Active Implantable Medical Devices Market Size, Share & Industry Analysis, By Product Type (Cardiovascular Implants {Cardiac Pacemakers, Implantable Cardioverter Defibrillators, Cardiac Resynchronization Therapy (CRT) Devices, and Others}, Neuromodulation Implants {Spinal Cord Stimulators, Deep Brain Stimulators, Vagus Nerve Stimulators, and Others}, Hearing Aids, Implantable Drug Delivery Pumps, and Others), By Application (Cardiology, Neurology, Diabetes management, Pain management, and Others), By End-user (Hospitals & Clinics, Homecare Settings, Others), and Regional Forecast, 2026-2034

Active Implantable Medical Devices Market Size and Future Outlook

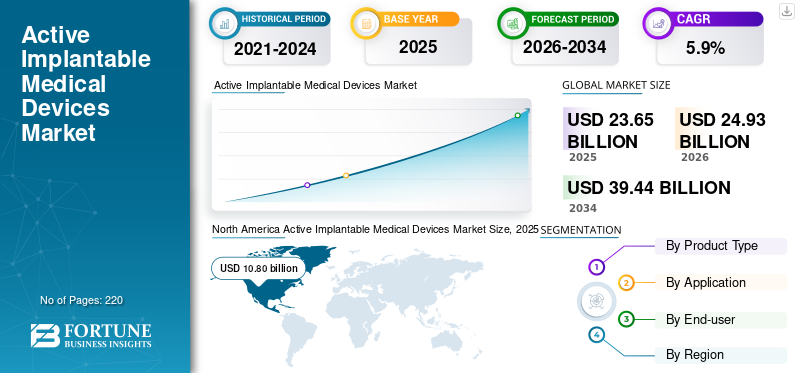

The global active implantable medical devices market size was valued at USD 23.65 billion in 2025. The market is projected to grow from USD 24.93 billion in 2026 to USD 39.44 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. North America dominated the global active implantable medical devices market with a market share of 45.67% in 2025.

The active implantable medical devices include advanced devices that are implanted in the body and use electrical or mechanical systems to support or improve a patient’s health. The industry includes products such as pacemakers, implantable defibrillators, neurostimulators, cochlear implants, and implantable pumps, among others. The market growth is attributed to the substantial prevalence of chronic heart conditions, neurological disorders, and hearing problems. In addition, technological advancements in implantable medical devices and rising investments in new innovations are also estimated to accelerate market growth.

Moreover, the market is dominated by major players, including Medtronic, Abbott, Boston Scientific Corporation, Biotronik, and LivaNova PLC, and others. These players are involved in innovations and strategic initiatives to expand their market reach.

Download Free sample to learn more about this report.

Active Implantable Medical Devices Market Key Takeaways

- 2025 Market Size: USD 23.65 billion

- 2026 Market Size: USD 24.93 billion

- 2034 Forecast Market Size: USD 39.44 billion

- CAGR: 5.9% from 2026–2034

- North America dominated the active implantable medical devices market with a 45.67% share in 2025.

- Cardiovascular implants accounted for the largest product type segment share in 2025.

- Hospitals & clinics are projected to hold a 64.2% market share in 2026.

North America

North America led the market with a value of USD 10.80 billion in 2025 and maintained the largest regional share.

Europe

Europe is projected to reach USD 6.95 billion in 2026, supported by the presence of major industry players.

Asia Pacific

Asia Pacific is expected to reach USD 4.53 billion in 2026, making it the third-largest regional market.

U.S.

The market is projected to reach USD 9.73 billion in 2026, driven by increasing adoption of advanced implantable devices.

Japan

The market is supported by growing demand for advanced implantable medical technologies and an aging population.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Burden of Chronic Heart Conditions and Neurological Disorders to Boost Market Growth

An increasing burden of chronic cardiac conditions, coupled with neurological disorders to boost the global active implantable medical devices market growth. Moreover, many patients now depend on devices such as pacemakers, defibrillators, neurostimulators, and cochlear implants for steady control of symptoms and better daily functioning. As populations’ age and lifestyle diseases increase, the adoption of such products is likely to increase during the forecast period.

- For example, according to data published by the Centers for Disease Control and Prevention (CDC), in May 2024, an estimated 3.0 million Americans suffer from epilepsy.

MARKET RESTRAINTS:

Exorbitant Cost and Complex Surgical Requirements to Deter Market Growth

The exorbitant cost of implantable medical devices, along with complex surgical requirements, is estimated to hamper the market growth. Devices including pacemakers, defibrillators, neurostimulators, and cochlear implants are expensive, and the total treatment cost also includes surgery, imaging, hospital stay, and long-term follow-up. Due to such high costs, many hospitals and patients cannot afford this full package, especially in regions with limited insurance coverage. Such factors are projected to hamper the product adoption, thereby deterring the market growth.

MARKET OPPORTUNITIES:

Growing Preference for Remote Monitoring Capabilities and Connected Devices to Provide Favorable Growth Opportunities

The market is witnessing an extensive rise in adoption and preference for devices with connected functionalities along with remote monitoring. Due to continual technological advancements and innovations, many novel technologies are entering the market. Such new implants support wireless data transfer, allowing healthcare professionals to track device performance and patient health without frequent hospital visits. In addition, hospitals also prefer these systems as they help detect issues early and reduce emergency admissions. As digital health tools spread and more patients become comfortable with home-based monitoring, demand for smart and connected implants is set to rise.

- For instance, in January 2023, Abbott received FDA approval for its new spinal cord stimulation device, Proclaim XR. The company also provided functionality for these patients to connect to physicians through their NeuroSphere Virtual Clinic app.

MARKET CHALLENGES:

Limited Patient Awareness and Fear of Implant Procedures to Pose Challenge for Market Growth

A major challenge for the active implantable medical devices market is the lack of awareness among patients and the fear of undergoing an implant procedure. Many patients have stigma regarding implants due to fear and as disability post-surgical consequences. Moreover, they worry about surgery, safety, long-term effects, and the idea of having a device inside the body. In some regions, patients still rely on medicines or external devices as they do not fully understand how these implants work or how much they can help.

ACTIVE IMPLANTABLE MEDICAL DEVICES MARKET TRENDS:

Growing Use of Absorbable and Tissue-Friendly Materials is One of Key Market Trends

A clear trend in the active implantable medical devices market is the move toward smaller devices with longer battery life. New pacemakers, neurostimulators, and implantable sensors are being designed with compact sizes and advanced battery systems that last many years without replacement. Surgeons prefer these smaller implants as they are easier to place and cause less discomfort for patients. Longer battery life also reduces the need for repeat surgeries, which lowers risk and cost. As technology improves, companies are adding better power management, wireless charging, and efficient electronics, which make these implants more reliable for long-term use. This shift toward miniaturized and durable devices is shaping buying decisions for hospitals and helping the market grow steadily.

- For instance, in July 2023, Baxter announced the launch of its new PERCLOT Absorbable hemostatic powder in the U.S. market. The product is especially designed to address mild bleeding.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Rising Adoption of Cardiac Implants Due to Superior Benefits for Cardiac Arrhythmia to Accelerate Segment Growth

Based on the product type segmentation, the market is categorized into cardiovascular implants, neuromodulation implants, hearing aids, implantable drug delivery pumps, and others.

To know how our report can help streamline your business, Speak to Analyst

The cardiovascular implants segment accounted for the largest global active implantable medical devices market share in 2025. The segment growth is majorly attributed to its significant adoption of pacemakers, ICDs, and CRTs, which is associated with the substantial prevalence of cardiac arrhythmia. In addition, an increasing number of products with technologically advanced functionalities to accelerate segment growth.

- For instance, in July 2023, Abbott announced the launch of its new and world’s first dual-chamber leadless pacemaker.

Additionally, the neuromodulation implants segment is anticipated to grow at a CAGR of 6.7% during the projection period.

By Application

Substantial Prevalence of Cardiac Conditions Across Globe to Accelerate Segment Growth

Based on application, the market is segmented into cardiology, neurology, diabetes management, pain management, and others.

By application, the cardiology segment accounted for the major share in 2025. The segment growth is majorly attributed to the substantial prevalence of cardiac conditions. Moreover, other factors such as an aging population and superior treatment outcomes of these active implantable devices are responsible for the high share of the cardiology application segment. Also, the segment is set to hold 58.7% share in 2026.

- For instance, according to data published by the Centers for Disease Control and Prevention in May 2024, an estimated 6.7 million people in the U.S. suffer from heart failure at the age of 20 years old.

In addition, the neurology segment is projected to grow at a CAGR of 6.6% during the forecast period.

By End-user

Considerable Availability of Infrastructure in Hospitals & Clinics Drives Segment Growth

Based on end-user, the market is classified into hospitals & clinics, homecare settings, and others.

In 2025, the global market was led by hospitals & clinics in terms of end-user. Hospitals and clinics lead the active implantable medical devices market as most surgical implants take place in these settings. In addition, these facilities are equipped with advanced instruments, which enable streamlining of the surgical procedure. Moreover, rising investments in such facilities are also projected to have a positive impact on the segment growth. , the segment is set to hold 64.2% share in 2026.

In addition, the homecare settings segment is projected to grow at a CAGR of 6.0% during the forecast period.

Active Implantable Medical Devices Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

NORTH AMERICA

North America held the leading share in 2024, valuing at USD 10.27 billion, and also maintained the leading share in 2025, with USD 10.80 billion. The growth is attributed to the increasing number of rising prevalence of chronic conditions, aging population, and introduction of advanced technologies. In 2026, the U.S. market is projected to touch USD 9.73 billion.

- For instance, in October 2023, Medtronic received FDA approved for its new Aurora EV-ICD MRI SureScan extravascular defibrillator. The device is developed for the treatment of sudden cardiac arrest.

North America Active Implantable Medical Devices Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

EUROPE and ASIA PACIFIC

Regions including Europe and the Asia Pacific, are projected to experience notable growth by 2034. Europe is projected to record a growth rate of 5.0% and reach a valuation of USD 6.95 billion by 2026. This growth is attributed to the presence of major players in countries including Germany, the U.K., and France. Due to these factors, the U.K. is expected to reach a valuation of USD 1.13 billion, Germany USD 1.56 billion, and France USD 0.93 billion in 2026. After Europe, the market in Asia Pacific is projected to reach USD 4.53 billion in 2026 and secure the position of the third-largest region in the market. In the region, China and India are both estimated to reach USD 1.61 billion and USD 1.07 billion, respectively, in 2026.

LATIN AMERICA and MIDDLE EAST & AFRICA

In the coming years, the Latin America and Middle East & Africa regions are expected to showcase moderate growth in the market. The Latin America market in 2026 is set to reach a valuation of USD 1.02 billion. The growth is attributed to technological advancements in implantable medical devices and increasing awareness of surgical care in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.27 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Focus on Product Launches and Approval to Strengthen Position of Key Players

In 2025, major players such as Medtronic, Abbott, Boston Scientific Corporation, Biotronik, and LivaNova PLC accounted for the largest global market share. The share is attributed to the focus of these players on innovations and other strategic initiatives, including partnerships, acquisitions, and collaborations.

Other prominent companies, such as Saluda Medical, Stimwave Technologies, Cochlear Ltd., and Infusyn Therapeutics, are focused on increasing product supply to emerging countries, which is expected to help them gain a significant market share.

LIST OF KEY ACTIVE IMPLANTABLE MEDICAL DEVICES MARKET COMPANIES PROFILED:

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Biotronik (Germany)

- LivaNova PLC (U.K.)

- Saluda Medical (Australia)

- NeuroPace (U.S.)

- Cochlear Ltd. (Australia)

- Infusyn Therapeutics (U.S.)

- Blackrock Neurotech (U.S.)

- BrainsWay (Israel)

- Neuronetics (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Onward Medical received FDA home use approval for its spinal cord stimulator.

- April 2025: Abbott introduced its new technologically advanced platform with an aim to streamline the implantation procedure for electrodes.

- March 2025: Newronika announced receiving of CE IVD approval for its AlphaDBS, an advanced DBS (deep brain stimulation system).

- January 2025: Saluda Medical, Inc. announced receiving of FDA approval for its biomarker-based and automated patient programming platform in spinal cord stimulation.

- October 2023: MicroPort Scientific Corporation announced the launch of its new ULYS ICD & INVICTA defibrillation leads in Japan. Both the leads are MRI conditional.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.9% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, End-user, and Region |

|

By Product Type |

Cardiovascular Implants

Neuromodulation Implants

|

|

By Application |

|

|

By End-user |

|

|

By Region |

North America (By Product Type, Application, End-user, and Country)

Europe (By Product Type, Application, End-user, and Country/Sub-region)

Asia Pacific (By Product Type, Application, End-user, and Country/Sub-region)

Latin America (By Size, Procedure, End-user, and Country/Sub-region)

Middle East & Africa (By Product Type, Application, End-user, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 23.65 billion in 2025 and is projected to reach USD 39.44 billion by 2034.

In 2025, the market value stood at USD 10.80 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

The cardiovascular implants segment led the market by product type.

The key factors driving the market are the increasing number of implantations and technological advancements.

Medtronic, Abbott, Boston Scientific Corporation, Biotronik, and LivaNova PLC are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us