Two Wheeler Rubber Hoses and Tubing Market Size, Share & Industry Analysis, By Vehicle Type (Motorcycles, Scooters, Mopeds, Three Wheelers, and Tractors), By Propulsion (ICE and Electric), By Product Type (Fuel Hose, Breather Hose, Radiator Hose, Air Intake Hose, Vacuum Hose, Tube Hose/Rubber Tubing Assemblies, & Others) By Material Type (EPDM Rubber, NBR, Silicone, Neoprene, Thermoplastic Elastomers, FKM, PBT/PA12/PA66 and Others), By Application (Engine System, Cooling System, Air Intake System, Emission Control System, & Others), By Sales Channel, and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

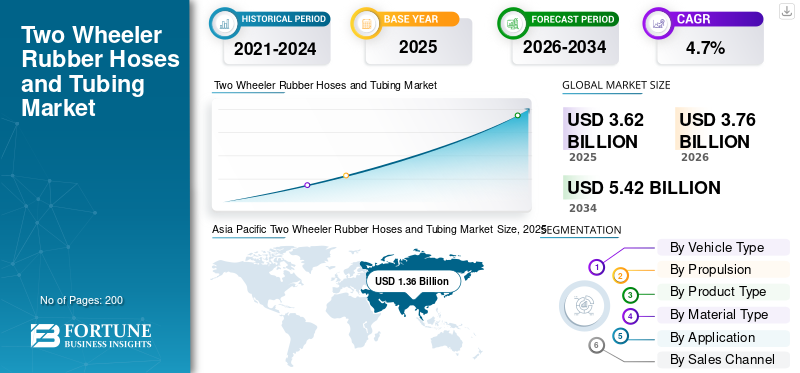

The two wheeler rubber hoses and tubing market size was valued at USD 3.62 billion in 2025. The market is projected to grow from USD 3.76 billion in 2026 to USD 5.42 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the global two wheeler rubber hoses and tubing market with a market share of 37.57% in 2025.

The two wheeler rubber hoses and tubing market represents the supply of flexible rubber components used to transport fluids, air, and fuel within two-wheelers. These include rubber hoses and tubing assemblies installed across engine, braking, fuel delivery, cooling, and emission control systems. Their primary function is to ensure safe and efficient fluid transfer while withstanding heat, pressure, and vibration during vehicle operation.

Market growth is closely linked to global two-wheeler production, especially in commuter-heavy economies. Motorcycles and scooters require multiple hose types with high oil resistance and ozone resistance to maintain performance under varying environmental conditions. As emission regulations tighten, demand for higher-quality hoses that extend service life and reduce leakage risks has increased.

Technological improvements in elastomer compounds, reinforcement layers, and hose construction are reshaping product standards. Manufacturers such as Polyrub, Gates Corporation, and Continental are increasingly using advanced EPDM and synthetic rubber blends to improve durability and reliability. The aftermarket also plays a key role, as hoses are wear-and-tear components requiring periodic replacement over the vehicle lifecycle.

Looking ahead, the industry will evolve through improved material formulations, lightweight designs, and enhanced resistance properties. As electrification is emerging, internal combustion engine dominance in two-wheelers ensures continued demand for conventional rubber hose applications. Growth in personal mobility, rising maintenance awareness, and steady OEM demand will support long-term market stability.

Download Free sample to learn more about this report.

Two Wheeler Rubber Hoses and Tubing Market Key Takeaways

- 2025 Market Size: USD 3.62 Billion

- 2026 Market Size: USD 3.76 Billion

- 2034 Forecast Market Size: USD 5.42 Billion

- CAGR: 4.7% from 2026–2034

- Asia Pacific dominated the two wheeler rubber hoses and tubing market with a 37.57% share in 2025.

- The motorcycles segment held the largest share of the market in 2025.

- The OEM segment accounted for the leading market share in 2025.

Asia Pacific

Asia Pacific led the global market due to strong two-wheeler production and high commuter dependence.

North America

North America is witnessing steady growth driven by recreational and premium motorcycle demand.

Europe

Europe's market is supported by premium motorcycles and stringent quality standards.

U.S.

Aftermarket replacement demand and longer vehicle ownership cycles support market growth.

Japan

Strong automotive manufacturing capabilities and demand for advanced vehicle components support the market.

Read More

Two Wheeler Rubber Hoses and Tubing MARKET TRENDS

Increasing Use of Advanced EPDM Compounds Improves Hose Durability

Manufacturers are increasingly using EPDM and synthetic rubber blends to enhance oil resistance, heat tolerance, and ozone resistance. This trend improves hose reliability and extends service life, aligning with OEM requirements for reduced warranty claims and improved vehicle longevity.

- For instance, in April 2024, Continental AG highlighted increased use of EPDM rubber in automotive hoses to improve heat resistance, ozone resistance, and durability under demanding two-wheeler operating conditions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Two-Wheeler Production Sustains Demand for Rubber Fluid Transfer Components

Growing two-wheeler production in Asia and emerging markets is a key driver for the rubber hoses market. Every vehicle requires multiple hose assemblies for fuel, braking, and cooling systems. As manufacturers emphasize durability and extended service life, demand rises for hoses with better oil resistance and environmental stability, directly supporting market expansion.

- For instance, in January 2024, the Society of Indian Automobile Manufacturers (SIAM) stated that rising motorcycle production volumes continue to support demand for engine, fuel, and brake rubber hose components.

MARKET RESTRAINTS

Gradual Shift Toward Electrification Reduces Engine-Related Hose Usage

The slow transition toward electric two-wheelers reduces the number of engine-related rubber hose applications. Electric drivetrains eliminate fuel and cooling hoses, lowering overall hose content per vehicle. Although adoption is gradual, this shift may limit long-term volume growth for traditional rubber hoses, especially in premium urban segments.

- For instance, in May 2024, NITI Aayog reported that increasing electric two-wheeler adoption reduces demand for engine-related components, potentially limiting long-term growth for conventional rubber hose applications.

MARKET OPPORTUNITIES

Aftermarket Replacement Demand Creates Stable Revenue Streams

Rubber hoses are wear components with finite service life, creating steady aftermarket replacement demand. As vehicle parc expands, maintenance needs grow, especially in high-usage commuter motorcycles. Suppliers offering durable, affordable replacement hoses with proven ozone resistance can capture recurring revenue beyond OEM supply.

- For instance, in October 2023, Hero MotoCorp emphasized the importance of periodic replacement of rubber components during scheduled servicing, supporting steady aftermarket demand for hoses with extended service life.

MARKET CHALLENGES

Volatile Raw Material Prices to Hinder Industry Expansion

Natural and synthetic rubber price fluctuations create cost pressure for hose manufacturers. Managing margins becomes challenging when OEM pricing remains fixed. Smaller suppliers face difficulty absorbing cost volatility, impacting investment in quality improvements and long-term capacity expansion.

- For instance, in July 2023, Rubber Board India reported volatility in natural rubber prices, creating cost pressure for automotive hose manufacturers and impacting margin stability across the supply chain.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Motorcycles Dominate Due to Rising Rubber Hoses Demand

On the basis of vehicle type, the market is divided into motorcycles, scooters, mopeds, three wheelers, and tractors. Motorcycles dominate the market as they require more rubber hoses than scooters for fuel, cooling, and emission systems. Higher engine displacement and thermal loads increase demand for hoses with strong oil resistance and extended service life, supporting sustained volume growth.

- For instance, in February 2024, the Society of Indian Automobile Manufacturers (SIAM) stated that motorcycles continue to account for the majority of two-wheeler production volumes, supporting higher demand for engine and fuel rubber hose systems.

To know how our report can help streamline your business, Speak to Analyst

The three wheelers segment is expected to grow at a CAGR of 4.9% over the forecast period.

By Propulsion

ICE Segment Dominates due to Limited Electric Penetration

On the basis of propulsion, the market is segmented into ICE and Electric. ICE vehicles dominate as electric penetration remains limited in many regions. Combustion engines require multiple hose systems, ensuring steady demand for rubber tubing with strong ozone resistance and durability.

- For instance, in June 2024, the International Energy Agency stated that internal combustion engine two-wheelers continue is likely to dominate global fleets, sustaining demand for fuel, oil, and cooling rubber hoses.

The electric segment is expected to grow at a CAGR of 7.2% over the forecast period.

By Product Type

Tube Hose Assemblies Dominate Due to Improved Installation Efficiency

On the basis of product type, the market is segmented into fuel hose, breather hose, radiator hose, air intake hose, vacuum hose, tube hose/rubber tubing assemblies, silicone hose, oil cooler hose and other. Tube hose and rubber tubing assemblies dominate as OEMs prefer pre-assembled, tested solutions. These assemblies improve installation efficiency and reliability, increasing adoption across engine and braking systems.

- For instance, in September 2023, Bosch Mobility Solutions highlighted that OEMs increasingly prefer pre-assembled rubber hose units to improve installation accuracy, durability, and leakage prevention during two-wheeler assembly.

The silicone hose segment is expected to grow at a CAGR of 7.1% over the forecast period.

By Material Type

EPDM Rubber Leads Due to Its Superior Ozone Resistance

On the basis of material type, the market is segmented into EPDM Rubber, NBR (Nitrile Butadiene Rubber, Silicone, Neoprene, Thermoplastic Elastomers (TPE), FKM, PBT/PA12/PA66, and others (Natural Rubber and others). EPDM rubber dominates due to its superior ozone resistance, thermal stability, and longer service life. It performs reliably in harsh engine environments, making it a preferred choice for two-wheeler hoses.

- For instance, in April 2024, Continental AG stated that EPDM rubber remains widely used in automotive hoses due to its strong ozone resistance, heat stability, and extended service life.

The silicone segment is expected to grow at a CAGR of 7.6% over the forecast period.

By Application

Engine Systems Segment Dominates due to Growing Cooling Circuits Relying Heavily on Rubber Hoses

On the basis of application, the market is segmented into engine system, cooling system, air intake system, emission control system, brake system, and fuel delivery system. Engine systems dominate as fuel, oil, and cooling circuits rely heavily on rubber hoses. Continuous exposure to heat and fluids requires durable materials with strong oil resistance, which drives replacement and OEM demand.

- For instance, in August 2023, Bajaj Auto confirmed that engine systems require multiple rubber hoses for fuel, oil, and cooling circuits, making them the highest-volume application area.

The cooling system segment is expected to grow at a CAGR of 7.0% over the forecast period.

By Sales Channel

OEM Channel Dominates Through Standardized Supply Contracts

On the basis of sales channel, the market is segmented into OEM and aftermarket. OEMs dominate as hoses are integrated during vehicle assembly. Long-term supply agreements ensure consistent quality, volume stability, and compliance with vehicle specifications.

- For instance, in January 2024, TVS Motor Company stated that critical rubber components, such as hoses are sourced directly through OEM supply contracts to ensure quality consistency and regulatory compliance.

The OEM segment is expected to grow at a CAGR of 5.4% over the forecast period.

Two Wheeler Rubber Hoses and Tubing Market Regional Outlook

By geography, the two wheeler rubber hoses and tubing market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific Two Wheeler Rubber Hoses and Tubing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the two wheeler rubber hoses and tubing market due to its large two-wheeler production base and high commuter dependence. Countries such as India, China, Indonesia, and Vietnam rely heavily on motorcycles for daily mobility, driving consistent OEM demand for durable rubber hoses. The presence of large OEM manufacturing hubs and cost-efficient component suppliers further supports regional leadership. Strong aftermarket replacement demand also contributes to sustained market growth.

- For instance, Japanese and Chinese automakers are actively developing electronic steering systems to support next-generation vehicle platforms.

North America shows steady growth, driven by demand for recreational motorcycles and premium models. In the U.S., the market is supported mainly by aftermarket replacement rather than large-scale production. Longer vehicle ownership cycles and high maintenance awareness sustain demand for high-quality hoses with extended service life.

Europe’s market growth is moderate and quality-driven. Demand is supported by premium motorcycles and strict regulatory standards, encouraging the use of advanced rubber materials with strong ozone resistance and durability. OEMs focus on performance and safety supports steady hose demand.

Rest of the World markets, including Latin America and Africa, grow gradually due to rising urban mobility needs. Two-wheelers remain affordable transport options, sustaining demand for engine-related rubber hoses, particularly through the replacement aftermarket.

COMPETITIVE LANDSCAPE

Key Industry Players

Cost Efficiency, Material Innovation, and OEM Integration Drive Competition Among Key Players

The competitive landscape of the two wheeler rubber hoses and tubing market is moderately fragmented, with regional specialists and global suppliers competing on quality, cost, and long-term OEM relationships. Key players focus on product reliability, consistency, and compliance with automotive standards, as hose failure directly affects vehicle safety and performance.

Leading manufacturers invest in compound development to improve oil resistance, ozone resistance, and overall service life. Customization for specific OEM platforms is a critical differentiator, as two-wheeler manufacturers demand precise dimensional tolerances and durability under engine heat and vibration. Companies with strong testing and validation capabilities gain a competitive edge.

Cost optimization is another major strategy. Suppliers expand manufacturing in cost-efficient regions while maintaining quality controls. Backward integration into rubber compounding and tooling helps reduce dependency risks and improve margins. Aftermarket branding and distribution networks also support revenue diversification.

Partnerships with OEMs during vehicle development cycles help suppliers secure long-term supply contracts. Players that can scale production quickly while maintaining consistent performance standards remain preferred partners.

- For instance, in 2024, Endurance Technologies highlighted continuous investment in rubber hose technology to meet OEM durability and emission compliance requirements for two-wheelers.

LIST OF KEY Two Wheeler Rubber Hoses and Tubing COMPANIES PROFILED

- Endurance Technologies (India)

- Jayashree Polymers (India)

- Imperial Auto Industries (India)

- Polyrub Extrusions (India)

- Gates Corporation (U.S.)

- Continental AG (Germany)

- Hutchinson SA (France)

- Toyoda Gosei (Japan)

- Sumitomo Riko (Japan)

- Yokohama Rubber (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Endurance Technologies announced capacity expansion at its Chakan facility to support rising OEM demand for rubber hoses and fluid transfer components used in two-wheelers.

- January 2025: Continental highlighted increased adoption of advanced elastomer compounds in motorcycle hoses to improve heat resistance, ozone resistance, and long-term performance.

- November 2024: Imperial Auto announced upgrades to its rubber hose manufacturing lines to meet growing two-wheeler OEM requirements for emission-compliant and high-durability hose systems.

- September 2024: Jayashree Polymers expanded its two-wheeler rubber tubing capacity, targeting increased supply to domestic motorcycle OEMs and replacement markets.

- March 2024: TVS Motor Company reiterated its focus on localized sourcing of rubber components to ensure supply stability and quality consistency for two-wheeler production.

REPORT COVERAGE

The two wheeler rubber hoses and tubing market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Propulsion, Product Type, Material Type, Application, Sales Channel, and Region |

|

By Vehicle Type |

· Motorcycles · Scooters · Mopeds · Three Wheelers · Tractors |

|

By Propulsion |

· ICE · Electric |

|

By Product Type |

· Fuel Hose · Breather Hose · Radiator Hose · Air Intake Hose · Vacuum Hose · Tube Hose / Rubber Tubing Assemblies · Silicone Hose · Oil Cooler Hose · Other |

|

By Material Type |

· EPDM Rubber · NBR (Nitrile Butadiene Rubber) · Silicone · Neoprene · Thermoplastic Elastomers (TPE) · FKM · PBT/PA12/PA66 · Others (Natural Rubber and others) |

|

By Application |

· Engine System · Cooling System · Air Intake System · Emission Control System · Brake System |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Geography |

· North America (By Vehicle Type, Propulsion, Product Type, Material Type, Application, Sales Channel, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Propulsion, Product Type, Material Type, Application, Sales Channel, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Propulsion, Product Type, Material Type, Application, Sales Channel, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, Propulsion, Product Type, Material Type, Application, Sales Channel, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.62 billion in 2025 and is projected to reach USD 5.42 billion by 2034.

In 2025, the market value stood at USD 1.36 billion.

The market is expected to exhibit a CAGR of 4.7% during the forecast period (2026-2034).

The ICE segment leads the market by propulsion.

Rising two-wheeler production is the key factor driving the market.

Endurance Technologies, Polyrub Extrusions, Gates Corporation, and Continental AG are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us