Wind Power Fastener Market Size, Share & Industry Analysis, By Material (Carbon Steel, Stainless Steel, and Others), By Application (Turbine Bases, Tower Constructions, Turbine Blades, Nacelle, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

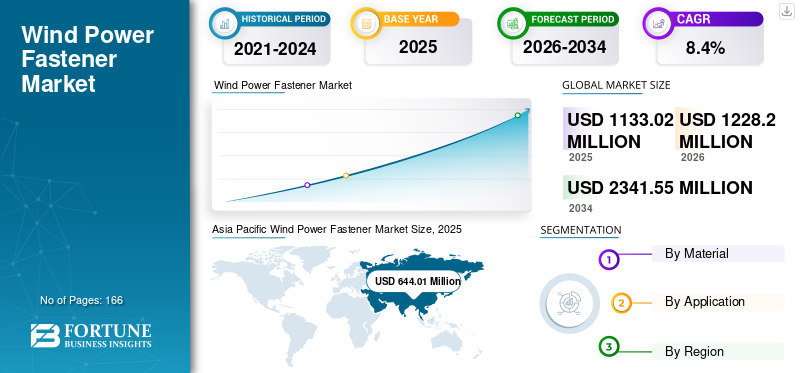

The global wind power fastener market size was valued at USD 1133.02 million in 2025. The market is projected to grow from USD 1228.20 million in 2026 to USD 2341.55 million by 2034, exhibiting a CAGR of 8.40% during the forecast period. Asia Pacific dominated the wind power fastener market with a market share of 56.84% in 2025.

A wind power fastener refers to any hardware or component used in the construction, maintenance, or assembly of wind turbines. These fasteners are essential for securing various parts of a wind turbine, such as the blades, tower, nacelle, and other components. They come in various shapes and sizes, including bolts, nuts, screws, anchors, and specialized fasteners designed to withstand wind turbines' unique stresses and environmental conditions. Properly selected and installed wind power fasteners are crucial for ensuring wind energy systems' safety, stability, and efficiency.

Download Free sample to learn more about this report.

Wind Power Fastener Market Trends

Trend of Floating Wind Power Projects Might Drive the Product Demand in the Coming Years

Wind power is sturdier and more productive in the ocean than on land; therefore, the development of offshore wind in recent years has observed an increase in several regions. Many governments around the world are implementing policies and offering incentives to promote renewable energy, including offshore wind. Subsidies, tax incentives, and favorable regulatory frameworks encourage investment in offshore wind projects.

Moreover, floating structures offer new opportunities and alternatives rather than fixed structures. Typically, it opens the chance to offshore sites by allowing the placement of wind turbines in larger and deeper offshore areas with higher wind potential. As this concept is trending all over the countries with a sea area attached, wind fasteners will also find an opportunity to enter this market.

For instance, in August 2023, the world’s largest floating wind farm was officially launched off the west coast of Norway. ‘Equinor,’ a petroleum refining company, is behind the huge Hywind Tampern farm. With 88 megawatts (MW) of capacity, it will generate energy to supply close oil and gas platforms. In addition, this project will use a new technology to connect 11 giant turbines to the seafloor, which has received mixed reactions from environmentalists.

Download Free sample to learn more about this report.

Wind Power Fastener Market Growth Factors

Increased Investment in the Wind Energy Sector to Propel Market Growth

Increased investment in the wind power sector plays a crucial role in several ways, boosting the market growth of wind power fasteners. Higher investments in wind power lead to the construction of more wind farms and the expansion of existing ones. This requires a substantial quantity of products for securing various components such as blades, towers, and nacelles. Increased investment often drives research and development efforts in the wind power sector. This can lead to the development of more efficient wind turbines, which may require specialized fasteners designed for improved performance and longevity.

For instance, according to the International Energy Agency, total investments in wind generation reached to about USD 185 billion in 2022 reflecting a surge of around 20% from the previous year, rebounding to growth after a slowdown in 2021 and resulting in anticipation of considerable capacity deployment in 2023. This is due to policy support and ambitious government targets.

Growing Number of Large Wind Power Projects to Drive Market Growth

All over the world, wind farms with almost implausible capacity are growing out of the land and sea. This requires stability in a harsh environment, where fasteners play an essential role by delivering several advantages.

Some gigantic wind projects globally are Jiuquan Wind Power Base/Gansu Wind Farm, China, Dogger Bank Wind Farm, U.K., the Jaisalmer Wind Park, India, Alta Wind Energy Center/Mojave Wind Farm, U.S., and others. These projects required large wind fasteners that could match their capability. Such fasteners are typically modified for the particular turbine, which drives the global market growth for wind power fasteners.

For instance, in January 2022, MidAmerican Energy, planned a USD 3.9 billion project named Wind Prime for the Iowa Utilities Board. This project comprises wind and solar farms, which will generate 2,042 MW of energy by wind and an additional 50 MW through solar. If permitted, construction could be finalized by late 2024, and it would become the biggest wind farm in the U.S.

RESTRAINING FACTORS

High Installation Cost of Wind Energy Infrastructure May Hinder Market Growth

When wind farm developers and operators have to allocate a vital portion of their budget to the expensive wind turbine infrastructure, they may have limited funds left for other components, such as fasteners. This can slow down the adoption of wind power fasteners. In addition, wind energy projects often have longer payback periods due to high initial costs. This can deter investors and project developers from prioritizing investments in specialized components, such as fasteners, which may not offer immediate returns. High upfront infrastructure costs may lead to a conservative approach in adopting new wind power fastener technologies. Developers may be hesitant to invest in innovative and expensive fasteners when traditional options are cheaper, which can stifle innovation in the market. The pressure to reduce overall project costs in the face of expensive infrastructure can lead to a focus on cost-cutting measures, potentially sacrificing quality and innovation in fasteners in favor of cheaper alternatives. In addition, as per the Office of Energy Efficiency & Renewable Energy of the U.S., wind energy faces competition in the current scenario owing to the alternatives available for clean energy production, such as solar power. Moreover, when comparing the energy costs associated with new power plants, solar and wind projects are now more economically competitive than gas, geothermal, coal, or nuclear facilities.

Segmentation Analysis

By Material Analysis

Carbon Steel Segment holds a Dominant Market Share Owing to its Physical Properties, Giving Strength and Durability for Better Performance

Based on material, the market is segmented into stainless steel, carbon steel, and others.

Carbon steel holds a major share of the market due to its excellent strength and durability. Wind power fasteners need to withstand significant stresses, especially in the harsh operating conditions of wind turbines. Carbon steel provides the necessary strength and reliability.

Stainless steel, especially corrosion-resistant grades such as austenitic stainless steel, is projected to grow steadily due to its escalating use in product manufacturing. It provides exceptional corrosion resistance, essential for fasteners subjected to challenging outdoor environments in wind turbines.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Turbine Blades Dominate as Blades are Becoming More Developed, Resulting in More Requirements for Fasteners

By application, the market has been broadly categorized into turbine bases, tower constructions, turbine blades, nacelle, and others.

The turbine bases segment is projected to dominate the market with a share of 8.75% in 2026, as turbine blades are likely to require many fasteners during the forecast period persistently. As wind turbine technology evolves to enhance efficiency and energy capture, blades might become more developed, resulting in more requirements for fasteners.

For instance, Siemens Gamesa reestablished a strong command of circularity within wind turbine blades and inaugurated its recyclable blade for onshore wind projects. This achievement is set to drive the activities that make wind energy even more eco-friendly, creating a fully circular sector. The Siemens Gamesa Recyclable Blade for offshore was brought to market within ten months: launched in September 2021 and deployed at RWE’s Kaskasi project in Germany in July 2022. Further development by Siemens Gamesa and its allies guarantees full compatibility with the product and process requirements for onshore blades.

The fasteners demand in nacelle applications is substantial. The nacelle houses numerous critical wind turbine components, comprising the gearbox, generator, and others. Fasteners are utilized in the building and servicing of nacelles.

REGIONAL ANALYSIS

By region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Wind Power Fastener Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accumulates the major share of the market as the demand for fasteners is high in the region due to the high number of installations. China is the major country in the onshore and offshore wind power installations in the world. Fasteners play a significant role in the building, servicing, and reliability of wind turbines, and their demand is strictly tied to the growth of wind energy projects.

Europe

Europe is also one of the significant regions active in the market. Germany and France are some of the major markets for wind power. With adding a record 19.1 GW (16.7 GW onshore and 2.5 GW offshore) installations in 2022, Europe has contributed significantly in the growth of the wind power fastener market.

North America

North America is also one of the key regions in the market. For instance, in total, 60 G.W. of onshore wind capacity is anticipated to be deployed in North America in the next five years, of which the majority will be installed in the U.S.

Latin America

The wind power fastener is an important market for the Latin America region as its vast coastal areas, robust winds, and favorable climatic conditions can help the region become a main wind energy powerhouse in the decades to come.

Latin America's offshore wind energy sector recorded a steady growth in 2022 as per the Global Wind Energy Council (GWEC). New installations in this region reached 5.2 GW, marking the second-highest installation rate in history. Having become Latin America’s acknowledged wind energy market leader over the past decade, with over 50% of the region’s installed wind capacity, Brazil achieved its position in 2022. In recent years, this boosted the demand for wind power fasteners as installation required sturdy nuts and bolts, which can endure harsh environments.

List of Key Wind Power Fastener Market Companies

Finework New Energy Technology Dominates the Market Due to its Expertise in the Product

Finework New Energy Technology is one of the major companies in the wind power fastener market. Its embedded screws used in wind turbines have gained traction in recent years. It also focuses on the research, development, and manufacturing processes of high-end fasteners.

For instance, in June 2022, Dongfang Electric Wind Turbine Blade Engineering Co., Ltd. awarded Finework New Energy Technology the ‘2021 Quality Outstanding Supplier Award’, which provides clients with high-strength fasteners for wind power blades.

LIST OF KEY COMPANIES PROFILED:

- Dokka Fasteners (U.K.)

- Beck Industries (France)

- Finework New Energy Technology (China)

- Ningbo Datian Fastener Co., Ltd (China)

- Berdan Civata (Turkey)

- Sundram Fasteners (India)

- Clyde Fasteners Limited (Scotland)

- ITH Bolting Technology (Germany)

- All-Pro Fasteners (U.S.)

- Big Bolt Nut (India)

KEY INDUSTRY DEVELOPMENTS:

- November 2022: Sundram Fasteners, an auto component company from the stable of TVS Group, announced that it is targeting to earn 50% of its revenue from export operations. The company has also been assertive in its non-auto business, such as energy, wind, and others.

- October 2022: Zhongfu Lianzhong rattled off the world's longest wind turbine blade, which is 62 tons and 123 meters long. It was successfully transported to the test site in Lianyungang for trial assemblage. It is worth stating that the embedded bolt sleeve fasteners for the world's longest wind turbine blade are all supplied by FNET (Finework New Energy Technology).

- May 2022: Millions of investments by Berdan Cıvata were observed for hot forging presses for its bolt and nut manufacturing facilities – where it can now produce bolts and nuts up to M155 (6 inches) diameters. In addition, the company developed a new facility to produce its forge molds and rolling dies for threading.

- January 2022: Norway’s Dokka Fasteners, a globally prominent industrial fasteners producer, announced that it is expanding its European operations and plans to establish a manufacturing unit in Klaipėda.

- December 2021: Finework New Energy Technology won the title of ‘Top 100 Hunan Manufacturing Enterprises’. This Hunan Entrepreneur Activity Day and Entrepreneur Annual Meeting was held in Changsha.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product/service types, and leading applications of the product. Besides this, it offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.40% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material, Application, and Region |

|

Segmentation |

By Material

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

A study by Fortune Business Insights states that the global market was valued at USD 1133.02 million in 2025.

The global market is projected to grow at a CAGR of 8.40% over the forecast period.

Asia Pacific market size stood at USD 644.01 million in 2025.

Based on application, the turbine blades segment dominates the global market.

The global market size is expected to reach USD 2341.55 million by 2034.

The increased investment in the wind power sector is propelling market growth.

Finework New Energy Technology and Dokka Fasteners are some of the top players actively operating across the market.

- 2021-2034

- 2025

- 2021-2024

- 166

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us