5G from Space Market Size, Share & Industry Analysis, By Solution (Hardware, Software, and Services (Direct‑to‑Device (D2D), Backhaul and Trunking, IoT , Enterprise / Private 5G, and Inorbit Services)), By Platform (Launch/manufacturing, Satellite Communications, Ground infrastructure, Space Operations, and Future constellations), By Application (Direct-To-Device, Satellite 5G, Satellite IoT, Satellite Backhaul For 5G Networks, Aviation & Maritime Connectivity, Real-Time EO And Mission Data Delivery, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

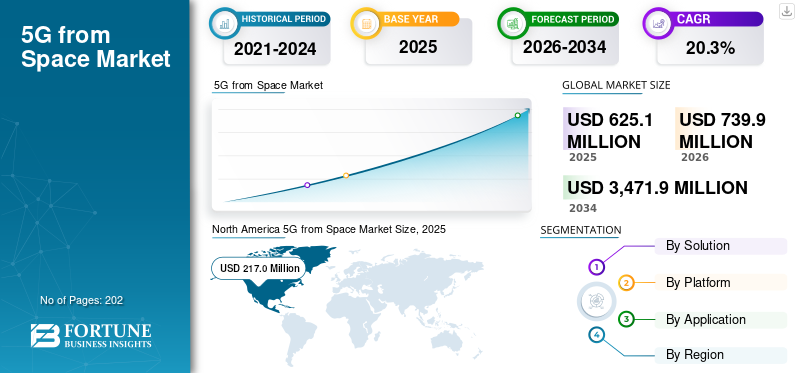

The global 5G from space market size was valued at USD 625.1 million in 2025. The market is projected to grow from USD 739.9 million in 2026 to USD 3,471.9 by 2034, exhibiting a CAGR of 20.3% during the forecast period. North America dominated the global 5G from space market with a market share of 34.7% in 2025.

5G from space refers to the integration of 5G cellular standards with Low Earth Orbit (LEO) satellite constellations to deliver uninterrupted, high-speed mobile broadband globally. It encompasses LEO satellite mega-constellations such as Starlink, direct-to-device (D2D) functionality enabling standard 5G handsets and IoT endpoints without modifications. The application of 5G from space are remote and rural regions without ground infrastructure, maritime and aviation sectors, defense operations in contested environments, disaster response scenarios.

Major players in the market include SpaceX (Starlink), OneWeb (Eutelsat), Qualcomm Technologies, Ericsson, Omnispace, among others. SpaceX delivers LEO mega-constellations for direct-to-device (D2D) 5G connectivity, targeting global IoT and mobile broadband in underserved areas. OneWeb provides NTN-compliant satellite backhaul integrated with terrestrial 5G cores for low-latency enterprise services.

Download Free sample to learn more about this report.

5G FROM SPACE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 625.1 million

- 2026 Market Size: USD 739.9 million

- 2034 Forecast Market Size: USD 3,471.9 by 2034

- CAGR: 20.30% from 2026–2034

- North America dominated the global 5G from space market with a market share of 34.7% in 2025.

- Services segment is fastest growing segment and is projected to grow at a highest CAGR of 21.7%.

- Future constellations segment is expected to grow with a fastest growth rate of 22.5%.

North America

The North America region holds the largest share in the market, valued at USD 217.0 million in 2025, and is expected to grow at a significant CAGR during the forecast period.

Europe

Europe 5G from space market is growing due to large public private programs (ESA, EU space initiatives).

Asia Pacific

The Asia Pacific market is growing at a fastest growth rate owing to large LEO/MEO constellations and rural‑coverage programs.

U.S.

The U.S. 5G from space market grows rapidly due to FCC approvals for LEO satellite constellations such as Starlink, which allows strong and seamless coverage in underserved rural and remote areas.

Japan

All such factors are expected to accelerate the demand of the 5G based communication in the region over the forecast period.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Strong Connectivity in Remote and Underserved Areas Expected to Drive Market Growth

Rising demand for strong connectivity, high speed internet in remote and underserved areas is a key driver for market growth. Space based 5G provide critical coverage voids where building satellite networks remains prohibitively expensive. Satellite constellations deliver seamless 5G services directly to standard devices in rural expanses, oceanic routes, and polar zones. There is need for reliable IoT sensor networks, real time asset tracking, and enhanced mobile broadband eMBB for isolated operations which is expected to drive the growth of the market. In addition, satellite communication is required for the evolving needs in mining, agriculture, maritime logistics, and defense deployments, further fueling 5G from space market demand.

- For instance, in November 2024, ESA demonstrated its 5G-HOST-SAT project in Lucca, Italy, integrating 5G satellite connectivity with terrestrial networks to enhance precision irrigation for agriculture

MARKET RESTRAINTS

High Infrastructure and Deployment Costs to Limit Market Expansion

High infrastructure and deployment costs restrain 5G from space industry expansion, as launching and maintaining massive LEO satellite constellations require high capital. The high cost for satellite manufacturing, launches, and ground stations limits the 5G from space market growth. Moreover, the regulatory hurdles, spectrum allocation and stringent licensing delays further growth of the industry.

MARKET OPPORTUNITIES

IoT Expansion in Remote Areas Presents Growth Opportunities for Market Growth

The explosive growth of IoT devices creates substantial opportunities for 5G based space communication sector by providing scalable connectivity in areas beyond terrestrial reach. The demand for real-time data collection from sensors for industries such as agriculture, mining, and smart infrastructure is expected to present growth opportunities for the 5G from space sector. Satellite NTNs support massive IoT deployments for asset tracking, environmental monitoring, and precision farming, where traditional networks fail due to geographic isolation. Thus, it is expected to provide lucrative opportunities for the market during the forecast period.

MARKET CHALLENGES

Interoperability Challenges Constraints Acts a Challenge for Market

A key market challenge in the market is full compatibility between diverse satellite constellations and terrestrial 5G infrastructure. Varying orbital speeds, signal delays, and protocol implementations create integration hurdles, raising development costs for operators aiming for unified services. Such integration difficulties are delaying enterprise deployments and consumer adoption which present challenges for the market growth.

5G FROM SPACE MARKET TRENDS

Strategic Partnerships between Satellite Operators and Telcos is a Significant Trend in Market

Strategic alliances between LEO satellite providers and terrestrial telecom operators represent a dominant market trend. There is an increase in integrating satellite NTNs with existing 5G cores for seamless hybrid coverage. These collaborations standardize direct-to-device protocols, enabling unmodified smartphones to connect directly to satellites without changes. Telcos gain extended reach into rural and maritime markets through these partnerships and propel market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Solution

Surging Need for Satellites, Antennas and User Terminals for Global 5G Coverage Drives Hardware Segment Growth

By solution, the market is segmented into hardware, software, and services.

The hardware segment holds the largest 5G from Space market share due to surging demand for physical components such as satellites, antennas, transponders, user terminals, and ground stations to enable global connectivity in remote areas. Advancements in satellite miniaturization, and increase in development of satellite for global 5G coverage is expected to drive segment growth.

- For instance, in, September 2025, Thales Alenia Space, was selected by CNES under the France 2030 program to lead “U DESERVE 5G,” a low‑Earth orbit demonstration of 5G direct‑to‑device connectivity. The project will launch a 5G‑compatible test satellite with an active antenna.

Services segment is fastest growing segment and is projected to grow at a highest CAGR of 21.7%. The factors responsible for segment growth is rising needs for system integration, network management, and maintenance to seamlessly blend satellite with terrestrial 5G networks. Demand for specialized offerings such as connectivity plans, data handling, and IoT support fuels segment growth.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Growing Expansion of Satellite Capacity, Constellation Planning Drive Satellite Communication Segment Growth

Based on platform, the market is segmented into launch/manufacturing, satellite communications, ground infrastructure, space operations, and future constellations.

Satellite communications currently account for the largest market share of the 5G‑from‑space / satellite‑5G ecosystem, as operators expand capacity and connectivity services for space operations or constellation planning activities. Moreover, need for extensive terrestrial integration for active satellite constellation drives segment growth. In addition, the players are investing in strategies for next‑generation 5G/6G non‑terrestrial connectivity for maritime, defense, IoT, enterprise, and direct‑to‑device.

- For instance, in December 2025, Cobham Satcom acquired 5G NTN software specialist Gatehouse Satcom and merged with Cobham’s Network Division to form a new subsidiary focused on 3GPP‑compatible 5G NTN solutions across LEO, MEO, and GEO orbits for 5G connectivity solutions.

Future constellations segment is expected to grow with a fastest growth rate of 22.5%. Future constellations and ground infrastructure are driven by large multi‑orbit LEO/MEO satellite development and the need for flexible, virtualized ground networks to support 5G integration.

By Application

Expanding Use of Satellite Links to Extend 5G into Rural and Maritime Areas Drive Satellite Backhaul Segment Growth

Based on application, the market is segmented into direct-to-device satellite 5G, satellite IoT, satellite backhaul for 5G networks, aviation & maritime connectivity, real-time EO and mission data delivery, and others.

Satellite backhaul segment dominates the market as the mobile network operators use satellite links to extend 5G coverage and fill rural or maritime gaps. Aviation and maritime connectivity together form another major block of demand, leveraging high‑throughput 5G‑ready satellites for passenger broadband and operational data.

Direct‑to‑device satellite 5G are projected to be the fastest‑growing applications and is expected to grow with a CAGR of 24.0%, driven by 3GPP NTN releases, satellite‑to‑handset launches and rapid expansion of low‑power IoT use cases. Moreover, the demand for real‑time EO and mission‑data delivery is growing as LEO constellations target low‑latency imagery and analytics, which further drives segment growth.

5G from Space Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

NORTH AMERICA

North America 5G from Space Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America region holds the largest share in the market, valued at USD 217.0 million in 2025, and is expected to grow at a significant CAGR during the forecast period. The growth of the market in the region is driven by early adoption of LEO constellations, a strong base of satellite operators and tech companies, and rise in development and testing of hardware for 5G technology for rural broadband and defense connectivity. The U.S. 5G from space market grows rapidly due to FCC approvals for LEO satellite constellations such as Starlink, which allows strong and seamless coverage in underserved rural and remote areas. Moreover, heavy investments in secure, low-latency communication network for defense drives market adoption.

- For instance, in January 2025, AmpliTech Group completed the initial phase of O-RAN Global PlugFest Fall 2025 testing for its advanced 64T64R CAT-B Massive MIMO O-RU, making it the first and the only U.S. company to bring a commercial‑grade 64T64R radio.

EUROPE

Europe 5G from space market is growing due to large public private programs (ESA, EU space initiatives). The expansion of multi‑orbit constellations and 5G integration drives steady growth in satellite 5G. The regulatory alignment across European Union member states and focus on secure, sovereign connectivity for government, defense and critical infrastructure stimulate NTN investments driving further market growth.

For instance, in November 2025, Sateliot opened Europe’s first 5G Satellite Development Center at its new Barcelona headquarters, marking the start of its industrial phase and positioning Catalonia and Spain as key hubs for 3GPP‑standardized 5G IoT connectivity from space.

ASIA PACIFIC

The Asia Pacific market is growing at a fastest growth rate owing to large LEO/MEO constellations and rural‑coverage programs. Rapid urbanization and industrial digitalization generate strong demand for NTN in transport, maritime, smart cities and agriculture. Governments push satellite‑enabled 5G to close the digital divide across extensive remote and island geographies. All such factors are expected to accelerate the demand of the 5G based communication in the region over the forecast period.

LATIN AMERICA

Latin America growth is driven by the need to extend 5G and broadband into sparsely populated and difficult terrains where terrestrial build‑out is uneconomic. Regulators and governments are increasingly supporting satellite solutions in universal‑service and connectivity programs, which encourages operator partnerships with satellite players.

MIDDLE EAST & AFRICA

The Middle East & Africa region grows as Gulf States invest in high‑throughput satellites and 5G infrastructure to support smart cities, aviation, maritime trade routes and energy operations. In Africa, satellite based 5G is positioned as a key tool to bridge severe rural connectivity gaps, often backed by multilateral and government programs.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation, Integration of AI, and Product Upgrade Drive Competitive Dynamics in Market

The 5G from Space market is characterized by companies including SpaceX (U.S.), OneWeb (U.K.), AST SpaceMobile (U.S.), Lynk Global (U.S.), SES (Luxembourg), Eutelsat Group (France), Inmarsat (UK), Telesat (Canada), and Sateliot (Spain), among others. These firms provide multi‑orbit constellations, software‑defined satellites, user terminals, flat‑panel antennas, gateway stations, and cloud‑integrated network management platforms that enable 5G‑class services from space.

In addition, to strengthen their market position, market players are making strategic investments in AI‑enabled network orchestration, digital twin–based constellation design, and virtualized ground infrastructure, often in collaboration with mobile network operators, hyperscalers, and space agencies. These players aim to optimize spectrum and power allocation, automate beam steering, and improve resilience against interference and cyber threats.

LIST OF KEY 5G FROM SPACE COMPANIES PROFILED

- SpaceX (U.S.)

- Eutelsat (France)

- AST SpaceMobile (U.S.)

- Lynk Global (U.S.)

- ST Engineering (Singapore)

- SES S.A. (Luxembourg)

- Telesat (Canada)

- Inmarsat (U.K.)

- Thales Alenia Space (France)

- Lockheed Martin (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Eutelsat announced world’s first successful 5G Non-Terrestrial Network (NTN) trial over LEO satellites, using OneWeb spacecraft plus 5G-Advanced NR NTN chipsets.

- June 2025: Vi and AST SpaceMobile announced a strategic partnership to deliver direct-to-smartphone satellite connectivity across India, extending Vi’s 4G/5G services into remote areas using AST’s space-based cellular broadband network.

- September 2025: Starlink agreed a USD 17 billion cash-and-stock deal to acquire AWS-4 and H-block spectrum from EchoStar, explicitly to grow its Direct-to-Cell constellation that provides cellular connectivity directly to unmodified smartphones

- May 2024: AT&T and AST SpaceMobile signed a definitive commercial agreement running to 2030 to build a space-based broadband network direct to everyday cell phones, integrating AST’s LEO satellites with AT&T’s terrestrial 4G/5G network.

- June 2024: Exolaunch signed a launch and deployment services agreement to deploy four Sateliot 5G NB-IoT LEO satellites on a SpaceX rideshare mission.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 20.3% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Solution, By Platform, By Application, and Region |

|

By Solution |

· Hardware · Software · Services o Direct‑to‑Device (D2D) o Backhaul and Trunking o IoT o Enterprise / Private 5G o Inorbit Services |

|

By Platform |

· Launch/ Manufacturing · Satellite Communications · Ground Infrastructure · Space Operations · Future Constellations |

|

By Application |

· Direct-to-device satellite 5G · Satellite IoT · Satellite backhaul for 5G networks · Aviation & maritime connectivity · Real-time EO and mission data delivery · Others |

|

By Region |

· North America (By Solution, By Platform, By Application, and Country) o U.S. (By Platform) o Canada (By Platform) · Europe (By Solution, By Platform, By Application, and Country) o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific (By Solution, By Platform, By Application, and Country) o China (By Platform) o Japan (By Platform) o India (By Platform) o South Korea (By Platform) o Rest of Asia Pacific (By Platform) · Latin America (By Solution, By Platform, By Application, and Country) o Brazil (By Platform) o Mexico (By Platform) o Rest of Latin America( By Platform) · Middle East & Africa (By Solution, By Platform, By Application, and Country) o UAE (By Platform) o Saudi Arabia (By Platform) o Rest of Middle East & Africa (By Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 625.1 million in 2025 and is projected to reach USD 3,471.9 million by 2034.

In 2025, the market value stood at USD 21.7.0 million.

The market is growing at a CAGR of 20.3% during the forecast period of 2026-2034.

The hardware segment led the market by solution in 2025.

The key factors driving the market are growth of market are rising demand for strong connectivity in remote and underserved areas.

SpaceX (U.S.), Eutelsat (France), AST SpaceMobile (U.S.), and Lynk Global (U.S.), and among others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us