense producers in India, South Korea, and Türkiye are also targeting export opportunities by developing indigenously manufactured turret systems aligned with global standards but at lower cost. The shift to multi-mission modular turrets capable of switching between guns, missiles, and sensor payloads offers a new commercial niche for system integrators and component suppliers. Additionally, the growth of UAV-mounted and small-caliber turret systems for surveillance and counter-drone applications opens fresh avenues in the aerospace segment. As countries expand defense cooperation and localize manufacturing, companies that can deliver modular, interoperable, and autonomous turret technologies stand to capture significant market share.

MARKET CHALLENGES

Technological Transition and Cybersecurity Risks are Major Challenges for Growth

The turret system industry faces complex challenges as it transitions toward digital, autonomous, and networked architectures. Integrating AI-driven targeting, multi-sensor fusion, and software-defined fire control not only increases system capability but also cyber vulnerability. Networked turrets on unmanned platforms present potential entry points for cyber intrusions, demanding robust encryption and real-time monitoring. Another major challenge is achieving interoperability and standardization among platforms from different OEMs and nations, particularly in multinational defense coalitions. Technologically, replacing hydraulic mechanisms with electric or hybrid drives requires redesigning core mechanical structures, introducing long qualification cycles. The defense sector’s conservative certification culture slows adoption of innovative materials and automation techniques. Additionally, the increasing density of UAVs, loitering munitions, and directed-energy systems is redefining battlefield dynamics, forcing turret designers to adapt rapidly. Balancing cutting-edge digitalization with battlefield ruggedness, cybersecurity, and affordability remains the defining challenge for turret manufacturers.

SEGMENTATION ANALYSIS

By Platform

Global Modernization and Border Conflicts Drives Land Segment Growth

By platform, the market is segmented into land, naval, and airborne.

In 2026, the land segment captured the largest share and is anticipated to dominate with a 62.93% share. The segment’s dominance is led by widespread modernization of armored vehicles, infantry fighting vehicles, and tanks. Rising border conflicts in Europe and Asia are compelling nations to replace legacy systems with stabilized, modular, and unmanned turrets, enhancing mobility, survivability, and network-enabled firepower on the ground.

The naval segment is expected to grow at a CAGR of 2.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Electric and Electro-Mechanical Systems are Highly Preferred Owing to Reliability and Efficiency

By technology, the segment is classified into hydraulic, electric/electro-mechanical, hybrid, and sensor tech class (optical, IR, radar, lidar).

The electric/electro-mechanical segment attained the largest market share and is anticipated to dominate with a 42.98% share in 2026. The electric/electro-mechanical turrets are in high demand as militaries transition from hydraulic systems to lighter, more efficient electric drives. These systems offer superior precision, lower maintenance, and smoother stabilization, supporting integration with autonomous and remote-controlled platforms. Their energy efficiency and digital compatibility make them vital for next-generation defense vehicles.

The hybrid demining segment is expected to grow at a CAGR of 3.2% over the forecast period.

By Deployment Mode

Vehicle-Mounted Turrets Experience High Demand Due to Operational Flexibility

The deployment mode segment is classified into vehicle-mounted, naval hull, stationary, and drone-mounted.

The vehicle-mounted segment held the largest market share in 2025 and will lead in 2026 with a 58.19% share. Demand for vehicle-mounted turrets is accelerating as forces prioritize mobility, modularity, and rapid deployability. Mounted turrets enable armored columns, patrol convoys, and reconnaissance units to maintain lethal readiness while moving. The rise in remote weapon stations and mobile artillery platforms further strengthens this segment’s strategic importance and procurement momentum.

The drone-mounted segment is expected to grow at a CAGR of 5.2% over the forecast period.

By Weapon

Small-Caliber (≤ 30 mm) Systems Lead Due to its Lightweight and Unmanned Applications

By weapon, the market is classified into small-caliber (≤ 30 mm), medium-caliber (30–50 mm), large-caliber, and missile/rocket integrated.

In 2026, the small-caliber (≤ 30 mm) segment held the leading position and will dominate with an anticipated 30.55% share. The segment’s strong demand is led by its suitability for light armored vehicles, UAVs, and naval patrol craft. These systems deliver effective firepower with minimal recoil and weight, aligning with the defense trend toward unmanned, fast-deploying, and cost-efficient combat platforms across multiple operational environments.

The medium-caliber (30–50 mm) segment is expected to grow at a CAGR of 3.3% over the forecast period.

By Component

Digitization Drive Increased Demand for Turret Control and Fire-Control Electronics

By component, the market is classified into turret drive (motors, gearboxes), turret control/fire control electronics, stabilization/gimbals, and others.

The turret control/fire control electronics component led in 2024 and will capture a 32.95% leading market share in 2025 as armed forces embrace AI, automation, and sensor fusion. Modern combat demands real-time target acquisition and precision engagement. Integration of digital fire-control modules and networked battle management systems makes this segment central to the evolution of smart and autonomous turrets.

The turret drive (motors, gearboxes) segment is expected to grow at a CAGR of 3.2% during the forecast period.

TURRET SYSTEM MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

North America Turret System Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

The North America region captured 34.06% of the global market in 2025, generating USD 7.08 billion in revenue, and is projected to reach USD 7.26 billion in 2026. Demand in this region is led by the U.S., driven by the modernization of armored fleets, naval turret upgrades, and advanced remote weapon stations. Focus on AI-assisted fire control and electric turret drives sustains consistent demand, with exports supporting regional manufacturing stability and incremental growth.

In 2026, the U.S. market is estimated to reach USD 6.29 billion as it remains the world’s largest market, powered by continuous R&D investment, autonomous turret development, and modernization of Abrams, Stryker, and naval platforms. Strong funding for electric and AI-integrated systems ensures long-term demand stability, with parallel export programs supporting allied nations’ defense requirements.

Europe

Europe maintained a strong presence in the global market, reaching USD 6.18 billion in 2025, accounting for 29.71% share, and is expected to reach USD 6.32 billion in 2026. Europe’s demand is surging due to rearmament programs and fleet replenishment following the Russia–Ukraine conflict. Germany, the U.K., Poland, and France are rapidly upgrading vehicle and naval turret systems with electric drives and modular payloads, pushing Europe into its strongest defense procurement phase in decades. The UK market is projected to reach USD 1.64 billion by 2026, while the German market is projected to reach USD 1.78 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific region generated USD 5.8 billion, contributing 27.88% to global market revenue, and is projected to grow to USD 5.97 billion in 2026, as turret demand is expanding fastest, driven by India, China, South Korea, and Japan pursuing domestic production and indigenous modernization. Border tensions, UAV proliferation, and emphasis on unmanned turret systems are fueling investments across land, air, and naval platforms, positioning the region as the market’s primary growth engine. The Japan market is projected to reach USD 0.76 billion by 2026, the China market is projected to reach USD 2.31 billion by 2026, and the India market is projected to reach USD 1.89 billion by 2026.

Rest of The World

In 2025, the market in the rest of the world is set to record USD 1.74 billion. In the Middle East, Africa, and Latin America, demand is episodic but high-value, centered on border defense and armored vehicle modernization. Gulf states, Israel, and Brazil are key buyers, focusing on remote-controlled and counter-drone turret systems suited to asymmetric warfare and mobile security missions.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Defense Leaders Focus on Incorporating Mechanical Precision with Digital Intelligence to Gain Market Advantage

The global turret system market is dominated by defense leaders integrating mechanical precision with digital intelligence. BAE Systems (U.K.), Rheinmetall (Germany), Leonardo (Italy), Elbit Systems (Israel), and General Dynamics (U.S.) hold major shares through full-system production. Supporting technology providers Moog, Thales, FN Herstal, and Northrop Grumman supply critical components such as drives, fire-control electronics, and stabilization units. Emerging producers from India, South Korea, and Türkiye are entering the field with modular, export-oriented turret solutions. Collectively, these firms drive innovation in electric drives, AI-enabled targeting, and unmanned turret integration, shaping the next generation of defense lethality systems.

LIST OF KEY TURRET SYSTEM COMPANIES PROFILED

- BAE Systems plc (U.K.)

- Rheinmetall AG (Germany)

- Leonardo S.p.A (Italy)

- Elbit Systems Ltd (Israel)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Moog Inc (U.S.)

- FN Herstal S.A (Belgium)

- Denel SOC Ltd (South Africa)

KEY INDUSTRY DEVELOPMENTS

- September 2025 - London Marine Consultants maintained its successful trajectory in Vietnam by securing a new contract to supply an external turret mooring system for the Block B floating storage and offloading vessel. Turret mooring systems are essential for Floating Storage and Offloading Vessels (FSOs) as they ensure the vessels remain stationary and serve as a channel for oil production.

- August 2025 - The United States Marine Corps granted a full-rate production contract to Kongsberg Defence & Aerospace (‘KONGSBERG’) worth USD 330 million for the 30mm remote turret associated with the Amphibious Combat Vehicle 30mm program (ACV-30).

- April 2025 - Elbit Systems Ltd. secured a contract valued at around USD 100 million to provide its state-of-the-art UT30 MK2 unmanned turret systems to General Dynamics European Land Systems (GDELS). These systems are set to be installed on the ASCOD armored fighting vehicles and will be delivered to a NATO European nation.

- March 2025 - Curtiss-Wright Corporation announced that it received several contracts to supply its turret drive aiming and stabilization technology to Rheinmetall. This technology will be utilized on the German Army's Boxer Heavy Weapon Carrier as well as on the Lynx infantry fighting vehicles (IFV) for the Hungarian Ministry of Defence (MoD).

September 2022 - Elbit Systems Ltd. announced that it has been awarded a contract worth USD 80 million to provide unmanned turrets for Armored Fighting Vehicles ("AFVs") for a country in Asia Pacific. This contract is set to be executed over a span of three years.

REPORT COVERAGE

The research report regarding the expansion of the turret system market provides an in-depth analysis by identifying the key companies, product categories, and main applications within the industry. Additionally, the report highlights market trends and notable developments in this field. In conjunction with the aforementioned aspects, the report includes several factors that have contributed to the rapid market growth seen in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2032 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.17% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By Technology

|

|

|

By Deployment Mode

|

|

|

By Weapon

|

|

|

By Component

|

|

|

By Geography North America (By Platform, Technology, Deployment Mode, Weapon and Component)

Europe (By Platform, Technology, Deployment Mode, Weapon and Component)

Asia Pacific (By Platform, Technology, Deployment Mode, Weapon and Component)

Rest of the World (By Platform, Technology, Deployment Mode, Weapon and Component)

|

Frequently Asked Questions

According to Fortune Business Insights, the market value stood at USD 20.79 billion in 2025 and is projected to reach USD 27.36 billion by 2034.

The market is projected to grow at a CAGR of 3.17% during the forecast period.

The electric/electro-mechanical technology is the leading segment.

Land is the leading segment of the global market, based on platform.

BAE Systems plc (UK), Rheinmetall AG (Germany), Leonardo S.p.A (Italy), Elbit Systems Ltd (Israel), Northrop Grumman Corporation (U.S.) are some of the leading OEMs in the market.

North America is projected to capture the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us