Vision Positioning System Market Size, Share & Industry Analysis, By Component (Sensors, Inertial & Aiding Subsystems, Processing Hardware, Navigation Software, Mapping/Reference data layer, and Integration, Ruggedization & Security), By Solution (Vision-aided Navigation, Visual Odometry/Visual-Inertial Odometry, Slam/Relocalization, Terrain-relative Navigation, & Others), By Platform (Air platforms, Land platforms, Space platforms, and Maritime platforms), By Device (Airborne Embedded Navigation Devices, Ground Platform-Mounted Devices, & Others), By End User and Regional Forecast, 2026-2034

Vision Positioning System Market Size and Future Outlook

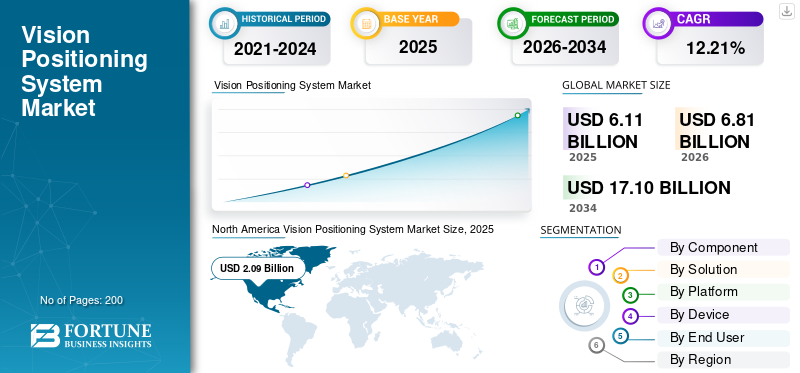

The global vision positioning system market size was valued at USD 6.11 billion in 2025. The market is projected to grow from USD 6.81 billion in 2026 to USD 17.10 billion by 2034, exhibiting a CAGR of 12.21% during the forecast period. North America dominated the vision positioning system market with a market share of 34.20% in 2025.

A vision positioning system (VPS) uses cameras, sensors, and software with computer vision, artificial intelligence and machine learning algorithms to determine the precise location and orientation of a device or object from visual cues, often indoors or where GPS is weak or unavailable. The market includes camera‑based positioning units, image processing software, and sensor fusion stacks deployed in robotics, drones, autonomous vehicles, industrial automation, and augmented reality navigation. Growth is driven by rising demand for indoor localization, warehouse and logistics automation, and advanced navigation in GPS denied environments such as tunnels, parking structures, and smart cities and factories.

Major players include DJI, Cognex Corporation, Omron Corporation, SICK AG, ABB, Fanuc Corporation, Qualcomm Technologies, and Sony Corporation, which provide camera based localization modules, industrial vision sensors, or integrated VPS platforms for unmanned aerial vehicles such, robots, and Industry 4.0 applications.

Download Free sample to learn more about this report.

Vision Positioning System Market KEY TAKEAWAYS

- 2025 Market Size: USD 6.11 billion

- 2026 Market Size: USD 6.81 billion

- 2034 Forecast Market Size: USD 17.10 billion

- CAGR: 12.21% from 2026–2034

- North America dominated the vision positioning system market with a 34.20% share in 2025.

- The Mapping/Reference Data Layer segment is projected to register the highest CAGR of 12.99% during the forecast period.

- The Relative Navigation/Docking/Capture segment is projected to grow at the highest CAGR of 12.93% during the forecast period.

Asia Pacific

Asia Pacific is projected to reach USD 1.94 billion by 2026, driven by industrial automation and expanding drone applications.

North America

North America reached USD 2.09 billion in 2025, supported by investments in autonomous drones and defense-grade navigation.

Europe

Europe is projected to reach USD 1.93 billion by 2026, fueled by growth in industrial automation and automotive robotics.

U.S.

U.S. is projected to reach USD 1.41 billion by 2026, driven by increasing deployment of commercial drones and warehouse robotics.

Japan

Japan is projected to reach USD 0.35 billion by 2026, supported by advancements in industrial robotics and automated logistics.

Read More

VISION POSITIONING SYSTEM MARKET TRENDS

Usage of Indoor and GPS‑Denied Navigation is a Key Market Trend

There is a shift toward indoor and GPS‑denied navigation using vision based positioning, driven by the need to operate drones, robots, and autonomous vehicles where satellite signals are weak or absent. Visual Simultaneous Localization and Mapping (SLAM) and vision based localization systems increasingly fuse cameras, IMUs, and sometimes LiDAR or Ultra-Wideband (UWB) to deliver stable, real time positioning in warehouses, tunnels, urban canyons, and indoor facilities. These optical centric stacks are favored as they require little fixed infrastructure, can map unfamiliar environments on the fly, and support emerging applications such as autonomous inspection, logistics, and mixed‑reality navigation beyond traditional GNSS dependent schemes.

Download Free sample to learn more about this report.

Russia Ukraine War Impact

The Russia Ukraine war has intensified military demand for GNSS‑independent vision positioning systems in drones, armored vehicles, and C4ISR platforms, accelerating development and procurement of camera based, AI‑driven navigation in Europe and NATO allied states. At the same time, sanctions and supply chain strains have constrained access to certain semiconductor and sensor inputs, pushing defense and industrial players to diversify components and integrate more robust, multi‑sensor vision‑positioning architectures.

Middle East War Impact

The Middle East war has driven strong demand for vision positioning systems based navigation systems as widespread GPS jamming and spoofing in the Gulf region force commercial vessels, drones, and land platforms to rely on alternative positioning technologies. Governments and maritime operators are investing in optical, inertial, and hybrid vision‑positioning payloads to maintain safe navigation and surveillance, while defense‑adjacent IT and sensor vendors are tailoring resilient navigation stacks for GPS denied, high risk theater operations.

MARKET DYNAMICS

MARKET DRIVERS

Rising automation in Industry 4.0 to Drive Market Growth

Rising automation under Industry 4.0 is a key driver of the vision positioning system market growth, as manufacturers increasingly deploy robotics, AI, and connected systems to boost efficiency, reduce downtime, and enable flexible, data driven production flows. Smart factory initiatives and digital twin based monitoring are pushing demand for advanced sensing, positioning, and control technologies that support collaborative robots, autonomous material handling, and real time asset tracking inside plants. This broader shift toward self-optimizing, highly automated production environments is expanding the installed base for industrial‑grade vision positioning, navigation, and machine vision systems beyond traditional human supervised lines.

MARKET RESTRAINTS

High Upfront Cost is a Market Restraint

High upfront cost is a significant market restraint, as implementing advanced automation and smart factory technologies often requires substantial investment in hardware, software, integration, and training, which many firms specially small and medium sized enterprises struggle to justify. Initial expenditures for sensors, controllers, connectivity infrastructure, and system design can delay or scale back deployment, particularly when the return on investment is uncertain or long‑term.

MARKET OPPORTUNITIES

Rising Predictive Maintenance Solutions New Market Opportunities

Rising adoption of predictive maintenance solutions is creating new market opportunities by shifting industries from reactive to data driven maintenance strategies that rely on IoT sensors, AI, and real time analytics. As manufacturers, energy operators, and transport fleets deploy these systems to cut unplanned downtime, extend asset life, and optimize maintenance scheduling, demand grows for integrated sensor platforms, edge processing units, and cloud-enabled analytics stacks. These trends open avenues for scalable, modular predictive maintenance offerings that can be adapted across sectors, including small and medium‑sized enterprises.

MARKET CHALLENGES

Cybersecurity Threats Present a Major Market Challenge

Cybersecurity threats present a major market challenge as expanding industrial IoT and predictive maintenance systems significantly widen the attack surface for malware, ransomware, and data exfiltration attempts. Concerns over data integrity, privacy, and potential sabotage make manufacturers cautious about rolling out large scale connected positioning and maintenance platforms, and force heavy investment in network segmentation, encryption, and zero‑trust architectures that slow deployment and increase total cost.

Segmentation Analysis

By Component

Sensors Segment to Lead due to Critical Role of Industry 4.0 Applications

Based on component, the market is segmented into sensors, inertial & aiding subsystems, processing hardware, navigation software, mapping/reference data layer, and Integration, ruggedization & security.

The sensor segment is anticipated to account for the largest market share. The segment’s growth is owing to the critical role of Industry 4.0 applications, where they provide robotic arms, Automated Guided Vehicles (AGVs), and Autonomous Mobile Robots (AMRs) with accurate, real-time spatial data needed for object detection, navigation, and 3D positioning.

The mapping/reference data layer segment is anticipated to rise with a highest CAGR of 12.99% over the forecast period.

By Solution

High Visibility Boosted Vision-aided Navigation Segment Growth

Based on solution, the market is segmented into vision-aided navigation, visual odometry/ visual-inertial odometry, SLAM/relocalization, terrain-relative navigation, relative navigation /docking/capture, and precision landing & terminal guidance.

In 2025, the vision-aided navigation segment dominated the global market. The segment’s growth is mainly due to its crucial role in industrial, warehousing, and Autonomous Mobile Robot (AMR) navigation, as they maintain good visibility in low light or changeable lighting circumstances.

The relative navigation/docking/capture segment is projected to grow at a highest CAGR of 12.93% over the forecast period.

By Platform

Air Platforms to Lead the Market Due to Extensive Reliance of Drones and UAVs

Based on platform, the market is segmented into air platforms, land platforms, space platforms, and maritime platforms.

The air platforms segment is anticipated to witness a dominant market share over the forecast period. The segment’s dominance is owing to extensive reliance of drones and UAVs on camera‑based and sensor-fusion technologies positioning for precise navigation, stable hovering, and obstacle avoidance in GPS‑denied or complex environments.

The space platforms segment is projected to grow at a highest CAGR of 12.71% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Device

Defense & Surveillance Upgrades Boosted the Airborne Embedded Navigation Devices Segment Expansion

Based on device, the market is segmented into airborne embedded navigation devices, Ground platform-mounted devices, weapon/seeker-based devices, soldier-worn/wearable devices, Spaceborne vision-navigation devices.

The airborne embedded navigation devices segment held the dominant vision positioning system market share. Modern defense and surveillance programs are upgrading drones and manned aircraft with advanced airborne embedded navigation devices that combine vision based positioning, inertial sensors, and secure data links for precise, GPS‑denied operation in contested environments.

Spaceborne vision-navigation devices are projected to grow at a highest CAGR of 13.18% during the study period.

By End User

Growing Deployment Across Diverse Applications Boosted Commercial Segment Growth

Based on end user, the market is segmented into commercial, defense, government/space agencies, and others.

The commercial segment dominated the market. The segment is gaining momentum as the product can be deployed across diverse applications from drone delivery and warehouse logistics to precision agriculture and infrastructure inspection using the same embedded navigation hardware with minor software tuning.

The government/space agencies are projected to grow at a highest CAGR of 12.49% during the study period.

Vision Positioning System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Vision Positioning System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1.88 billion, and also maintained its leading share in 2025, with USD 2.09 billion, driven by strong investments in autonomous drones, industrial automation, and defense‑grade navigation.

U.S. Vision Positioning System Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.41 billion in 2026, accounting for roughly 12.62% CAGR. The U.S. is the leading market, underpinned by rapid deployment of commercial drones, warehouse robotics, and military UAVs that rely on embedded vision‑based navigation.

Europe

Europe is projected to record a steady growth rate during the forecast period of 11.91%, which is the second-highest among all regions, and reach a valuation of USD 1.93 billion by 2026. The region exhibits strong growth, particularly in industrial automation, automotive robotics, and precision‑agriculture drones.

U.K. Vision Positioning System Market

The U.K. market is estimated at around USD 0.62 billion by 2026, representing roughly 12.42% CAGR during the study period. The U.K. is expanding vision positioning‑enabled drone operations, especially in inspection, surveying, and eventually BVLOS commercial flights governed by evolving CAA rules.

Germany Vision Positioning System Market

Germany’s market is projected to reach approximately USD 0.56 billion by 2026. Germany is a core hub for industrial‑grade VPS, given its advanced manufacturing, robotics, and automotive sectors.

Asia Pacific

The Asia Pacific region is estimated to reach USD 1.94 billion by 2026 and secure the position of the third-largest region in the market and fastest-growing during the study period. The region is led by dense urban logistics, agricultural‑drone expansion, and growing industrial automation.

Japan Vision Positioning System Market

The Japanese market is estimated at around USD 0.35 billion by 2026, accounting for roughly 12.73% of compound annual growth rate (CAGR) during the forecast period. Japan is advancing product in industrial robotics, disaster response drones, and automated logistics, leveraging its strong electronics and sensor manufacturing base.

China Vision Positioning System Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.59 billion. China is a major center for the product, driven by domestic drone manufacturing, smart city initiatives, and large scale agricultural drone fleets. Chinese UAV firms and avionics suppliers are investing in integrated camera‑plus‑IMU stacks and AI‑driven navigation chipsets, while state‑backed infrastructure and logistics‑modernization plans.

India Vision Positioning System Market

The Indian market is estimated at around USD 0.53 billion by 2026. India is emerging as an important market, spurred by digital‑agriculture schemes, smart ‑city projects, and drone delivery pilot programs.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. Latin America, the Middle East, and Africa are growing markets, particularly in mining, oil‑and‑gas inspection, and urban‑infrastructure monitoring. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.38 billion and USD 0.23 billion, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Strategic Partnerships to Gain Competitive Edge

The vision positioning system market is moderately consolidated, with specialized technology providers such as DJI, Cognex Corporation, SICK AG, Omron, and ABB holding significant shares through embedded OEM integrations and certified sensing stacks tailored for industrial and aerial platforms. These players focus on advancing camera-based localization, sensor fusion, and AI‑driven navigation technologies to address evolving performance and safety standards in autonomous vehicles, drones, and smart factories. Strategic partnerships are accelerating market expansion, as DJI collaborates with large logistics and agriculture OEMs on autonomous drone navigation platforms, Cognex integrates its machine vision and positioning modules into industrial robotics supplied by global automation integrators. SICK AG partners with major AGV and cobot manufacturers to embed 3D‑vision navigation into warehouse and factory‑floor systems.

LIST OF KEY VISION POSITIONING SYSTEM COMPANIES PROFILED

- SZ DJI Technology Co., Ltd. (China)

- Cognex Corporation (U.S.)

- SICK AG (Germany)

- OMRON Corporation (Japan)

- ABB Ltd. (Switzerland)

- Fanuc Corporation (Japan)

- Parrot Drones SAS (France)

- Seegrid Corporation (U.S.)

- Pepperl+Fuchs GmbH (Germany)

- Senion AB (Verizon Communications Inc.) (Sweden)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Hensoldt completed the first release milestone for its Ceretron software-defined defense runtime environment. This was done in order to integrate containerized algorithms into ground systems for operating optronic reconnaissance sensors with nearly real-time results presentation.

- January 2025: The U.S. Army awarded L3Harris Technologies a USD 263 million order to continue manufacturing the Enhanced Night Vision Goggle Binocular (ENVG-B).

- January 2025: sA delivery order worth over USD 139 million was given to Elbit Systems of America to continue manufacturing the Enhanced Night Vision Goggle Binocular (ENVG-B) systems for the U.S. Army, along with spare parts and logistical assistance.

- January 2025: SICK, a global supplier of sensor-based automation systems with its headquarters located in Germany, announced that it has acquired Accerion, a Dutch technology startup. Accerion focuses on positioning technology for mobile robots and is an expert in AI-based image processing.

- April 2023: For high-speed manufacturing lines, Cognex introduced its In-Sight 3800 Vision System, which is said to provide a comprehensive vision toolkit, strong imaging capabilities, and adaptable software for a range of inspection applications.

REPORT COVERAGE

The global vision positioning system industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, and key aviation industry developments and prevalence by key regions. The global market report also provides an in-depth competitive landscape, including information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.21% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Solution, Platform, Device, End User, and Region |

| By Component |

|

| By Solution |

|

| By Platform |

|

| By Device |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.11 billion in 2025 and is projected to reach USD 17.10 billion by 2034.

In 2025, the market value stood at USD 2.09 billion.

The market is expected to exhibit a CAGR of 12.21% during the forecast period.

By component, the sensors segment is expected to dominate the market.

Rising automation in Industry 4.0 is a key factor driving market growth.

SZ DJI Technology Co., Ltd., Cognex Corporation, SICK AG, OMRON Corporation, ABB Ltd. are few key players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us