Aerospace Testing Market Size, Share & Industry Analysis, By Testing Type (Material Testing, Structural Testing, Environmental Testing, Acoustic Testing, Vibration & Shock Testing, Electromagnetic Compatibility (EMC) Testing, Non-Destructive Testing (NDT), and Software & Simulation Testing), By System (Structural, Propulsion, Avionics, & Launch Systems), By Testing Phase (Development & Certification Testing, Production & Quality Assurance Testing, and Operational & Maintenance Testing), By Sourcing (In house, Outsourced, and Collaborative Testing) By End User, & Regional Forecast, 2026-2034

Aerospace Testing Market Size and Future Outlook

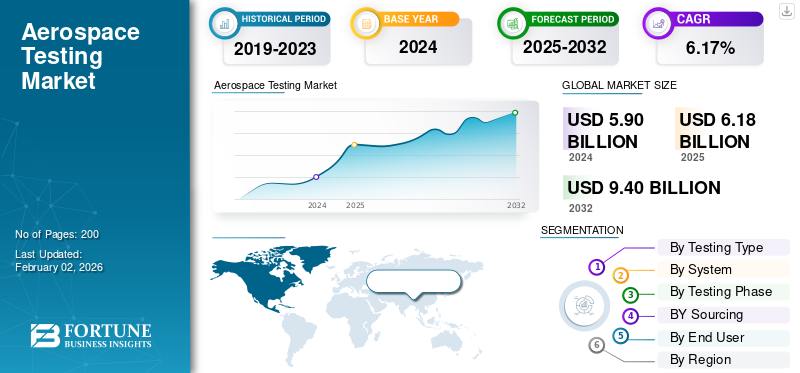

The global aerospace testing market size was valued at USD 6.2 billion in 2025. The market is projected to grow from USD 6.5 billion in 2026 to USD 10.50 billion by 2034, exhibiting a CAGR of 6.10% during the forecast period. North America dominated the aerospace testing market with a market share of 45.00% in 2025.

The market encompasses all activities that validate the safety, durability, and performance of aircraft, spacecraft, and their subsystems. It spans the entire product lifecycle from early design and certification to production testing and ongoing maintenance checks. Testing covers structural loads, vibration, fatigue, propulsion, avionics, and environmental performance, using both physical trials and advanced digital simulations. Non-destructive testing, thermal and acoustic evaluation, and electromagnetic compatibility checks have become routine as aircraft systems grow more complex and software-driven. These processes ensure that every component meets the rigorous standards set by authorities such as the FAA, EASA, and NASA.

Key players include Boeing, Airbus, Safran, GE Aerospace, Rolls-Royce, Honeywell, Lockheed Martin, and Northrop Grumman, supported by NASA, ESA, and leading defense research organizations. Independent laboratories and certification bodies such as Element Materials Technology, Applus+, and Bureau Veritas also contribute to qualification testing and compliance audits. As next-generation aircraft become more digital, electric, and autonomous, the demand for precise testing continues to rise, making this field a vital link between innovation, regulatory approval, and flight safety.

Download Free sample to learn more about this report.

Aerospace Testing Market Key Takeaways

- 2025 Market Size: USD 6.2 Billion

- 2026 Market Size: USD 6.5 Billion

- 2034 Forecast Market Size: USD 10.50 Billion

- CAGR: 6.10% from 2026–2034

- North America dominated the aerospace testing market with a market share of 45.00% in 2025.

- The structural testing segment is projected to dominate the market with a share of 24.35% in 2026.

- The structural systems segment is projected to dominate the market with a share of 30.17% in 2026.

North America

North America recorded a market size of USD 2.8 Billion in 2025, capturing 45.00% of the global market share, and is projected to reach USD 2.95 Billion in 2026.

Europe

Europe accounted for USD 1.39 billion in 2025, driven by mature aerospace manufacturing capabilities, aircraft modernization initiatives, and stringent certification standards.

Asia Pacific

Asia Pacific generated USD 1.06 billion in 2025 and is witnessing strong growth due to expanding aerospace production, defense modernization, and increasing investments in domestic aviation programs.

U.S.

The market was valued at USD 2.00 billion in 2026, supported by major aerospace OEMs, government-backed research facilities, and growing investments in next-generation aircraft and space programs.

Japan

The market is projected to reach USD 0.20 billion in 2026, driven by increasing aerospace innovation, strengthening certification requirements, and continued investments in advanced aviation technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growing Demand for Structural and NDT Validation Across Aerospace Systems Drives Market Growth

Aerospace programs today are under greater pressure than ever to prove safety, performance, and life-cycle reliability. With each new airframe, propulsion system, or launch vehicle, extensive testing is required before certification. Structural, vibration, fatigue, and material strength assessments remain the backbone of these efforts, ensuring that wings, fuselage panels, and propulsion mounts can withstand years of stress and extreme conditions. Simultaneously, Non-Destructive Testing (NDT) methods such as ultrasonic, radiographic, and eddy-current inspection are expanding rapidly, as both OEMs and MRO providers rely on them for quality assurance and in-service checks. The growing use of composite and additive-manufactured components has amplified the need for precise flaw detection techniques. Regulatory bodies such as the FAA, EASA, and ESA mandate stringent validation routines, making testing a non-negotiable step in every project.

MARKET RESTRAINTS

Capital Intensity and Limited Testing Infrastructure Hinder Market Expansion

Aerospace testing remains one of the most capital-heavy segments of the industry. Building large structural rigs, propulsion test cells, acoustic chambers, or thermal-vacuum facilities requires multimillion-dollar investments and continuous calibration to maintain certification validity. Many national laboratories and OEMs operate near full capacity, leading to scheduling bottlenecks for both development and maintenance programs. Smaller suppliers and new entrants often depend on third-party laboratories, which increases project timelines and costs. Maintenance of complex test instrumentation, data-acquisition systems, and high-temperature enclosures adds further overhead. In propulsion and launch testing, fuel safety and exhaust-handling regulations increase the cost even more.

MARKET OPPORTUNITIES:

Rising Composite, Propulsion, and Space Exploration Programs Offer New Market Opportunities

The shift toward lighter, stronger materials and advanced propulsion architectures is creating a wave of new testing requirements. Composite primary structures, hybrid metallic assemblies, and additive-manufactured components must undergo specialized fatigue and material property testing to verify durability and bonding integrity. The propulsion segment, ranging from high-bypass turbofans to reusable rocket engines, demands complex thermal, vibration, and combustion environment tests. Simultaneously, growing satellite and launch activity is expanding the market for environmental, acoustic, and shock testing, particularly under vacuum and cryogenic conditions. Defense modernization programs are adding new missile and propulsion test campaigns, while commercial manufacturers continue to expand fatigue and damage-tolerance evaluations for extended life certification.

AEROSPACE TESTING MARKET TRENDS:

Integration of Digital Tools and Advanced NDT Redefines Test Operations, Driving Market Trends

Aerospace testing is rapidly transitioning toward a hybrid model that blends physical experimentation with digital insight. Digital twins, advanced simulation, and high-fidelity sensor networks now complement traditional structural and propulsion tests, allowing engineers to predict performance before full-scale validation. Non-destructive testing has evolved from manual inspection to automated, AI-assisted analysis using phased-array ultrasonics, digital radiography, and thermography. These technologies enable continuous monitoring of airframes and engines throughout their life cycle, turning maintenance into a data-driven process.

MARKET CHALLENGES:

Skilled Personnel and Data Integration Remain Persistent Barriers to Hamper Market Growth

As testing technologies become more sophisticated, the demand for specialized expertise has outpaced supply. Operating a large structural test frame, calibrating ultrasonic NDT systems, or managing high-temperature propulsion trials requires deeply experienced engineers who understand both aerospace design and regulatory standards. Many regions face shortages of qualified technicians, particularly in non-destructive inspection, materials analysis, and thermal-vacuum operations. At the same time, test campaigns now produce immense amounts of sensor data, strain, vibration, temperature, and acoustics, creating challenges in data management, traceability, and cybersecurity. Integrating results from physical tests with digital simulations is still difficult, as data formats and calibration practices vary among OEMs and suppliers.

US Tariff Impact

U.S. tariffs on metals, electronic components, and imported machinery have a ripple effect on the market. Higher costs for aluminum, titanium, sensors, and precision instruments increase the price of structural and material testing equipment, raising operational expenses for test facilities and OEMs. Tariffs also disrupt global supply chains, delaying delivery of specialized components needed for fatigue rigs and NDT systems. While domestic equipment suppliers benefit marginally, testing service providers face squeezed margins and longer project timelines. Overall, tariffs heighten program costs and slow the modernization of test infrastructure, particularly for smaller independent laboratories dependent on imported systems.

Download Free sample to learn more about this report.

Segmentation Analysis

By Testing Type

Rising Airframe Production and Lightweight Design Requirements Drive Growth in Structural Testing Segment

On the basis of the testing type segmentation, the market is classified into material testing, structural testing, environmental testing, acoustic testing, vibration & shock testing, Electromagnetic Compatibility (EMC) Testing, Non-Destructive Testing (NDT), and software & simulation testing.

The structural testing segment is projecteed to dominate the market with a share of 24.35% in 2026. Growth in this segment is driven by the continuous development of lighter, high-strength airframes made from advanced composites and hybrid alloys.

The material testing segment is expected to grow at a 5.70% CAGR during the forecast period.

By System

Increased Use of Composite Airframes and Fatigue Life Extension Programs Boost Growth of Structural Systems Segment

In terms of system, the market is categorized into structural systems, propulsion systems, avionics systems, launch systems, and others.

The structural systems segment is projecteed to dominate the market with a share of 30.17% in 2026. Advanced joining methods such as additive manufacturing and bonded structures require new forms of durability and damage-tolerance evaluation.

The propulsion systems segment is expected to record a CAGR of 20.93% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Testing Phase

Continuous Aircraft Development and Certification Programs Strengthen Demand for Development & Certification Testing Segment

Based on the testing phase, the market is segmented into development & certification testing, production & quality assurance testing, and operational & maintenance testing.

The development & certification testing segment is projecteed to dominate the market with a share of 65.02% in 2026. The segment dominated the aerospace testing cycle and continues to grow steadily with each new aircraft, engine, or satellite program.

The segment of operational & maintenance testing is set to flourish and is growing at a CAGR of 20.41% over the forecast period.

By Sourcing

OEMs’ Focus on Quality Control and Data Security Supports Expansion of In-House Testing Segment

Based on sourcing, the market is segmented into in house testing, outsourced testing, and collaborative testing.

The in house testing segment is projecteed to dominate the market with a share of 42.63% in 2026. This segment remains the preferred mode for major aerospace manufacturers and defense agencies due to its direct control over quality, data security, and regulatory compliance.

The segment of outsourced testing is set to flourish with the highest growth rate of 21.84% during the forecast period.

By End User

New Aircraft Deliveries and Advanced Platform Development Propel Growth of OEM End-User Segment

Based on end-user, the market is segmented into OEM, MRO, defense agencies, space agencies, and others.

The OEM segment held the dominating position in 2024. Original Equipment Manufacturers (OEMs) represent the largest and most influential customer base for aerospace testing services. Their growth is tied directly to increasing aircraft and engine production, the rollout of next-generation designs, and the push for greater fuel efficiency.

The segment of defense agencies is set to flourish with a growth rate of 21.29% over the forecast period.

Aerospace Testing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America Aerospace Testing Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America recorded a market size of USD 2.8 Billion in 2025, capturing 45.00% of the global market share, and is projected to reach USD 2.95 Billion in 2026. The region is projected to expand to USD 2.95 billion in 2026, supported by its highly developed aerospace ecosystem and extensive testing infrastructure. The U.S., valued at USD 2.00 billion in 2026, remains the primary growth engine due to the presence of major OEMs, government-backed research facilities, and defense testing programs. Stringent regulatory standards governing aircraft certification, safety validation, and defense compliance continue to drive demand for advanced testing solutions, while increasing investments in next-generation aircraft and space programs further strengthen market expansion.

Europe

In 2025, Europe represented USD 1.39 Billion, accounting for 22.48% of the worldwide market, and is projected to grow to USD 1.46 Billion in 2026. The region benefits from a mature aerospace manufacturing base, strong participation in commercial aviation programs, and a robust regulatory framework focused on safety, environmental compliance, and airworthiness standards. The U.K. and Germany, valued at USD 0.50 billion and USD 0.37 billion respectively in 2026, remain key contributors to regional growth. Demand for aerospace testing is being supported by ongoing aircraft modernization initiatives, rising investments in sustainable aviation technologies, and increased emphasis on certification processes for advanced aerospace systems.

Asia Pacific

The Asia Pacific market generated USD 1.06 Billion in 2025, representing 17.10% of the global market landscape, and is expected to reach USD 1.13 Billion in 2026. The region is witnessing rapid expansion due to accelerating industrialization, defense modernization programs, and growing investments in domestic aerospace manufacturing capabilities. China, Japan, and India are projected to reach market values of USD 0.39 billion, USD 0.20 billion, and USD 0.29 billion respectively in 2026. Regulatory authorities across the region are increasingly strengthening certification and quality assurance requirements to support expanding aviation activities. Rising aircraft production, increasing defense procurement, and the emergence of indigenous aerospace development programs are expected to sustain strong demand for testing services and technologies.

Latin America

Latin America is projected to experience moderate growth, with the market estimated at USD 0.29 billion in 2025. Regional demand is supported by gradual modernization of aviation infrastructure, fleet expansion activities, and increasing focus on operational safety standards. Regulatory agencies are enhancing oversight of aircraft maintenance and certification procedures, encouraging greater adoption of aerospace testing solutions. While the region remains smaller in scale compared to developed markets, ongoing investments in commercial aviation and defense sectors are expected to contribute to steady market development.

Middle East & Africa

Middle East & Africa is anticipated to witness stable growth, reaching a market value of USD 0.65 billion in 2025. Growth is primarily driven by expanding aviation networks, increasing defense expenditure, and strategic investments in aerospace capabilities across key economies. Regulatory bodies are progressively aligning with international aviation safety and certification standards, supporting the need for advanced testing and validation services. Rising aircraft procurement programs, airport expansion projects, and growing participation in aerospace maintenance and repair activities are expected to create sustained demand for aerospace testing solutions throughout the forecast period.

Rest of the World

The market in Rest of the World reached USD 0.9 Billion in 2025, representing 0.151% of total market revenue, and is projected to reach USD 1 Billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Extensive R&D and Collaborative Testing Programs Define Competitive Landscape

The global market is moderately consolidated, led by major OEMs and specialized testing organizations that combine in-house expertise with collaborative research. Key players Element Materials Technology, Applus+ Laboratories, Bureau Veritas, SGS SA, Southwest Research Institute (SwRI), and National Aerospace Solutions, supported by testing and certification firms such as Element Materials Technology, Applus+, Bureau Veritas, and SGS. Defense and space agencies such as NASA, ESA, and DRDO also play pivotal roles through shared infrastructure and co-development projects. Continuous investment in R&D, automation, and advanced NDT technologies enables these companies to enhance precision, reduce testing cycles, and meet evolving aerospace safety and certification requirements.

LIST OF KEY AEROSPACE TESTING COMPANIES PROFILED:

- Element Materials Technology (U.K.)

- Applus+ Laboratories (Spain)

- Bureau Veritas (France)

- SGS SA (Switzerland)

- Southwest Research Institute (SwRI) (U.S.)

- National Aerospace Solutions (U.S.)

- Intertek Group plc (U.K.)

- Mistras Group, Inc. (U.S.)

- NTS (National Technical Systems) (U.S.)

- Eurofins EAG Laboratories (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2024: Astrion revealed that Beyond New Horizons, LLC (BNH), an Astrion Joint Venture (JV) with Fluor, was granted the Test Operations and Sustainment (TOS) II contract worth over USD 3.7 billion by the U.S. Air Force.

- November 2024: Sierra Lobo, Inc. of Fremont, Ohio, has been chosen by NASA to handle technical system maintenance, test operations, and test support at the agency's Stennis Space Center. The NASA Stennis Test Operations Contract is a level-of-effort, fixed-price agreement worth roughly USD 47 million.

- October 2025- The U.S. Air Force has awarded Peraton a USD 980 million multiple-award, indefinite-delivery, indefinite-quantity contract to support its global network of automatic testing systems.

- May 2025: Southwest Research Institute, a nonprofit organization established in San Antonio, was given a USD 250 million contract by the U.S. Department of Defense to support the Center for Aircraft Structural Life Extension at the U.S. Air Force Academy in Colorado.

- February 2024: Willick Engineering Co, Inc., a supplier of Non-Destructive Testing (NDT) X-ray equipment and provider of related services to the military, aerospace, and medical device sectors, has been acquired by Pinnacle X-Ray Solutions, LLC, a manufacturer of non-destructive testing and inspection systems, with its headquarters located in Santa Fe Springs, CA.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key aerospace testing industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.10% from 2026-2034 |

| Unit | Value (USD Billion ) |

| Segmentation | By Testing Type, System, Testing Phase, Sourcing, End User, and Region |

| By Testing Type |

|

| By System |

|

| By Testing Phase |

|

| By Sourcing |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.2 billion in 2025 and is projected to reach USD 10.50 billion by 2034.

In 2025, the market value stood at USD 2.8 billion.

The market is expected to exhibit a CAGR of 6.10% during the forecast period of 2026-2034.

The structural system segment led the market by system type.

Growing demand for structural and NDT validation across aerospace systems is a primary cause for market growth.

Element Materials Technology, Applus+ Laboratories, Bureau Veritas, SGS SA, Southwest Research Institute (SwRI), and National Aerospace Solutions are some of the prominent players in the market.

North America dominated the market with the largest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us