3D Printed Satellite Market Size, Share & Industry Analysis, By Component (Structural Panels, Propulsion Systems, Antennas, Protective Shells, and Others), By Type (Small Satellite, Medium Satellite, and Large Satellite), By 3D Printing Technology (Directed Energy Deposition (DED), Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), and Others), By Material (Metals, Polymers, and Ceramics), By End User (Commercial, Government and Military, Civil, and Others), and Regional Forecast, 2026-2034

3D Printed Satellite Market Size and Industry Overview

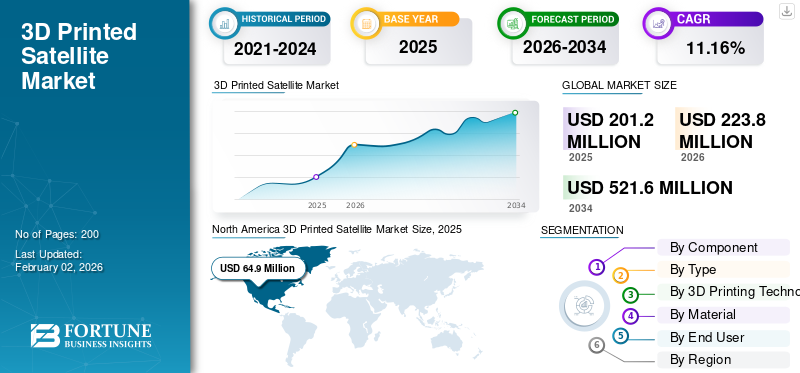

The global 3D printed satellite market size was valued at USD 201.2 million in 2025 and is projected to grow from USD 223.8 million in 2026 to USD 521.6 million by 2034, exhibiting a CAGR of 11.16% over the forecast period. North America dominated the 3D printed satellite market with a market share of 32.36% in 2025.

A 3D printed satellite is a spacecraft that is made using additive manufacturing, also known as 3D printing, for some or all of its parts. This technology makes it possible to build intricate and bespoke satellite components, which may result in lighter weight, lower production costs, and shorter production times when compared to conventional methods. Materials including titanium, aluminum, and high-performance polymers (such as PEEK) are utilized in 3D printing for satellites due to their exceptional strength-to-weight ratio and ability to endure space conditions. The use of 3D printing enhances the speed of design iteration and prototyping, which in turn speeds up the creation and testing of satellite parts. The capacity to create lightweight components is one of the most important benefits of 3D printing since it helps to lower launch expenses and increase payload capacity.

Key players include leading companies such as NASA, ISRO, Thales Group, Airbus, and others. These companies are focused on investing in technological upgradation, increasing adoption of 3D printing in satellite manufacturing, R&D activities to improve the manufacturing process, and reducing overall cost.

The COVID-19 pandemic has hampered space missions’ deployments and slowed the delivery of new products for the majority of the major space producers. Space organizations have provided significant financial and administrative help to government contractors in Asia, Europe, and North America through expedited and advance payments.

Download Free sample to learn more about this report.

3D Printed Satellite Market Key Takeaways

- 2025 Market Size: USD 201.2 million

- 2026 Market Size: USD 223.8 million

- 2034 Forecast Market Size: USD 521.6 million

- CAGR: 11.16% from 2026–2034

- North America dominated the 3D printed satellite market with a 32.36% share in 2025.

- The structural panels segment held the largest component share at 36.07% in 2026.

- The small satellite segment accounted for a 43.48% market share in 2026.

North America

North America accounted for USD 64.9 million in 2025, representing 32.36% of the global market, and is projected to reach USD 71.9 million in 2026.

Europe

Europe generated USD 58.3 million in 2025, capturing 28.99% of global revenue, and is expected to reach USD 65.1 million in 2026.

Asia Pacific

Asia Pacific held a 20.98% market share in 2025 with a valuation of USD 42.2 million and is projected to reach USD 47.2 million in 2026.

U.S.

The 3D printed satellite market is projected to reach USD 48.3 million by 2026.

Japan

The 3D printed satellite market is projected to reach USD 8.0 million by 2026.

Read More

Market Dynamics

Market Drivers

Need for Lightweight and Customizable Satellites is Expected to Bolster Market Growth

Reducing satellite weight is essential for a reduction in launch cost, payload constraints, and other factors. Even a reduction of a few kg in satellite mass leads to substantial cost savings during launch. 3D printing technology enables us to achieve this goal by allowing the construction of optimized structures that are light and robust. 3D printing satellites also give design freedom and customization. Material such as high-strength polymers, specialized metal alloys, and composites are used increasingly, which give the ability to produce complex geometries and integrate multifunctional components into a single lightweight structure.

Market Restraints

High Initial Investment Cost Required for Additive Manufacturing Implementation is Ought to Restrict Market Expansion

Satellite production using 3D printing demands advanced equipment, quality control systems, and training. Beyond hardware, there are other overhead costs such as setup, installation, and software acquisition, which increase the overall cost structure. The cost of specialized materials for meeting the required thermal and mechanical specifications also remains high. Additionally, investments in R&D to adapt 3D printing techniques for aerospace applications further add to initial costs. This barrier particularly affects smaller satellite manufacturers and startups with limited budgets, hampering innovation and market expansion.

Market Opportunities

Expanding Communication Infrastructure and IoT Deployment Offer Major Growth Opportunity

A significant market opportunity for 3D printed satellites is the rapid expansion of communication networks and Internet of Things applications. 3D printing enables manufacturers to build lightweight, complex components such as antenna, housings, and payload modules for communication satellites. The technology’s ability to deliver custom-designed parts accelerated satellite constellation launches. As demand for high-speed data transmission and global coverage is rising, there is a good opportunity for 3D printed satellite components for scaling large networks of communication satellites.

Furthermore, 3D printing's capacity to generate complex designs makes it a viable choice for manufacturing tiny, intricate parts, including wireless sensors, which are essential for many IoT applications in sectors such as healthcare and smart cities. For IoT devices that need both structural integrity and sophisticated electronics, 3D printing makes it easier to directly integrate electronic components into satellite structures, simplifying the process and speeding up assembly.

Market Challenges

Regulatory and Quality Assurance Hurdles Can Lead to Growth Challenges

Additive manufacturing technologies for space applications must comply with strict safety, reliability, and environmental standards. These requirements exist to ensure that 3D printed components (antennas, payload modules, housing, bracket, and others) can work in a harsh space environment. This requires verification, certifications, testing procedures, and can further add overhead time and costs.

Moreover, to ensure consistent and replicable manufacturing procedures, it is essential to precisely regulate parameters including laser power, scan speed, and temperature, as well as real-time monitoring to identify and avoid faults. Methods such as X-ray computed tomography (CT), ultrasonic testing (UT), and eddy current testing are essential for inspecting components for internal defects without causing harm. While particular AM standards are still being developed, adherence to quality management standards such as ISO 9001 and AS/EN 9100 is often required.

3D PRINTED SATELLITE MARKET TRENDS

Innovation in Material Science and In-Space Manufacturing is a Market Trend

Researchers are working to create cutting-edge materials, including high-strength alloys, lightweight composites, and specialized polymers such as PEEK (Polyether Ether Ketone) that have superior mechanical, thermal, and radiation resistance. The development of advanced polymers and metal alloys tailored for space environments has increased the strength, durability, and thermal resistance of 3D printed satellite components. These materials meet the rigorous mechanical and environmental requirements of space, including exposure to radiation, extreme temperatures, and others.

In space manufacturing (ISM) makes it possible to manufacture entire satellite components, spare parts, and even tools right in orbit. By utilizing resources available in space, such as asteroid resources and lunar regolith, for production, ISM uses strategies such as In-Situ Resource Utilization (ISRU), which supports sustainable space exploration. With the successful demonstration of 3D printing onboard the International Space Station (ISS), NASA’s additive manufacturing facility, on-orbit fabrication is rapidly growing.

Download Free sample to learn more about this report.

Impact of U.S. Tariffs

The 3D printing sector and its applications in the satellite industry have been severely impacted by the U.S. tariffs. The cost of producing satellites and their parts has increased significantly as a result of tariffs on materials such as steel, aluminum, advanced composites (such as carbon fiber), electronics (including microchips and sensors), and 3D printing equipment.

The imposition of tariffs has disrupted the overall supply chain, further increasing the overall cost. U.S. businesses have been compelled to rethink their sourcing strategies and seek substitutes for suppliers in impacted nations, including China. This has resulted in longer lead times, delays in obtaining essential parts, and more complexity in managing supply chains. Businesses are investigating diversification tactics, considering nations such as India, South Korea, Taiwan, and areas of Europe as possible substitutes for components and materials.

However, the tariffs have also encouraged investments in domestic manufacturing capacity for precision components in the long run, particularly those pertaining to satellite bus platforms and additive manufacturing.

SEGMENTATION ANALYSIS

By Component

Structural Panels Dominate Owing to its Extensive Manufacturing in 3D Printed Satellite Launches

The market is classified by component into structural panels, propulsion systems, antennas, protective shells, and others.

Among components, the structural panels segment led the market accounting for 36.07% market share in 2026 and is the fastest growing segment for 2026-2034. Growth in the segment is propelled by growing usage of manufacturing complex structural planes using the 3D printing technique to improve overall payload capacity and reduce launch cost.

The propulsion system segment is anticipated to show significant growth during the study period. Propulsion systems components, such as thrusters, fuel tanks, benefit from 3D printing owing to a reduction in part count, optimized design, and enhanced performance.

- In June 2025, A South Korean space company named INNOSPACE launched an Advanced Manufacturing Division. It specialized in the production of rocket engines and critical components for space launch vehicles through metal additive manufacturing (AM) technology.

To know how our report can help streamline your business, Speak to Analyst

By Type

Owing to Cost Efficiency, Quick Production Cycle, Small Satellite Segment Dominated Market

In terms of type, the market is sectioned into small satellite, medium satellite, and large satellite.

Among these types, the small satellite segment dominated the market accounting for 43.48% market share in 2026 and is expected to exhibit the fastest growth. These satellites, manufactured using 3D printing, give cost efficiency, less production cycle time, and are also used in broader application areas in earth observation, communication, and research.

The medium satellite segment is anticipated to witness significant growth during the study period. There are various advantages of these satellites, such as mission-durable designs, lower launch costs, and being used to deploy experimental payloads. This gives the segment a boost for the 3D printed satellite market growth during the study period.

By 3D Printing Technology

Ideal for Manufacturing Large and Complex Parts Results in Dominance of DED Technology

By 3D printing technology, the market is segregated into directed energy deposition (DED), fused deposition modeling (FDM), stereolithography (SLA), selective laser sintering (SLS), and others.

Among the 3D printing technology, the DED segment dominated the global market share of 39% in 2026. This technology is ideal for manufacturing large, complex parts such as support frames, propulsion components. This technology also uses metals with high precision and builds a robust structure.

The FDM segment in technology is anticipated to show moderate growth during the study period. The segment is widely used for prototyping lightweight non-critical components. A few other advantages of this technology are its cost effectiveness, ease of material switching, and suitability for critical polymer design.

By Material

Growing Demand for Metals to Design and Manufacture Different Components in Space Sector Contributed to Segment Growth

Based on material, the market is categorized into metals, polymers, and ceramics.

Among materials, the metals segment is projected to dominate the market with a share of 45.84% in 2026, Due to rising demand, this rise is attributed to the fact that metal 3D printing is in great demand for the creation and production of spacecraft, rockets, and launch vehicle components, such as nozzles, engine parts, and other components, with complicated designs and weight reduction requirements.

- In May 2023, The Relativity Space Terran 1 rocket was launched from Cape Canaveral Space Force Station in Florida. This was the first launch of a test rocket that was 100 feet in height and 7.5 feet in width and was constructed entirely of 3D-printed components. The nine additively produced engines of Terran 1 were made of a cutting-edge copper alloy.

The polymers segment is anticipated to show significant growth during the study period. Advanced materials such as carbon fiber reinforced polymers and aerospace-grade thermoplastics enable miniaturization and cost-effective production.

By End User

Growing Demand for Connectivity in Broadband and IoT Sector Contributed to Segment Growth

In terms of end user, the market is divided into commercial, government and military, civil, and others.

Among end users, the commercial segment dominated the global market in 2024. The growing need for smaller, less expensive, and adaptable satellites in a variety of sectors, including IoT, digital connectivity, and others, is driving this demand. The advantages of 3D printing, such as quick prototyping, design flexibility, and the ability to produce complex, lightweight parts, are driving this expansion.

The government and military sectors segment is anticipated to show significant growth during the study period. This segment adopts 3D printed satellites to improve responsiveness, mission flexibility, and resilience.

3D PRINTED SATELLITE MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

NORTH AMERICA

North America 3D Printed Satellite Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 64.9 million in 2025, representing 32.36% of the global market share, and is expected to reach USD 71.9 million in 2026. North America leads the market, driven by a unique ecosystem combining government investment, advanced aerospace infrastructure, and private sector investments. The region includes key players such as NASA, SpaceX, Maxar Technologies, and others. The region further benefits from R&D funding in space and 3D printing technology.

The U.S. dominated the market as government and space agencies, along with private players, invest heavily in 3D technology for both civil and military space applications. The U.S. market is projected to reach USD 48.3 million by 2026.

EUROPE

The Europe market was valued at USD 58.3 million in 2025, capturing 28.99% of global revenue, and is estimated to reach USD 65.1 million in 2026. Europe is anticipated to have a significant 3D printed satellite market share in the coming years. The European Space Agency (ESA) and national agencies in France, Germany, and the U.K. play a pivotal role in advancing 3D printing of satellite components. In January 2024, the European Space Agency (ESA) was heavily engaged in 3D printing, notably for in-space production. They have made accomplishments such as the first 3D printing of metal in space, which took place aboard the International Space Station (ISS). By minimizing dependence on expensive and time-consuming replenishment operations from Earth, this technology enables the fabrication of components, instruments, and maybe even habitats in space. The UK market is projected to reach USD 19.9 million by 2026, while the Germany market is projected to reach USD 16 million by 2026.

ASIA PACIFIC

In 2025, Asia Pacific held 20.98% of the global market, reaching a valuation of USD 42.2 million, and is projected to grow to USD 47.2 million in 2026. Asia Pacific 3D printed satellite is emerging as a high-growth region, accounting for a significant share during the study period. Major economies such as China, India, and Japan are making significant investments in 3D printed satellite parts. In July 2023, with the successful launch of three new satellites created by Nanyang Technological University (NTU), the institution's total number of satellite launches increased to 13. The satellites—SCOOB-II, VELOX-AM, and ARCADE—showcase NTU's top-tier expertise in satellite engineering and space engineer training for undergraduates. They will be used for orbital experiments, including assessing new space materials, measuring atmospheric data, and testing 3D-printed components in space. The Japan market is projected to reach USD 8 million by 2026, the China market is projected to reach USD 15.2 million by 2026, and the India market is projected to reach USD 12.6 million by 2026.

REST OF THE WORLD

Rest of the World maintained a strong presence in the global market, reaching USD 35.8 million in 2025, accounting for 17.77% share, and is expected to reach USD 39.6 million in 2026. The rest of the world includes Latin America and the Middle East & Africa. The regions are focused on boosting investment in additive manufacturing infrastructure and research efforts. To gain a competitive advantage in the market, the Middle East & Africa area is expanding 3D printed satellite projects in collaboration with foreign satellite operators. Nevertheless, these areas have difficulties such as a lack of domestic production and high entry barriers, both of which may have an impact on the regional growth of the entire market.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Focused on Offering Innovative Solutions and Catering to Specific Niches Within Industry

Key players in the market are focused on offering innovative solutions and catering to specific niches within the industry. The market is not excessively concentrated, with only a few dominant competitors, which encourages a vibrant competitive landscape and the entry of smaller, specialized businesses. The market is witnessing a rise in the number of specialized businesses and new businesses that cater to particular niches in the industry and provide cutting-edge solutions. Relativity space, which is renowned for its 3D-printed rockets and satellites, and launcher, which specializes in 3D-printed satellites and launch vehicles, are two examples. Furthermore, the technology development of specialized and mission-specific solutions is made possible by the growing collaboration between aerospace companies, research facilities, and 3D printing technology suppliers.

LIST OF KEY 3D PRINTED SATELLITE COMPANIES PROFILED

- Maxar Space Systems (U.S.)

- Boeing (U.S.)

- 3D Systems (U.S.)

- Northrop Grumman Corporation (U.S.)

- Fleet Space Technologies Pty Ltd (Australia)

- Airbus (Netherlands)

- Thales Group (France)

- National Aeronautics and Space Administration (U.S.)

- Indian Space Research Organisation (India)

- Relativity Space Inc. (U.S.)

- Rocket Lab Corporation (U.S.)

- SpaceX (U.S.)

- OneWeb (U.S.)

- United Launch Alliance, LLC (U.S.)

- Lockheed Martin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025 – Momentus Inc. has signed a five-year master services agreement (the "Master Services Agreement") with Velo3D, Inc. (OTC: VLDX) ("VLD"), a market leader in additive manufacturing solutions for the aerospace industry that enable quicker, more affordable manufacturing of system components.

- March 2025 – The Colorado-based company is applying additive manufacturing (AM) for propulsion systems, Ursa Major has been awarded a contract by an unnamed customer for GEO (geostationary earth orbit) propulsion systems. A propulsion system for a satellite bus will be researched, developed, produced, assembled, integrated, and tested during the course of the multi-year, USD 10–15 million contract.

- May 2024 – Agnikul, a startup incubated at IIT Madras and responsible for the creation of solar-powered rockets named Agnibaan - SOrTeD, launched the world's first single-piece 3D printed engine rocket from Sriharikota. Additionally, the 'Agnibaan - SOrTeD' suborbital technology demonstrator has the singular distinction of having been launched from India's first commercial launch pad, 'Dhanush,' which was constructed by Agnikul. It is also the first launch of a rocket in India that is powered by a semi-cryogenic engine.

- January 2024 – The Space Development Agency (SDA) has chosen Rocket Lab, a launch and space systems business that makes extensive use of 3D printed engines and components, to develop and construct 18 Tranche 2 Transport Layer-Beta Data Transport Satellites (T2TL – Beta). The contract is worth USD 515 million.

- June 2023 – The additive manufacturing (AM) process for the intricate series manufacture of antenna clusters has been successfully industrialized by Airbus and Oerlikon AM. These will be utilized in a network of communication satellites that will soon be orbiting the planet. This represents a significant accomplishment in the ten-year partnership between both companies in a field that demands complete accuracy, which has led to a USD 4.40 million deal to use additive manufacturing to produce these satellite parts.

REPORT COVERAGE

The report outlines competitive dynamics by assessing market segmentations, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global market research analysis provides detailed insights into the market segmentation. Besides this, the report offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, company profile, and highlights key space industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.16% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component

|

|

By Type

|

|

|

By 3D Printing Technology

|

|

|

By Material

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 201.2 million in 2025 and is anticipated to reach USD 521.6 million by 2034.

The market is estimated to grow at a CAGR of 11.16% during the forecast period.

The top players in the industry are Maxar Space Systems (U.S.), Boeing (U.S.), Airbus (Netherlands), Thales Group (France), National Aeronautics and Space Administration (U.S.), Indian Space Research Organisation (India), Relativity Space Inc. (U.S.), and Lab Corporation (U.S.) among others.

North America dominated the market in 2026.

The need for lightweight and customizable satellites is expected to bolster the market growth.

Innovation in material science and in-space manufacturing is a leading market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us