General Aviation Market Size, Share & Russia Ukraine War Analysis, By Aircraft Type (Fixed-Wing Aircraft (Piston Aircraft, Turboprop Aircraft, & Business Jets), Rotary Wing Aircraft, and Others), By Application (Personal/Leisure Flight, Business Aviation, Flight Training, and Others), By Operator (Private Owners, Corporate Owners, Charter Operators, Fractional Ownership Programs, Flight Schools, and Government Agencies), By Range (Short, Medium & Long, Ultra-Long Range), By Propulsion (Piston Engine, Turbine Engine, & Electric), and Regional Forecast, 2026-2034

General Aviation Market Size and Future Outlook

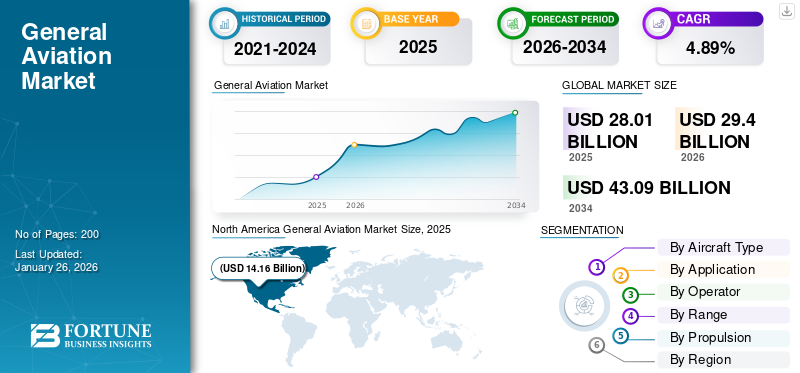

The global general aviation market size was valued at USD 28.01 billion in 2025 and is projected to grow from USD 29.40 billion in 2026 to USD 43.09 billion by 2034, exhibiting a CAGR of 4.89% during the forecast period. North America dominated the general aviation market with a market share of 50.56% in 2025.

General aviation includes civil aviation operations excluding commercial air transport (airlines) and military aviation. GA includes aerial work such as agricultural spraying, surveying, firefighting, and others. It refers to all the activities that range from private aviation to business jet travel. Business aviation plays a vital role in air transportation which encompasses corporations and individuals using jets and turboprops for flexible, point-to-point travel.

The major government and regulatory bodies such as Federal Aviation Administration (FAA), European Union Aviation Safety Agency (EASA), and the International Civil Aviation Organization (ICAO) are responsible for the introduction and regulation of safety standards, certification, and operational frameworks for the general aviation industry across the globe. Moreover, key players in the market such as Textron Aviation (Cessna, Beechcraft), Cirrus Aircraft, Piper Aircraft, and Embraer Executive Jets manufacture a wide range of piston, turboprop, and business jet aircraft. In addition, aircraft companies such as Dassault Aviation and Bombardier produces aircrafts for the business jet segment.

Download Free sample to learn more about this report.

General Aviation Market Key Takeaways

- 2025 Market Size: USD 28.01 billion

- 2026 Market Size: USD 29.40 billion

- 2034 Forecast Market Size: USD 43.09 billion

- CAGR: 4.89% from 2026–2034

- North America dominated the general aviation market with a 50.56% share in 2025.

- The Fixed-Wing Aircraft segment accounted for the largest market share of 69.53% in 2026.

- The Business Aviation segment is projected to hold a 55.14% share in 2026.

North America

North America held 50.56% share in 2025, valued at USD 14.16 billion.

Asia Pacific

Asia Pacific market valued at USD 5.29 billion in 2025.

Europe

Europe market valued at USD 5.79 billion in 2025.

U.S.

Market projected to reach USD 14.86 billion by 2026.

Latin America

Latin America is projected to grow to USD 1.62 billion in 2026.

Read More

Impact of Russia Ukraine War on the Market

Russia Ukraine War Impacted Supply Chains, Raising the Costs of GA Aircraft Manufacturing

The Russia Ukraine War has created significant impact on the market. One of the most critical impacts is the disruption of supply chains, as both Russia and Ukraine are important suppliers of aerospace materials such as titanium and aluminum. Sanctions on Russia and damage to Ukrainian industries have raised costs for GA aircraft manufacturing and maintenance. Another key factor is the surge in fuel prices, which directly affects operating expenses for piston and turboprop aircraft that dominate GA fleets. Moreover, the war has increased geopolitical risk perception which may impact market expansion. Overall, the war has not significantly hampered the general aviation growth, but it has introduced higher costs, operational constraints, and investment uncertainties.

MARKET DYNAMICS

MARKET DRIVERS:

Demand for Flexible Travel & Surge in Emergency Medical Services to Propel the Market Growth

Recently, corporations and high net worth individuals are depending increasingly on business aviation for fast, flexible, and point-to-point travel. There is an increase in globalization of business and growth in emerging markets which has further boosted the demand for flexible and quick mobility across regions. The business aviation growth is due to increase in cross border business activities and increased demand for secondary airport connectivity, and investment in aviation infrastructure.

- For instance, according to the General Aviation Manufacturers Association (GAMA), business jets experienced a standout growth segment in the first half of 2025. Deliveries increased from 322 units in the first half of 2024 to 354 units in the same period of 2025, marking a 9.9% increase. This growth overcame other general aviation categories, highlighting the sustained demand for corporate and private air travel.

Simultaneously, rise in demand for air ambulance and other medical services is expanding which is expected to boost the market demand.

MARKET RESTRAINTS:

High Operating and Ownership Costs of Aircraft to Restrict Market Expansion

Aircrafts such as business jets, private jets, and turboprops have significant fixed expenses including fuel, hangar fees, insurance, and regular maintenance mandated by regulators. Moreover, high annual operating costs of such aircrafts allow only corporations and high net worth individuals to access jets. This high cost acts as a barrier to entry for new users and constrain fleet expansion for existing operators. Thus, such high costs are expected to slow market growth.

MARKET OPPORTUNITIES:

Adoption of Sustainable Aviation Technologies to Create Lucrative Growth Opportunities

Governments and regulators (such as EASA in Europe and the FAA in the U.S.) are under pressure to align aviation with broader net-zero emissions targets. Therefore, general aviation is also trying to adopt electric propulsion systems for aircrafts with small size and shorter missions.

- For instance, in June 2025, Beta Technologies’ all-electric Alia CX300 successfully carried four passengers on a 130-km flight from East Hampton to JFK Airport. The aircraft is designed to offer smooth travelling without traffic.

Moreover, governments and regulators are increasingly supporting the electrification trend with the help of various funding programs, initiatives, and certification standards. Moreover, cost savings and efficient travel are expected to drive the growth of the market.

MARKET CHALLENGES:

Regulatory and Certification Hurdles to Hamper Market Growth

Aircraft manufacturers and operators must comply with stringent regulation which are enhancing safety in aviation, emissions, and noise regulations, which vary as per different regions. Certification of new technologies such as electric or hybrid propulsion, advanced avionics, or sustainable fuels is often lengthy, complex, and expensive. These processes delay product launches and increase development costs, especially for smaller OEMs and startups. Regulatory uncertainty around emerging technologies can also discourage investments. This challenge slows down innovation adoption and creates barriers for general aviation market growth.

GENERAL AVIATION MARKET TRENDS:

Rise in Use of Advanced Avionics and Digital Cockpit Systems is a Significant Market Trend

The market is experiencing a strong shift towards advanced avionics and digital cockpit systems. These technologies help pilots to get real time data to enhance situational awareness and improve decision making capabilities. Connectivity features such as ADS-B and satellite communication are enabling seamless communication and compliance with regulatory mandates. The installation of digital cockpits in aviation industry is expected to promote innovation in general aircraft systems.

- For instance, in in January 2025, Honeywell and NXP announced that they are expanding their collaboration to integrate Honeywell’s Anthem cockpit system, a cloud based digital avionics platform.

Training costs are being optimized as standardized digital systems simplify pilot transition across aircraft types. Overall, the trend of digitalization is expected to improve general aviation, making it safer, more efficient, and more attractive to operators.

Download Free sample to learn more about this report.

Segmentation Analysis

By Aircraft Type

Broader Mission Capability, Higher Speed, and Cost Efficiency Contributes to Segmental Growth of Fixed-Wing Aircraft

On the basis of the segmentation of aircraft type, the market is classified into fixed-wing aircraft, rotary wing aircraft, and others. The fixed-wing aircraft includes piston aircraft, rotary wing aircraft, and others. Moreover, others include gliders, motor-gliders, light sport aircraft, electric vertical take-off and landing eVTOL aircraft prototypes, and other aircrafts.

The fixed-wing segment is anticipated to hold a dominant market share of 69.53% in 2026. The segment holds largest share as it be used for wide range of missions in general aviation, from personal flying and business travel to training and cargo. This type of aircraft is preferred due its lower operating cost and long range & speed provided. The segment is also the fastest growing as the deliveries of business jets and other fixed-wing aircrafts have increased.

- For instance, GAMA’s Q2 report highlights that the general aviation market is experiencing steady growth, with piston airplane shipments rising 5.1% to 810 units in the first half of 2025.

The others segment will grow at a fastest rate due to rising demand for gliders, motor-gliders, light sport aircraft, eVTOL prototypes, and other aircrafts. There is an increasing interest in affordable recreational flying, as well as investments in new technologies such as electric propulsion and urban air mobility solutions, which is expected to fuel more demand for these aircrafts.

- For instance, in May 2025, Joby Aviation advanced its eVTOL prototype testing program in the U.S. which showcases the growing popularity in the urban air mobility

To know how our report can help streamline your business, Speak to Analyst

By Application

Rise in Corporate Travel & Expansion of Charter Services Fuels Growth of Business Aviation Segment

In terms of application, the market is categorized into personal/ leisure flight, business aviation, flight training, aerial work, and emergency services. Aerial work encompasses agricultural aviation, aerial survey and mapping, observation & patrol, aerial photography, and other applications.

The business aviation segment is anticipated to hold a dominant market share of 55.14% in 2026, owing to the growth in demand for private jets and turboprop aircraft among corporate travelers, high-net-worth individuals (HNWIs), and charter operators. The segment growth is propelled by rise in the globalization of businesses, time-saving requirements, and expansion of charter services and fractional ownership. Furthermore, development and launches of new business models with enhanced fuel efficiency and long-range capabilities are attracting more buyers and operators.

- For instance, in March 2025, Gulfstream Aerospace delivered the first G700 business jet to a European customer, reflecting the growing demand for advanced long-range business aircraft.

The flight training is expected to be fastest growing segment due to rising demand for aircrafts for basic training purposes and to teach flying skills. There is an expansion of flight training schools which is expected to fuel more demand for aircrafts.

- For instance, in May 2025, Paragon Flight Training expanded its operations in Georgia (U.S.) in 2024 by acquiring a flight school and adding more aircrafts.

By Operator

Surge in Demand for Personal Mobility and Business Travel Fuels Growth of Private Owners Segment

In terms of operator, the market is categorized into private owners, corporate owners, charter operators, fractional ownership programs, flight schools, and government agencies.

The private owners segment is anticipated to hold a dominant market share of 26.90% in 2026, as general aviation aircraft are being increasingly used for personal mobility and business travel. Moreover, the constant upgrades and modernization of existing private aircrafts is expected to drive the growth of the segment.

- For instance, according to General Aviation Manufacturers Association (GAMA), new private jet deliveries increased by 4.7% to 764 units.

The flight school segment is expected to be the fastest growing segment due to rising demand for new and skilled pilots which is pushing the need for a safer, glass-cockpit model to train pilots. Moreover, there is a surge in the expansion of flight training academies across various countries which is expected to increase the demand for training aircraft models.

- For instance, in January 2025, Air India Flying Training Academy ordered up to 93 Piper Archer DX trainers (31 firm for 2025 and 62 options through 2027), with deliveries starting Q1 2025, to equip its new Amravati, Maharashtra school.

By Range

Demand for Regional Business Travel to Stimulate Medium Range Segment Growth

In terms of range, the market is categorized into short range (less than 700 nm), medium range (700–1,800 nm), long range (1,800 nm to 6,000 nm), and ultra-long range (more than 6,000 nm).

The medium range (700–1,800 nm) segment is anticipated to hold a dominant market share of 35.57% in 2026, as the aircraft of this particular range criteria is used extensively for regional business travel and charter. The medium segment aircrafts are preferred during regional business trips and charter shuttles due to broad airport access and short & effective performance. In addition, shift towards development of eco-friendly and energy efficient aircraft is expected to propel the segment growth.

- For instance, in March 2025, Beyond Aero unveiled BYA-1 hydrogen-electric eight-passenger business jet concept. The aircraft is equipped with battery-free 2.4 MW fuel-cell system and targets ~800 nm (≈1,482 km) range.

The long range (1,800 nm to 6,000 nm) is expected to be fastest growing segment due to rise in the demand for long range aircrafts to complete more trips without stopping and with fewer refueling stops for business and charter travelling. Leading OEMs in the market are focused on the development of long range aircraft models with lower operating costs and better comfort which is expected to promote segment growth. Key players such as Embraer (Praetor 500/600), Textron Aviation (Cessna Citation Longitude), and Bombardier (Challenger 3500) offer aircraft designed to operate in the 2,000–4,000 nm range.

By Propulsion

Efficiency and Capability of Supplemented The Turbine Engine Segment Growth

Based on propulsion, the market is segmented into piston engine, turbine engine, and electric.

The turbine engine segment held the dominating position in 2025. The segment is growing due to the efficiency and capability of turbine engines for long-range business travel. There is an increase in popularity of turbine engines among business aviation customers for saving time and improve flight productivity which is expected to fuel the growth of the segment during the forecast period.

The electric segment is anticipated to be the fastest growing segment during the forecast period due to increase in adoption of electric propelled aircraft for training, leisure, and short haul applications. Various factors contributing to the growth of the segment are less operating costs, low emissions, and regulatory support by government of different countries for sustainable aviation.

- For instance, in April 2025, Pipistrel expanded deliveries of its Velis Electro aircraft in Europe,

Thus, such development highlight the integration of certified electric aircraft into flight training and recreational flying stimulating further growth in the segment.

General Aviation Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America General Aviation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region accounted for largest share in the market and is expected to expand at a significant rate during the forecast period. The North America general aviation market growth is attributed to strong presence of major OEMs and well-established infrastructure. Moreover, there is a high demand for both business aviation and pilot training in the U.S. and Canada. In addition, various supportive regulations and avionics adoption stimulate the market growth in North America. Rising demand for private mobility solutions and increasing fleet modernization further support growth. In 2025, the North America market stood at USD 14.16 billion, representing 50.56% of global demand, and is projected to grow to USD 14.86 billion in 2026.

- For instance, GAMA’s Q2 2025 report highlighted that North America led global shipments, with business jet deliveries rising nearly 10% year-on-year in the first half of 2025.

Europe

Europe is anticipated to witness a notable growth during the forecast period. The growth is driven by increased business travel, strong investments in sustainable aviation. Countries in the region such as Germany, U.K., and France are key contributors, with high demand for business jets and turboprops. In addition, the region’s focus on sustainability in aviation and electric aircraft development is expected to drive the growth of the market in the region during the forecast period. The Europe region captured 20.67% of the global market in 2025, generating USD 5.79 billion in revenue, and is projected to reach USD 6.01 billion in 2026.

- For instance, in 2023, German eVTOL manufacturer Lilium signed a MoU with Lufthansa in December 2023 to explore a strategic partnership for bringing electric air taxis to Europe.

Asia Pacific

The Asia Pacific region is witnessing a steady growth in market. The market is due to rapid economic expansion and rising disposable incomes. The region is witnessing increased interest in private and business aviation. Countries in the region such as China, India, and Australia are investing heavily in training infrastructure to meet increasing demand for pilots. The surge in use of general aviation aircraft for energy and other sectors and the expansion of flight schools are major drivers for the market growth. Asia Pacific maintained a strong presence in the global market, reaching USD 5.29 billion in 2025, accounting for 18.90% share, and is expected to reach USD 5.64 billion in 2026.

- For instance, in February 2025, China’s Skyco International Leasing ordered six additional Airbus H175 helicopters, following an earlier order in 2024, to support offshore industry operations.

Latin America and Middle East & Africa

During the forecast period, Latin America and Middle East & Africa are expected to grow at a moderate rate due to use of aircraft for regional connectivity, agricultural applications, and pilot training. Countries such as Brazil and Mexico in Latin America are major contributors, leveraging GA aircraft for both personal and commercial purposes in areas with limited airline connectivity. The Middle East & Africa market accounted for USD 1.2 billion in 2025, representing 4.29% of the global industry, and is expected to reach USD 1.27 billion in 2026. In 2025, Latin America represented USD 1.56 billion, accounting for 5.58% of the worldwide market, and is projected to grow to USD 1.62 billion in 2026.

- For instance, in August 2025, Embraer expanded its general aviation presence in Latin America by partnering with Chile’s Aerocardal as an Authorized Service Center for executive jets. Based in Santiago, the new facility will provide maintenance and technical support for Embraer aircraft.

In addition, the Middle East & Africa is experiencing increasing investments in business aviation, particularly in countries such as the UAE and Saudi Arabia, where private jet usage is growing rapidly.

COMPETITIVE LANDSCAPE

Key Industry Players:

Product Diversification, Sustainable Technologies, and Strategic Partnerships Supports the Expansion of Key Players in the Market

The global market is driven by rising demand for business aviation, pilot training, and personal flying. The market is further influenced by growing investments in electric and hybrid aircraft, sustainable aviation fuels (SAF), and digital cockpit systems.

Key players in this market include Textron Aviation (Cessna, Beechcraft), Cirrus Aircraft, Piper Aircraft, Bombardier, Embraer, Dassault Aviation, Gulfstream Aerospace, and emerging innovators such as Lilium and Joby Aviation in electric aviation. These companies contribute to the market growth by offering a wide portfolio of solutions across piston aircraft, turboprops, business jets, training aircraft, and eVTOL platforms.

Companies are focusing on delivering advanced avionics suites, fuel-efficient propulsion systems, lighter composite airframes, and sustainable aircraft models to capture the evolving demand. Moreover, major OEMs are investing heavily in electrification, hybrid propulsion, and digital technologies to align with regulatory requirements and customer preferences.

LIST OF KEY GENERAL AVIATION COMPANIES PROFILED:

- Textron Aviation (U.S.)

- Cirrus Aircraft (U.S.)

- Piper Aircraft (U.S.)

- Gulfstream Aerospace (General Dynamics) (U.S.)

- Bombardier Aviation (Canada)

- Embraer (Brazil)

- Dassault Aviation (France)

- Pilatus Aircraft (Switzerland)

- Diamond Aircraft Industries (Austria)

- BAE Systems (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: Cirrus Aircraft announced the SR Series G7+ with Safe Return Emergency Autoland, making it the world’s first single-engine piston aircraft with FAA-approved autonomous emergency landing capability.

- June 2025: Embraer released its Market Outlook 2025 predicting demand for 10,500 new jets and turboprops in the sub-150-seat category through 2044, driven by connectivity needs and fleet renewal.

- June 2025: Dassault Aviation and Reliance Aerostructure Limited signed an agreement at the 2025 Paris Air Show to manufacture Falcon 2000 LXS business jets in India.

- April 2025: General Dynamics (Gulfstream) secured FAA and EASA certifications for the Gulfstream G800 business jet, clearing the way for its entry into service in both the U.S. and Europe.

- November 2024: Gulfstream Aerospace Corp. announced its G500 and G600 fleet reached 300 customer deliveries, highlighting continued demand for modern large and super-mid business jets.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2024-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.89% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Aircraft Type

By Application

By Operators

By Range

By Propulsion

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 28.01 billion in 2025 and is projected to reach USD 43.09 billion by 2034.

In 2025, the market value stood at USD 14.16 billion.

The market is expected to exhibit a CAGR of 4.89%% during the forecast period.

The fixed-wing aircraft segment led the market by aircraft type segment.

The key factors driving the market are growth of market are rising adoption of business jets for flexible travel & surge in demand for emergency medical services.

Textron Aviation (U.S.), Cirrus Aircraft (U.S.), Bombardier Aviation (Canada), and Embraer (Brazil) are some of the prominent players in the market.

North America dominated the general aviation market with a market share of 50.56% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us