Agricultural Chelates Market Size, Share & Industry Growth Report, By Chelate Type (Synthetic, & Organic/Bio based Chelates), By Formulation (Liquid Chelates, Powdered Chelates, Capsulated Chelates, & Combination Products), By Nutrient Type (Iron, Zinc, Manganese, Copper, Magnesium, & Calcium Chelates, & Micronutrient Blends), By Mode of Application (Soil treatment, Foliar Spray, Fertigation, Seed Treatment, & Post-harvest Treatment), By End Use (Commercial Agriculture, Smallholder & Subsistence Farming, Horticulture, Floriculture, & Others), By Crop Type, and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

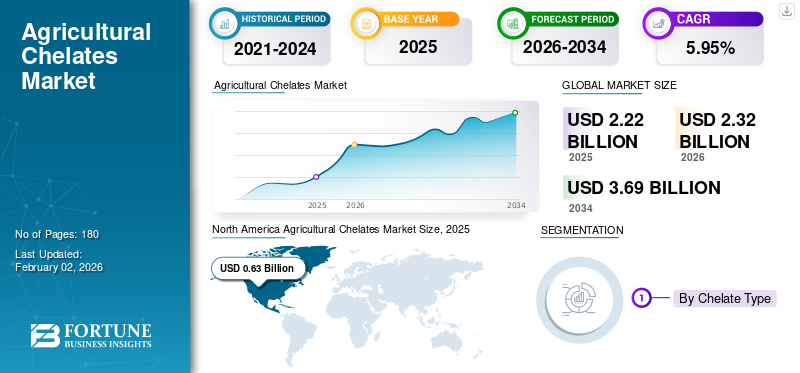

The global agricultural chelates market size was valued at USD 2.22 billion in 2025 and is projected to grow from USD 2.32 billion in 2026 to USD 3.69 billion by 2034, registering a CAGR of 5.95% over the forecast period. North America dominated the agricultural chelates market with a market share of 28.36% in 2025.

Agricultural chelates are compounds that are used in farming to improve the availability and absorption of plant micronutrients. Such products are highly suitable for alkaline and calcareous soils where the micronutrients are present in insoluble forms. Some of the common chelating agents used in agriculture include EDTA, DTPA, EDDHA, IDHA, GLDA, and others. Growing emphasis on enhancing global food security is expected to boost the usage of such products for enhancing crop yield.

Companies such as BASF SE, Syngenta, and Nouryon are some of the well-known players operating to meet the growth in agricultural chelates demand. Soil degradation and micronutrient deficiencies in key agricultural regions are driving increased demand for agricultural chelates.

Download Free sample to learn more about this report.

Agricultural Chelates Market Key Takeaways

- 2025 Market Size: USD 2.22 billion

- 2026 Market Size: USD 2.32 billion

- 2034 Forecast Market Size: USD 3.69 billion

- CAGR: 5.95% from 2026–2034

- North America dominated the agricultural chelates market with a 28.36% share in 2025.

- The Synthetic Chelates segment is projected to account for 70.56% of the global market share in 2026.

- The Iron Chelates segment represented 36.45% of the global market share in 2026.

North America

North America market representing 28.36% of global demand, and is projected to grow to USD 0.66 billion in 2026 & is supported by widespread precision farming practices and strong demand for micronutrient management solutions.

Asia Pacific

Asia Pacific accounting for 22.60% share, and is expected to reach USD 0.52 billion in 2026, driven by rising adoption of high-efficiency fertilizers and increasing horticulture crop production across the region.

Europe

Europe captured 21.83% of the global market in 2025, and is projected to reach USD 0.51 billion in 2026 & is expected to witness steady growth, supported by sustainable farming initiatives and regulatory compliance requirements.

U.S.

The market is projected to reach USD 0.47 billion by 2026, supported by the need to address micronutrient deficiencies across major agricultural regions.

Japan

The market is projected to reach USD 0.07 billion by 2026, driven by the adoption of advanced agricultural practices and the demand for improved crop productivity.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Inputs that Help Generate High Yield Fuels Market Growth

Optimized use of agricultural inputs helps farmers increase crop yield and improve their profit margins. In recent years, as the global population continues to increase, there is a growing need to increase food production and security. As the agricultural land is limited, the farmers have to produce more crops from such a limited crop area. Thus, demand for inputs that can help farmers produce that is of export quality motivates them to use such products that help to enhance crop yield and improve crop appearance. Thus, the demand for such products is expected to continue in the future as well. Rising pressure to boost agricultural productivity is accelerating the demand for high-efficiency fertilizers, driving the agricultural chelates market growth globally.

MARKET RESTRAINTS

High Cost Of Products Impacts Adoption Rate and Impedes Growth

Chelated products are expensive compared to other traditional non-chelated fertilizers, which forces farmers to use these products optimally. The high cost of such products is mainly attributed to the complex manufacturing process, the high cost of raw materials such as organic acids, chelating agents, maintaining product quality, and others. As farmers have limited investment money, the use of chelating agents becomes expensive for long-term usage.

MARKET OPPORTUNITIES

Growing Popularity of Sustainable Agriculture Creates Opportunity to Expand Product Lines

The government is supporting farmers with different agricultural advice and inputs to shift toward sustainable agricultural practices and adopt environmentally safe inputs. Bio-based chelates are environmentally safe and help to deliver micronutrients efficiently to the crops, enhancing the crop yield and soil health. Biodegradable chelating agents are environmentally friendly alternatives to traditional synthetic chelates (such as EDTA), designed to degrade naturally in the soil without leaving harmful residues. Such inputs are also suitable for organic farming, and this creates an opportunity for the farmers to develop products for organic farming that help to meet the increasing consumer preference for organic produce.

AGRICULTURAL CHELATES MARKET TRENDS

Integration of Advanced Technology Compatible Formulations to Boost Market Demand

Adoption of advanced agricultural techniques is impacting the methods through which such agricultural inputs are applied to the crops. As the adoption of precision agricultural techniques is on the rise and advanced instruments such as drones, soil sensors, and GPS are increasingly being used for fertilizer delivery to the crops, manufacturers are developing chelating formulations that are compatible with such technology and can be applied to the crops easily.

- In April 2025, France is using drone-compatible chelate formulations for precision application. This method allowed applying these products in around 800 hectares of vineyards in France.

Download Free sample to learn more about this report.

Segmentation Analysis

By Chelate Type

Synthetic Products Account for Largest Market Share Owing to their Stability Across Different Soil pH Levels

The market is divided by chelate type into synthetic and organic. Synthetic types are further segmented into EDTA, DTPA, EDDHA, and others. Organic types are further divided into amino acids, acid chelates, lignosulfonates, and heptagluconates.

The Synthetic Chelates segment is projected to reach the market by chelate type, accounting for 70.56% of the global market share in 2026. Such products remain stable over a wide pH range of oil, and hence, they help to ensure that the plants receive the necessary micronutrients at every soil condition. As they provide better crop yield even with minimal application, they become cost-effective for farmers.

The organic chelates segment is expected to grow at a CAGR of 6.20% over the forecast period. They are biodegradable and environment friendly, hence popular among farmers who are adopting sustainable agricultural practices for farming.

By Mode of Application

Foliar Spray are More Popular Due to its Rapid Correction of Nutrient Deficiencies in Soil

The market is segmented by mode of application into soil treatment, foliar spray, fertigation, seed treatment, and post-harvest treatment.

Foliar sprays segment is projected to reach 35.47% of the market share in 2026. This application method allows nutrients to be sprayed on the leaves of the crops, and they are rapidly absorbed by the plants, which eases the process of correcting nutritional deficiencies. Some soil may also have poor drainage, which can lead to nutrient loss and environmental pollution. Applying fertilizer by this method helps to prevent such issues and enhance crop yield.

Soil treatment is another popular method for applying agricultural inputs to the soil. It is expected to grow by 5.67% during the forecast period. Applying chelates through this process supports the nutrient needs of the plants over a longer period and their growth.

By Nutrient Type

Wide Usage of Iron Chelates Contributes to its High Market Share

Based on nutrient type, the market is segmented into iron (Fe) chelates, zinc (Zn) chelates, manganese (Mn) chelates, copper (Cu) chelates, magnesium (Mg) chelates, calcium (Ca) chelates, and micronutrient blends.

The Iron Chelates segment is projected to reach 36.45% of the global market share in 2026. Iron deficiency is widespread in the soil, and iron is often unavailable to plants as it is present in forms that are not bioavailable. Chelated iron remains stable in different pH levels, enabling quick and effective nutritional deficiency correction.

Apart from iron deficiency, zinc deficiency is another major deficiency impacting the soil. Hence, zinc chelate is another type of product widely used in nutritional deficiency correction, accounting for a CAGR of 5.59% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Formulation

Powdered Formulation Accounted for Higher Market Share Owing to Longer Shelf Life and Lower Cost

On the basis of the formulation, the market is segregated into liquid chelates, powdered chelates, capsulated chelates, and combination products.

Powdered chelates will account for the largest market share in 2024. Compared to liquid formulations, these products have a long shelf life and are resistant to degradation over time. Moreover, they are cheaper to manufacture and can be transported easily. These products can also be easily applied to both conventional and organic agricultural products, leading to higher crop yields.

Liquid formulations are expected to grow 5.88% during the forecast period, the fastest growth rate in this category. These products can be easily applied to crops through drip irrigation, foliar spray, and hydroponics. This helps reduce farmers' reliance on labor and the cost of application.

By Crop Type

Cereals and Grains Exhibited a Majority Share Attributed to Strong Usage by Farmers to Improve Crop Yield

The market is segregated into cereals and grains, fruits and vegetables, oilseeds and pulses, and others based on crop type. Cereals and grains are further divided into wheat, rice, corn, barley, and others. Fruits and vegetables are further divided into citrus, berries, vine crops, root vegetables, and others. Oilseeds and pulses are further divided into soybeans, sunflowers, lentils, peas, and others.

The Cereals & Grains crop type segment accounted for 33.74% of the market share in 2026. Wheat, barley, and maize suffer from zinc and iron deficiencies owing to poor soil quality, and such deficiencies are widespread in Asian and African countries. The use of such inputs helps to improve root and shoot growth and enhance grain size and weight.

Fruits and vegetables account for the second-highest market share, owing to the growing need to maximize yield and quality of fruits and ensure better marketability of the crops. The segment is projected to grow at a CAGR of 5.78% during the study period.

By End Use

Commercial Agriculture to Exhibit a Majority Share Attributed to Nutrient Depletion Caused by Intensive Farming

The market is segregated into commercial agriculture, smallholder and subsistence farming, horticulture, floriculture, and others based on the end use.

Commercial agriculture is the largest user of such products owing to large-scale farming operations, which help to enhance efficiency, increase crop yield, and ensure high product quality. This is one reliable method to optimize micronutrient availability and is suitable for poor-quality soil. As intensive farming causes nutrient depletion of soil, these micronutrient-rich chelates help to maintain soil quality. These fillings help maintain uniformity and product consistency and ensure that products have a higher shelf life.

Horticulture is expected to register a growth of 5.50% during the forecast period. As these crops require high nutrient demand and are sensitive to nutrient deficiencies, such products are popular among farmers.

Agricultural Chelates Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

NORTH AMERICA

North America Agricultural Chelates Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 0.63 billion, representing 28.36% of global demand, and is projected to grow to USD 0.66 billion in 2026. The region is highly industrialized and generates a significant amount of crop yield through the use of precision farming. Such products also help to ensure solubility, stability, and compatibility of the products with the advanced agriculture equipment used by the farmers in the region. In the U.S. regions such as the Midwest, the Great Plains, and the western U.S. have high micronutrient deficiency, which is mitigated through the use of chelated products. The U.S. market is projected to reach USD 0.47 billion by 2026. Therefore, the agricultural chelates market analysis reveals a strong growth trajectory driven by strong demand among farmers in the region.

ASIA PACIFIC

Asia Pacific maintained a strong presence in the global market, reaching USD 0.5 billion in 2025, accounting for 22.60% share, and is expected to reach USD 0.52 billion in 2026. Countries such as China, India, and Southeast Asian countries suffer from zinc, iron, and boron deficiencies, which help to reduce soil degradation that has been caused by the intensive agricultural farming conducted in the region over the decades. The growing demand for high-efficiency fertilizers is fueling the expansion of the agricultural chelates market, as farmers seek solutions that improve nutrient uptake and crop performance. Moreover, there is a rapid expansion of horticulture crop production in the region, and chelates can be easily applied to such crops through drip irrigation, foliar treatment, and others. The Japan market is projected to reach USD 0.07 billion by 2026, the China market is projected to reach USD 0.24 billion by 2026, and the India market is projected to reach USD 0.10 billion by 2026.

EUROPE

The Europe region captured 21.83% of the global market in 2025, generating USD 0.48 billion in revenue, and is projected to reach USD 0.51 billion in 2026. The level of micronutrient deficiency in the soil of the region is less several in comparison to Asia and North American countries. Moreover, the region also has stringent regulatory guidelines, and manufacturers need to conform to the strict environmental regulations established in the country. This discourages farmer from using synthetic products, including synthetic chelates, in their soil. During the forecast period, the European region is projected to record a growth rate of 7.18%. The UK market is projected to reach USD 0.06 billion by 2026 and the Germany market is projected to reach USD 0.12 billion by 2026.

SOUTH AMERICA and MIDDLE EAST & AFRICA

Over the forecast period, South America and the Middle East & Africa regions would witness a moderate growth in this market. The Middle East & Africa market accounted for USD 0.29 billion in 2025, representing 13.00% of the global industry, and is expected to reach USD 0.3 billion in 2026. The South America market in 2025 is set to record USD 0.32 billion as its valuation. As the farmers in the region are predominantly small holders and agricultural chemicals are expensive, the usage rate of such products is still limited. Data-driven farming practices are increasing the demand for high-efficiency fertilizers, further propelling the growth of the agricultural chelates market to enhance agricultural productivity. In the Middle East & Africa, South Africa is set to grow at a CAGR of 5.31% during the forecast period.

Latin America

In 2025, Latin America represented USD 0.32 billion, accounting for 14.30% of the worldwide market, and is projected to grow to USD 0.33 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Specialized Crop Solution Launched By Companies Is a Key Strategy Adopted by Key Manufacturers

The global market exhibits a consolidated structure due to the presence of several multinational companies and a limited number of local/regional players competing with each other for higher market share. Manufacturers invest heavily in developing environmentally safe, biodegradable chelates that meet tightening regulations, especially in Europe and parts of Asia. Companies are focused more narrowly on plant nutrition and soil health to provide a specialized solution to the farmers. This includes companies such as Valagro, ATP Nutrition are some of the manufacturers developing specialty chelates for different regions. Large multinational companies such as BASF, Syngenta, and others are manufacturing chelates and integrating them into their product portfolio and broadening their product offerings for farmers in different countries/regions. The market for agricultural chelates is expanding rapidly, driven by rising soil micronutrient deficiencies, sustainable farming practices, and the demand for higher crop yields.

LIST OF KEY AGRICULTURAL CHELATE COMPANIES PROFILED

- Nouryon (Amsterdam)

- BASF SE (Germany)

- Syngenta (Switzerland)

- Yara International ASA (Norway)

- Haifa Group (Israel)

- AkzoNobel N.V. (Netherlands)

- Nufarm Limited (Australia)

- Aries Agro Limited (India)

- Van Iperen International (Netherlands)

- Deretil Agronutritional (Spain)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Bayer Crop Science launched new generation crop health product in the market named Wojiarun in the Chinese market. The calcium fertilizer which is a part of this product line was upgraded from ionic state to a complex and chelated state which is easy to use.

- August 2024: CHS Inc. launched six new products in the U.S. market. It launched chelating agent Levesol in the market which helps to improve the availability of micronutrients to the crops.

- August 2024: CHS Inc. introduced six new micronutrient fertilizer named New Trivar EZ that contained Levesol chelating agent which helps to improve the crop yield.

- July 2024: Coromandel International Limited launched new magnesium fortified complex fertilizer named “Paramfos Plus” in the Indian market. These fertilizers contains 16% Nitrogen, 20% Phosphorus, and 13% Sulphur, along with an additional 0.6% Magnesium.

- August 2022: Innospec launched ENVIOMET C which is a product line of chelating agent biofertilizers that is available in powder and liquid form. The product is suitable for horticulture, arable crops, and seed dressing.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.95% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use , and Region |

|

By Chelate Type |

|

|

By Formulation |

|

|

By Crop Type |

|

|

By Mode of Application |

|

|

By Nutrient Type |

|

|

By End Use |

|

|

By Region |

North America (By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use, and Country)

Europe (By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use and Country)

Asia Pacific (By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use and Country)

South America (By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use and Country)

Middle East and Africa (By Chelate Type, Formulation, Crop Type, Mode of Application, Nutrient Type, End Use and Country)

Rest of the Middle East & Africa (By Formulation) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.22 billion in 2025 and is projected to grow from USD 2.32 billion in 2026 to USD 3.69 billion by 2034

In 2025, the market value stood at USD 0.63 billion.

The market is expected to exhibit a CAGR of 5.95% during the forecast period of 2026-2034.

By chelate type, the synthetic segment led the global market in 2024.

Growing demand for inputs that help generate high yield fuels the market growth.

BASF SE, Syngenta and Nouryon are a few of the key players in the market.

North America held the largest market share in 2024.

Integration of advanced technology compatible formulations to Boosts Market Demand.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us