Vaginal Slings Market Size, Share & Industry Analysis, By Product (Tension-Free Vaginal Tape Slings, Transobturator Slings, and Mini-Slings), By Type (Midurethral Sling and Traditional Sling), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Vaginal Slings Market Size and Future Outlook

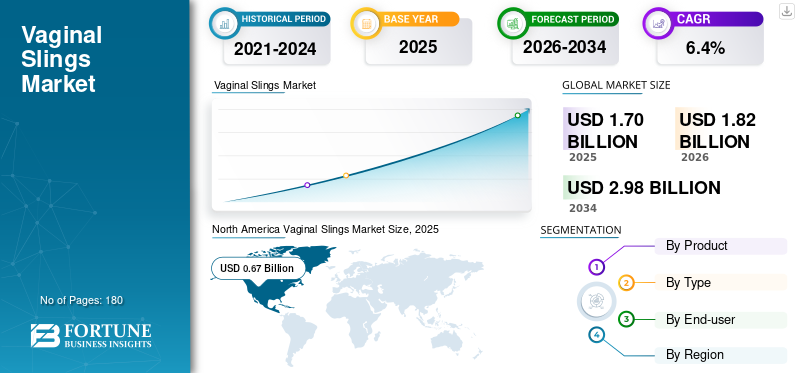

The global vaginal slings market size was valued at USD 1.70 billion in 2025. The market is projected to grow from USD 1.82 billion in 2026 to USD 2.98 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the vaginal slings market with a market share of 39.41% in 2025.

Vaginal slings are surgically implanted support systems placed under the urethra to reduce involuntary urine leakage during coughing, sneezing, laughing, exercise, or other activities that increase abdominal pressure. The market includes tension-free vaginal tape slings, transobturator slings, and mini-slings used mainly in midurethral sling procedures. The global market is growing steadily as stress urinary incontinence becomes more widely diagnosed and treated among women, particularly after childbirth, menopause, pelvic surgery, and age-related weakening of pelvic floor muscles. Demand is further supported by the rising female geriatric population, increasing awareness of urinary incontinence as a treatable medical condition, growth in urogynecology services, and the shift toward minimally invasive outpatient procedures. Although mesh-related safety scrutiny has affected adoption in some countries, clinically selected sling procedures continue to remain an important surgical option for women with stress urinary incontinence.

Key players such as Caldera Medical, Boston Scientific Corporation, Coloplast A/S, and Promedon S.A., Ltd held the largest market share, driven by the limited market presence of other players and market consolidation.

Download Free sample to learn more about this report.

VAGINAL SLINGS MARKET TRENDS

Shift Toward Minimally Invasive and Outpatient Sling Procedures is Shaping the Market Trend

A clear market trend is the gradual movement toward less invasive sling procedures, shorter hospital stays, and greater use of outpatient or ambulatory care settings. Midurethral slings remain the core treatment category; however, product preference is increasingly influenced by ease of placement, operative time, recovery profile, and surgeon familiarity. Mini-slings and single-incision sling systems are gaining traction as they may reduce tissue dissection, avoid larger incisions, and fit well with outpatient care models. The FDA has reviewed randomized clinical trial evidence comparing SUI mini-slings with traditional midurethral slings and stated that the clinical performance of mini-slings is comparable to that of traditional midurethral slings, although product-specific evidence and regulatory expectations remain important.

At the same time, hospitals and ASCs are focusing on standardized surgical pathways, improved patient selection, and better documentation to reduce complications and support long-term outcomes. This trend is also encouraging companies to design sling kits with improved ergonomics, dedicated introducers, and simplified procedural steps. In mature markets, the trend is not simply on increasing procedure volume, but on enabling safer, better-documented, and more efficient procedures. In emerging markets, outpatient adoption remains slower but is expected to improve as specialist training and surgical infrastructure continue to develop.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Burden of Stress Urinary Incontinence is Driving Product Demand

A major driver for the market is the large and growing burden of female stress urinary incontinence, which continues to affect quality of life, physical activity, work productivity, and emotional well-being. Many women delay treatment due to embarrassment, lack of awareness, or the belief that urine leakage is a normal part of aging or childbirth. However, greater education by gynecologists, urologists, urogynecologists, and primary care providers is encouraging more women to seek diagnosis and treatment. This is expanding the pool of patients moving from lifestyle management, pelvic floor therapy, or medication toward surgical options when conservative treatment is not sufficient. Vaginal slings, particularly midurethral sling procedures, remain widely used as they are less invasive than many traditional surgical repairs and can often be performed in hospital outpatient departments or ambulatory surgery centers.

The market is also supported by aging female populations in North America, Europe, Japan, and parts of Asia Pacific, where post-menopausal pelvic floor weakness is more common. In emerging markets, improving access to women’s health specialists and private hospitals is gradually increasing procedural adoption. Together, these factors are creating sustained demand for sling systems, especially in countries with strong reimbursement and established pelvic floor care pathways.

MARKET RESTRAINTS

Mesh-related Safety Concerns and Regulatory Scrutiny to Restrain Product Adoption

The key restraint for the market is ongoing concern around mesh-related complications, litigation history, and country-specific restrictions on pelvic floor mesh procedures. Although vaginal slings for stress urinary incontinence are distinct from transvaginal mesh used for pelvic organ prolapse, public perception often groups these products, creating hesitancy among patients and referring physicians. Complications such as pain, mesh exposure, erosion, infection, urinary problems, and the need for revision surgery have increased the emphasis on informed consent, surgeon training, patient selection, and long-term follow-up.

In some markets, especially the U.K. and parts of Europe, mesh procedures have been subject to pauses, registries, and stricter clinical governance, slowing procedure volumes. Manufacturers also face higher evidence requirements, postmarket surveillance expectations, and reputational risks, which can limit new product launches or market expansion. For hospitals and ASCs, the need to document mesh type, product identification, surgical details, and outcomes increases administrative complexity. This restraint does not eliminate demand, but it makes the market more selective and evidence-driven.

MARKET OPPORTUNITIES

Expanding Access in Emerging Markets Offers a Strong Growth Opportunity

A significant opportunity lies in expanding diagnosis and treatment access across Asia Pacific, Latin America, and the Middle East & Africa, where many women with stress urinary incontinence remain untreated. In several emerging countries, urinary incontinence is underreported due to social stigma, limited access to urogynecology specialists, and low awareness of available procedures. As private hospitals, specialty clinics, and women’s health centers continue to expand in these regions, more patients are expected to gain access to treatment pathways. This development creates room for both global and regional manufacturers to introduce cost-appropriate sling systems, physician training programs, and distribution partnerships.

Asia Pacific is a particularly attractive market for investors due to its large female population, rising healthcare spending, and improving surgical infrastructure in China, India, Southeast Asia, and South Korea. Meanwhile, Latin America offers growth opportunities through Brazil and Mexico, where private healthcare networks support the adoption of minimally invasive gynecological and urological procedures. In the GCC, the expansion of premium hospitals and medical tourism programs is strengthening access to advanced female pelvic floor procedures. Manufacturers that provide clinical education, procedural support, and differentiated pricing can improve adoption in these markets.

MARKET CHALLENGES

Lack of Patient Trust and Surgeon Training and Increasing Pressure For Evidence Generation Remain Key Market Challenges

The vaginal slings market faces several practical challenges that extend beyond demand generation. One of the primary challenges is patient trust. Media coverage and litigation related to mesh products have made many women cautious about undergoing sling procedures, even when stress urinary incontinence conditions significantly affect their daily lives. As a result, physicians are required to spend more time explaining benefits, risks, alternatives, and the difference between SUI slings and pelvic organ prolapse mesh.

Another major challenge is the uneven level of surgeon experience across healthcare systems. Clinical outcomes are heavily dependent on correct patient selection, surgical technique, placement accuracy, and the ability to manage complications. In regions with fewer trained urogynecologists or urologists, adoption may remain limited even when patient need is high.

The market faces increasing pressure for evidence generation and long-term follow-up requirements. Regulatory authorities and clinical bodies are demanding stronger long-term outcome data, complication tracking, and transparent reporting, which can be difficult to implement in fragmented healthcare systems. Reimbursement limitations further restrict market growth, especially in countries where women’s pelvic floor procedures are not prioritized or where out-of-pocket healthcare spending reduces patient access. In addition, competition from non-surgical alternatives such as pelvic floor therapy, pessaries, and injectable bulking agents may affect sling volumes among patients who prefer less invasive options. These challenges make the market more dependent on clinical confidence, training programs, and careful communication rather than aggressive product promotion.

Segmentation Analysis

By Product

Transobturator Slings Segment Leads Due to Their Wide Usage in Standard Stress Urinary Incontinence Procedures

Based on product, the market is segmented into tension-free vaginal tape slings, transobturator slings, and mini-slings.

The transobturator slings segment accounts for the highest vaginal slings market share, as they are widely used in standard stress urinary incontinence procedures and are familiar to many urogynecologists and urologists. The transobturator approach avoids the retropubic space, which may reduce concern around certain bladder or vascular injuries compared to traditional retropubic techniques.

To know how our report can help streamline your business, Speak to Analyst

The mini-slings segment is projected to grow at a CAGR of 10.1% during the forecast period.

By Type

Midurethral Slings Segment Lead Due to Established Clinical Acceptance

By type, the market is classified into midurethral sling and traditional sling.

The midurethral sling segment dominates the market as they are the standard sling-based surgical approach for female stress urinary incontinence. These procedures are less invasive than many traditional sling surgeries and are commonly performed through retropubic, transobturator, or mini-sling approaches. Moreover, the segment is projected to hold an 91.8% share by 2026.

The traditional sling segment is estimated to grow at a CAGR of 3.5% during the forecast period.

By End-user

Hospitals and ASCs Dominate Due to Surgical Infrastructure and Procedural Safety Needs

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

The hospitals and ASCs segment holds the largest market share as vaginal sling implantation is a surgical procedure requiring sterile operating environments, anesthesia support, trained surgeons, and post-procedure monitoring. Hospitals remain important for complex patients, revision cases, and markets where procedures are concentrated in public or tertiary care systems. Furthermore, the segment is set to hold a 68.3% share by 2026.

The specialty clinics segment is projected to grow at a CAGR of 7.8% during the forecast period.

Vaginal Slings Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Vaginal Slings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest market share in 2024 with USD 0.62 billion, reaching USD 0.67 billion in 2025. North America is expected to maintain a leading position in the global market due to high diagnosis and treatment rates for stress urinary incontinence, strong access to urogynecologists and urologists, and well-established hospital and ambulatory surgery center infrastructure. The U.S. accounts for the majority of the regional market share, supported by higher procedure volumes, favorable outpatient surgery adoption, and stronger average selling prices for branded sling systems. In addition, rising awareness among women that urinary leakage is a treatable medical condition, along with the growing elderly female population and post-menopausal pelvic floor disorders, continues to support demand.

U.S. Vaginal Slings Market

The U.S. market is forecasted to represent USD 0.66 billion by 2026, capturing 36.2% of total global revenues.

Europe

Europe is expected to achieve a 4.8% growth rate during the coming years, the second-highest globally, reaching USD 0.45 billion by 2026. Europe is projected to grow at a moderate pace, driven by the large target patient population, established gynecology and urology care networks, and gradual recovery of sling procedures in selected countries. Germany, France, Italy, Spain, and Scandinavia continue to support market demand through specialist-led pelvic floor care and access to surgical treatment options.

U.K. Vaginal Slings Market

The U.K.’s market is projected to reach USD 0.04 billion by 2026, accounting for 2.3% of the global market revenue.

Germany Vaginal Slings Market

Germany's market is forecasted to reach about USD 0.10 billion by 2026, representing roughly 5.5% of global revenue.

Asia Pacific

The Asia Pacific market is predicted to reach USD 0.48 billion by 2026, ranking as the second-largest globally. Asia Pacific is expected to be the fastest-growing region in the market during the study period due to its large female population, rising awareness of stress urinary incontinence, improving diagnosis rates, and expanding access to specialist women’s health services. Countries such as China, India, Japan, South Korea, Australia, and Southeast Asian markets are witnessing increasing adoption of minimally invasive gynecological and urological procedures. Growth is especially strong in emerging markets where private hospitals, specialty clinics, and urban healthcare infrastructure are expanding rapidly.

Japan Vaginal Slings Market

The Japanese market is projected to generate approximately USD 0.08 billion in revenue by 2026, contributing nearly 4.6% to the global market.

China Vaginal Slings Market

China's market is forecasted to reach approximately USD 0.14 billion by 2026, contributing about 7.9% to global revenues.

India Vaginal Slings Market

The Indian market is expected to touch approximately USD 0.08 billion by 2026, corresponding to about 4.3% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate growth during the study period. Latin America is expected to reach around USD 0.11 billion by 2026. The region is expected to show steady vaginal slings market growth, supported by Brazil, Mexico, and selected urban healthcare markets across the region. Rising awareness of women’s pelvic floor disorders, expansion of private hospital networks, and increasing availability of minimally invasive surgical procedures are key factors supporting demand. The Middle East & Africa market is expected to grow from a smaller base, supported by improving women’s health services, rising private healthcare investment, and increasing availability of advanced gynecological and urological procedures in urban centers.

GCC Vaginal Slings Market

By 2026, the GCC is expected to generate approximately USD 0.03 billion in the market, accounting for nearly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global market is moderately consolidated, with a few multinational and specialist women’s health companies holding a significant share. At the same time, several regional manufacturers compete in Europe, Latin America, Asia Pacific, and other emerging markets. Caldera Medical, Boston Scientific Corporation, Coloplast A/S, and Promedon S.A. These players maintain strong market positions due to their established midurethral sling portfolios, broad distribution networks, strong surgeon familiarity, and strong access to hospital and ASC purchasing channels. Moreover, Caldera Medical’s acquisition of Ethicon’s GYNECARE TVT portfolio further strengthens its position in the global SUI sling segment.

Moreover, other key players, such as UroCure, A.M.I. – Agency for Medical Innovations GmbH, Neomedic International, and Betatech Medical, compete through ongoing technological advancements and the development of products in clinical trials.

LIST OF KEY VAGINAL SLINGS MARKET COMPANIES PROFILED

- Caldera Medical (U.S.)

- Boston Scientific Corporation (U.S.)

- Coloplast A/S (Denmark)

- Promedon S.A. (Argentina)

- UroCure (U.S.)

- M.I. – Agency for Medical Innovations GmbH (Austria)

- Neomedic International (Spain)

- Betatech Medical (Turkey)

- Cousin Surgery (France)

- Herniamesh S.r.l. (Italy)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Caldera Medical is expanding its commitment to women’s health with the acquisition of Ethicon’s Gynecare TVT family of products. The TVT product line consists of TVT, TVT Exact, TVT-O, and TVT Abbrevo, which provide minimally invasive treatment options for women with stress urinary incontinence (SUI).

- October 2024: Coloplast A/S announced that the FDA cleared an updated Altis Single Incision Sling System under K242473, covering mesh-related modifications.

- January 2024: UroCure and LiNA Medical USA announced the nationwide launch of ArcSP and ArcTO slings, expanding UroCure’s SUI sling portfolio.

- December 2021: Caldera Medical announced FDA clearance and launch of Desara TVez, expanding its Desara family for stress urinary incontinence treatment.

- September 2021: UroCure and LiNA Medical USA announced a strategic sales distribution and product development collaboration for UroCure’s ArcTV sling and wider women’s health portfolio.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Type, End-user, and Region |

| By Product |

|

| By Type |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.70 billion in 2025 and is projected to reach USD 2.98 billion by 2034.

In 2025, the market value stood at USD 0.67 billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period.

The transobturator slings segment leads the market by product.

The key factor driving the market is the rising burden of stress urinary incontinence.

Caldera Medical, Boston Scientific Corporation, Coloplast A/S, and Promedon S.A. are some of the major players in the market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us