5G in Defense Market Size, Share & Industry Analysis, By Solution Type (Hardware, Software, & Services), By Communication Infrastructure (Small & Macro Cell Network, Radio Access Network (RAN), Satellite / High-Altitude 5G Nodes, Private 5G Tactical Networks), By Core Network Technology (SDN, NFV, Edge & Fog Computing (MEC/Fog), Network Slicing, and AI-Driven Network Management), By Platform (Land, Airborne, Naval, and Space Platforms), By Frequency Band (Low-Band (<1 GHz), Mid-Band (1–6 GHz), and High-Band/mmWave (>24 GHz)), By Application, By End User, and Regional Forecast, 2026-2034

5G in Defense Market Size and Future Outlook

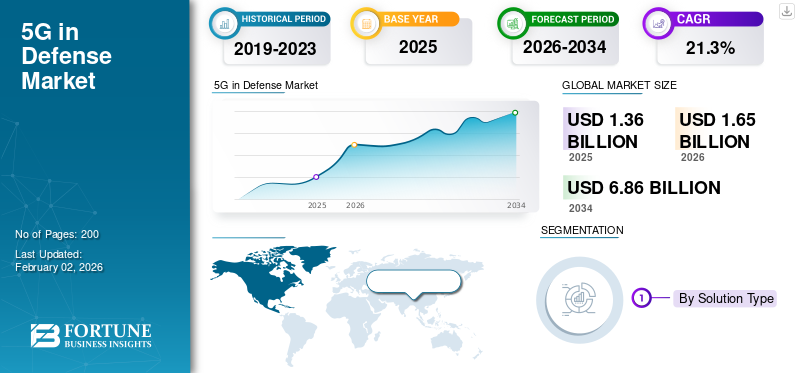

The global 5G in defense market size was valued at USD 1.360 million in 2025. The market is projected to grow from USD 1.650 million in 2026 to USD 6.860 million by 2034, exhibiting a CAGR of 19.46% during the forecast period. Europe dominated the global 5G in defense market with a market share of 25.31% in 2025.

The 5G defense market is moving from early trials to large-scale deployment as militaries recognize its potential to change modern warfare. This growth comes from the need for real-time situational awareness, the rise of autonomous and robotic systems, and the modernization of military bases and communication networks. Countries are investing in private 5G tactical systems to secure operations. Ongoing conflicts in Europe, the Middle East, and Asia are accelerating the demand for cyber-resilient digital command networks. By connecting all domains such as air, land, sea, and space, 5G is helping militaries become smarter, more connected, and more focused on data.

By 2030, over 45% of global defense communication infrastructure is expected to be 5G-enabled, transforming command networks, unmanned systems, and real-time ISR coordination.

Top companies such as Lockheed Martin, BAE Systems, Thales Group, Raytheon Technologies, Huawei, NEC, Samsung, Ericsson, and Elbit Systems are leading this change. They are building secure 5G battlefield networks, AI-powered management systems, and solutions for autonomous connectivity. Their efforts are driving the global shift toward a fully digital and network-focused defense setup.

Download Free sample to learn more about this report.

5G in Defense Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.36 billion

- 2026 Market Size: USD 1.65 billion

- 2034 Forecast Market Size: USD 6.86 billion

- CAGR: 19.46% from 2026–2034

- Europe dominated the market with a 25.31% share in 2025.

- Hardware segment held the largest market share with 61.09%.

- Edge & Fog Computing (MEC/Fog) segment is projected to grow at a CAGR of 24.6%.

North America

North America USD 0.71 billion in 2026. Strong DoD-led 5G defense programs and advanced smart military base integration supporting market leadership.

Europe

Europe USD 0.41 billion in 2026. NATO-driven 5G defense modernization and strong industrial collaboration supporting regional expansion.

Asia Pacific

Asia Pacific USD 0.44 billion in 2026. Rising defense modernization and increasing 5G military infrastructure investment across China, India, Japan, and South Korea driving growth.

U.S.

U.S. USD 0.65 billion in 2026. Large-scale defense 5G deployments and advanced C4ISR integration driving market dominance.

Japan

Japan USD 0.06 billion in 2026. Increasing defense digitalization and growing adoption of secure communication technologies supporting demand.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Integration of Autonomous and Robotic Systems Driving 5G Adoption in Defense

The increasing use of autonomous and robotic platforms in land, air, and sea operations is a major factor, driving 5G in defense market growth. Modern military missions increasingly rely on unmanned systems, robotic surveillance, and AI-driven decision networks. These technologies need low-latency communication to operate effectively in real time. 5G technology offers the reliable, high-speed connections these systems require to work together in challenging environments. This includes drone swarms, robotic convoys, automated threat detection, and sensor fusion networks. As militaries move toward network-based warfare, integrating 5G with robotics leads to faster data processing, better coordination, and improved awareness on the battlefield, thereby driving the market growth.

Over 25 military installations across the U.S., Europe, and Asia-Pacific are already testing 5G tactical networks, with programs such as the U.S. DoD’s 5G-to-NextG, the U.K.’s 5G Battlefield Initiative, and South Korea’s Defense 5G Modernization, which is driving frontline integration.

- For instance, in February 2024, the U.S. Department of Defense expanded its 5G-to-NextG Initiative by testing autonomous combat vehicles and unmanned ground systems at Nellis Air Force Base. This testing demonstrated real-time control and decision-making using 5G links.

MARKET RESTRAINTS

Cybersecurity Vulnerabilities and Data Security Risks Are Hindering Market Growth.

5G in defense market is a rising concern over cybersecurity issues and data interception risks. Defense operations rely heavily on the integrity and confidentiality of real-time information. However, as 5G networks become more software-defined and interconnected, they create new opportunities for cyberattacks and electronic warfare. Unlike older, closed communication systems, 5G’s distributed architecture depends on edge computing, virtualization, and AI, all of which can be exploited if not properly secured. Militaries are cautious about using open or commercial 5G standards for sensitive missions, due to the risk of spying, data leaks, and network manipulation. The lack of standardized global security protocols and trusted suppliers further exacerbates the challenge. As a result, defense agencies are taking a slower, more cautious approach to large-scale deployment.

While 5G in commercial sectors achieved maturity by 2024, defense integration lags by 3–5 years due to higher cybersecurity and reliability requirements, creating a unique high-growth window for defense suppliers throughout 2032.

MARKET OPPORTUNITIES:

Growing Investment in Private 5G Tactical Networks Presents Major Market Opportunity

The best opportunities in the global 5G defense market are the growth of private 5G tactical networks designed for military use. Unlike public or commercial 5G systems, these networks provide dedicated spectrum access, better encryption, and specific customization for missions. This allows defense forces to maintain secure, high-speed connectivity, even in remote or contested areas. Private 5G networks help militaries connect command centers, unmanned systems, sensors, and troops within a unified and resilient ecosystem. This change is reshaping the concept of battlefield digitization. As more countries concentrate on domestic production and secure data transfer, private 5G setups are becoming the foundation of next-generation defense communication infrastructure.

Furthermore, as next-generation 6G-ready defense networks are expected to emerge post-2030, and early 5G integrators will hold over the maximum percentage share of cross-domain communication contracts by that time.

- For instance, in October 2023, Lockheed Martin and the U.S. Department of Defense completed the world’s first end-to-end demonstration of a private 5G tactical network. This network supports secure data links for autonomous vehicles and ISR missions at Marine Corps Base Camp Pendleton.

5G IN DEFENSE MARKET TRENDS:

Integration of Artificial Intelligence (AI) with 5G Networks Is a Key Market Trend

Defense organizations are increasingly combining AI-driven analytics with high-speed 5G communication. This combination enables autonomous decision-making, predictive maintenance, and real-time threat response. AI helps military networks to dynamically allocate bandwidth, detect intrusions, and manage thousands of connected sensors and systems without human help. When paired with 5G’s ultra-low latency and high data transfer, AI changes traditional command and control into adaptive, self-optimizing defense systems. This trend speeds up the move toward multi-domain, data-focused warfare, where information from satellites, UAVs, and ground sensors is processed and acted upon instantly. The result is a smarter, faster, and more secure defense network that improves both situational awareness and operational flexibility.

- For instance, in July 2024, the NATO Communications and Information Agency (NCIA) launched its AI-5G Integration Initiative. This initiative aims to explore how AI-based traffic management can improve secure battlefield communications and situational awareness across allied forces.

MARKET CHALLENGES:

High Infrastructure Costs and Spectrum Allocation Complexity Pose Major Market Challenges

The challenge in the 5G in defense market is the high cost and logistical complexity of deploying infrastructure. Creating secure, standalone defense networks involves significant investment in base stations, edge computing nodes, encryption systems, and rugged hardware that can endure a harsh environment. Governments need to balance civilian telecom needs with military requirements for secure and clear bandwidth. Integrating 5G with existing communication systems can also lead to technical challenges, which can lead to interoperability issues and longer deployment timelines. These challenges are especially serious in emerging economies, where budget limitations and limited industrial capability hinder the rollout of advanced communication infrastructure, hindering the market growth.

Russia-Ukraine War Impact

The Russia-Ukraine War has significantly impacted the 5G Defense Market, acting as a Real-World Catalyst for Faster Defense Digitalization.

The conflict showed how connectivity, data advantage, and autonomous systems can influence the outcomes of modern warfare. Ukraine’s dependence on real-time intelligence, drone surveillance, and encrypted communications highlighted the importance of ultra-reliable networks, which are the very capabilities that 5G provides. At the same time, Russia’s widespread use of electronic warfare and cyber operations revealed weaknesses in traditional communication systems. This exposure has prompted militaries around the world to invest in resilient, low-latency, and jam-resistant tactical 5G networks.

The war has also encouraged NATO members, European allies, and nations in Asia and the Middle East to accelerate the integration of 5G with AI, satellite communication, and unmanned systems. Governments are focusing on private defense 5G infrastructure to secure command chains and support autonomous operations on the battlefield, even during electronic attacks. As a result, the war has turned 5G from a future goal into an essential part of military strategy, shifting global defense priorities toward connectivity, autonomy, and cyber resilience as critical elements of modern military strength.

In June 2025, NATO committed nearly USD 39 million to fund satellite communications, network gear, and command infrastructure for Ukraine’s defense forces, strengthening their digital, secure communication capabilities under war conditions.

Rising geopolitical instability and the global AI race are accelerating defense digitization, making 5G-enabled command superiority a top strategic priority across NATO, Indo-Pacific, and Middle Eastern alliances.

Download Free sample to learn more about this report.

Segmentation Analysis

By Solution Type

Hardware Segment Leads the Market Due to Large-Scale Infrastructure Deployment and Tactical Modernization

In terms of solution type, the market is categorized into hardware, software, and services.

The hardware segment leads the global 5G in defense market share, holding about 61.09% of the solution type segment. Segment dominance is attributed to the fact that most defense organizations are focused on building the physical infrastructure that supports secure and resilient military communication networks. As nations move from legacy systems to 5G-enabled environments, there is a strong demand for base stations, antennas, small cell networks, rugged devices, and edge computing equipment capable of handling high-speed, encrypted battlefield data. Hardware remains essential for integrating 5G into critical defense applications such as C4ISR, autonomous vehicles, and smart military bases.

For instance, in August 2024, the U.S. Department of Defense started a significant 5G infrastructure upgrade at Joint Base Pearl Harbor-Hickam. They deployed advanced tactical radio nodes and base stations to improve situational connectivity and operational coordination.

The services segment in the market is expected to grow at the fastest CAGR of 24.2% over the forecast period.

By Communication Infrastructure

Radio Access Network (RAN) Segment Dominates the Market Due to Its Central Role in Tactical Connectivity and Infrastructure Expansion

On the basis of Communication Infrastructure, the market is classified into Small Cell Network, Macro Cells Network, Radio Access Network (RAN), Satellite / High-Altitude 5G Nodes, and Private 5G Tactical Networks.

The Radio Access Network (RAN) segment leads the global 5G in defense market because it connects all defense communication elements. These elements includes sensors, soldier systems, vehicles, UAVs, and command posts. Every 5G-enabled defense network, whether it uses terrestrial or satellite links, relies on RAN components for example base stations, antennas, and distributed units to provide secure, low-latency, high-bandwidth communication. This makes RAN the foundation of military-grade 5G infrastructure. As military forces expand their 5G presence, they focus on RAN deployments to ensure reliable coverage, network slicing capability, and interoperability across various platforms, resulting in segment’s dominance. accounting for 33.00% market share in 2026

For instance, in May 2024, Ericsson and the U.S. Department of Defense worked together on the Open RAN for Tactical 5G Program. They deployed next-generation RAN modules across test bases to improve real-time communication, surveillance, and joint force connectivity under secure military conditions.

To know how our report can help streamline your business, Speak to Analyst

By Core Network Technology

Network Function Virtualization (NFV) Segment Dominates the Market Due to Its Foundational Role in Network Flexibility and Security

Based on By Core Network Technology, the market is segmented into Software-Defined Networking (SDN), Network Functions Virtualization (NFV), Edge & Fog Computing (MEC/Fog), Network Slicing, and Artificial Intelligence-Driven Network Management.

The NFV segment currently accounts for the largest share in the 5G in defense market because it provides the main virtualization layer that makes modern military networks more scalable, secure, and adaptable. By separating critical defense network functions virtualization (NFV) from traditional hardware, NFV allows militaries to quickly deploy, reconfigure, and secure communication systems across multiple areas. This flexibility is vital for developing private 5G cores, enabling network slicing, and securing data routing. It also forms the basis for all future edge and AI applications. NFV is especially prominent in the early to mid-stage defense 5G deployments in the U.S., NATO, and Asia, where governments focus on network resilience, cloud integration, and cost-effective upgrades.

For instance, in November 2023, BAE Systems and VMware announced a partnership with the U.S. Department of Defense to virtualize command network infrastructure using NFV and software-defined architectures. This collaboration aims to develop more secure, adaptable, and low-latency defense communication systems.

The segment of Edge & Fog Computing (MEC/Fog) is growing at a CAGR of 24.6% during the forecast period.

By Platform

Land Platforms Segment Dominates the Market Due to Widespread Adoption across Armored Systems, Bases, and Ground Networks

Based on platform, the market is segmented into land platforms, airborne platforms, naval platforms, and space platforms.

The land platforms segment holds the largest share in the global 5G in defense market. This growth is driven by a wide range of ground-based military assets that are adopting 5G connectivity. These assets include armored vehicles, command centers, smart military bases, and mobile communication hubs. Land operations form the backbone of every defense communication network. These operations require fast, secure, and reliable data exchange to coordinate soldiers, sensors, and unmanned systems in real time. The deployment of 5G-enabled command-and-control systems, AI-assisted logistics, and robotic ground vehicles has further reinforced this dominance. Many defense modernization programs, particularly in the U.S., U.K., India, Israel, and South Korea, are investing heavily in land-based 5G networks to improve C4ISR, mobility, and tactical decision-making. accounting for 54.81% market share in 2026

The segment of space platforms is set to flourish with a CAGR of 24.6% during the forecast period, followed by the airborne segment.

By Frequency Band

Mid-Band (1–6 GHz) Segment Dominates the Market Due to Its Balance between Range, Speed, and Tactical Reliability

Based on frequency band, the market is segmented into Low-Band (<1 GHz), Mid-Band (1–6 GHz), and High-Band / mmWave (>24 GHz).

The mid-band (1–6 GHz) frequency range leads the 5G in defense market because it provides the best balance between coverage, signal strength, and data capacity. This option is the most practical and widely favored choice for military operations, supporting tactical communications, base connectivity, and mobile command systems. It delivers higher speeds than low-band frequencies while simultaneously providing greater coverage than high-band or millimeter wave (mmWave) frequencies. Moreover, its reliability in both urban and remote areas allows defense networks to function without relying heavily on dense infrastructure, resulting in segment dominance.

The segment of High-Band / mmWave (>24 GHz) is set to flourish with a CAGR of 24.9% during the forecast period.

By Application

C4ISR Segment Dominates the Market Due to Its Central Role in Real-Time Command, Control, and Situational Awareness

On the basis of application, the market is segmented into Command, Control, Communications, Computers, Intelligence, Surveillance & Reconnaissance (C4ISR), autonomous & robotic systems, smart military bases & infrastructure, remote weapon & sensor control, training & simulation systems, and mission-critical communications.

The C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) segment leads the global 5G in defense market because it forms the main operational layer of modern military communication and decision-making. 5G’s ultra-low latency and high-speed connectivity allow for seamless integration of large data streams from drones, satellites, sensors, and radar systems. Defense forces around the world are focusing on 5G-enabled C4ISR systems to boost network-centric warfare. The combination of 5G with AI analytics, cloud computing, and edge networks is changing traditional defense operations into dynamic, data-driven systems, resulting in segmental growth.

For instance, in May 2024, the U.S. Department of Defense teamed up with AT&T and Northrop Grumman to improve C4ISR modernization through a secure 5G pilot at Fort Irwin, California. This pilot integrates real-time data from unmanned systems, sensors, and command centers to speed up decision-making and enhance situational awareness.

The segment of autonomous & robotic systems is set to grow at a CAGR of 25.2% during the forecast period

By End User

Military End User Dominates the Market Due to Rising Soldier Modernization and Cross-Border Security Programs

In terms of end user, the market is segmented into military forces, homeland security agencies, defense contractors & OEMS, and government & research institutions.

The military segment is the largest end user in the 5G in Defense market. Increased global defense modernization efforts, increased defense spending, and the need for better survivability in modern warfare drive this growth. Military forces in the U.S., Europe, China, India, and Russia are focusing on integrating advanced armor systems, including modular body armor, ballistic helmets, vehicle armor kits, and blast-resistant materials. Rising geopolitical tensions, such as the Russia-Ukraine conflict and territorial disputes in the Indo-Pacific, have increased procurement activities and research and development investments in this area.

For instance, in January 2024, the U.S. Department of Defense awarded Ceradyne, Inc., a subsidiary of 3M, a USD 168 million contract. This contract is to supply advanced ballistic helmets and armor plates for U.S. Army personnel under the Soldier Protection System program. The goal is to improve combat survivability and mission readiness.

The segment of homeland security agencies is set to grow at a CAGR of 24.5% growth across the forecast period.

5G in Defense Market Regional Outlook

North Americ 5G in Defense Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America Dominates the 5G in Defense Market Due to Strong U.S. Defense Modernization and Early 5G Integration Initiatives

By region, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World (Middle East & Africa, and Latin America).

North America

North America recorded a market size of USD 0.58 billion in 2025, capturing 43.00% of the global market share, and is projected to reach USD 0.71 billion in 2026, it captured the largest market share, generating USD 710 million, led primarily by the U.S., which alone contributed over 92.61% share in 2024 of the regional share. The U.S. Department of Defense (DoD) has been at the forefront of integrating 5G across smart military bases, C4ISR systems, and autonomous platforms, investing in large-scale testbeds under its 5G-to-NextG Initiative. The U.S. market is projected to reach USD 0.65 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 0.35 billion in 2025, representing 25.99% of the global market landscape, and is expected to reach USD 0.44 billion in 2026. Other regions such as Asia-Pacific, Europe, and the Middle East are expected to see significant growth in the 5G in Defense Market in the coming years. During the forecast period, the Asia-Pacific region is projected to have a growth rate of 24.8%, which is the fastest growing among all regions. In the Asia-Pacific, countries including China, India, South Korea, and Japan are increasing investment in military infrastructure and platforms. Based on these factors,. The Japan market is projected to reach USD 0.06 billion by 2026, the China market is projected to reach USD 0.13 billion by 2026, and the India market is projected to reach USD 0.09 billion by 2026.

Europe

In 2025, Europe represented USD 0.34 billion, accounting for 25.31% of the worldwide market, and is projected to grow to USD 0.41 billion in 2026, making it the second-largest region in the market. In this region, both the UK and Germany are expected to reach USD 84.4 million and USD 67.9 million, respectively, in 2025. In Europe, growth is supported by NATO-led 5G defense modernization and strong industrial collaboration in countries such as France, the U.K., and Germany. The UK market is projected to reach USD 0.1 billion by 2026, and the Germany market is projected to reach USD 0.08 billion by 2026.

Rest of the World

The market in Rest of the World reached USD 0.08 billion in 2025, representing 5.70% of total market revenue, and is projected to reach USD 0.09 billion in 2026. Meanwhile, the Rest of the World (Middle East & Africa, and Latin America) collectively contributes approximately 5.60% in 2024, with nations such as the UAE, Israel, Saudi Arabia, and Brazil leading in smart base and border communication initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players:

5G in Defense Market Shaped by Strategic Partnerships, Technological Innovation, and Dual-Use Collaboration

The 5G in defense market is highly competitive. It includes a mix of traditional defense companies, leading telecom firms, and emerging tech startups, all aiming to modernize military communication systems. Major defense contractors such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, and Thales Group are incorporating 5G technologies into platforms that support C4ISR, autonomous systems, and tactical communication networks. Meanwhile, telecom and tech companies such as Ericsson, Nokia, Samsung, Huawei, and NEC Corporation contribute their skills in network infrastructure, AI management, and cybersecurity, connecting commercial 5G to defense-grade uses.

The competitive landscape also features a rise in public and private partnerships. Governments are funding large-scale trials, while industry partners provide secure network solutions. For example, the U.S. Department of Defense’s 5G-to-NextG Initiative involves several companies working at pilot sites to develop 5G-enabled command centers and autonomous logistics.

The market is shifting from traditional hardware delivery to comprehensive digital ecosystem development. Company growth now depends on mastering 5G integration, AI-driven management, and interoperability across domains.

LIST OF KEY 5G IN DEFENSE COMPANIES PROFILED:

- Lockheed Martin (U.S.)

- Nokia (Finland)

- AT&T (U.S.)

- L3Harris Technologies (U.S.)

- Ericsson (Sweden)

- Verizon (U.S.)

- Raytheon Technologies (U.S.)

- Keysight Technologies (U.S.)

- Oceus Networks (U.S.)

- BAE Systems (U.K.)

- Cohere Technologies (U.S.)

- Airbus Defence and Space (Europe)

- Samsung Electronics (South Korea)

- NEC Corporation (Japan)

- General Dynamics Mission Systems (U.S.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS:

- For Instance, in March 2024, Ericsson and the Swedish Armed Forces partnered to deploy a private, standalone 5G network designed for military-grade encryption and mission-critical communications across training and operational zones.

- For Instance, in October 2024, the U.S. Department of Defense formally adopted a strategy for rolling out private 5G networks at military installations, aiming to leverage both commercial and private 5G to provide high-speed connectivity tailored to mission needs.

- For Instance, in March 2025, Lockheed Martin announced the successful integration of Nokia’s military-grade 5G solutions and Verizon network management into its 5G.MIL HBS (Hybrid Base Station), enabling a seamless bridge between commercial 5G links and tactical communications.

- For Instance, in February 2025, Lockheed Martin, along with Intel and Radisys, deployed a standalone 5G network during the U.S. Marine Corps’ Steel Knight 2024 exercise to support cross-domain operations.

- For Instance, in May 2025, Nokia and Blackned (a Rheinmetall subsidiary) announced a joint venture to develop next-generation 5G tactical communication systems tailored for the German armed forces.

REPORT COVERAGE

The global 5G in Defense Market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The 5G in Defense Market research report also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.46% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation

|

By Solution Type

By Communication Infrastructure

By Core Network Technology

By Platform

By Frequency Band

By Application

By End User

By Region

|

Frequently Asked Questions

The global 5G in defense market size is projected to grow from $1.650 million in 2026 to $6,860 million by 2034, exhibiting a CAGR of 19.46%

In 2025, the market value stood at USD 580 million.

The market is expected to exhibit a CAGR of 19.46% during the forecast period of 2026-2034.

The hardware segment led the market by solution type.

Rising integration of autonomous and robotic systems is driving 5g adoption in defense, driving the market growth.

Lockheed Martin, L3Harris Technologies, Raytheon Technologies, BAE Systems, Samsung Electronics, Nokia, AT&T, Ericsson, Verizon, Cohere Technologies, Airbus Defence and Space, NEC Corporation, General Dynamics Mission Systems, Keysight Technologies, Oceus Networks, Thales Group, and Leonardo S.p.A. are the top companies in the 5G in Defense market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us