Aerospace Ground Handling System Market Size, Share & Industry Analysis, By Offering (Ground Support Equipment (Pushback Tugs & Tractors, Ground Power Units (GPUs), Baggage & Cargo Loaders, Aircraft Refuelers, & Others) and Software / Digital Ramp Systems), By Application (Passenger Handling, Baggage Handling, Cargo and Mail Handling, & Others), By Power Source (Diesel / ICE, Electric Battery, Hybrid, & Others), By Aircraft Type (Commercial Aircraft (Narrow-body Aircraft, Wide-body Aircraft, & Regional Aircraft), General Aviation, & Others), By End User, and Regional Forecast, 2026-2034

Aerospace Ground Handling System Market Size and Future Outlook

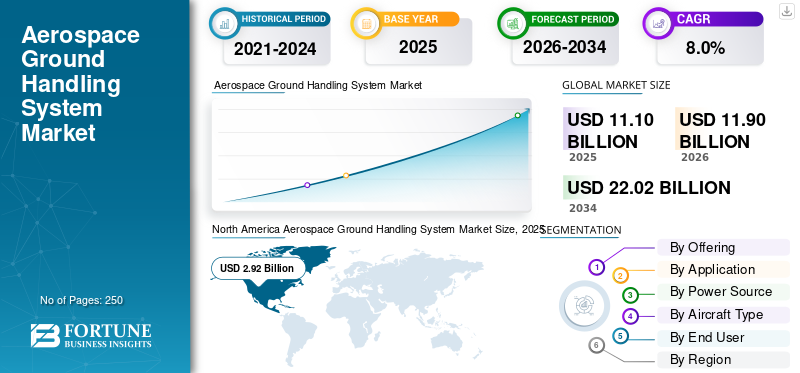

The global aerospace ground handling system market size was valued at USD 11.10 billion in 2025. The market is projected to grow from USD 11.90 billion in 2026 to USD 22.02 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period. North America dominated the aerospace ground handling system market with a market share of 26.30% in 2025.

The global aerospace ground handling market is experiencing robust growth, fueled by surging air passenger traffic, extensive airport infrastructure expansions, and the push for faster aircraft turnaround times to boost operational efficiency. Rising e-commerce and air cargo demand further amplify the need for advanced ramp and cargo handling services worldwide.

- For instance, in 2026, Swissport collaborated with U.K. based Aurrigo International to launch its first global pilot of autonomous ground handling tech at Zurich Airport. The project features a digital simulation platform and a live trial of a fully autonomous electric vehicle to boost airside logistics efficiency.

Leading companies such as JBT Aerotech, Swissport International, Menzies Aviation, Aviapartner, and Mallaghan Engineering are prioritizing innovations such as Electric Ground Support Equipment (eGSE) to reduce emissions, autonomous guided vehicles for safer pushback operations, and AI-integrated systems for real-time workflow optimization.

Download Free sample to learn more about this report.

AEROSPACE GROUND HANDLING SYSTEM MARKET TRENDS

Adoption of Electric & Autonomous Ground Support Equipment is a Defining Market Trend

The adoption of electric and autonomous ground support equipment is emerging as a key trend in the industry. The trend is driven by stringent environmental regulations and net-zero emission targets at major airports. Airport and aircraft operators are rapidly transitioning from diesel-powered tugs, loaders, and baggage carts to battery-electric alternatives that significantly reduce carbon footprints and operational noise.

- For instance, in February 2026, Swissport completed Geneva Airport's first fully electric aircraft turnaround for a Brussels Airlines flight, using battery-powered ground support equipment for all tasks from arrival to pushback. The process included passenger boarding/disembarking, baggage and cargo handling, aircraft servicing, and gate pushback, with no diesel vehicles involved under standard operating conditions.

Autonomous features, including AI-guided navigation and remote operation, further enhance this shift by minimizing human error, optimizing ramp workflows, and enabling 24/7 operations with reduced labor costs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Surge in Global Air Passenger & Cargo Traffic to Drive Market Growth

The surge in global air passenger traffic and air travel serves as a primary driver of the market. Fueled by economic recovery, expanding middle-class populations in emerging regions, and rebounding tourism post-pandemic.

- IATA forecast passenger volumes to reach 5.2 billion in 2026, intensifying ramp operations and equipment demands worldwide. Cargo volumes are expected to reach 71.6 million tons in 2026.

This growth necessitates scalable ground support systems to enable faster aircraft turnarounds, increased baggage throughput, and efficient pushback services to minimize delays at congested hubs such as Dubai, Atlanta, and Delhi. Airlines and airports are investing heavily in high-capacity GSE to handle larger widebody fleets from Boeing and Airbus, directly boosting procurement of tugs, loaders, and de-icing units.

MARKET RESTRAINTS

High Capital Costs for Specialized Equipment and Maintenance Infrastructure to Limit Market Expansion

High capital costs for specialized equipment and maintenance infrastructure represent a key restraint in the market. Investment in advanced GSE including high-lift passenger stairs, widebody-compatible pushback tractors, and precision-guided baggage carts requires substantial upfront investments that burden smaller operators and regional airports with limited capital access. Routine maintenance demands for these assets, such as hydraulic servicing, electrical diagnostics, and component replacements, generate recurring expenditures and hamper the aerospace ground handling system market growth during the forecast period.

MARKET OPPORTUNITIES

Rise in Airport Infrastructure Expansion Presents Growth Opportunities for the Market

Rise in airport infrastructure expansion offers a major growth opportunity for the market. Ongoing global investments in new terminals, runways, and capacity upgrades generate sustained demand for advanced ground handling equipment to manage increased aircraft parking, ramp throughput, and operational scale. This development spurs procurement of high-capacity GSE designed for efficient handling of diverse fleets, from narrowbody to widebody aircraft, enhancing turnaround efficiency at expanded facilities. Airport modernization initiatives prioritize integrated systems that support higher flight frequencies and cargo volumes, creating opportunities to deploy advanced equipment.

- For instance, in February 2026, Kempegowda International Airport (BLR) started expansion with a USD 2 billion plan to handle over 100 million passengers annually, including Terminal 1 refurbishment, adding 10 million in capacity by 2026-2027, and Terminal 2 Phase 2 upgrades. Moreover, Menzies Aviation secured a 15-year ground handling license at Kempegowda International Airport Bengaluru (BLR). The agreement expands Menzies' 15-year cargo presence to full services across Terminals 1 and 2, including passenger, ramp, and baggage operations for integrated airline support.

MARKET CHALLENGES

Stringent Regulatory Compliance Costs Limits Flexibility and Innovation and Acts as a Key Market Challenge

Stringent regulatory compliance costs limit flexibility and innovation, posing a key market challenge. Evolving mandates on emissions standards, complex supply chains, worker safety protocols, and equipment certification impose substantial financial burdens through rigorous testing, documentation, and recurring audits, diverting resources from R&D initiatives. Operators must navigate disparate regional regulations, such as EU ETS carbon pricing and FAA noise restrictions, which require customized GSE modifications that escalate design and validation costs while prolonging approval timelines.

Segmentation Analysis

By Offering

Commercial Flight Movements Increase Drives GSE Segment Growth

Based on offering, the market is divided into ground support equipment and software / digital ramp systems.

The ground support equipment segment leads the market, driven by its direct role in aircraft turnaround efficiency, operational continuity, and airport capacity utilization. Demand is supported by the steady increase in commercial flight movements, which raises the need for towing, loading, power supply, servicing, and ramp support equipment across airports.

For instance, in November 2025, dnata deployed over 100 ground support vehicles, including electric, hybrid, and bio-diesel models, for the Dubai Airshow 2025 at Dubai World Central (DWC). The 111 assets comprised pushback tractors, ground power units, passenger steps, and air conditioning units to facilitate aircraft movements across static and flying displays.

Software / digital ramp systems segment is anticipated to grow with a CAGR of 9.4% over the forecast period.

By Application

Global Air Passenger Traffic Increase Propels Passenger Handling Segment Growth

By application, the market is segmented into passenger handling, baggage handling, cargo and mail handling, aircraft handling and loading, aircraft servicing, and others.

Passenger handling segment held the largest market share in 2025 due to growth in global air passenger traffic and the resulting need for energy efficient front-end airport operations. As passenger volumes rise, airports and ground handlers must strengthen their capabilities in check-in support, boarding coordination, gate operations, passenger transfer, and associated baggage interface activities. Growth is further supported by increasing pressure on airports to improve throughput, reduce congestion, and maintain service quality.

The cargo and mail handling is projected to be the fastest growing segment, with a CAGR of 10.0% over the forecast period.

By Power Source

Established Infrastructure and Heavy-Duty Reliability Drives Diesel / ICE Segment Growth

By power source, the market is segmented into diesel / ICE, electric battery, hybrid, and hydrogen / fuel-cell.

Diesel / ICE segment dominated the market in 2025. The existing airport GSE fleet remains conventionally powered. Its demand is supported by operational familiarity, established refueling infrastructure, and suitability for heavy-duty applications requiring long operating hours and high equipment availability. In many airports, particularly in developing markets, diesel-powered equipment remains the most practical option due to lower upfront transition requirements and limited charging infrastructure.

Electric battery systems segment is projected to grow with a CAGR of 10.1% over the forecast period. The segment is growing rapidly due to a focus on lowering emissions, advancing cargo workflows, and reducing manual labor at airport terminals worldwide.

For instance, in April 2025, Cathay Cargo Terminal at Hong Kong International Airport completed the world's first end-to-end trial of an Autonomous Electric Tractor (AET), towing cargo dollies from inside the terminal directly to the West Cargo Apron for flight loading.

By Aircraft Type

Scheduled Passenger/Cargo Operations Expansion Support Commercial Aircraft Segment Growth

Based on aircraft type, the market is segmented into commercial aircraft, general aviation, and military aircraft. Commercial aircraft includes narrow-body aircraft, wide-body aircraft, and regional aircraft.

The commercial aircraft segment accounts for the largest aerospace ground handling system market share, as airport ground handling systems are primarily designed for scheduled passenger and cargo operations. Growth in this segment is driven by rising airline traffic, increasing aircraft movements, network expansion, and the continued development of airport infrastructure to handle higher flight volumes. In addition, airport operators aim to introduce proven autonomous baggage handling innovations for commercial aviation sector.

- For instance, on April 8, 2025, Aurrigo International and Aviation Solutions announced a partnership to commercialize Aurrigo's Auto-DollyTug and Auto-Sim autonomous solutions across Aviation Solutions' network of over 60 airports.

To know how our report can help streamline your business, Speak to Analyst

General aviation segment is expected to grow with a steady growth rate of 5.6% over the forecast period.

By End User

Outsourcing for Cost Efficiency and Scale Advantages to Support Segment Growth

Based on end user, the market is segmented into airlines, airport operators, third-party ground handling service providers, government / military aviation operators, and others

The third-party ground handling service provider segment is dominating, as airlines increasingly rely on outsourced specialists to improve cost efficiency, operational flexibility, and service consistency across airport networks. These providers benefit from scale advantages, as they can deploy equipment, labor, and digital systems across multiple airline customers and airport locations more efficiently than individual carriers operating in-house models.

Third-party ground handling service providers segment is projected to grow at the fastest rate of 9.2% over the forecast period.

Aerospace Ground Handling System Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

North America

North America Aerospace Ground Handling System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held a significant market share in 2025, with a valuation of USD 2.90 billion, and is expected to maintain its leading position, reaching USD 3.09 billion in 2026. North America remains a major market, due to its large installed airport base, high aircraft movement density, and strong replacement demand for aging ramp equipment. Growth in the region is being supported less by greenfield airport expansion and more by modernization spending, electrification of GSE fleets, and operational efficiency upgrades across mature airports. The U.S., in particular, benefits from structured public funding support, including FAA programs for zero-emission airport vehicles and related infrastructure, which are accelerating equipment renewal and digital ramp upgrades. Moreover, the expansion of airport terminals and the replacement of outdated infrastructure are driving the procurement of advanced ground handling systems, which is propelling market growth in the region.

For instance, in November 2025, the New Terminal One at JFK Airport selected Menzies Aviation and Worldwide Flight Services to provide above-wing and below-wing ground handling services. Above-wing covers check-in, baggage office operations, meet-and-assist, and irregular operations support; below-wing includes electric GSE for aircraft servicing, emphasizing safety and efficiency.

U.S. Aerospace Ground Handling System Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 2.58 billion in 2025. Rising air passenger traffic and cargo volumes at major US hubs such as JFK, LAX, and ATL require expanded GSE fleets to support efficient ramp operations. Massive airport infrastructure investments drive demand for eGSE, automation, and compatible handling systems. Sustainability mandates from the Port Authority (net-zero by 2050) and FAA regulations accelerate the adoption of electric GSE to replace diesel equipment by 2030.

Europe

Europe is projected to record a growth rate of 6.8% during the forecast period. The region is expected to witness steady growth, driven by the need to improve turnaround efficiency, maintain service quality, and replace legacy equipment across a dense and highly regulated airport network. The region also benefits from its strong international traffic base, which typically requires more structured and equipment-intensive ramp handling operations. Moreover, third party ground handling service providers collaborate with GSE manufacturers to develop advanced, effective ground support equipment to enhance passenger boarding and handling.

- For instance, in November 2025, Aviramp signed a five-year procurement contract with dnata at the Dubai Airshow, enabling dnata's worldwide bases to directly order passenger boarding ramps without tender processes.

U.K. Aerospace Ground Handling System Market

The U.K. market in 2025 is estimated at around USD 0.59 billion, representing roughly 5.3% of global revenues.

Germany Aerospace Ground Handling System Market

Germany’s market is projected to reach approximately USD 0.34 billion in 2025, equivalent to around 3.0% of global sales.

Asia Pacific

Asia Pacific market reached USD 3.74 billion in 2025. Asia Pacific is the strongest structural growth market, due to its large airport traffic base, ongoing airport expansion, and high fleet-growth potential. ACI World’s forecast places Asia Pacific at 3.5 billion passengers in 2024, while ACI Asia Pacific & MID expects the region to record 4.8% annual passenger growth during 2025-2028, supported by resilient demand and infrastructure investment. This creates a broad requirement for new towing, loading, passenger-handling, refueling, and ramp-support systems across both established and expanding airports.

Japan Aerospace Ground Handling System Market

The Japanese system market in 2025 was valued at around USD 0.36 billion, accounting for roughly 3.2% of global revenues.

China Aerospace Ground Handling System Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 1.33 billion, representing roughly 12.0% of global sales.

India Aerospace Ground Handling System Market

The Indian market in 2025 was valued at around USD 0.63 billion, accounting for roughly 5.7% of global revenues.

Latin America and Middle East & Africa

Latin America is an emerging growth market where demand is being supported by steady traffic recovery, airport capacity expansion, and gradual modernization of airport operations. Middle East & Africa is the fastest-growing regional market. This supports strong demand for loaders, tugs, GPUs, passenger-handling systems, and servicing equipment at major hub airports where wide-body operations, transfer traffic, and cargo activity are particularly important.

Saudi Arabia Aerospace Ground Handling System Market

Saudi Arabia’s market in 2025 was valued at around USD 0.28 billion, accounting for roughly 2.5% of global revenues.

COMPETITIVE LANDSCAPE

Strategic Alliances, Electrification, and Autonomous Innovation Drive Market Leadership

The global aerospace ground handling systems market features intense competition among leading service providers and equipment manufacturers delivering electric GSE, autonomous tugs, and integrated ramp solutions to enable efficient aircraft turnarounds. Major players such as Swissport, Menzies Aviation, dnata, TLD Group, and Oshkosh AeroTech prioritize electrification of baggage loaders and pushbacks, AI-enabled autonomy such as Aurrigo's Auto-DollyTug, and hydrogen/electric power units across major hubs, including Zurich, Bengaluru, Geneva, and Schiphol Airports. Focus on fleet standardization, modular battery integration from partners such as Scania-Dynell, and digital simulation platforms accelerates the shift to zero-emission operations amid airport expansion demands.

LIST OF KEY AEROSPACE GROUND HANDLING SYSTEM COMPANIES PROFILED

- TLD Group (France)

- Oshkosh AeroTech (U.S.)

- Textron GSE (U.S.)

- Tronair Inc. (U.S.)

- ITW GSE (Denmark)

- AERO Specialties (U.S.)

- Cavotec SA (Switzerland)

- Weihai Guangtai (China)

- Menzies Aviation (U.S.)

- Mallaghan Engineering (U.K.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Aviaco GSE signed a 14-year contract with KLM Royal Dutch Airlines to supply 14 electric TLD ABS580-E widebody staircases for Schiphol Airport. The units will handle Airbus A330, Boeing 777, and Boeing 787 aircraft, supporting next-generation ground operations.

- March 2026: Menzies Aviation secured a 15-year ground handling license at Kempegowda International Airport Bengaluru (BLR), effective from April 1, 2026, pending regulatory approvals. The license, awarded by BIAL, expands Menzies' existing cargo operations to full passenger, ramp, and baggage services across Terminals 1 and 2 at one of India's fastest-growing airports.

- March 2026: Exeter Airport in the U.K. is conducting its second hydrogen-powered GSE trial, the HyGPU Winter Operations Project, testing a dual-fuel hydrogen/diesel ground power unit in cold weather overnight. Supported by Cranfield University, ULEMCo, Connected Places Catapult, and the U.K. CAA, it follows a prior April 2025 trial that used three hydrogen technologies for a TUI Boeing 737-800 turnaround.

- February 2026: Scania partnered with Austrian firm Dynell to electrify airport ground support equipment, supplying its Core 800 and 700 battery systems for Dynell's DEM 045-090 electric ground power units, which deliver up to 90 kVA of mobile aircraft power.

- January 2026: Oshkosh Corporation showcased advanced autonomy, AI, connectivity, and electrification technologies at CES 2026 to transform airports, job sites, and emergency response. Highlights include electrified vehicles for airport teams, AI collision warnings, modular robots for faster aircraft turnarounds, and AI recycling systems.

- May 2025: Swissport partnered with U.K.-based Aurrigo International for a global pilot of autonomous ground handling at Zurich Airport, starting with the Auto-Sim digital platform to virtually model operations. The project advances to live trials of Aurrigo's electric Auto-DollyTug, featuring 360° obstacle detection and automated ULD loading for enhanced ramp efficiency.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, By Application, By Power Source, By Aircraft Type, By End User and Region |

| By Offering |

|

| By Application |

|

| By Power Source |

|

| By Aircraft Type |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.10 billion in 2025 and is projected to reach USD 22.02 billion by 2034.

In 2025, the North Americas market value stood at USD 2.92 billion.

The market is expected to exhibit a CAGR of 8.0% during the forecast period.

By power source, the diesel / ICE segment led the market in 2025.

Surge in global air passenger & cargo traffic are the key factors driving the market.

TLD Group (France), Oshkosh AeroTech (U.S.), Textron GSE (U.S.), and Tronair Inc. (U.S.) are some of the major players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us