Wearable Ultrasound Devices Market Size, Share & Industry Analysis, By Product Type (Patch-based, Band/Strap-based, and Others), By Application (Cardiovascular Monitoring, Oncology & Tumor Monitoring, Musculoskeletal Monitoring, Maternal & Fetal Monitoring, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Wearable Ultrasound Devices Market Size and Future Outlook

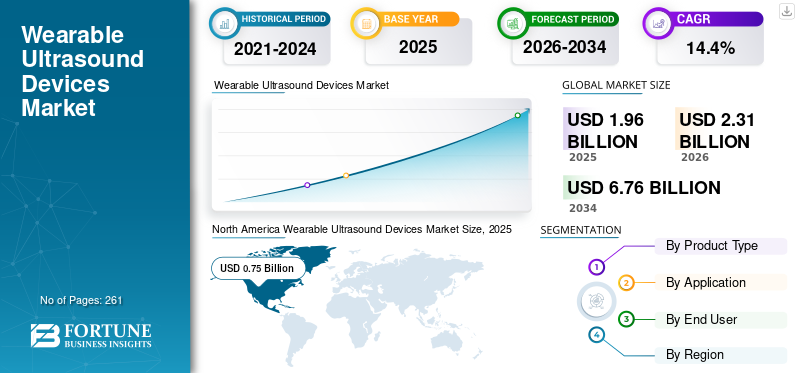

The global wearable ultrasound devices market size was valued at USD 1.96 billion in 2025. The market is projected to grow from USD 2.31 billion in 2026 to USD 6.76 billion by 2034, exhibiting a CAGR of 14.4% during the forecast period. North America dominated the wearable ultrasound devices market with a market share of 38.26% in 2025.

Wearable ultrasound devices are compact and flexible transducers that provide long-term monitoring of internal tissues, blood flow, and organ function. The growing prevalence of chronic diseases, growing awareness about early detection of disorders, rising number of diagnostic imaging procedures, and growing risk pregnancies are resulting in an increasing adoption rate of these devices in the market. The advancements in flexible electronics and miniaturized transducers are further supporting the demand for wearable devices, such as ultrasound, in the market.

- For instance, according to the 2023 data published by the Centers for Disease Control and Prevention (CDC), about 1 in 20 adults aged 20 and older has coronary artery disease in the U.S.

Moreover, the rising research and development activities in these products among the major players, namely Flosonics and ClearSens, Inc., among others, are further driving the demand in the market.

Download Free sample to learn more about this report.

WEARABLE ULTRASOUND DEVICES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.96 billion

- 2026 Market Size: USD 2.31 billion

- 2034 Forecast Market Size: USD 6.76 billion

- CAGR: 14.40% from 2026–2034

- North America dominated the wearable ultrasound devices market with a market share of 38.26% in 2025.

- The band/strap-based segment is projected to grow at a CAGR of 14.9% over the forecast period.

- The segment of oncology & tumor monitoring is set to flourish with a growth rate of 15.4% across the forecast period.

North America

The North America market held the dominant share in 2024, valued at USD 0.51 billion, and also took the leading share in 2025 with USD 0.75 billion.

Europe

Europe is projected to record a growth rate of 13.2% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.63 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 0.56 billion in 2026 and secure the position of the third-largest region in the market.

U.S.

U.S. market can be analytically approximated at around USD 0.80 billion in 2026, accounting for roughly 34.8% of global sales.

Japan

The Japan market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 4.7% of global revenues.

Read More

Wearable Ultrasound Devices Market Trends

Incorporation of AI and Flexible Electronics in Device Design to Fuel Product Demand

An increasing emphasis is being placed on the integration of artificial intelligence, wireless connectivity, and flexible electronics in these devices, which improves image clarity, automated measurements, and reduces abnormalities in real time. The prominent market players are mostly focusing on technologically advanced devices that improve diagnostic accuracy.

Additionally, increasing research and development funding for imaging technologies and advancements in biocompatible materials have further enabled the creation of skin-adhered patches offering stable acoustic contact during movement. The players are providing ultrasound arrays that adhere comfortably for long periods. The integration of Bluetooth and cloud connectivity enables clinicians to monitor patients remotely and access imaging data.

- According to 2024 statistics published by Trackxn, it was reported that digital health wearables startups have received the funding of USD 1.04 billion in the U.S.

Market Dynamics

Download Free sample to learn more about this report.

Market Drivers

Growing Prevalence of Chronic Disorders to Boost Market Growth

The increasing instances of chronic conditions, including cardiovascular disorders and oncology cases, among others, is leading to a rising number of diagnostic procedures within the patient population, consequently driving the demand for wearable ultrasound imaging devices in the market.

- For example, based on 2024 the data released by the Center for Disease Control & Prevention (CDC), it was reported that approximately 1 in 20 adults in the U.S. is affected by coronary artery disease.

This, along with increasing investment among healthcare settings in point-of-care technologies to enhance patient throughput and minimize inpatient stays, subsequently supporting wearable ultrasound adoption. Consequently, the above factors, combined with the increasing focus of major market players on research and development activities to introduce novel products, are expected to support the adoption frequency of these devices. Thereby, this is expected to support the global market size.

Other Prominent Drivers

- Miniaturization of ultrasound products and improved battery/packaging enabling continuous monitoring.

- Growing telehealth adoption and demand for home-based monitoring solutions.

Market Restraints

High Cost and Limited Reimbursement Policies to Limit Market Growth

Despite substantial technological advancements, the market is facing challenges related to reimbursement ambiguity, cost, and clinical integration. These wearable ultrasound devices require advanced materials, compact electronics, and advanced software algorithms, which increase production costs.

Additionally, reimbursement frameworks are still evolving to accommodate continuous imaging modalities, creating uncertainty for healthcare systems considering large-scale deployment, thereby hampering the penetration rate of these products in the market.

- For instance, according to the data published by Etsy, the cost of an ultrasound strap watch is around USD 17.0.

Market Opportunities

Expansion of Ambulatory Surgical Centers to Support Product Adoption

The preference for Ambulatory Surgical Centers (ASCs) for diagnostic procedures has risen owing to their benefits, including improved accuracy, availability of advanced products, and a lower risk of infections acquired from hospitals.

- As per the 2025 statistics released by Definitive Healthcare, there are nearly 10,000 active ambulatory surgical centers in the U.S.

There is a growing expansion of healthcare facilities across developing countries, such as Mexico, Brazil, and others. However, the increasing volumes of diagnostic procedures, expansion of hospital infrastructure, and the growing number of ASCs are consequently driving the adoption of wearable ultrasound devices in clinical settings.

Market Challenges

Clinical Validation and Standardization Barriers to Limit Market Growth

One of the most prominent challenges in the market is achieving clinical validation and standardized usage procedures. The early studies have demonstrated feasibility in musculoskeletal and cardiac monitoring. The requirement of robust comparative data against conventional ultrasound systems before the integration of new technologies into routine practice among physicians is posing challenges in the adoption of these products.

Furthermore, signal quality, motion artefacts, and standardization of image acquisition and analysis remain another challenge. Continuous imaging generates massive datasets, requiring structured methods to ensure clinically actionable insights within the patient population. Additionally, ensuring consistent skin adherence across diverse patient populations can be technically challenging, further hampering the growth of the market.

- For example, as per a 2024 study published by the National Center for Biotechnology Information (NCBI), 32% of participants exhibited lower adherence, with the device worn on fewer than 4 days within the requested initial 14-day period among 22 participants in the U.S.

SEGMENTATION ANALYSIS

By Product Type

Increasing Development of Wearable Ultrasound Patches Led to Patch-based Segment Dominance

Based on product type, the market segments are patch-based, band/strap-based, and others.

The patch-based segment held the largest revenue share in 2025. The growth is owing to the growing cases of chronic conditions among patients, resulting in a rising number of diagnostic procedures globally. This, along with the increasing focus of prominent players on the launch of novel devices, is further expected to contribute to the global wearable ultrasound devices market growth.

- In November 2024, researchers at the University of California, San Diego, developed a clinically validated, wearable ultrasound patch for continuous blood pressure monitoring.

The band/strap-based segment is projected to grow at a CAGR of 14.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Growing Prevalence of Cardiovascular Disorders Led to Dominance of Cardiovascular Monitoring Segment

Based on application, the market is segmented into cardiovascular monitoring, oncology & tumor monitoring, musculoskeletal monitoring, maternal & fetal monitoring, and others.

The cardiovascular monitoring segment dominated the global market in 2025. By application, the cardiovascular monitoring segment accounted for 35.9% in 2025. The growth is due to the growing prevalence of cardiovascular diseases, resulting in a growing number of ultrasound examinations, thereby contributing to the adoption rate of these products in the market.

- For instance, according to 2025 data published by the British Heart Foundation, 7.6 million people in the U.K. live with heart and circulatory diseases.

The segment of oncology & tumor monitoring is set to flourish with a growth rate of 15.4% across the forecast period.

By End User

Increasing Number of Hospitals & ASCs Led to Segmental Dominance

Based on end user, the market is divided into hospitals & ASCs, specialty clinics, homecare settings, and others.

The hospitals & ASCs segment dominated the market in 2025. The increasing prevalence of chronic conditions, the growing number of hospitals and ambulatory surgical centers, among others, are some of the key factors supporting the growth of the segment in the market. Furthermore, the segment is set to hold a 56.9% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 14.8% CAGR during the forecast period.

Wearable Ultrasound Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Wearable Ultrasound Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 0.51 billion, and also took the leading share in 2025 with USD 0.75 billion. The growing prevalence of chronic diseases, strong clinical trials, and telehealth infrastructure, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2026 statistics published by the Orthopaedic Research Society, musculoskeletal diseases affect more than 1 in 2 people aged 18 and over in the U.S.

U.S. Wearable Ultrasound Devices Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.80 billion in 2026, accounting for roughly 34.8% of global sales.

Europe

Europe is projected to record a growth rate of 13.2% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.63 billion by 2026. The regulatory scrutiny and strong medical technology adoption in countries including Germany, U.K., and Netherlands are anticipated to support the market growth.

U.K. Wearable Ultrasound Devices Market

The U.K. market in 2026 is estimated at around USD 0.12 billion, representing roughly 5.1% of global revenues.

Germany Wearable Ultrasound Devices Market

Germany’s market is projected to reach approximately USD 0.13 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.56 billion in 2026 and secure the position of the third-largest region in the market. The fastest device adoption in portable ultrasound, manufacturing hubs, and a large patient base is expected to support the growth of the market. In the region, India and China are both estimated to reach USD 0.09 billion and USD 0.16 billion, respectively, in 2026.

Japan Wearable Ultrasound Devices Market

The Japan market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 4.7% of global revenues. Japan has historically reported a relatively high prevalence of acute and chronic conditions, with a significant adoption of wearable devices.

China Wearable Ultrasound Devices Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.16 billion, representing roughly 6.8% of global sales.

India Wearable Ultrasound Devices Market

The Indian market size in 2026 is estimated at around USD 0.09 billion, accounting for roughly 4.0% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.12 billion in 2026. The growth is due to the emerging adoption of advanced devices and telemedicine investments in these regions. In the Middle East & Africa, the GCC is set to reach a value of USD 0.05 billion in 2026.

South Africa Wearable Ultrasound Devices Market

The South Africa market is projected to reach around USD 0.02 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches to Support Their Dominance

A robust and diversified product portfolio, along with a significant focus on strategic initiatives globally, is among the key factors supporting the leadership of these companies in the market. In 2025, Flosonics and ClearSens, Inc., are prominent players operating in the industry. Moreover, the growing emphasis of key players on strategic initiatives to increase the adoption of their products is anticipated to enhance their presence, further contributing to the global wearable ultrasound devices market share.

- In June 2025, Flosonics made an announcement that The Mount Sinai Hospital has adopted FloPatch, the first wireless Doppler ultrasound device, in its surgical and transplant intensive care units.

Other key participants, including Sonus Microsystems and others, are also expanding their portfolio in the market, primarily due to their increasing emphasis on acquisitions and collaborations among other players to strengthen their market presence.

List of Key Wearable Ultrasound Devices Companies Profiled

- Flosonics (Canada)

- Sonus Microsystems (Canada)

- ClearSens, Inc. (U.S.)

- MEDIVEL BIO (South Korea)

- NOVOSOUND HEALTH (Scotland)

- Simulab Corporation (U.S.)

- MIT Alliance for Research and Technology (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Researchers from the Massachusetts Institute of Technology, Nanyang Technological University, and the National University of Singapore (NUS) are working together to develop wearable ultrasound stickers that can provide continuous imaging of a patient’s internal organs for up to 48 hours.

- November 2025: The Korea Advanced Institute of Science and Technology (KAIST) developing a flexible ultrasound sensor with statically adjustable curvature.

- July 2025: Sutter Health, an integrated not-for-profit healthcare system, and Flosonics Medical today announced an expansion of the deployment of FloPatch, the first wireless wearable Doppler ultrasound device, across multiple hospital sites to support more precise and timelier intravenous (IV) fluid management.

- April 2025: Sonus Microsystems, a player in innovative ultrasound technology, partnered with Providence Health Care Ventures (PHCV) today, marking the first collaboration in PHCV's Innovation Program. This helped the company to strengthen its market presence.

- March 2025: Flosonics has secured USD 7.5 million CAD in venture debt financing from RBCx. The financing and specialized support will accelerate Flosonics Medical’s mission to improve patient outcomes through non-invasive, data-driven solutions that empower clinicians to make faster, more informed decisions at the bedside.

- March 2024: Novosound developed a wearable, Wi-Fi-enabled ultrasound device that uses gel-free, high-resolution sensors to solve issues associated with traditional ultrasound technology.

- March 2020: Novosound is preparing to launch its first flexible thin-film ultrasound sensor for inspecting curved surfaces, after securing an approximately USD 4.3 million investment in its technology.

REPORT COVERAGE

The report provides a detailed global wearable ultrasound devices market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Application, End User, and Region |

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.96 billion in 2025 and is projected to reach USD 6.76 billion by 2034.

In 2025, the North America regional market value stood at USD 0.75 billion.

Growing at a CAGR of 14.4%, the market will exhibit steady growth over the forecast period.

By product type, the patch-based segment is the leading segment in this market.

The introduction of novel wearable ultrasound devices is one of the major factors driving the markets growth.

Flosonics and ClearSens, Inc., are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions, the increasing number of diagnostic procedures, among others, are some of the crucial factors expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us