Wind Turbine Inspection Drones Market Size, Share & Industry Analysis, By End User (Wind Farm Operators, Drone Service Providers, and Original Equipment Manufacturers), By Payload (Camera, Thermal Camera, and Ultrasonic Sensor), By Autonomy Level (Remotely Piloted, Semi-Autonomous, and Autonomous), By Inspection Type (Visual Inspection, Thermal Inspection, and Ultrasonic Inspection), By Application (Onshore Wind Turbines and Offshore Wind Turbines), and Regional Forecast, 2026-2034

Wind Turbine Inspection Drones Market Size and Future Outlook

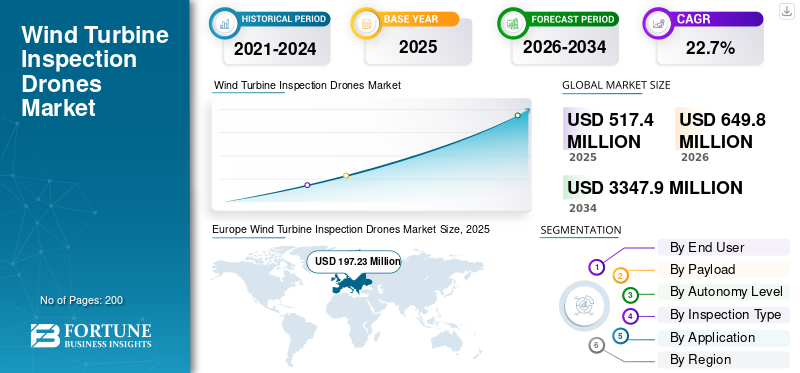

The global wind turbine inspection drones market size was valued at USD 517.4 million in 2025. The market is projected to grow from USD 649.8 million in 2026 to USD 3,347.9 million by 2034, exhibiting a CAGR of 22.7% during the forecast period. Europe dominated the wind turbine inspection drones market, with a market share of 38.11% in 2025.

Wind turbine inspection drones enhance maintenance efficiency for wind energy assets by deploying aerial robotics equipped with high-resolution cameras, thermal imaging, LiDAR, and AI-driven analytics to assess blades, towers, nacelles, and hubs without halting operations. This market addresses challenges associated with traditional rope-access or crane-based inspections, which are labor-intensive, hazardous, and weather-dependent, especially for tall onshore and remote offshore turbines. Drones enable georeferenced 3D modeling, real-time defect detection (such as cracks, erosion, or lightning damage), and predictive maintenance through data integration with SCADA systems.

Key players include SZ DJI Technology Co., Ltd., a leader in multirotor drone platforms with advanced imaging sensors; SkySpecs, Inc., which specializes in AI-driven automation and digital twins solutions for fleet inspections. Cyberhawk Innovations Limited excels in offshore BVLOS operations with rugged VTOL platforms. Raptor Maps, Inc. offers end-to-end analytics software for defect classification. Drone Volt SA provides integrated hardware-software for European wind farms.

Download Free sample to learn more about this report.

Wind Turbine Inspection Drones Market Takeaways

- 2025 Market Size: USD 517.4 million

- 2026 Market Size: USD 649.8 million

- 2034 Forecast Market Size: USD 3,347.9 million

- CAGR: 22.7% from 2026–2034

- Europe dominated the wind turbine inspection drones market with a 38.11% share in 2025.

- The drone service providers segment is projected to grow at a CAGR of 23.7% during the forecast period.

- The autonomous segment is anticipated to expand at a CAGR of 24.6% through 2034.

North America

North America is projected to attain USD 107.9 million in 2026, supported by increasing investments in wind farm maintenance and digital inspection technologies.

Europe

Europe led the global market with a valuation of USD 197.23 million in 2025, supported by extensive offshore wind installations and advanced renewable energy infrastructure.

Asia Pacific

Asia Pacific is expected to reach USD 212.5 million in 2026, registering a CAGR of 23.5%, driven by rapid wind energy capacity expansion across major economies.

U.S.

The market is estimated to reach USD 116.5 million by 2026, accounting for approximately 21.9% of global sales.

Japan

The market is projected to reach USD 27.5 million by 2026, growing at a CAGR of 23.1% during the forecast period.

Read More

WIND TURBINE INSPECTION DRONES MARKET TRENDS

Shift to VTOL Drones is the Latest Trend in the Market

The shift to VTOL drones and AI-driven analytics enables autonomous flights and instant flaw detection. Integration of 5G and edge computing supports live data processing, while digital twin technology enhances inspections through simulations. Service models such as inspection-as-a-service gain traction, standardizing workflows and accelerating the transition from manual inspection methods through tech-led approaches.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Wind Energy Capacity Fuels Demand for the Product

The global expansion of wind energy capacity is increasing turbine fleets, driving the adoption of drone-based inspections adoption to minimize manual risks associated with tall structures and offshore sites. Drones deliver faster and more detailed imaging using thermal and LiDAR sensors, supporting predictive maintenance. Cost savings resulting from reduced downtime and lower labor requirements, combined with regulatory emphasis on renewable energy deployment, are accelerating market integration. Operators also benefit from real-time data insights that enhance asset management and enhance turbine reliability, particularly in harsh environments.

MARKET RESTRAINTS

Elevated Costs for Specialized Drones to Limit Market Growth

High upfront expenses for specialized drones, advanced sensors, and workforce training pose significant barriers, especially for smaller operators. Stringent and regionally varying aviation regulations further complicate deployment and certification processes. Supply chain issues affecting critical components increase operational expenses, while reliance on certified and skilled operators limits scalability.

MARKET OPPORTUNITIES

Rapid Offshore Wind Development to Present Several Opportunities in the Market

Rapid offshore wind development is driving demand for rugged, long-endurance drones capable of conducting inspections in remote inspections. BVLOS approvals and AI-enabled autonomy are expanding operational coverage across large wind farm sites. Collaborations between drone providers and turbine OEMs are fostering integrated inspection and maintenance solutions. Emerging markets and subscription-based service models are targeting underserved turbine fleets, leveraging predictive analytics technologies to support long-term maintenance contracts.

MARKET CHALLENGES

Harsh Conditions and Visual-Line-of-Sight Limitations Present Operational Challenges

Extreme weather conditions, turbine interference, and visual-line-of-sight limitations present operational challenges, particularly in offshore environments. Achieving precise data capture in turbulent wind conditions requires advanced stability and sensors. Additionally, cybersecurity risk associated with connected inspection platforms and skilled workforce shortages adds hurdles. Adapting to diverse regulatory landscapes across regions adds complexity to achieving reliable and widespread use of drone-based inspection solutions.

Segmentation Analysis

By End User

Wind Farm Operators Segment Dominated due to its Ability to Maintain Data Quality

Based on end user, the market is segmented into wind farm operators, drone service providers, and original equipment manufacturers.

The wind farm operators segment is anticipated to account for the largest market share. Growth is driven by operators increasingly bringing inspection activities in-house to reduce downtime, maintain control data quality, and standardize maintenance decisions across turbine fleets. Demand is expected to strengthen further as turbine fleets age and post-warranty maintenance budgets become more constrained.

The drone service providers segment is anticipated to rise with a CAGR of 23.7% over the forecast period.

By Payload

Cameras Segment Led due to Cost-Effective Blade Surface Coverage

Based on payload, the market is segmented into camera, thermal camera, and ultrasonic sensor.

In 2025, the camera segment dominated the global market. Demand remains highest for standard optical cameras, as they deliver fast, cost-effective blade surface coverage and strong visual documentation. They’re the strong payload for routine inspections, warranty checks, and contractor verification activities.

The ultrasonic sensor segment is projected to grow at a CAGR of 24.0% over the forecast period.

By Autonomy Level

Remotely Piloted Segment to Dominate as They Align Well with Existing Operational Workflows

Based on autonomy level, the market is segmented into remotely piloted, semi-autonomous, and autonomous.

The remotely piloted segment is anticipated to witness a dominant market share over the forecast period. Demand stays strong as remotely piloted drones are easier to certify, deploy, and insure, especially under restrictive flight rules. They align well with existing operational workflows and dominate high-frequency, multi-site inspection programs.

The autonomous segment is projected to grow at a high CAGR of 24.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Inspection Type

Visual Inspection Segment Led the Market due to the Need for Rapid Defect Triage

Based on inspection type, the market is segmented into visual inspection, thermal inspection, and ultrasonic inspection.

The visual inspection segment dominated the market. Demand is anchored by visual inspections as the first-line diagnostic for leading-edge erosion, cracks, lightning damage, and contamination. Operators use it to triage issues quickly before ordering deeper thermal or NDT checks.

The thermal inspection segment is projected to grow at a CAGR of 22.8% during the study period.

By Application

Onshore Wind Turbines Segment Led, Driven by the Frequent Inspection Cycles

Based on application, the market is segmented into onshore wind turbines and offshore wind turbines.

The onshore wind turbines segment dominated the market due to sheer turbine volumes and frequent inspection cycles. Remote site locations and ongoing technician shortages are increasing reliance on drones-based inspections to cut climbing risks and keep O&M costs predictable.

The offshore wind turbines segment is projected to grow at a CAGR of 23.5% during the study period.

Wind Turbine Inspection Drones Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Europe

Europe Wind Turbine Inspection Drones Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2024, valued at USD 160.6 million, and also maintained the leading share in 2025, with USD 197.23 million. Demand is strong in regions with high offshore wind density, where access and maintenance costs are substantial. Operators prioritize repeatable inspection quality and standardized digital records to optimize asset management. Although regulation frameworks are complex, Europe’s mature service ecosystems support accelerated adoption.

U.K. Wind Turbine Inspection Drones Market

The U.K. market is estimated to reach around USD 39.1 million in 2026, representing a roughly 22.4% CAGR of global sales. Growth is primarily driven by offshore wind capacity, where vessel logistics constraints and narrow weather windows increase the value proposition of drone-based inspections. Operators are increasingly implementing routine blade health programs, integrating drone-captured data with advanced analytics platforms to enhance predictive maintenance planning.

Germany Wind Turbine Inspection Drones Market

Germany’s market is projected to reach approximately USD 42.8 million by 2026. Demand is driven by a dense onshore turbine base and a strong safety culture. Operators use drones to reduce climbing risk and improve documentation. While growth remains steady, fragmented asset ownership slows uniform nationwide standardization.

North America

North America is estimated to reach USD 107.9 million by 2026, ranking as the third-largest regional market. Demand is supported by aging onshore fleets, increased focus on O&M cost optimization, and higher safety standards. Although permitting complexities and BVLOS rules present constraints, utility-scale operators are progressively standardizing drone-led inspection workflows.

U.S. Wind Turbine Inspection Drones Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 116.5 million in 2026, accounting for roughly 21.9% of global sales. Demand is propelled by large onshore fleets, warranty-to-post-warranty transitions, and pressure to cut downtime. Service providers scale standardized inspection programs, while BVLOS approvals and utility procurement cycles continue to influence adoption rates.

Asia Pacific

Asia Pacific is projected to record a growth rate of 23.5% during the forecast period, the second-highest among all regions, reaching an estimated valuation of USD 212.5 million by 2026. Demand is expanding fastest as massive installed bases require scalable blade health monitoring. Cost sensitivity in several markets favors outsourced drone services and semi-autonomous inspection models. Additionally, strong local manufacturing capabilities and rapid renewables energy inspection are sustaining high inspection volumes.

Japan Wind Turbine Inspection Drones Market

Japan’s market is estimated to reach around USD 27.5 million by 2026, registering a CAGR of 23.1% during the forecast period. Demand is rising due to high typhoon exposure, corrosion risk in coastal regions, and growing offshore ambitions. Operators value high-quality defect detection and traceability. Regulatory rigor and limited service capacity keep growth measured but consistent.

China Wind Turbine Inspection Drones Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 131.5 million. Demand is expanding rapidly, supported by the world’s largest installed turbine base and aggressive O&M efficiency targets. Strong domestic drone and sensor manufacturing capabilities are accelerating deployment, with inspection frequency rising across large utility-scale portfolios.

India Wind Turbine Inspection Drones Market

The India market is estimated to reach around USD 30.5 million by 2026. Growth is driven by expanding wind capacity and rising cost pressures to minimize downtime, particularly at remote project sites. Outsourced drone inspections are gaining traction; however, workforce training, challenging terrain conditions, and the need for standardized operational frameworks remain practical constraints to faster scaling.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 24.2 million and USD 30.0 million, respectively, in 2026. The Middle East & Africa represent roughly 20.3% CAGR of global sales. Demand is emerging around large wind corridors in Latin America, MEA, and parts of Oceania. Adoption is driven by limited technician availability and the prevalence of remote wind sites, where market maturity varies significantly across countries, leading to uneven adoption rates.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Ruggedization to Secure Utility-Scale and Offshore-Adjacent Contracts

Key players in the wind turbine inspection drones are expanding in two clear directions: improving aircraft performance and autonomy for repeatable, higher-throughput inspections, and enhancing software/analytics capabilities that turn visual data into actionable maintenance decisions. DJI remains the volume hardware backbone for many service providers, while specialist platforms such as SkySpecs and Cyberhawk continue to scale end-to-end inspection programs across multi-GW fleets. Drone OEMs such as Drone Volt, Delair, AeroVironment, and PrecisionHawk lean on ruggedization, longer-range operations, and enterprise procurement readiness to secure utility-scale and offshore-adjacent contracts. Autonomy-driven players such as Percepto are expanding the market by enabling persistent, automated inspection routines with minimal on-site personnel, particularly in high-risk environments.

LIST OF KEY WIND TURBINE INSPECTION DRONES COMPANIES PROFILED IN REPORT

- SZ DJI Technology Co., Ltd. (China)

- SkySpecs, Inc. (U.S.)

- Cyberhawk Innovations Limited (U.K.)

- Raptor Maps, Inc. (U.S.)

- Drone Volt SA (France)

- PrecisionHawk, Inc. (U.S.)

- AeroVironment, Inc. (U.S.)

- Percepto Ltd. (Israel)

- Delair SAS (France)

- Sharper Shape Oy (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Danish drone startup Quali Drone collaborated with RWE and its partners to demonstrate autonomous offshore wind turbine blade inspections conducted while blades were rotating, highlighting advancements in live-condition inspection capabilities.

- August 2025: Vestas partnered with Denmark’s Ministry of Climate, Energy and Utilities and the Ministry of Transport to enable autonomous drone operations for offshore wind inspection and maintenance, targeting lower emissions and operating costs.

- September 2024: RES acquired Sulzer Schmid Laboratories AG, a specialist in autonomous drone inspections and wind turbine blades condition monitoring, to strengthen RES’s wind O&M service portfolio.

- July 2023: Nearthlab expanded its strategic partnership with ONYX Insight beyond North America into Europe and APAC, combining autonomous drone inspection capabilities with predictive maintenance

- September 2018: Siemens Gamesa Renewable Energy and SkySpecs signed an agreement to deploy autonomous drone inspections for Siemens Gamesa wind turbine blades, covering both onshore and offshore fleets.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.7% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By End User, By Payload, By Autonomy Level, By Inspection Type, By Application, and Region |

| By End User |

|

| By Payload |

|

| By Autonomy Level |

|

| By Inspection Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 517.4 million in 2025 and is projected to reach USD 3,347.9 million by 2034.

In 2025, the market value stood at USD 197.23 million.

The market is expected to exhibit a CAGR of 22.7% during the forecast period (2026-2034).

The camera segment dominated the market by payload.

Global expansion of wind energy capacity is a key factor driving the growth of the market.

SZ DJI Technology Co., Ltd. (China), SkySpecs, Inc. (US), Cyberhawk Innovations Limited (UK), Raptor Maps, Inc. (US), Drone Volt SA (France) are a few major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us