Vacuum Evaporators Market Size, Share & Industry Analysis, By Product Type (Rotary Vacuum Evaporators, Centrifugal Vacuum Evaporators, and Others), By Application (Laboratory, Wastewater Treatment, Product Processing, and Others), By End User (Pharmaceuticals, Electronics & Semiconductor, Chemical & Petrochemical, Food & Beverages, Energy & Power, and Others), and Regional Forecast, 2026-2034

Vacuum Evaporators Market Size and Future Outlook

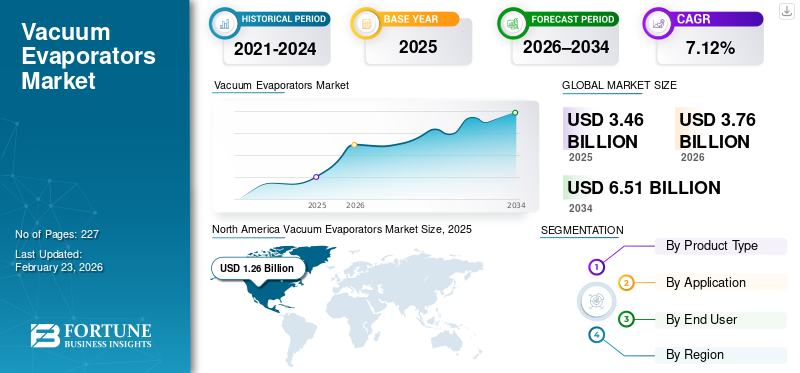

The global vacuum evaporators market size was valued at USD 3.46 billion in 2025. The market is projected to grow from USD 3.76 billion in 2026 to USD 6.51 billion by 2034, with a CAGR of 7.12% over the forecast period. North America dominated the vacuum evaporators market with a market share of 36.42% in 2025.

Vacuum evaporators are thermal separation systems that remove water or other solvents from liquids by operating under reduced pressure, which lowers the boiling point of the liquid. This allows evaporation to occur at lower temperatures, making the process energy-efficient and suitable for heat-sensitive materials. They are widely used for concentrating solutions, recovering solvents, and reducing wastewater volume. Vacuum evaporators are applied across laboratory, industrial processing, and wastewater treatment applications. Common configurations include rotary, centrifugal, and multi-effect or mechanical vapor recompression (MVR) systems, depending on capacity and efficiency requirements.

The growth of the market is primarily driven by increasing environmental regulations related to industrial wastewater discharge and the rising adoption of zero liquid discharge (ZLD) systems. Growing water scarcity and the need for water reuse across industries such as chemicals, power, and pharmaceuticals are further accelerating demand. The expansion of chemical, food & beverage, and pharmaceutical processing industries is increasing the need for efficient concentration and solvent recovery solutions. Technological advancements such as energy-efficient MVR and multi-effect evaporators are improving operating economics and adoption. Additionally, the rising emphasis on sustainable manufacturing and cost reduction through waste minimization continues to support market growth.

Veolia Water Technologies, GEA Group, Alfa Laval, SUEZ Water Technologies & Solutions, and Condorchem Enviro Solutions are among the key participants shaping the global vacuum evaporators market. Veolia Water Technologies plays a strategic leadership role in the market by driving large-scale adoption of vacuum evaporators in industrial wastewater treatment technologies and zero liquid discharge (ZLD) projects. The company integrates vacuum evaporation systems into turnkey water and effluent management solutions, particularly for chemicals, power generation, and heavy industries. Its role is critical in commercializing advanced evaporation technologies, scaling high-capacity systems, and setting performance benchmarks related to energy efficiency, reliability, and regulatory compliance.

Download Free sample to learn more about this report.

Vacuum Evaporators Market Trends

Shift toward Energy-Efficient and Automated Systems to Drive Market Growth

A major trend shaping the market is the shift toward energy-efficient and automated systems, particularly through the adoption of Mechanical Vapor Recompression (MVR) and heat pump technologies. The growing industry preference to lower operating costs and reduced carbon emissions have led to the shift toward MVR technology, which recycles vapor energy to reduce overall power consumption. This trend responds to rising industrial energy costs and sustainability goals, as manufacturers seek to cut both environmental impact and ongoing utility expenses. Automated control systems and IoT-enabled monitoring are also gaining traction, allowing predictive maintenance and improved process optimization. For example, smart evaporators with cloud-based monitoring platforms help reduce unplanned downtime and enhance reliability in industrial wastewater applications. Across regions, energy-efficient designs and modular configurations are increasingly integrated into new installations and retrofits. These developments signal a broader market shift toward sustainable, low-energy, high-performance evaporation systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Stringent Environmental Regulations and Growing Adoption of Zero-Liquid-Discharge (ZLD) Mandates to Push the Market Expansion

A primary driver of the vacuum evaporators market growth is stringent environmental regulations and the growing adoption of zero-liquid-discharge (ZLD) mandates across major industrial regions. Governments and regulators in North America, Europe, and Asia Pacific are tightening effluent discharge limits, compelling industries such as chemicals, pharmaceuticals, and food processing to install advanced treatment systems. ZLD regulations reduce liquid waste release and promote internal water reuse, making vacuum evaporators central to industrial wastewater strategies. In Switzerland, a chemical manufacturer achieved over 95% wastewater recovery by deploying vacuum evaporators, avoiding regulatory penalties and significantly reducing freshwater intake. Similarly, EPA mandates in the U.S. and the EU Industrial Emissions Directive are major drivers pushing large and mid-sized facilities to integrate vacuum evaporation into their treatment infrastructure, fueling market growth.

Market Restraints

High Capital and Operational Costs to Limit the Market Expansion

A key restraint on the vacuum evaporators market is the high capital and operational costs associated with acquiring, installing, and maintaining these systems, which can limit adoption among small and medium enterprises (SMEs). Vacuum evaporators, particularly large multi-effect or MVR units, involve significant upfront investment due to expensive components such as high-grade pumps, corrosion-resistant heat exchangers, and precision controls. Many stakeholders globally (around 40%) cite these costs as a major barrier, especially in cost-sensitive industries or emerging economies where financing options are limited. Moreover, ongoing operational costs, including energy consumption, routine maintenance, and fouling management, add to the total cost of ownership, discouraging some potential buyers. In developing regions such as parts of Latin America and Africa, the lack of accessible financing and the high initial expenditure often lead facilities to choose cheaper, lower-efficiency alternatives despite long-term benefits, thereby constraining market expansion.

Market Opportunities

Expansion of Product Processing Applications Beyond Wastewater Treatment to Create New Growth Avenues

An important opportunity in the vacuum evaporators market lies in the expansion of product processing applications beyond wastewater treatment, notably in pharmaceuticals, food & beverage processing, and specialty chemical concentration. While wastewater treatment remains the largest segment, other industrial uses are gaining share as manufacturers seek efficient ways to concentrate product streams and recover valuable materials. Data show that, besides wastewater, product processing applications hold a significant share of installations, reflecting the growing demand for operations such as juice concentration, dairy processing, flavor extraction, and API (active pharmaceutical ingredient) concentration at low temperatures. This trend is particularly strong in Asia Pacific, where rapid industrial growth and investment in manufacturing are driving adoption, and in developed markets focused on high-value processing. Advanced materials and design innovations, such as hybrid evaporator systems and stainless-steel construction, further support the expanded use and demand for effective wastewater treatment. Increasing urbanization and food safety standards also boost investment in compact, energy-efficient processing evaporators across sectors.

Market Challenges

Technical Complexity of Operation and the Associated Skill Gap to Limit Market Growth

A significant challenge confronting the vacuum evaporators market is the technical complexity of operation and the associated skill gap, which affects both adoption and long-term performance. Vacuum evaporator systems require the precise control of vacuum levels, temperature, and phase separation, with specialized calibration that demands trained technicians familiar with thermodynamics, fluid mechanics, and integrated control systems. This complexity is particularly pronounced in industrial settings handling highly variable and complex wastewater streams that differ widely in chemical composition and solid content. Scaling, fouling, and corrosion can further degrade heat transfer efficiency and increase maintenance requirements, reducing system uptime and increasing costs. In many regions, especially emerging markets, the shortage of skilled labor and limited technical support infrastructure lead to operational inefficiencies, extended downtimes, and higher lifecycle costs. Continuous innovation and workforce training are essential to mitigate this challenge and ensure reliable operation in diverse industrial environments.

Segmentation Analysis

By Product Type

Large Requirement in Industrial Application to Push Centrifugal Vacuum Evaporators Segment Growth

Based on product type, the market is segmented into rotary vacuum evaporators, centrifugal vacuum evaporators, and others.

The centrifugal vacuum evaporators segment accounts for approximately 65.52% of the market share. The segment represents a dominant share of the market, largely driven by industrial-scale applications such as solvent recovery, chemical processing, and selective concentration processes. These systems are preferred where enhanced separation efficiency and higher throughput are required, particularly in continuous or semi-continuous operations. Compared to rotary systems, centrifugal evaporators typically have higher average selling prices but are deployed in lower volumes, resulting in a moderate overall share. Their adoption is the strongest in chemical, food processing, and specialty manufacturing industries.

The rotary vacuum evaporators segment is expected to grow at a CAGR of 8.02% during the forecast period.

By Application

Heavy Demand in the Industrial Sector to Reduce Liquid Waste Volumes to Fuel the Wastewater Treatment Segment Growth

Based on application, the market is segmented into laboratory, wastewater treatment, product processing, and others.

The wastewater treatment segment accounted for a leading vacuum evaporators market share of 47.84% in 2025. This reflects the broad industrial need to reduce liquid waste volumes, meet discharge regulations, and implement zero liquid discharge (ZLD) solutions. Vacuum evaporators in this domain often form part of large, integrated wastewater treatment systems that may include crystallizers, multi-effect stages, and energy recovery components. These installations have high average selling prices, are frequently customized, and are more expensive than basic laboratory or processing units.

The product processing segment is expected to grow at a CAGR of 7.29% during the forecast period of 2026-2034.

To know how our report can help streamline your business, Speak to Analyst

By End User

Stringent Environmental Regulations to Propel the Electronics & Semiconductor Segment Growth

Based on end user, the market is segmented into pharmaceuticals, electronics & semiconductor, chemical & petrochemical, food & beverages, energy & power, and others.

The electronics & semiconductor segment represents the largest share of the market and accounted for approximately 34.23% share in 2025. The segment encompasses vacuum evaporator applications for ultrapure process wastewater treatment, solvent recovery, and chemical processing in semiconductor fabs and electronics manufacturing. These facilities have stringent purity requirements and often integrate vacuum evaporation with advanced water-treatment trains. While total unit counts are lower relative to larger industrial sectors, the equipment value per unit is relatively high due to technical specifications.

The pharmaceuticals segment was the second leading segment with a share of 24.51% in 2025.

Vacuum Evaporators Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Vacuum Evaporators Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 1.26 billion in 2025, accounting for approximately 36.43% of the global vacuum evaporators market. The region’s dominance stems from an advanced industrial base that includes chemicals, pharmaceuticals, food & beverage, and energy sectors, all of which are major consumers of evaporation technologies. Regulatory frameworks such as stringent effluent discharge limits and corporate sustainability commitments have accelerated the adoption of vacuum evaporators in industrial wastewater treatment and zero liquid discharge (ZLD) systems. For example, several large petrochemical and power plants in Texas and the U.S. Midwest have installed multi-effect and mechanical vapor recompression (MVR) vacuum evaporators to meet state environmental mandates. Meanwhile, the pharmaceutical industry’s concentrated R&D activity in states such as New Jersey and California continues to drive laboratory and pilot-scale vacuum evaporator sales. These factors combine to make North America one of the largest and most mature markets globally.

U.S. Vacuum Evaporators Market

The U.S. market was valued at USD 1.09 billion in 2025 and is estimated to touch USD 1.17 billion in 2026. This dominance is driven by a deep industrial base in chemicals, pharmaceuticals, food & beverage processing, and energy infrastructure that routinely employs vacuum evaporation for concentration, solvent recovery, and wastewater reduction. Strong environmental regulations at federal and state levels, particularly requirements for industrial wastewater discharge limits, accelerate the adoption of advanced vacuum systems, including multi-effect and mechanical vapor recompression (MVR) technologies. Laboratories and research institutions also contribute a high unit demand for rotary vacuum evaporators.

Europe

Europe accounted for USD 0.76 billion in 2025, representing approximately 21.89% of global revenues. Europe maintains a robust demand for vacuum evaporators, supported by a strong manufacturing ecosystem and progressive environmental regulation. The European Union directives on water reuse and industrial discharge have compelled chemical, food processing, and energy companies across Germany, France, and the Netherlands to adopt advanced evaporative technologies. For instance, major chemical clusters along the Rhine have integrated high-efficiency vacuum evaporation systems into wastewater treatment trains to reduce effluent volumes and achieve internal reuse targets. Additionally, Europe’s leadership in sustainability has incentivized investment in energy-efficient configurations such as MVR and multi-effect evaporators, enhancing overall demand. The prevalence of retrofit projects in aging European plants also strengthens the mid-to-long-term market pipeline. Collectively, these drivers place Europe among the top regional contributors to both equipment sales and integrated service contracts in the vacuum evaporators market.

Germany Vacuum Evaporators Market

The Germany market reached a value of USD 0.19 billion in 2025 and is estimated to touch USD 0.21 billion in 2026. Germany is a key European market with strong manufacturing and regulatory drivers supporting vacuum evaporator adoption. Its chemical, pharmaceutical, and food processing sectors are highly developed and stringent EU wastewater discharge standards drive investments in energy-efficient wastewater treatment solutions that often include vacuum evaporation. German industrial firms also retrofit aging plants with modern evaporative systems to meet tighter water reuse mandates. Automation and precision manufacturing further increase average selling prices in this market.

U.K. Vacuum Evaporators Market

The U.K. market was valued at USD 0.11 billion in 2025 and is poised to reach USD 0.12 billion in 2026. The U.K. represents a moderate but influential share of the European market. The chemical, pharmaceutical, and food industries in the U.K. are major users of concentrated processing technologies and environmental regulations tied to EU legacy standards and domestic policy continue to push the adoption of wastewater reduction systems. Investments in advanced thermal separation, including MVR and multi-effect units, is particularly notable in larger industrial complexes.

Asia Pacific

The Asia Pacific vacuum evaporators market was valued at USD 1.05 billion in 2025, accounting for approximately 30.43% of global revenues. Rapid industrialization in China, India, the Southeast Asia, and South Korea is expanding the product demand across chemicals, pharmaceuticals, textiles, and food & beverage sectors, where evaporation technologies are essential for concentration, solvent recovery, and wastewater volume reduction. In China’s industrial hubs, a wave of new manufacturing capacity has led to the increased installation of large, high-capacity vacuum evaporation and ZLD systems. An instance of the same is expanded chemical parks in Jiangsu Province. Environmental reform and water scarcity concerns in India’s industrial belts, such as Gujarat and Maharashtra, are also driving the uptake of wastewater-focused vacuum evaporators. This robust combination of economic growth, regulatory drivers, and rising technology adoption positions the Asia Pacific as a key growth engine in the global market.

China Vacuum Evaporators Market

China remains the dominant contributor in Asia Pacific. The region reached a value of USD 0.47 billion in 2025 and is estimated to hit a valuation of USD 0.52 billion in 2026. Rapid industrial expansion in chemicals, pharmaceuticals, textiles, food processing, and energy sectors generates massive demand for concentration, solvent recovery, and industrial wastewater management systems. Central and provincial environmental regulations, aimed at reducing industrial effluents and promoting water reuse, have driven widespread deployment of vacuum evaporation technologies, particularly large multi-effect and MVR systems in zero liquid discharge (ZLD) applications. China also leads in retrofit projects as older facilities modernize.

India Vacuum Evaporators Market

The India market touched a value of USD 0.20 billion in 2025 and is estimated to reach USD 0.21 billion in 2026, driven by increasing industrial activity in chemicals, textiles, pharmaceuticals, and food & beverage sectors. Water scarcity concerns and stricter enforcement of effluent discharge norms in states such as Maharashtra, Gujarat, and Tamil Nadu are prompting investments in wastewater reduction and reuse technologies, including vacuum evaporation. While overall market revenue per unit tends to be lower than in developed countries due to cost sensitivity, the high volume of facilities adopting modernization strategies generates substantial demand. Thus, India’s market share is prominent within South Asia and is expected to grow faster than many mature markets.

Japan Vacuum Evaporators Market

The Japan market was valued at USD 0.14 billion in 2025 and is set to reach USD 0.15 billion in 2026. Japan’s advanced manufacturing and process industries make it an important national market for vacuum evaporators, with strong participation in chemicals, semiconductors, pharmaceuticals, and precision engineering firms. Japanese companies emphasize high-efficiency, low-energy systems and often implement vacuum evaporation as part of broader sustainability and resource reuse initiatives. The country’s established industrial automation and quality control environments also support steady demand for laboratory and pilot vacuum evaporators. Japan’s share is significant within Asia Pacific, though it is generally smaller than China’s due to China’s larger industrial expansion.

Latin America

The Latin America market accounted for USD 0.22 billion in 2025, accounting for approximately 6.22% of global revenues. The industrial demand is concentrated in regions with significant agro-industry, food processing, mining, and chemical sectors, such as Brazil, Argentina, and Chile. In the mining sector, especially in Chile’s copper operations, vacuum evaporators are part of water reuse and effluent management strategies in water-stressed environments. Brazil’s large food processing industry also supports mid-range evaporator demand for product concentration. However, broader market growth in Latin America is impacted by slower capital investment cycles and financing constraints for advanced treatment systems in smaller enterprises. Nonetheless, recent infrastructure initiatives in urban wastewater management and tightening regional environmental standards are incrementally boosting market activity, suggesting steady growth potential from a modest base.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.17 billion in 2025. Countries in the Gulf Cooperation Council (GCC), including Saudi Arabia, the UAE, and Qatar, invest heavily in water reuse and industrial wastewater treatment, with vacuum evaporation playing a role in zero liquid discharge systems for petrochemical and power plants. For example, large refineries and chemical complexes in the UAE have adopted thermal and mechanical vapor recompression vacuum evaporators to meet stringent discharge norms and reclaim water in arid conditions. In Africa, the demand is more project-specific, often tied to mining operations requiring water recycling and effluent reduction. While market volumes are smaller than in other regions, the Middle East & Africa’s strategic need for water-efficient technologies and continued industrial investment support a growing niche market presence.

GCC Vacuum Evaporators Market

The GCC market was estimated at USD 0.080 billion in 2025 and USD 0.085 billion in 2026. The GCC region, including Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, and Oman, holds a strategically important share of the vacuum evaporators market. However, its overall revenue share is modest compared to larger economies. Demand in this region is primarily driven by petrochemical complexes, oil & gas refineries, and power plants that require robust wastewater management and water reuse systems in arid conditions. Vacuum evaporators, especially high-capacity and energy-efficient configurations, form part of zero liquid discharge (ZLD) strategies in large industrial installations. Additionally, government initiatives to reduce water imports and enhance sustainability bolster the region’s adoption.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Companies Offer Extensive Vacuum Evaporators Portfolios to Cater to Clientele Needs

Veolia Water Technologies, GEA Group, Alfa Laval, SUEZ Water Technologies & Solutions, and Condorchem Enviro Solutions are some of the key players in this market. Veolia is one of the most influential players in the vacuum evaporators industry, particularly in the context of industrial wastewater management and zero liquid discharge (ZLD) systems. The company integrates vacuum evaporators into broader water treatment solutions for heavy industries such as chemicals, petrochemicals, power, mining, and food & beverage. In these sectors, Veolia designs, supplies, and often operates complex evaporation trains, combining multi-effect evaporators, mechanical vapor recompression (MVR), crystallizers, and ancillary systems, to reduce effluent volumes, recover clean water, and help clients meet stringent discharge regulations.

List of Top Vacuum Evaporators Companies Profiled

- Veolia (France)

- GEA Group (Germany)

- SUEZ Water Technologies & Solutions (France)

- Alfa Laval (Sweden)

- SPX FLOW (U.S.)

- Condorchem Enviro Solutions (Spain)

- De Dietrich Process Systems (Germany)

- Lenntech (Netherlands)

- ENCON Evaporators (U.S.)

- Eco-Techno (Italy)

- SAMSCO (U.S.)

- Sirco Industrial (U.S.)

- Labconco (U.S.)

- IKA Works (Germany)

- Buchi Labortechnik (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- January 2025: GEA Group launched the eZero Dairy Evaporator, a next-generation MVR-based vacuum evaporation system targeting the dairy sector, capable of reducing energy consumption by up to 60% and enabling zero CO₂ emissions when powered by renewable electricity. This product addresses rising energy costs and tighter sustainability targets in food processing by significantly cutting both operational expenses and environmental impact.

- January 2025: De Dietrich introduced a short-path evaporation system specifically built for refining vegetable oils and extracting high-value compounds such as squalene, sterols, and tocopherols. This development expands vacuum evaporation applications into value-added processing sectors beyond traditional wastewater uses.

- December 2024: SPX Flow announced plans to move toward integrating AI-driven analytics and predictive performance optimization into its evaporator offerings in 2025, aiming to reduce unplanned downtime and improve process reliability. This aligns with a broader industry shift toward digitalized and automated thermal separation systems.

- September 2024: Veolia’s Evaled™ vacuum evaporator technology continued to evolve with enhanced automation, greater energy efficiency, and modular integration for industrial wastewater and zero liquid discharge (ZLD) systems. These advances help industrial clients reduce disposal costs dramatically by enabling effective water reuse and by-product recovery, while complying with tightening regulations.

- August 2024: Condorchem Enviro Solutions introduced a new high-recovery Mechanical Vapor Recompression (MVR) evaporator series designed for industrial effluent streams with high dissolved solids. This series enhances water recovery up to 98% while minimizing brine volume, addressing a common challenge in textile, chemical, and mining wastewater treatment. The updated units also integrate advanced fouling-resistant heat exchanger surfaces and digital controls that improve operational reliability in continuous duty cycles.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.12% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type · Rotary Vacuum Evaporators · Centrifugal Vacuum Evaporators · Others |

|

By Application · Laboratory · Wastewater Treatment · Product Processing · Others |

|

|

By End User · Pharmaceuticals · Electronics & Semiconductor · Chemical & Petrochemical · Food & Beverages · Energy & Power · Others |

|

|

By Region

|

Frequently Asked Questions

According to a study by Fortune Business Insights, the market size was valued at USD 3.46 billion in 2025 and is expected to reach USD 6.51 billion by 2034.

The market is likely to grow at a CAGR of 7.12% over the forecast period (2026-2034).

By product type, the centrifugal vacuum evaporators segment leads the market.

The North America market size stood at USD 1.26 billion in 2025.

Stringent environmental regulations and the growing adoption of Zero-Liquid-Discharge (ZLD) mandates are key factors poised to push the market growth.

Some of the leading players in the market include Veolia Water Technologies, GEA Group, Alfa Laval, SUEZ Water Technologies & Solutions, and Condorchem Enviro Solutions.

- 2021-2034

- 2025

- 2021-2024

- 227

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us