Wet Pet Food Market Size, Share & Industry Analysis, By Pet Type (Dogs and Cats), By Source (Animal and Plant), By Price Range (Economy, Medium, and Premium), By Packaging (Pouches, Cans, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Wet Pet Food Stores, Online Channels, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

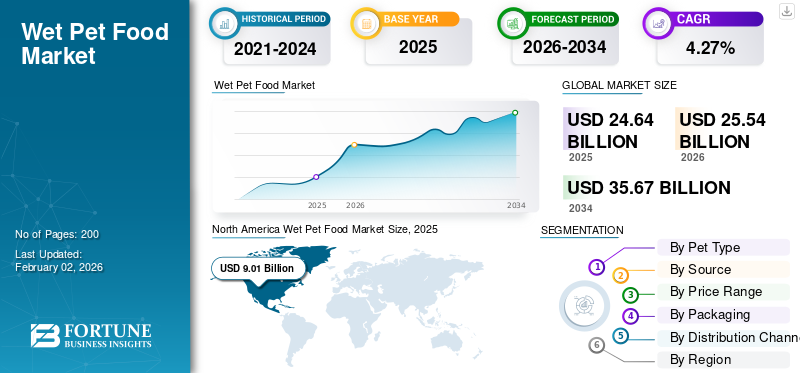

The global wet pet food market size was valued at USD 24.64 billion in 2025. The market is projected to grow from USD 25.54 billion in 2026 to USD 35.67 billion by 2034, exhibiting a CAGR of 4.27% during the forecast period. North America dominated the global wet pet food market, with a 36.57% share in 2025.

Wet pet food, available in pâtés, stews, shredded textures, broths, and gravy-based preparations, is increasingly preferred due to its high palatability, hydration benefits, and suitability for pets with dental or digestive issues. The rising humanization of pets, growing adoption of premium and functional formulations, and the increasing shift toward moisture-rich diets for cats and dogs are the major forces accelerating global demand. Wet food is particularly gaining traction in urban markets where owners prioritize convenience, portion control, and enhanced taste appeal.

Large multinational pet food manufacturers such as Nestlé Purina PetCare, Mars Petcare, Hill’s Pet Nutrition, General Mills, and The J.M. Smucker Company dominate the market. These companies are leveraging advanced processing capabilities, strong brand equity, and global distribution networks.

Download Free sample to learn more about this report.

Wet Pet Food Market Key Takeaways

- 2025 Market Size: USD 24.64 billion

- 2026 Market Size: USD 25.54 billion

- 2034 Forecast Market Size: USD 35.67 billion

- CAGR: 4.27% from 2026–2034

- North America dominated the global wet pet food market with a market share of 36.57% in 2025.

- The dogs segment held the dominant position in the global market, capturing 55.63% share by pet type in 2025.

- The animal-based segment accounted for a 74.39% share of the global market in 2025.

North America

North America generated USD 9.01 billion in revenue in 2025, supported by strong premiumization trends and growing adoption of veterinarian-recommended wet pet food products.

Europe

Europe reached USD 8.41 billion in 2025, driven by high pet ownership rates, premium product demand, and stringent pet nutrition standards.

Asia Pacific

Asia Pacific recorded a market size of USD 5.36 billion in 2025, benefiting from rising pet ownership and expanding e-commerce channels for premium pet food products.

U.S.

The market is supported by high consumer spending on pet care, increasing demand for premium nutrition, and widespread availability of specialized wet pet food products.

Japan

Growing pet humanization trends and demand for high-quality, nutritionally balanced pet food continue to support market growth in the country.

Read More

MARKET DYNAMICS

Market Drivers

Rising Cat Ownership and Increasing Shift toward Moisture-Rich Diets to Accelerate Market Growth

Rising cat ownership and the strong shift toward moisture‑rich, health‑positioned diets are emerging as two of the most powerful structural drivers for global market demand, particularly in the cat segment. As this cat base expands, owners report dissatisfaction with traditional dry‑only options and are actively seeking more varied, fresh‑like, and functional wet formats targeting the pets’ urinary health, weight management, life‑stage nutrition, and other specific needs. This is prompting manufacturers to broaden wet portfolios such as pâtés, gravies, broths, toppers, pouches, and to position them as core, not just occasional, feeding choices.

- According to the European Pet Food Industry, in 2024, Europe had 129 million cats, surpassing dogs, which were 106 million. This marked a shift where cats have become the leading pet, surpassing dogs in total numbers across the continent, with a significant rise in feline ownership in recent years.

Market Restraints

High Production & Packaging Costs to Limit Price Competitiveness

High pet food production and packaging costs are eroding price competitiveness, which is acting as a structural restraint on the global wet pet food market growth even as growing demand fundamentals remain positive. Cost pressures are particularly acute in premium and sustainable formats that rely on high-quality ingredients and complex, resource‑intensive packaging. Wet pet food is more expensive to manufacture than dry pet food as it uses higher-moisture formulations, more animal-based ingredients, and heat-intensive sterilization processes, all of which increase energy and equipment costs.

- According to the Pet Food Industry, from late 2018 to late 2025, the U.S. pet food Producer Price Index (PPI) climbed by roughly 34%, while the Consumer Price Index (CPI) for retail-level pet food prices rose about 27%. This steeper increase at the producer level reflects higher costs for labor, energy, packaging, and key ingredients such as animal proteins and grains, forcing manufacturers to manage significant margin pressure or raise shelf prices.

Market Opportunities

Expansion of Online Retail and Subscription-Based Wet Food Services to Unlock New Growth Opportunities

Online channels are the fastest-growing distribution segment in the market, fueled by e-commerce surges post-pandemic and consumer shifts toward convenience. The subscription models for wet pet food are emerging as key opportunities, offering personalized, recurring deliveries of fresh, and premium products to busy owners. Innovations such as tailored premium nutrition and auto-ship options boost retention, particularly for wet formats with limited shelf life.

- According to the Pet Food Industry and Packaged Facts' September 2025 survey, 27% of U.S. consumers use subscriptions for everyday items such as groceries, pet food, and household goods, highlighting a significant trend toward convenience and regular, scheduled deliveries in the e-commerce market.

Wet Pet Food Market Trends

Rising Popularity of Single-Serve Pouches

The mounting popularity of single-serve pouches is a prominent trend in the global market, driven by the consumer demand for convenience, portion control, freshness, and suitability for busy lifestyles and pet travel. This packaging format addresses key challenges such as limited shelf life in wet foods while aligning with pet humanization trends, where owners prioritize premium, grab-and-go options that reduce waste and ensure palatability. Manufacturers are also launching innovative products to meet the rising demand.

- For instance, in February 2025, Fancy Feast, a Purina brand, launched Gems, as a chef-inspired wet cat food featuring single-serve 2oz pyramid-shaped pouches (tubs) of delicate mousse paté topped with cascading savory gravy. This innovative product targets adult cats with 100% complete and balanced nutrition in beef, chicken, tuna, or salmon flavors.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Pet Type

Preference for High Moisture and Wet Palatable Foods to Drive Dogs Segment Dominance

By pet type, the market is segmented into dogs and cats.

The dogs segment held the dominant position in the global market, capturing 55.63% share by pet type in 2025. This leadership stems from higher global dog ownership, as well as dogs' greater caloric needs. Another factor influencing segment is the owners' preference for moisture-rich, palatable wet formats supporting hydration, digestion, and weight management.

The cat segment is expected to grow significantly with a CAGR of 4.58% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Source

Animal Segment Led the Market Due to Superior Nutrition and Palatability

On the basis of source, the market is segmented into animal and plant.

The animal-based segment held a 74.39% market share globally in 2025, driven by consumer trust in their superior nutrition, palatability, and alignment with carnivorous pet diets. This dominance stems from the high demand for recipes featuring real meat chunks, organ meats such as liver and kidney, and elevated protein levels that support muscle health, hydration, and digestibility.

As alternative protein adoption increases in urban markets, the plant-based segment is poised to grow modestly at a CAGR of 4.48% over the analysis period.

By Price Range

Medium Segment Leads the Global Market Share Due to Quality and Affordability

On the basis of price range, the market is segmented into economy, medium, and premium.

In terms of price range, the medium segment accounted for a major wet pet food market share of 43.61% in 2025 and will grow at a high CAGR of 4.85% over the forecast period. Medium price range pet food products dominate the global market due to their appeal to price-conscious mass-market consumers seeking balanced quality and affordability.

The premium segment is anticipated to grow at a CAGR of 3.90% during the forecast period.

By Packaging

Cans Segment Dominated the Market with Benefits of Durability, Protection, and Long Shelf

On the basis of packaging, the market is segmented into pouches, cans, and others.

The cans segment held a dominant share of 45.11% in the market in 2025, due to their proven reliability and consumer familiarity. Cans offer robust protection against light, air, and moisture, ensuring product integrity through the supply chain with minimal damage. Their rigid structure withstands high-pressure retort sterilization, preserving nutritional quality in protein-rich formats such as pâtés and chunks. Cans provide extended shelf life via airtight seals and sterilization, eliminating the need for preservatives and maintaining freshness and flavor. This reliability supports cost-effective, value-driven feeding for mainstream consumers.

The pouches segment is anticipated to grow at a CAGR of 4.59% during the forecast period.

By Distribution Channel

Broader Reach and Promotional Offers to Fuel Supermarkets/Hypermarkets Segment’s Leadership

On the basis of distribution channel, the market is segmented into supermarkets/hypermarkets, specialty pet food stores, online channels, and others.

The supermarkets and hypermarkets segment leads due to economies of scale, broad customer reach, and diverse revenue options that support wide product assortments. They offer competitive pricing, a wide variety, promotional schemes, and assured product freshness, making them highly convenient for consumers seeking canned and pouched formats. The segment held around 45.67% market share in 2025 for wet pet food distribution, outpacing others, such as online or specialty stores.

The online channels segment is anticipated to grow at a CAGR of 5.16% during the forecast period.

Wet Pet Food Market Regional Outlook

Regionally, the report covers the market analysis across North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

North America

North America Wet Pet Food Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North American market held the largest market share of 36.56% in 2025. High premiumization and vet-prescribed wet pet food industry in the region align with broader trends. High disposable incomes in North America enable premium spending, with pet owners treating pets as family members and prioritizing nutritious wet formats over dry kibble. The strong adoption of vet-recommended diets reflects a heightened awareness of tailored nutrition for conditions such as digestive issues, boosted by e-commerce access to these products.

Europe

Europe's market reached USD 8.41 billion in 2025, with growth fueled by high pet ownership rates, demand for premium products, and adherence to FEDIAF's strict nutritional and safety guidelines on ingredients, formulation, and labeling. The product demand surges for sustainable innovations such as recyclable flexible pouches made from polypropylene, pioneered by brands such as Nestlé Purina's Felix line, aligning with Europe's zero-waste and circular economy initiatives.

Asia Pacific

Asia Pacific market reached around USD 5.36 billion in 2025, aligning closely with the stated USD 5.66 billion trajectory for 2026. The regional growth is propelled by surging pet ownership in urban China, Japan, and South Korea, alongside e-commerce and retail expansions facilitating imported premium products.

South America

The South America market reached USD 1.32 billion in 2025, with Brazil dominating due to rising pet ownership and investments in premium production facilities amid economic recovery in Brazil and Argentina. Brazil leads with 58.00% regional pet food share, driven by e-commerce via MercadoLibre and veterinary endorsements for wet diets addressing dental and hydration issues.

Middle East & Africa

The Middle East & Africa market remains nascent and is expected to grow at a CAGR of 3.15% over the forecast period. The regional market growth is accelerating from urban pet ownership in the UAE, Saudi Arabia, and South Africa, alongside the demand for imported premium wet products offering high moisture and palatability.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Support Market Growth

The market exhibits moderate consolidation, dominated by multinationals such as Nestlé Purina PetCare, Mars Petcare, Colgate-Palmolive (Hill's), General Mills, J.M. Smucker, and Unicharm, leveraging global manufacturing scale and R&D investments. Companies prioritize high-meat recipes, e.g., Chicken Soup for the Soul's Cuts in Gravy with real beef/turkey, functional diets for weight management (Royal Canin Appetite Control), and veterinary lines such as SquarePet VFS for digestion/skin support, alongside palatable enhancements via emulsions and fibers.

Key Players in the Wet Pet Food Market

|

Rank |

Company Name |

|

1 |

Nestlé Purina PetCare |

|

2 |

Mars Petcare |

|

3 |

Colgate-Palmolive (Hill's) |

|

4 |

General Mills |

|

5 |

J.M. Smucker |

List of Key Wet Pet Food Companies Profiled

- Nestlé S.A. (Switzerland)

- Mars, Incorporated (U.S.)

- Hill’s Pet Nutrition (U.S.)

- General Mills (U.S.)

- The J.M. Smucker Company (U.S.)

- WellPet LLC (U.S.)

- Unicharm Corporation (Japan)

- Diamond Pet Foods (U.S.)

- Deuerer Group (Germany)

- Affinia Petcare (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Mankind Pharma launched PetStar Delight, a wet cat food range. The new range targets kittens (1-12 months) and adult cats with tailored nutrition: 32% protein and 12% fat for kittens; and 30% protein and 10% fat for adults.

- August 2025: Wellness Pet Company launched over 20 new wet cat food products at SUPERZOO 2025 in the U.S. The move helped the company expand its portfolio to 93 varieties focused on hydration, texture variety, and unique proteins such as lamb, shrimp, and egg.

- July 2025: Natures Menu, a U.K.-based natural pet food company, launched its full cat range in mid-2025, expanding from dog-focused products to include redesigned wet foods, treats, and new dry options for adult cats and kittens.

- May 2025: Post Consumer Brands, a subsidiary of Post Holdings, launched seven new pet food products across its brands, including 9Lives, Kibbles ‘n Bits, Nature’s Recipe, and Nutrish, targeting kittens, adult dogs, large breeds, and cats with specialized nutrition. These include dry, wet, and freeze-dried options emphasizing real meat ingredients, complete nutrition, and health benefits such as immune support and digestion.

- February 2025: Reveal Pet Food expanded its cat nutrition portfolio by launching Reveal Entrées, a premium wet cat food line, and two new lickable treats. Reveal Entrées feature four paté recipes, including chicken breast, tuna fillet with mackerel, tuna fillet with salmon, and tuna fillet, plus a fish selection variety pack.

REPORT COVERAGE

The global industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market growth dynamics, prominent companies, investment in research and development, and end-use. Besides this, the market research report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.27% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Pet Type

|

|

By Source · Animal · Plant |

|

|

By Price Range

|

|

|

By Packaging · Pouches · Cans · Others |

|

|

By Distribution Channel · Supermarkets/Hypermarkets · Specialty Wet Pet Food Stores · Online Channels · Others |

|

|

By Region · North America (By Pet Type, Source, Price Range, Packaging, Distribution Channel, and Country) • U.S. (By Pet Type) • Canada (By Pet Type) • Mexico (By Pet Type) · Europe (By Pet Type, Source, Price Range, Packaging, Distribution Channel, and Country) • Germany (By Pet Type) • Spain (By Pet Type) • Italy (By Pet Type) • France (By Pet Type) • U.K. (By Pet Type) • Rest of Europe (By Pet Type) · Asia Pacific (By Pet Type, Source, Price Range, Packaging, Distribution Channel, and Country) • China (By Pet Type) • Japan (By Pet Type) • India (By Pet Type) • Australia (By Pet Type) • Rest of Asia Pacific (By Pet Type) · South America (By Pet Type, Source, Price Range, Packaging, Distribution Channel, and Country) • Brazil (By Pet Type) • Argentina (By Pet Type) • Rest of South America (By Pet Type) · Middle East & Africa (By Pet Type, Source, Price Range, Packaging, Distribution Channel, and Country) • South Africa (By Pet Type) • UAE (By Pet Type) • Rest of the Middle East & Africa (By Pet Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 24.64 billion in 2025 and is anticipated to reach USD 35.67 billion by 2034.

The global market will exhibit steady growth at a CAGR of 4.27% over the forecast period.

By pet type, the dogs segment leads the market in 2025.

North America held the largest market share in 2025.

Rising cat ownership and increasing shift toward moisture-rich diets is a key factor driving the market growth.

Nestle Purina PetCare, Mars Petcare, Hill’s Pet Nutrition, General Mills, and The J.M. Smucker Company are the leading companies in the market.

The rising popularity of single-serve pouches is a key trend in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us