Waste To Diesel Market Size, Share & Industry Analysis, By Feedstock (Plastic Waste, Biomass, Industrial Waste, Municipal Solid Waste, Rubber Waste, and Others), By Technology (Catalytic Depolymerization, Gasification + FT, Hydrothermal Liquefaction (HTL), Pyrolysis, and Others), By End User (Automotive, Industrial, Power Generation, and Marine), and Regional Forecast, 2026-2034

Waste to Diesel Market Overview

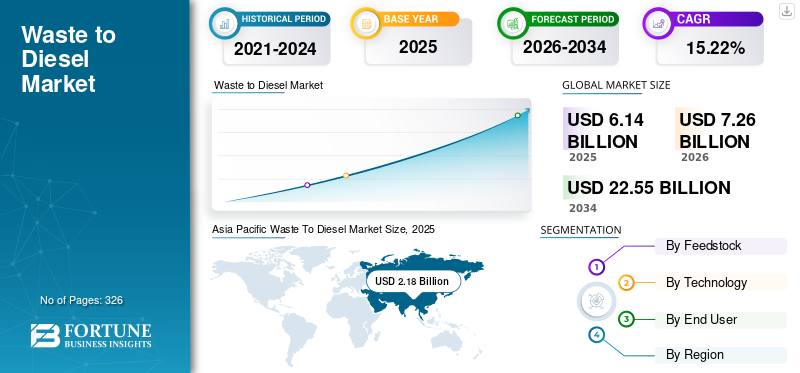

The global waste to diesel market size was valued at USD 6.14 billion in 2025. The market is projected to grow from USD 7.26 billion in 2026 to USD 22.55 billion by 2034, exhibiting a CAGR of 15.22% during the forecast period. Asia Pacific dominated the waste to diesel market with a market share of 35.5% in 2025.

Waste to diesel refers to the process of converting various waste materials, such as plastic waste, municipal solid waste, biomass, industrial residues, and rubber waste, into diesel-range fuels through advanced thermochemical technologies. These technologies typically include pyrolysis, gasification followed by Fischer–Tropsch synthesis, catalytic depolymerization, and hydrothermal liquefaction. The process breaks down complex waste polymers and organic matter into hydrocarbons that can be refined into usable diesel fuel. Diesel facilities support circular economy principles by diverting waste from landfills and reducing dependence on conventional fossil fuels. It also contributes to lower lifecycle greenhouse gas emissions when compared to traditional petroleum-based diesel.

The market is expected to be driven by rising global waste generation, increasing focus on renewable energy, and surging pressure to reduce landfill dependency. Stringent environmental regulations on plastic disposal and carbon emissions are encouraging governments and industries to adopt advanced waste-to-fuel technologies. Growing demand for alternative and low-carbon fuels in transportation, marine, and industrial sectors further supports market expansion. Technological advancements in pyrolysis, gasification, and catalytic upgrading have improved conversion efficiency and fuel quality, enhancing commercial viability. Additionally, the shift toward circular economy models and energy security concerns in many countries is accelerating investment in waste-to-diesel infrastructure.

Agilyx Corporation, Plastic Energy, Enerkem, Brightmark, and Fulcrum BioEnergy are among the leading companies in this market. These companies play a significant role in advancing waste-to-diesel production through large scale refining infrastructure, integration of advanced thermochemical conversion technologies, feedstock sourcing networks, and strategic partnerships across the waste management and energy value chain. They contribute to commercialization, capacity expansion, technology optimization, and the development of low-carbon fuel distribution networks globally.

Download Free sample to learn more about this report.

WASTE TO DIESEL MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 6.14 Billion

- 2026 Market Size: USD 7.26 Billion

- 2034 Forecast Market Size: USD 22.55 Billion

- CAGR: 15.22% from 2026–2034

- Asia Pacific dominated the waste to diesel market with a 35.5% share in 2025.

- Plastic waste accounted for 53.29% of the market share in 2025.

- Pyrolysis held approximately 55.45% of the market share due to its commercial maturity and scalability.

Asia Pacific

Asia Pacific led the market with USD 2.18 billion in 2025 and is projected to reach USD 2.59 billion in 2026.

Europe

Europe generated USD 1.60 billion in 2025 and is expected to grow to USD 1.90 billion in 2026.

North America

North America accounted for USD 1.13 billion in 2025 and is projected to reach USD 1.34 billion in 2026.

U.S.

The waste to diesel market was valued at USD 0.98 billion in 2025 and is projected to reach USD 1.14 billion in 2026.

Japan

The market reached USD 0.28 billion in 2025 and is expected to grow to USD 0.34 billion in 2026.

Read More

Waste To Diesel Market Trends

Inclination Toward Scalable and Modular Conversion Systems are Amplifying Market Growth

A defining trend in the market is the shift toward scalable, modular conversion systems that can be deployed locally to handle region-specific waste streams. Traditionally, early projects relied on pilot-scale plants handling only a few tons per day, but recent commercial deployments are moving into the 50–200 ton-per-day class. These facilities use technologies such as advanced pyrolysis reactors with better heat recovery, automated feedstock handling, and integration with existing refineries. As transport and logistics costs rise, deploying multiple mid-sized waste-to-diesel units near waste generation points becomes increasingly attractive compared to centralized mega-plants. This decentralization trend is supported by improvements in digital process controls that allow remote monitoring and optimization, reducing staffing needs and improving uptime. Key industrial clusters are now actively integrating these modular units into larger hubs where plastic recycling facilities, MSW sorting centers, and end-of-life tire processors are colocated, creating a local ecosystem of waste conversion. This trend is reinforcing the notion that successful waste-to-diesel deployment requires not only core conversion technology but also robust integration with upstream waste collection and downstream fuel distribution networks.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Waste Generation and Tightening Environmental Standards to Push Market Growth

A principal driver for the waste to diesel market growth is the waste generation combined with tightening environmental standards that make landfill disposal less economically attractive or politically acceptable. As urban populations expand and consumption patterns shift toward packaged goods, the amount of plastic waste and mixed municipal waste rises steadily year after year. At the same time, many governments are implementing stricter landfill taxes, single-use plastic bans, and extended producer responsibility policies that significantly increase the cost of traditional disposal. This combination creates a strong economic push toward alternative waste valorization pathways, where converting waste into diesel and other usable fuels becomes a financially viable option. Corporations committed to net-zero goals are also attracted by the potential to reduce their Scope 1 and Scope 3 emissions by blending waste-derived diesel into existing fuel pools or by meeting internal sustainability mandates. As conventional diesel remains a backbone fuel for heavy logistics and industrial operations, the appeal of producing an alternative that meets required specifications while lowering the carbon footprint adds commercial momentum and investment interest across regions.

Market Restraints

Volatile Regulatory Landscapes Across the Globe to Limit Market Growth

One key restraint on market expansion is policy uncertainty and inconsistent regulatory incentives across regions, which create financial risk for investors and project developers. While some jurisdictions offer incentives such as tax credits, renewable fuel blending mandates, or landfill diversion surcharges that favor waste-to-fuel pathways, many others lack stable long-term frameworks. In regions where incentive programs are short-term or subject to political change, financiers are reluctant to commit capital to long-lead-time projects that require predictable returns. This inconsistency is further compounded by differing definitions of what qualifies as renewable or sustainable diesel in various policy regimes, leading to confusion around certification, eligibility for credits, and lifecycle emissions accounting. Without harmonized fuel quality standards and clear pathways for securing value from environmental benefits, companies may face stranded assets or underperforming facilities. The result is that developers often focus on a handful of supportive markets while deprioritizing regions with weak regulatory signals, thereby restraining broader global uptake. Until policy frameworks become more aligned and durable, this restraint will continue to slow the scale-up and geographic diversification of waste-to-diesel infrastructure.

Market Opportunities

Increasing Range of Feedstock Sources to Create New Growth Avenues

A significant opportunity in the waste-to-diesel space lies in expanding the range of feedstock streams beyond traditional plastics toward more challenging waste categories such as mixed municipal refuse, organic-rich waste, and composite materials. Many regions have developed only basic sorting infrastructure, meaning large volumes of waste are landfilled or incinerated with minimal energy recovery. Introducing technologies that can handle heterogeneous waste without intensive preprocessing opens up vast untapped feedstock supply. For example, improved hydrothermal liquefaction processes can convert organic and wet waste that is currently uneconomical for other pathways, while catalytic depolymerization variants are increasingly capable of handling mixed polymer streams that would otherwise be incinerated or mechanically recycled at low value. This expansion of feedstock not only increases the potential volume of diesel-range output but also strengthens the business case by reducing the cost of feedstock acquisition and improving utilization rates. Additionally, by linking waste-to-diesel facilities with carbon credit markets or renewable fuel standards in key jurisdictions, operators can capture additional revenue streams that enhance long-term project viability. This presents a meaningful opportunity for new entrants and existing players to scale operations and integrate vertically across waste collection, processing, conversion, and fuel distribution.

Market Challenges

Complexity and Variability of Waste Streams to Limit Market Growth

A central challenge for waste-to-diesel projects is the complexity and variability of waste streams, which directly impacts plant performance, fuel quality, and operational costs. Unlike dedicated biomass or homogenous feedstocks such as virgin vegetable oil, waste streams such as mixed plastics, municipal solid waste, and industrial residues vary widely in composition, energy content, moisture, and contaminants. This variability can cause fluctuations in yield, corrosion issues in reactors, catalyst deactivation, and unstable product quality if not properly managed. Designing conversion processing plants that can robustly handle this variability without frequent downtime for cleaning, sorting, or maintenance adds engineering complexity and cost. In practice, operators often have to invest heavily in front-end sorting and preconditioning facilities to remove inert materials, moisture, and non-hydrocarbon fractions before conversion, increasing the capital outlay and reducing project margins. Furthermore, meeting stringent diesel specification standards requires additional upgrading, refining, and quality assurance steps that are sensitive to input feedstock quality. As a result, the industry continues to wrestle with the trade-off between feedstock breadth and economic performance, making high-efficiency, low-cost waste-to-diesel conversion technically and commercially challenging.

Segmentation Analysis

By Feedstock

High Hydrocarbon Content in Plastic Waste to Lead Segment Growth

Based on feedstock, the market is segmented into plastic waste, biomass, industrial waste, municipal solid waste, rubber waste, and others.

Plastic waste accounts for approximately 53.29% of the waste to diesel market share in 2025. Plastic waste is the most significant and widely deployed feedstock in the global market due to its high hydrocarbon content and energy density, which enable comparatively higher liquid fuel yields per ton of input. The large generation of plastics from packaging, consumer goods, and industrial products, with many regions still lacking effective recycling systems, means that a substantial fraction of plastic ends up in landfill or incineration. This creates both environmental pressure and regulatory incentives to divert plastics into thermochemical conversion pathways such as pyrolysis and catalytic depolymerization. Technologies that can handle mixed plastic streams without intensive sorting are gaining ground, attracting investments as they can process materials previously considered unrecyclable. As countries tighten single-use plastic bans and impose higher landfill costs, plastic-to-diesel systems become commercially attractive, enabling players to monetize both waste diversion and fuel production.

Municipal solid waste is expected to grow at a CAGR of 16.06% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Simpler Design and Modular Scalability for Pyrolysis Technology to Lead Segment Growth

Based on technology segment, the market is segmented into catalytic depolymerization, gasification + FT, Hydrothermal Liquefaction (HTL), pyrolysis, and others.

Pyrolysis accounts for approximately 55.45% of the market share. Pyrolysis is the most commercially deployed and mature technology in the global waste-to-diesel sector, widely valued for its relative simplicity, modular scalability, and applicability to a broad spectrum of waste feedstocks, particularly plastics, tires, and carbonaceous industrial residues. By thermally decomposing feedstock in the absence of oxygen, pyrolysis yields a liquid condensate that can be further refined into diesel and other hydrocarbon products. Its popularity stems from lower capital costs and the ability to operate at small to mid-scale facilities, enabling deployment near waste generation sources and reducing transportation costs. This modularity has catalyzed market growth in regions lacking large centralized infrastructure, including parts of Asia Pacific, South America, and emerging economies. Many projects combine pyrolysis with downstream quality upgrading units to enhance fuel stability and meet regional diesel specifications.

Catalytic depolymerization is expected to grow at a CAGR of 16.67% during the forecast period.

By End User

Heavy Reliance on Diesel by Automotive Sector to Propel Segment Growth

Based on end user, the market is segmented into automotive, industrial, power generation, and marine.

Automotive segment represents the largest share of around 49.38% in the market in 2025. The automotive segment is the largest end-use application for diesel fuels globally, making it a critical driver of the market. As heavy-duty vehicles, commercial fleets, buses, and logistics trucks continue to rely on diesel for efficiency and range, demand for alternative diesel sources grows in tandem with sustainability commitments by fleet operators. Waste-derived diesel, produced from feedstocks such as plastic waste, MSW, and industrial polymers, can be blended into existing diesel pools or used in dedicated low-carbon fuel programs without major engine modifications. Regulatory pressures in major markets, including stricter tailpipe emissions standards and carbon intensity reduction programs, are encouraging adoption of low-carbon diesel alternatives as transitional fuels. Additionally, large corporate sustainability targets and fuel procurement strategies are increasingly incorporating waste-to-diesel as a viable pathway to reduce Scope 1 emissions.

Automotive segment is the second leading segment with a share of 8.57% in 2025.

Waste To Diesel Market Regional Outlook

By region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Waste To Diesel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 1.13 billion in 2025, accounting for approximately 18.43% of the global market. The market in North America is driven by a combination of strong regulatory pressures on plastic waste diversion, high diesel demand in transportation and industrial sectors, and ample investment capital for emerging energy technologies. The U.S. alone generates hundreds of millions of tons of municipal solid waste annually, with plastics accounting for a significant share, meaning there is a substantial feedstock pool for conversion technologies such as pyrolysis and catalytic depolymerization. Several commercial pyrolysis facilities in the U.S. have been commissioned to convert post-consumer plastic into diesel-range fuels, and partnerships between waste collection authorities and fuel producers are expanding across states such as California and Texas. In Canada, similar initiatives are gaining traction, with provincial mandates encouraging waste-to-fuel adoption. The region’s strong logistics infrastructure supports distributed deployment of modular units, enabling producers to place waste conversion plants near major waste hubs.

U.S. Waste To Diesel Market

The U.S. market was estimated at USD 0.98 billion in 2025 and USD 1.14 billion in 2026. The U.S. market is driven by advanced waste management infrastructure, high diesel consumption in transportation and industrial sectors, and active private investment into pyrolysis and catalytic conversion projects. Strong regulatory focus on plastic waste diversion and low-carbon fuel credits further increases the region’s share relative to emerging markets.

Europe

Europe accounted for USD 1.60 billion in 2025, representing approximately 25.89% of global revenues. Europe’s waste-to-diesel landscape is shaped by stringent environmental legislation, ambitious carbon reduction commitments, and well-established waste management infrastructure. Countries within the European Union have historically led efforts to divert waste from landfills, resulting in meticulously sorted waste streams that facilitate conversion into fuels. For instance, several Western European nations have achieved landfill diversion rates exceeding 70%, with robust recycling and material recovery schemes feeding advanced conversion technologies. In parts of Central and Northern Europe, gasification combined with Fischer–Tropsch synthesis has been piloted to convert mixed municipal solid waste into diesel-range hydrocarbons, while Southern European regions are increasingly adopting pyrolysis units to process agricultural and plastic waste. Moreover, the growth of circular economy initiatives, including extended producer responsibility for packaging, is increasing the volume of post-consumer plastics available for conversion. Diesel demand in Europe remains high for freight transportation and industrial applications, prompting national governments to incentivize low-carbon fuel adoption.

Germany Waste To Diesel Market

Germany was estimated at USD 0.40 billion in 2025 and USD 0.48 billion in 2026. Germany’s market demand is supported by strict landfill diversion targets and a mature recycling ecosystem. Its share is bolstered by sophisticated waste sorting systems and pilot projects that utilize gasification + FT and catalytic depolymerization for high-quality diesel production.

U.K. Waste To Diesel Market

The U.K. market was valued at USD 0.24 billion in 2025 and USD 0.28 billion in 2026. The U.K.’s share is growing rapidly as policy incentives promote circular economy solutions and low-carbon fuels, particularly for transport and industrial applications. The combination of strong environmental mandates and expanding conversion facilities positions the U.K. as a notable European contributor to global market volumes.

Asia Pacific

Asia Pacific market is the largest region in 2025, valued at USD 2.18 billion, accounting for approximately 35.43% of global revenues. Asia Pacific dominates the global market, due to rapid urbanization, high population density, and escalating waste generation. Major metropolitan areas such as Tokyo, Shanghai, Delhi, and Jakarta produce vast quantities of municipal solid waste, much of which contains high fractions of plastic and organic material. With traditional waste management systems in many parts of Asia struggling to keep pace, often resulting in open dumping or informal burning, governments and private developers are turning toward advanced conversion pathways to extract value from this waste. Industrial clusters in China and India have begun integrating modular pyrolysis plants near recycling centers to process mixed plastics into diesel range outputs, while feedstock processing facilities are rising in Southeast Asian countries to support regional demand.

China Waste To Diesel Market

China remains the dominant contributor in Asia Pacific, estimated at USD 0.98 billion in 2025 and USD 1.17 billion in 2026. China represents one of the largest national market shares globally due to immense waste generation from urbanization and rapid industrial expansion. The country’s investment in modular pyrolysis plants and MSW conversion infrastructure supports a high volume of waste-derived diesel production relative to other Asian economies.

India Waste To Diesel Market

India was estimated at USD 0.40 billion in 2025 and USD 0.48 billion in 2026. India’s share is expanding as plastic waste volumes soar and municipal waste systems modernize, especially in major cities. Growing demand for diesel in transport, agriculture, and power generation, combined with emerging projects, positions India as a fast-emerging market within Asia Pacific.

Japan Waste To Diesel Market

Japan was valued at USD 0.28 billion in 2025 and USD 0.34 billion in 2026. Japan’s market share is supported by strong technology adoption, stringent emission standards, and efficient waste collection systems. Concentrated industrial demand and integration of waste conversion with existing fuel networks sustain Japan’s steady contribution to the global market.

Latin America

Latin America accounted for USD 0.69 billion in 2025, or approximately 11.22% of global revenues. In Latin America, the market is progressing as countries confront waste accumulation challenges and seek alternative energy solutions amid energy cost volatility. Large urban centers, such as São Paulo, Mexico City, and Buenos Aires, generate millions of tons of municipal waste annually, with plastics and organic refuse comprising a significant fraction. Traditional waste handling systems in the region often lack sufficient landfill capacity, prompting municipalities to explore waste-to-fuel technologies as part of broader integrated waste management plans. Private and public partnerships have begun emerging to establish pyrolysis and gasification facilities that convert scrap plastics and industrial residues into diesel-range fuels, leveraging local feedstock supplies. Additionally, diesel consumption remains robust in Latin America’s heavy transport and industrial sectors, where diesel-powered trucks, buses, and machinery are prevalent. In some countries, high import costs for conventional diesel and periodic fuel price spikes further incentivize domestic production of alternative fuels.

Middle East & Africa

The Middle East & Africa were valued at USD 0.55 billion in 2025. The Middle East & Africa region presents a unique market characterized by contrasting waste volumes, energy consumption patterns, and infrastructure maturity. In the Middle East, high per-capita waste generation, particularly in rapidly urbanizing GCC states, is driving interest in waste conversion technologies to reduce reliance on landfills and recover energy. Countries with strong fossil fuel sectors are exploring waste-to-diesel as a complementary pathway for diversifying energy portfolios, especially for powering remote operations and industrial zones where diesel gensets are widely used. Advanced pyrolysis facilities processing plastic and rubber waste are being piloted near major metropolitan centers to turn waste into usable fuel, helping address both waste management and energy needs.

GCC Waste To Diesel Market

The GCC market which was estimated at USD 0.25 billion in 2025 and USD 0.29 billion in 2026. The GCC’s market share is growing selectively, driven by high per-capita waste generation and government initiatives to reduce landfill reliance and diversify energy sources. Waste-to-diesel projects in Saudi Arabia, UAE, and neighboring states leverage plastic and industrial waste in regions with high diesel consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

Extensive Waste To Diesel Portfolio are Booming Market Share for Companies

Agilyx Corporation, Plastic Energy, Enerkem, Brightmark, and Fulcrum BioEnergy are some of the key players in the industry. These companies play pivotal roles in driving technological innovation, scaling commercial deployment, and integrating waste-to-fuel solutions with broader waste management and energy systems. By developing and commercializing advanced conversion technologies, such as chemical recycling of mixed plastics, pyrolysis of waste materials, and gasification with downstream fuel synthesis, they are helping transform waste streams that would otherwise end up in landfills or incinerators into valuable diesel-range fuels. Their efforts help validate emerging business models, reduce technology risks, and attract investment into what has historically been a capital-intensive sector.

- In 2022, Virgin Group and Agilyx Corporation collaborated to convert hard-to-recycle plastic waste into synthetic crude oil, which can then be refined into lower-carbon fuels. The initiative aims to divert non-recyclable plastics from landfills while expanding the currently limited supply of sustainable fuel alternatives. As part of its broader net-zero strategy targeting 2050, Virgin Group intends to use these fuels within its portfolio businesses, with Virgin Atlantic expected to be among the early adopters.

List of Key Waste To Diesel Companies Profiled

- Brightmark (U.S.)

- Agilyx Corporation (U.S.)

- Plastic Energy (U.K.)

- Enerkem (Canada)

- Klean Industries (Canada)

- Covanta (U.S.)

- WasteFuel (U.S.)

- Nexus Fuels (U.S.)

- Fulcrum BioEnergy (U.S.)

- Bioelektra Group (Poland)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Viva Energy and Cleanaway Waste Management have partnered to produce renewable diesel in Australia using used cooking oil (UCO). Under the agreement, Cleanaway will supply UCO from its Laverton treatment facility, refining it into a suitable feedstock. Viva Energy has already conducted pilot trials at its Geelong refinery in Victoria, co-processing purified UCO with crude oil to generate renewable fuel products. The initiative aims to strengthen domestic feedstock supply and promote a circular model linking waste recovery with fuel production.

- August 2025: Moeve and Apical have awarded Grupo Cobra and Masa, subsidiaries of Cobra IS under VINCI Group, the contract for electrical, piping, and mechanical works at Spain’s largest second-generation biofuel plant. The facility, being developed in Palos de la Frontera (Huelva) next to Moeve’s La Rábida Energy Park, represents an investment of about €1.2 billion. Designed to produce 500,000 tons per year of sustainable fuels, including SAF and renewable diesel (HVO100), the plant will utilize agricultural residues and used cooking oil as feedstocks.

- June 2025: Sprague Operating Resources LLC has been chosen by the New York City Department of Citywide Administrative Services to supply renewable diesel for New York City’s marine fleet, including the Staten Island Ferry. The contract supports the city’s plan, announced in October 2024, to shift its vessels toward fuels with lower greenhouse gas emissions.

- November 2024: Technip Energies has secured engineering, procurement services, and construction management contracts from Galp SGPS S.A. for a project in Portugal focused on sustainable aviation fuel (SAF), renewable diesel, and green hydrogen. The development will take place at Galp’s existing refinery in Sines, where Galp and Mitsui & Co. Ltd. plan to establish a joint venture to expand renewable diesel and SAF production capacity.

- February 2021: Maire Tecnimont S.p.A., through its subsidiary NextChem, has signed a Front-End Engineering Design (FEED) contract and a Memorandum of Understanding with Essential Energy USA Corp. to develop a renewable diesel biorefinery in South America. Pending the client’s final investment decision, the facility is planned to produce 200,000 tons per year of high-quality renewable diesel using advanced non-food biofeedstocks. NextChem will act as the exclusive EPC contractor, with operations targeted to begin in 2023.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.22% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Feedstock

|

|

By Technology

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.14 billion in 2025 and is projected to reach USD 22.55 billion by 2034.

In 2025, the market value stood at USD 2.18 billion.

The market is expected to exhibit a CAGR of 15.22% during the forecast period.

By feedstock, plastic waste segment is expected to lead the market.

The rising waste generation coupled with tightening environmental standard are driving market expansion.

Agilyx Corporation, Plastic Energy, Enerkem, Brightmark, and Fulcrum BioEnergy are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us