3D Display Market Size, Share & Industry Analysis, By Type (Stereoscopic Display, Volumetric Display, and Holographic Display), By Technology (LED, OLED, Plasma Display Panel, and Digital Light Processing), By Access Method (Screen Based Display and Micro Display), By Application (Television, Smartphones/Mobile Devices, Monitors, Projectors, Head-Mounted Displays, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

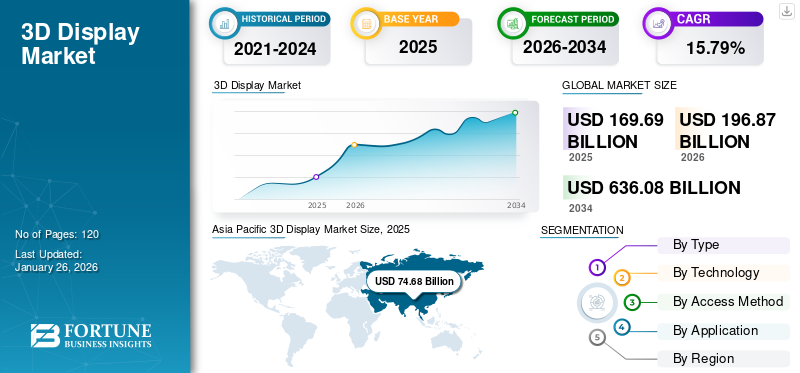

The global 3D display market size was valued at USD 169.69 billion in 2025. The market is projected to grow from USD 196.87 billion in 2026 to USD 636.08 billion by 2034, exhibiting a CAGR of 15.79% during the forecast period. North America dominated the global market with a share of 23.93% in 2025.

3D display is a display technology that generates the illusion of depth (three-dimensional perception) for viewers, rather than just showing two-dimensional, flat images. It simulates how we naturally see the world by delivering slightly different visual information to each eye or by projecting images that can be viewed from multiple angles. The technology also offers immersive, realistic experiences in gaming, 3D movies, and VR.

The growing adoption of 3D displays in automotive HUDs, medical imaging, and digital signage accelerates market growth, as industries seek realistic visualization and enhanced user engagement. Additionally, falling component costs and expanding content ecosystems are making 3-dimensional displays accessible across both consumer and professional markets. This trend is gaining rapid traction, boosting market growth.

The market is dominated by established key players, such as Sony Corporation, Samsung Electronics Co., Ltd., Panasonic Corporation, LG Electronics Inc., and Sharp Corporation. They focus on technological innovation and product differentiation, investing in advanced solutions such as holographic, glasses-free 3D, and AR/VR head mounted displays (HMD) to enhance user experience.

Download Free sample to learn more about this report.

3D Display Market Key Takeaways

- 2025 Market Size: USD 169.69 Billion

- 2026 Market Size: USD 196.87 Billion

- 2034 Forecast Market Size: USD 636.08 Billion

- CAGR: 15.79% from 2026–2034

- Asia Pacific dominated the 3D display market with a 44.01% share in 2025.

- The Stereoscopic Display segment is projected to dominate the market with a 65.08% share in 2026.

- The LED Technology segment is expected to lead the market with a 51.64% share in 2026.

Asia Pacific

Asia Pacific generated USD 74.68 billion in 2025 and is projected to reach USD 88.98 billion in 2026.

North America

North America accounted for USD 40.61 billion in 2025 and is expected to reach USD 45.65 billion in 2026.

Europe

Europe represented USD 32.24 billion in 2025 and is projected to grow to USD 36.66 billion in 2026.

U.S.

The market is projected to reach USD 32.39 billion by 2026.

Japan

Continued investments in display manufacturing, consumer electronics, and immersive technologies are supporting regional growth.

Read More

IMPACT OF GENERATIVE AI

AI-Powered Automation Enhances Efficiency Driving Demand for 3D Displays

Generative AI is reshaping the market by enabling rapid creation of high-quality, realistic 3D content, reducing the traditional bottleneck of limited 3D content availability. AI-driven tools can automatically generate immersive environments, models, and animations, making it easier for industries such as gaming, film, advertising, and healthcare to adopt 3D displays at scale. Moreover, it also improves design efficiency by automating rendering and optimizing visuals for different display formats, from AR/VR headsets to large 3D billboards. Overall, generative AI accelerates adoption by lowering costs, expanding creative possibilities, and boosting the overall value proposition of 3-dimensional display solutions.

- In June 2025, according to industry experts, companies such as Zalando, IKEA, and American Eagle deploying AI-generated 3D content led to an approximate 94% increase in conversion rates in marketing/e-commerce scenarios.

IMPACT OF RECIPROCAL TARIFFS

Trade Barriers Increase Prices and Drive Localization in 3D Display Production

Reciprocal tariffs on electronic components and finished displays can significantly impact the market by raising production costs and end-user prices, especially since key inputs such as semiconductors, optical modules, and flat panels are heavily traded across Asia, North America, and Europe. Higher import duties could disrupt global supply chains, slowing adoption in cost-sensitive segments such as consumer electronics and public signage. At the same time, tariffs may encourage regional manufacturing and localization strategies, prompting leading players to invest in domestic production or near-shoring to reduce dependency on cross-border trade.

MARKET DYNAMICS

Market Drivers

Rising Demand for Immersive Experiences among Consumers Bolsters Market Growth

Consumers and enterprises are increasingly seeking immersive and realistic experiences in gaming, entertainment, and AR/VR applications. 3-dimensional displays provide depth perception that enhances engagement, making them essential for 3D cinema, VR headsets, and interactive advertising. The gaming industry, in particular, has included 3D visualization as a core differentiator to create more lifelike environments. This rising demand is pushing manufacturers to scale production and invest in innovative 3D display solutions.

- In September 2024, according to an industry survey, the global shipments of AR/VR headsets are projected to increase by 41.4% in 2025, driven by lower prices and AI features.

Market Restraints

High Cost of Advanced 3D Displays May Hinder Market Growth

The adoption of advanced 3D displays, particularly holographic, light-field, and micro-OLED based systems, is significantly hindered by high production costs. These technologies require specialized optical engines, precision lenses, and high-resolution microdisplays, all of which involve complex manufacturing processes and low yield rates, driving up component costs.

High pricing restricts adoption primarily to premium consumer electronics, enterprise solutions, and specialized verticals such as healthcare imaging, defense, and professional design visualization. This excludes cost-sensitive markets such as smartphones, mainstream TVs, and retail signage. As a result, advanced 3-dimensional displays often remain limited to premium or enterprise-level applications, obstructing the 3D display market growth.

Market Opportunities

Increasing Adoption of 3D Billboards Propels Growth in Retail and Advertising

The advertising and retail sectors present strong opportunities through 3D billboards, holographic signage, and anamorphic LED installations. Major cities are adopting 3D billboards to display eye-catching content and attract consumers, resulting in brands willing to pay premiums for impactful advertising. Advances in direct-view LED and holographic displays are enabling glasses-free 3D signage, making adoption more practical in public spaces. This trend is particularly strong in Asia Pacific markets such as China, Japan, and South Korea, where digital out-of-home advertising is booming. As advertisers seek innovative ways to engage audiences, 3D signage is expected to grow into a mainstream channel.

- In June 2025, Australia unveiled its first 3D billboard (in Tasmania) featuring a highly animated 3D wombat using advanced LED display technology in collaboration with Fujifilm.

3D Display Market Trends

Shift in Popularity Toward Glasses-Free 3-dimensional Displays

One of the strongest trends in the market is the move toward autostereoscopic and glasses-free 3D technologies. Earlier consumer 3D TVs and monitors struggled due to the inconvenience of special glasses, but new light-field and lenticular lens technologies are addressing this barrier. Glasses-free 3D is gaining traction in public signage, retail displays, and advertising billboards, where ease of viewing is critical.

Moreover, companies are launching large-format naked-eye 3D billboards in Asia Pacific cities, which have gone viral due to their immersive and attention-grabbing visuals. This trend is also visible in consumer electronics, with experimental glasses-free 3D tablets and smartphones re-emerging in 2023–2025. As technology matures, glasses-free displays are expected to replace stereoscopic formats in many applications, improving user comfort and broadening adoption. For instance,

- In May 2024, Looking Glass, a provider of hologram, unveiled new glass-free (headset-free) spatial display devices (16-inch and 32-inch formats) using light-field technology for multiple viewers.

SEGMENTATION ANALYSIS

By Type

Widespread Adoption of AR/VR Fuels Stereoscopic Display Dominance

Based on type, the market is sub-divided into stereoscopic display, volumetric display, and holographic display.

Stereoscopic display captured the largest market share in 2025 and in 2026, the segment is anticipated to dominate with a 65.08% share. Stereoscopic displays provide a realistic depth perception by delivering separate images to each eye, making them highly effective for immersive experiences in gaming, cinema, and AR/VR headsets. They are also cost-effective and widely available, leveraging mature LCD and OLED technologies, which makes them the dominant and most commercially scalable type of 3D display technology today.

- In September 2025, Lenovo announced a free software update for its Legion Glasses 2, which introduces a 3D Mode converting 2D games into stereoscopic 3D, for over 20 games at launch.

Holographic display is anticipated to grow at the highest CAGR of 20.0% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Rise in Demand for High Brightness and Efficiency Drives LED Adoption

Based on technology, the market is classified into LED, OLED, plasma display panel, and digital light processing.

LED technology captured the largest share of the 3D display in 2025 and is estimated to hold a market share of 51.64% in 2026. It offers high brightness, energy efficiency, and long lifespan, making it ideal for large-format 3D applications such as billboards, signage, and automotive displays. Its scalability and declining cost also make LED-based 3-dimensional displays more commercially viable, ensuring wider adoption across both consumer and professional markets. For instance,

- In January 2025, Hisense unveiled a 116-inch RGB LED TV (UX Trichroma) at the Consumer Electronics Show (CES), with peak brightness of 10,000 nits. Through this product launch, the company aims to highlight how LED is pushing technical frontiers in brightness and color accuracy.

OLED technology is expected to grow at the highest CAGR of 21.2% over the forecast period.

By Access Method

Surge in Use of Screen-Centric Displays Boosts Usage Across Electronics Devices

Based on access method, the market is bifurcated into screen based display and micro display.

Screen based display captured the largest market share in 2025 as they are widely accessible with ease of integration and can be incorporated into TVs, monitors, smartphones, and tablets. Their ability to deliver immersive depth perception on standard flat-panel platforms makes them cost-effective and scalable, supporting mass adoption across both consumer and professional markets. Furthermore, the segment is set to hold 55.91% of the 3D display market share in 2026.

Micro displays are anticipated to grow at the highest CAGR of 20.1% during the forecast period.

By Application Analysis

Growing Adoption of Large-Screen Immersion Increases the Appeal of TV Appeal

Based on application, the market is categorized into television, smartphones/mobile devices, monitors, projectors, head-mounted displays, and others (signage, billboards, etc.).

Television accounted for the largest market share in 2025 and in 2026, the segment is anticipated to dominate with a 36.17% share. It offers large-screen immersive viewing for home entertainment, delivering realistic depth for movies, sports, and gaming. With widespread consumer familiarity and integration into living rooms, 3D TVs have historically been a key driver of mass-market adoption. However, their role today is more limited to premium and niche applications.

- In January 2025, Samsung re-entered the 3D conversation by announcing its Odyssey 3D monitor at the start of 2025, signaling that major TV/display brands have potential in revisiting immersive large-screen experiences.

Head-mounted displays are projected to grow at the highest CAGR of 20.0% over the forecast period.

3D DISPLAY MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific 3D Display Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific market generated USD 74.68 billion in 2025, representing 44.01% of the global market landscape, and is expected to reach USD 88.98 billion in 2026. The factors fostering the dominance of the region include strong consumer demand for immersive entertainment and gaming, coupled with rapid deployment of 3D billboards and digital signage in China, Japan, and South Korea. Additionally, the region’s position as a global manufacturing hub for display technologies enables faster commercialization and lower costs, further boosting uptake across consumer and professional applications. In the region, India and China are both estimated to reach USD 12.68 billion and USD 17.95 billion, respectively, in 2026.

Download Free sample to learn more about this report.

North America and Europe

North America recorded a market size of USD 40.61 billion in 2025, capturing 23.93% of the global market share, and is projected to reach USD 45.65 billion in 2026. In 2025, Europe represented USD 32.24 billion, accounting for 19.00% of the worldwide market, and is projected to grow to USD 36.66 billion in 2026. Other regions, such as North America and Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, North America is anticipated to record a growth rate of 12.9%, which is the fifth highest amongst all the regions, and reach USD 40.61 billion in 2025. The adoption of 3-dimensional displays is fueled by high demand for AR/VR devices in gaming, healthcare, and enterprise training, supported by strong consumer spending on advanced entertainment technologies. Moreover, early adoption of automotive 3D Heads-Up Displays (HUDs) and premium digital signage strengthens the region’s leadership in immersive display solutions. Backed by these factors, the U.S. market is estimated to reach USD 32.39 billion in 2026. After North America, the market in Europe is estimated to reach USD 32.24 billion in 2025 and secure the position of the third-largest region in the market. In the region, the U.K. is expected to record USD 6.99 billion, Germany to record USD 6.78 billion, and France to record USD 5.25 billion in 2026.

South America and the Middle East & Africa

Middle East & Africa accounted for USD 12.62 billion in 2025, representing 7.44% of the global market share, and is projected to reach USD 14.6 billion in 2026. South America and the Middle East & Africa would witness a prominent growth in this market. The South American market in 2025 is set to hit USD 9.53 billion. In the region, growing adoption of 3D displays is driven by rising investment in digital signage, cinema, and entertainment sectors, particularly in urban centers seeking innovative consumer engagement. In the Middle East & Africa, GCC is set to attain the value of USD 3.92 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Wide Range of Product Offerings, coupled with the Strong Geographic Presence Companies Support their Leading Position

The global 3D display market showcases a fragmented structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and market expansion.

Sony Corporation, Samsung Electronics Co., Ltd., Panasonic Corporation, LG Electronics Inc., and Sharp Corporation are some of the dominating players actively creating advanced solutions to cater to customer demands. Also, they focus on collaboration, acquisitions, and partnerships with regional players to maintain dominance.

Apart from this, other prominent players in the market include Toshiba Corporation, Mitsubishi Electric Corporation, Konica Minolta, Inc., TCL, Himax Technologies, Inc., and others. These companies are undertaking various strategic initiatives such as investments in R&D, geographic expansion, and product launches, to bolster their product offerings.

Long List of Companies Studied

- Sony Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- Panasonic Corporation (Japan)

- LG Electronics Inc. (South Korea)

- Toshiba Corporation (Japan)

- Sharp Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Konica Minolta, Inc. (Japan)

- TCL (China)

- Himax Technologies, Inc. (Taiwan)

- HYPERVSN (U.K.)

- Vision 3D (India)

- AUO Corporation (Taiwan)

- BOE Technology Group Co., Ltd. (China)

- Innolux Corporation (Taiwan)

- Leia Inc. (U.S.)

- Light Field Lab, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- The Coretec Group Inc. (U.S.)

- 3D Global GmbH (Germany)

….and more

KEY INDUSTRY DEVELOPMENTS

- September 2025: OMOVIE entered into a partnership with Epitone. Through this collaboration, the company aims to launch an ultra-compact 3D head-up display (HUD) announced at Internationale Automobil-Ausstellung (IAA) 2025.

- June 2025: HP unveiled the HP Dimension, the first enterprise device built for Google Beam (formerly Starline): a 65-inch light-field display with six cameras, spatial audio, no glasses needed, priced at USD 24,999.

- May 2025: Zeiss entered into a partnership with Tesa. Through this partnership, the company aims to mass-produce large-format holographic films for transparent display applications such as automotive windshields.

- April 2025: Samsung introduced its Odyssey 3D monitor line in Singapore, including a 27-inch glasses-free 3D monitor using eye-tracking and lenticular lens tech, along with Odyssey OLED G8 and G9 models.

- March 2025: Roblox unveiled its Mesh Generator API, a generative-AI model (CUBE 3D) to speed up creation of 3D objects for developers and creators.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.79% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type

North America (By Type, Technology, Access Method, Application, and Country)

South America (By Type, Technology, Access Method, Application, and Country)

Europe (By Type, Technology, Access Method, Application, and Country)

Middle East & Africa (By Type, Technology, Access Method, Application, and Country)

Asia Pacific (By Type, Technology, Access Method, Application, and Country)

|

| Companies Profiled in the Report |

|

Frequently Asked Questions

The market is expected to reach USD 636.08 billion by 2034.

In 2025, the market was valued at USD 169.69 billion.

The market is projected to grow at a CAGR of 15.79% during the forecast period.

By type, stereoscopic display led the market.

Rising demand for immersive experiences among consumers is driving the market growth.

Sony Corporation, Samsung Electronics Co., Ltd., Panasonic Corporation, LG Electronics Inc., Toshiba Corporation, Sharp Corporation, Mitsubishi Electric Corporation, Konica Minolta, Inc., TCL, and Himax Technologies, Inc. are the top players in the market.

Asia Pacific held the highest market share.

By application, the head-mounted displays are expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us