Ultra-Fast EV Charging Systems Market Size, Share & Industry Analysis, By Power Output Level (150 kW–249 kW, 250 kW–349 kW, and 350 kW & Above), By Charging Infrastructure Type (Highway/Corridor Charging Stations, Urban Public Charging Hubs, Commercial Fleet Depots, and Bus & Truck Dedicated Charging Stations), By Vehicle Type Supported (Passenger Cars, Light Commercial Vehicles (LCVs), Medium & Heavy Commercial Vehicles (M&HCVs), and Electric Buses), By Connector Standard (CCS (CCS1 & CCS2), NACS, CHAdeMO, and GB/T), and Regional Forecast, 2026–2034

Ultra-Fast EV Charging Systems Market Size and Future Outlook

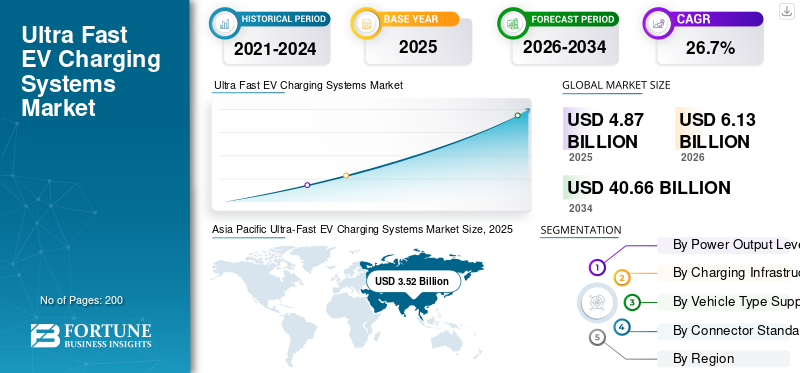

The global ultra-fast EV charging systems market size was valued at USD 4.87 billion in 2025. The market is projected to grow from USD 6.13 billion in 2026 to USD 40.66 billion by 2034, exhibiting a CAGR of 26.7% during the forecast period. Asia Pacific dominated the ultra fast ev charging systems market with a market share of 72.28% in 2025.

Ultra-Fast EV charging systems are high-power electric vehicle charging solutions typically delivering 150 kW to 350 kW & above, enabling rapid battery replenishment within 10-20 minutes for long-range electric mobility applications. Market growth is driven by technological advancements, supportive regulations, infrastructure investments, consumer adoption, cost reductions, and expanding industry applications across regions.

Major players in the market include ABB, Siemens, Tesla, Tritium, Alpitronic, and Delta Electronics, competing through high-power charging technology, grid integration capabilities, ultra-fast charging reliability, digital energy management, and strategic infrastructure partnerships.

Download Free sample to learn more about this report.

ULTRA-FAST EV CHARGING SYSTEMS MARKET TRENDS

Expansion of Highway and Corridor Charging Networks Emerging as a Key Market Trend

Governments and private operators are prioritizing the development of high-power charging corridors along highways and intercity routes. This market trend reflects the need to support long-distance electric mobility and commercial fleet electrification. Charging hubs are being designed with multi-megawatt grid connections, energy storage integration, and smart load balancing capabilities. Such infrastructure development and modernization enhance utilization rates and strengthen competitive positioning among operators, contributing positively to overall market analysis during the forecast period.

- In February 2026, Tesla updated its Find Us map to include 64 additional Megacharger sites across 15 U.S. states, expanding its heavy-duty EV charging networks for the Tesla Semi with 1.2 MW DC fast charging capable of replenishing up to 400 miles in 30 minutes along major freight corridors.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising High-Power EV Adoption to Accelerate Ultra-Fast Charging Deployment

The rapid increase in long-range electric vehicles equipped with high-capacity battery packs is significantly driving demand for ultra-fast EV charging systems. Automakers are introducing 800V architectures and higher C-rate battery chemistries that support 250 kW to 350 kW charging, reducing range anxiety and improving user convenience. This shift is strengthening the overall ultra-fast EV charging systems market growth as consumers increasingly expect refueling times comparable to internal combustion vehicles. Expanding EV sales across passenger and commercial segments continues to stimulate sustained ultra-fast EV charging system demand globally.

MARKET RESTRAINTS

High Infrastructure and Grid Upgrade Costs Limiting Rapid Deployment

The installation of ultra-fast EV charging systems in the EV charging market requires substantial capital investment in grid upgrades, transformers, cooling systems, and power electronics. Securing high-capacity grid connections can be time-consuming and expensive, particularly in urban or grid-constrained areas. These financial and logistical barriers may slow deployment in certain regions, especially in developing markets. While long-term prospects remain strong, upfront infrastructure costs continue to restrain broader penetration and impact short-term market share expansion for smaller operators.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Energy Storage Creating Growth Opportunities

The integration of solar, wind, and battery energy storage systems with ultra-fast EV charging stations presents significant opportunities for innovation. Operators are increasingly deploying on-site storage to manage peak loads, reduce electricity costs, and enhance grid stability. This approach supports sustainability goals while improving charging reliability and operational efficiency. As energy transition policies strengthen globally, renewable-powered charging hubs are expected to unlock new revenue streams and reinforce long-term market growth potential.

- In February 2026, Allye Energy launched a higher-capacity EV battery-powered energy storage system featuring advanced lithium-ion cells designed for grid support, renewable integration, and enhanced peak load management, improving charging station uptime and reducing operational costs.

MARKET CHALLENGES

Managing Grid Stability and Peak Load Balancing as a Critical Industry Challenge

Ultra-fast charging systems demand extremely high-power levels, often exceeding 350 kW per vehicle, creating stress on local distribution networks. Simultaneous charging events can generate peak load spikes that challenge grid stability and increase operational costs. Utilities and charging operators must implement smart energy management systems, dynamic pricing, and load balancing technologies to maintain efficiency. Addressing these technical complexities remains a significant challenge, influencing deployment strategies across the global market.

Segmentation Analysis

By Power Output Level

Expanding Highway Electrification to Strengthen 150 kW–249 kW Segment Leadership

Based on power output level, the market is segmented into 150 kW–249 kW, 250 kW–349 kW, and 350 kW & above.

The 150 kW–249 kW segment dominates the market due to its wide deployment across existing public charging corridors and urban fast-charging hubs. This power range balances cost efficiency, grid compatibility, and faster charging capability, making it suitable for most current-generation EVs. Strong installed base expansion and retrofit projects continue to reinforce its leading market share globally.

- In November 2025, bp pulse opened a new 40-stall EV fast charging hub near Houston’s William P. Hobby Airport, featuring 150 kW DC fast chargers, covered canopies, and free Wi-Fi, expanding its U.S. public infrastructure footprint and supporting ride-hail, rental fleets, and local EV drivers.

The 350 kW & above segment is expected to grow at a CAGR of 30.1% during the forecast period. Rising adoption of 800V EV platforms, premium electric vehicles, and long-haul electric trucks is accelerating demand for ultra-high-power charging infrastructure globally.

By Vehicle Type Supported

Mass EV Adoption and Urban Charging Expansion to Cement Passenger Car Segment Dominance

Based on vehicle type supported, the market is segmented into passenger cars, light commercial vehicles (LCVs), medium & heavy commercial vehicles (M&HCVs), and electric buses.

The passenger cars segment holds the largest market share due to accelerating EV adoption, expanding urban charging infrastructure, and strong policy incentives supporting personal mobility electrification. High sales volumes of battery electric sedans and SUVs, coupled with rising consumer preference for reduced charging time, continue driving large-scale deployment of ultra-fast charging systems across metropolitan and highway networks.

- According to the IEA Global EV Outlook 2025, worldwide electric car sales are expected to surpass 20 million units in 2025, accounting for over 25% of total new vehicle sales globally.

The medium & heavy commercial vehicles M&HCVs segment is projected to grow at a CAGR of 30.2% during the forecast period. Rapid electrification of long-haul freight, regulatory emission mandates, and fleet decarbonization targets are significantly accelerating demand for high-capacity ultra-fast charging infrastructure tailored to heavy-duty vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Charging Infrastructure Type

Intercity Travel Electrification to Drive Highway/Corridor Charging Stations’ Dominance

Based on charging infrastructure type, the market is segmented into highway/corridor charging stations, urban public charging hubs, commercial fleet depots, and bus & truck dedicated charging stations.

Highway/corridor charging stations hold the largest share in the market. The growth is due to their critical role in enabling long-distance electric mobility. Governments and private operators prioritize high-power installations along expressways to reduce range anxiety and support intercity travel. High utilization rates, strategic locations, and multi-vehicle charging capacity continue to strengthen their leading market position globally.

- In January 2025, bp pulse opened its first EV charging hub at a TravelCenters of America site in Jacksonville, Florida, featuring 12 ultra-fast 400 kW DC chargers along the I-95 corridor with driver amenities, and plans to roll out at least 40 similar hubs nationally.

The bus & truck dedicated charging stations segment is projected to grow at a CAGR of 30.3% during the forecast period. Accelerating electrification of public transport and heavy-duty freight fleets is driving demand for high-capacity, depot-based ultra-fast charging solutions.

By Connector Standard

Strong Domestic EV Ecosystem and Policy Support to Sustain GB/T Segment Dominance

Based on the connector standard, the market is segmented into CCS (CCS1 & CCS2), NACS, CHAdeMO, and GB/T.

The GB/T segment dominates the market share due to its extensive deployment across China. Strong government standardization policies, widespread public charging infrastructure, and high domestic EV production volumes reinforce GB/T widespread adoption. Integrated ecosystem alignment between automakers and charging operators continues to support sustained installation growth across urban and highway networks.

The CCS (CCS1 & CCS2) segment is projected to grow at a CAGR of 28.4% during the forecast period. Expanding cross-border infrastructure harmonization, increasing 800V EV adoption, and a regulatory push for standardized fast charging station networks across Europe and North America are accelerating CCS deployment globally.

- In December 2024, CHARGE opened South Africa’s first off-grid EV charging station in Wolmaransstad, featuring six 200 kW CCS-standard DC ultra-fast chargers, 480 bifacial solar panels, a 546-kWh liquid-cooled battery, and a 250 kVA renewable generator, enabling 80% charge in 20 minutes while operating independent of the grid.

Ultra-Fast EV Charging Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Ultra-Fast EV Charging Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest ultra-fast EV charging systems market share, driven primarily by China’s large-scale EV adoption and aggressive public charging deployment. Strong government initiatives and subsidies, domestic manufacturing strength, and grid expansion programs continue to accelerate market growth. Japan and South Korea further contribute through advanced battery technologies and high-power charging innovation. Rapid urbanization, highway electrification corridors, and policy-backed infrastructure investments collectively sustain strong product demand across the region.

- In February 2026, Huawei and SP Mobility deployed Singapore’s first battery-buffered ultra-fast EV charging station at Temasek Polytechnic, integrating a 480-kW liquid-cooled DC charger with battery energy storage to add up to 200 km range in 5 minutes while reducing grid strain and enabling high-power charging where local infrastructure is limited.

China Ultra-Fast EV Charging Systems Market

The China market in 2026 is estimated at around USD 3.44 billion, accounting for roughly 56.1% of global revenues. Dominance is driven by large-scale EV adoption, strong state-backed infrastructure expansion, domestic charger manufacturing leadership, and extensive highway corridor electrification investments.

Japan Ultra-Fast EV Charging Systems Market

The Japan market in 2026 is estimated at around USD 0.29 billion, accounting for roughly 4.8% of global revenues. Advanced battery innovation, urban fast-charging upgrades, government decarbonization policies, and rising deployment of high-power chargers along expressways support growth.

India Ultra-Fast EV Charging Systems Market

The India market in 2026 is estimated at around USD 0.25 billion, accounting for roughly 4.1% of global revenues. Rapid growth is fueled by government incentives, expanding EV manufacturing, urban charging infrastructure programs, and increasing private sector investment.

Europe

Europe represents the second-largest market, supported by stringent emission regulations, cross-border charging harmonization, and strong EV penetration rates. The European Union’s Alternative Fuels Infrastructure Regulation (AFIR) is accelerating high-power charging installations along major transport corridors. Countries such as Germany, France, and the Netherlands are expanding 350 kW networks to support long-range mobility. Strong public-private partnerships and renewable energy integration continue to reinforce steady market growth during the forecast period.

- In February 2026, Delta introduced a 350 kW ultra-fast EV charger designed for Europe, featuring liquid-cooled cable tech, modular architecture, and integrated payment systems that support CCS charging standards, rapid thermal management, and easy installation, enhancing charging network scalability across urban and highway locations.

Germany Ultra-Fast EV Charging Systems Market

The Germany market in 2026 is estimated at around USD 0.30 billion, accounting for roughly 4.9% of global revenues. Growth is driven by strong EV penetration, industrial electrification initiatives, highway corridor expansion, and compliance with EU charging infrastructure regulations.

U.K. Ultra-Fast EV Charging Systems Market

The U.K. market in 2026 is estimated at around USD 0.23 billion, accounting for roughly 3.8% of global revenues. Net-zero commitments, rapid public charger deployment, urban mobility electrification, and government-backed funding schemes support market expansion.

North America

North America ranks as the third-largest market, driven by federal funding programs, expanding highway charging corridors, and rising adoption of long-range electric SUVs and pickup trucks. The U.S. National Electric Vehicle Infrastructure (NEVI) program is supporting large-scale ultra-fast charger installations nationwide. Private investments by automotive OEMs and charging network operators further strengthen infrastructure density. Increasing fleet electrification initiatives also contribute to sustained regional market demand.

- In January 2026, Eaton and ChargePoint partnered to launch Express Grid fast-charging solutions that use smart load management and bidirectional power controls to reduce grid upgrade costs, optimize peak load, and enable more than 150 kW and above DC fast chargers with enhanced reliability and lower infrastructure expenses.

U.S. Ultra-Fast EV Charging Systems Market

The U.S. market in 2026 is estimated at around USD 0.23 billion, accounting for roughly 3.7% of global revenues. Growth is accelerated by federal infrastructure funding, rising electric SUV adoption, private network expansion, and strategic highway fast-charging corridor development.

Rest of the World

The Rest of the World region is projected to grow at a CAGR of 32.6% during the forecast period. Emerging economies in the Middle East, Latin America, and parts of Southeast Asia are investing in next-generation charging corridors and smart city mobility projects. Government diversification strategies, rising EV imports, and infrastructure modernization are accelerating ultra-fast charging deployment. Lower base penetration combined with strategic foreign investments is driving rapid percentage-based market growth.

- In February 2026, the UAE opened one of the world’s largest ultra-fast EV charging hubs in Dubai, featuring multiple 350 kW and above DC fast chargers, integrated solar canopies, and advanced energy storage to support simultaneous high-power charging and enhance regional EV infrastructure capacity.

COMPETITIVE LANDSCAPE

Key Industry Players

High-Power Technology Innovation and Strategic Partnerships Intensify Competitive Positioning

The ultra-fast EV charging systems market is shaped with a mix of global power electronics leaders and specialized charging infrastructure providers competing on technology, reliability, and network scalability. Key players such as ABB, Siemens, Tesla, Tritium, Alpitronic, and Delta Electronics focus on high-power charging platforms, grid integration, and digital energy management systems. Companies strengthen market share through strategic partnerships with utilities, OEM collaborations, and corridor-based expansion projects. Investments in liquid-cooled cables, megawatt charging systems, and software-driven load optimization enhance differentiation. Mergers, localized manufacturing, and long-term service agreements further reinforce competitive intensity across regions.

LIST OF KEY ULTRA-FAST EV CHARGING SYSTEM COMPANIES PROFILED

- ABB E-mobility (Switzerland)

- Siemens AG (Siemens eMobility) (Germany)

- Tesla, Inc. (U.S.)

- Tritium DCFC Limited (Australia)

- Alpitronic GmbH (Italy)

- Delta Electronics, Inc. (Taiwan)

- Schneider Electric SE (France)

- EVBox (Liberty Global subsidiary) (Netherlands)

- ChargePoint Holdings, Inc. (U.S.)

- Blink Charging Co. (U.S.)

- Wallbox N.V. (Spain)

- Star Charge (Wanbang Digital Energy Co., Ltd.) (China)

- BTC Power (U.S.)

- SK Signet Inc. (South Korea)

- Heliox Energy B.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- February 2026: BYD reportedly began rolling out its megawatt flash charging network in China, accelerating deployment of ultra-high-power charging infrastructure to support next-generation EVs.

- February 2026: BYD began large-scale deployment of 1,360 kW liquid-cooled flash chargers across China, featuring ultra-high-power DC outputs, advanced cooling, and high current delivery to charge next-gen EVs faster while reducing heat-related losses and infrastructure strain.

- February 2026: ACCIONA secured a contract to build a 4,000 kW EV charging hub in Madrid featuring 20 ultra-fast charging points (400 kW each) and renewable energy integration for public and heavy-duty vehicles.

- February 2026: BYD began large-scale deployment of megawatt-flash charging facilities in China, using 1 MW ultra-fast chargers with 1,000 V/1,000 A capability to reduce cable drag and support rapid expansion of high-power infrastructure.

- January 2026: Delta unveiled a 350-kW high-power DC ultra-fast EV charger for the Europe, the Middle East & Africa market with intelligent load management, backend connectivity, dynamic power distribution, and grid-constraint flexibility tailored for passenger cars, buses, and trucks.

- December 2025: Creek Power and Virta launched fast charging for heavy-duty EVs in Stockholm with optimized high-power DC chargers designed to support commercial vehicle fleets.

- September 2025: Mercedes-Benz and Alpitronic launched 600 kW ultra-fast DC chargers (HYC1000) capable of delivering up to 600 kW per point with modular power units and intelligent distribution across sites.

REPORT COVERAGE

The global ultra-fast EV charging systems market analysis provides an in-depth study of the market size & forecast by all the market segments included in the vehicle security components market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 26.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Power Output Level, By Vehicle Type Supported, By Charging Infrastructure Type, By Connector Standard, and By Region |

| By Power Output Level |

|

| By Vehicle Type Supported |

|

| By Charging Infrastructure Type |

|

| By Connector Standard |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.87 billion in 2025 and is projected to reach USD 40.66 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 3.52 billion.

The market is expected to exhibit a CAGR of 26.7% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type supported.

Rising high-power EV adoption to accelerate ultra-fast charging deployment.

Major players in the market include ABB, Siemens, Tesla, Tritium, Alpitronic, and Delta Electronics.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us