AI in Bioinformatics Market Size, Share & Industry Analysis, By Component (Software & Services), By Deployment (Cloud-based, On-Premise, & Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing, & Others), By Application (Genomics & Sequence Analysis, Multi-omics Analysis, Protein Structure & Functional Analysis, Drug Discovery & Molecular Design, Clinical Genomics / Precision Medicine, & Others), By End User (Pharmaceutical & Biotechnology Companies, CROs/CDMOs, Academic & Research Institutes, & Others), and Regional Forecast, 2026-2034

AI in Bioinformatics Market Size and Future Outlook

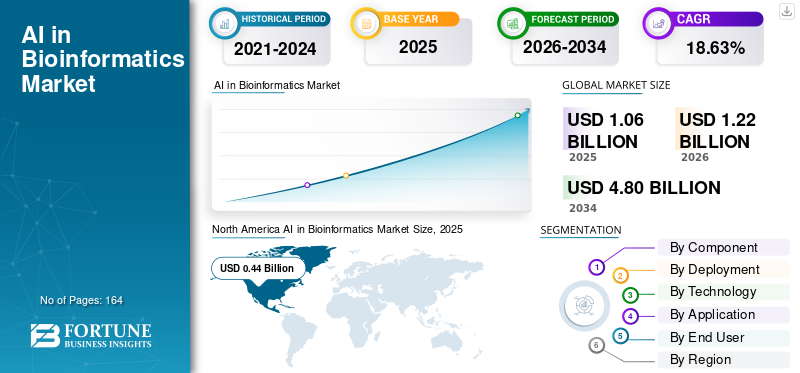

The global AI in bioinformatics market size was valued at USD 1.06 billion in 2025. The market is projected to grow from USD 1.22 billion in 2026 to USD 4.80 billion by 2034, exhibiting a CAGR of 18.63% during the forecast period. North America dominated the AI in bioinformatics market with a market share of 41.51% in 2025.

Artificial intelligence in bioinformatics involves applying AI to assess and comprehend biological information. It enhances variant interpretation, multi-omics integration, biomarker identification, protein function prediction, and drug target or molecule discovery, while also facilitating scalable cloud-based analysis and quicker research decision-making. The market's expansion is driven by the increasing volume of sequencing and multi-omics data, the increasing application of AI in drug discovery and precision medicine, and the rising need for cloud-based bioinformatics platforms capable of handling large-scale complex biological datasets.

Key participants in the market consist of Illumina, Tempus, SOPHiA GENETICS, DNAnexus, and Fabric Genomics. These firms are concentrating on AI-enhanced genomics analysis, clinical decision-making assistance, precision health data systems, multi-omics analysis, and cloud-supported research processes.

Download Free sample to learn more about this report.

AI in Bioinformatics Market Key Takeaways

- 2025 Market Size: USD 1.06 billion

- 2026 Market Size: USD 1.22 billion

- 2034 Forecast Market Size: USD 4.80 billion

- CAGR: 18.63% from 2026-2034

- North America dominated the AI in bioinformatics market with a 41.51% share in 2025.

- The services segment is projected to grow at a CAGR of 19.82% during the forecast period.

- The hybrid segment is expected to expand at a CAGR of 19.14% during the forecast period.

North America

North America accounted for USD 0.44 billion in 2025, maintaining its leading position in the global market.

Europe

Europe is projected to expand at a CAGR of 17.08% during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 0.29 billion in 2026.

U.S.

The market is estimated to reach USD 0.47 billion in 2026, representing around 38.0% of global revenue.

Japan

The market is estimated to reach USD 0.04 billion in 2026, accounting for approximately 3.6% of global revenue.

Read More

AI IN BIOINFORMATICS MARKET TRENDS

Growing Focus on Precision Medicine is a Key Market Trend

An increasing emphasis on precision medicine is a significant trend in the AI in bioinformatics sector, as healthcare and life sciences organizations are progressively moving away from generic treatment approaches toward data-informed, personalized care. This highlights the necessity for AI tools capable of analyzing genomic, transcriptomic, clinical, and other biological data collectively to identify disease patterns and treatment responses more accurately. With the expansion of precision medicine initiatives, there is a growing need for AI-driven platforms that facilitate biomarker discovery, molecular profiling, patient categorization, and therapy selection. This trend is promoting broader adoption of cloud-based bioinformatics platforms capable of handling extensive multimodal datasets effectively. Moreover, pharmaceutical and biotechnology firms are employing AI in bioinformatics to speed up targeted drug development and enhance clinical decision-making support. Consequently, precision medicine is emerging as a key long-term growth engine for this market. These factors are supporting the overall global AI in bioinformatics market growth.

- For instance, in April 2025, Illumina Inc. and Tempus collaborated to combine Illumina’s AI technologies with Tempus’ multimodal data platform to accelerate clinical adoption of molecular testing and advance precision medicine.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Drug Discovery Acceleration & Genomic Data Expansion is Propelling Market Growth

The swift advancement of drug discovery and the growth of genomic data are significant factors driving the market, as life sciences firms generate far more sequencing, multi-omics, and biological pathway data than conventional tools can effectively manage. This amplifies the demand for AI-driven bioinformatics platforms that can swiftly analyze complex datasets, uncover hidden patterns, and reduce the time needed for target discovery and molecule selection. As drug developers aim to enhance R&D efficiency, AI is increasingly used to link genomic findings to disease mechanisms, support biomarker discovery, and rank candidates. Concurrently, the growing volume of genomic data is driving organizations to adopt automated and cloud-based analysis systems. This is boosting the need for AI-driven software and services in genomics, multi-omics, and molecular design processes. Consequently, the integration of increasing biological data and the urgency to hasten drug discovery are directly driving market expansion. All these factors cumulatively drive the overall market growth.

- For instance, in January 2025, Illumina Inc. introduced new omics and data analytics solutions to unlock deeper biological understanding and support faster discovery across genomics and multiomics research.

MARKET RESTRAINT

Limited Availability of Skilled Personnel to Hamper Market Growth

The restricted access to experts with a blend of AI, biology, and bioinformatics skills poses a significant limitation for the sector, as these platforms demand unique proficiencies in data science, genomics, computational biology, and model analysis. Many end users can use AI tools, but they often struggle to implement them effectively without trained bioinformaticians and AI experts. This hinders implementation, diminishes the pace of workflow integration, and raises reliance on external service providers. The difficulty is even greater in emerging markets and public research environments, where attracting and keeping skilled professionals remains a challenge. As biological datasets grow in complexity, the lack of multidisciplinary specialists can negatively impact the quality of results, model validation, and regulatory trust. This results in a divide between the availability of technology and its practical use, which may hinder market growth.

- For instance, according to a Nature Medicine article published in September 2025, although African countries have expanded genomics and bioinformatics training, major barriers still threaten workforce retention and long-term sustainability.

MARKET OPPORTUNITIES

Rising Investments in Biotechnology Research to Offer Market Growth Opportunities

Rising investments in biotechnology research are creating a major opportunity for the market, as research programs are producing larger and more complex genomic, single-cell, and multi-omics datasets that need advanced analysis tools. As biotechnology companies increase spending on discovery platforms, translational research, and precision medicine programs, demand is rising for AI-based bioinformatics software that can speed up target identification, biomarker discovery, and biological data interpretation. This is also creating opportunities for cloud-based platforms and specialized service providers that help research teams manage data at scale. In addition, higher biotech funding is supporting adoption of AI tools in earlier-stage research, where faster insight generation can improve R&D productivity. The trend is especially favorable for vendors offering integrated analytics across sequencing, multi-omics, and discovery workflows. As a result, expanding biotech research investment is opening new revenue opportunities across this market. All these factors would drive the market growth over the coming years.

- For instance, in September 2025, llumina launched BioInsigh, a new business created to meet industry demand for deeper biologic insights by combining sequencing, software, data analysis, and AI to support technology- and data-driven discovery.

MARKET CHALLENGES

Complex Data Integration Pose a Prominent Challenge to Market Growth

Integrating complex data poses a significant market challenge, as biological research increasingly merges genomic, transcriptomic, proteomic, clinical, and imaging data produced in various formats and scales. Numerous organizations continue to face challenges integrating these datasets into a single usable workflow, hindering analysis and restricting the complete potential of AI models. Variations in data quality, annotation criteria, compatibility, and storage infrastructures complicate integration, particularly in multi-site research and clinical settings. This heightens the demand for sophisticated platforms that can integrate data prior to generating valuable insights. The challenge escalates further as multi-omics and precision medicine initiatives grow, as they necessitate integrating various levels of biological and patient data. Consequently, the complexity of data integration may postpone deployment, increase implementation expenses, and slow down the decision-making process. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Component

Growing Number of Software Deployments to Propel Software Segmental Growth

In terms of component, the market is divided into software and services.

The software segment captured the largest global AI in bioinformatics market share in 2025. The segment’s growth can be attributed to the central role of software in converting large genomic, multi-omics, and biological datasets into usable insights across research and clinical workflows. Compared with services, software generates stronger recurring revenue through subscriptions, enterprise licenses, and platform expansions, which help it maintain a larger market share. In addition, pharmaceutical and biotechnology companies, research institutes, and diagnostic laboratories increasingly prefer scalable software environments that can automate analysis and improve turnaround time. The growing need for standardized, reproducible, and high-throughput data interpretation has also strengthened software demand across this market.

- For instance, in May 2025, QIAGEN announced the acquisition of Genoox, an AI powered software company, to strengthen its clinical bioinformatics portfolio through the Franklin platform for genomic analysis and interpretation.

The services segment is anticipated to rise with a CAGR of 19.82% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Scalable Access and Faster Deployment to Supported the Cloud-Based Segmental Dominance

On the basis of deployment, the market is divided into on-premise, cloud-based, and hybrid.

The cloud-based segment captured the largest market share in 2025. The growth of this segment is driven by the increasing need to process large genomic, multi-omics, and biological datasets without heavy upfront infrastructure investment. Cloud deployment makes it easier for pharmaceutical and biotechnology companies, research institutes, and diagnostic laboratories to scale computing power, store high-volume data, and run AI models faster across multiple users and sites. It also supports easier software updates, remote collaboration, and faster integration of new analysis tools, making it more practical than on-premises systems for many customers. In addition, as AI workflows in bioinformatics become more data-intensive, cloud environments are becoming more suitable for handling speed, flexibility, and cost efficiency. This has strongly supported the segment’s larger market share. Furthermore, the segment is set to hold a 52.0% share in 2026.

- For instance, several companies such as TEMPUS, Illumina Inc. and others offer cloud-based AI solutions for bioinformatics.

The hybrid segment is anticipated to rise with a CAGR of 19.14% over the forecast period.

By Technology

High Usage in Various Applications to Boost Segmental Growth

Based on technology, the market is classified into natural language processing, machine learning & deep learning, and others.

The machine learning & deep learning segment captured the leading position in the global market in 2025. The segment’s growth can be attributed to its wide use in core bioinformatics tasks such as genomic pattern recognition, variant interpretation, multi-omics analysis, protein structure prediction, and drug molecule optimization. These technologies are better suited to handle large and complex biological datasets, which makes them more useful than other AI approaches in high-value research workflows. In addition, their ability to improve prediction accuracy, automate analysis, and reduce discovery time has increased adoption among pharmaceutical and biotechnology companies, research institutes, and diagnostic laboratories. This has strongly supported the segment’s leading market position. Furthermore, the segment is set to hold a 67.8% share in 2026.

- For instance, in September 2025, Eli Lilly launched TuneLab, an artificial intelligence and machine learning platform designed to give biotechnology companies access to Lilly-trained models for faster drug discovery.

The natural language processing segment is anticipated to rise with a CAGR of 19.48% over the forecast period.

By Application

High Usage in Genomics Studies to Boost Genomics & Sequence Analysis Segmental Growth

On the basis of application, the market is divided into genomics & sequence analysis, multi-omics analysis, protein structure & functional analysis, drug discovery & molecular design, clinical genomics / precision medicine, laboratory workflow automation, and others.

The genomics & sequence analysis segment captured the highest share of the global market in 2025. Sequence data is the starting point for many AI bioinformatics workflows across research, clinical genomics, and precision medicine. Analyzing DNA and RNA data for variant detection, disease understanding, biomarker identification, and treatment-related insights supports segment growth. In addition, many newer AI applications in bioinformatics are built on top of sequencing data, which further strengthens this segment’s leading position in the market. Furthermore, the segment is set to hold a 27.3% share in 2026.

- For instance, in January 2026, SOPHiA GENETICS and MD Anderson announced a strategic collaboration to create bioinformatics pipelines that enable clinicians to rapidly interpret complex RNA-sequencing data for cancer diagnosis and treatment.

The multi-omics analysis segment is anticipated to rise with a CAGR of 20.99% over the forecast period.

By End User

High Utilization by Pharmaceutical & Biotechnology Companies to Support Segment’s Leading Position

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs/CDMOs, academic & research institutes, hospitals & diagnostic laboratories, and others.

In 2025, the pharmaceutical & biotechnology companies segment held the leading position in the global market. These companies are the biggest users of AI in bioinformatics for drug discovery, target identification, biomarker analysis, molecular design, and precision medicine research. They usually handle very large genomic and multi-omics datasets, which increases the need for advanced software platforms and specialized services. In addition, these companies have larger budgets and a stronger willingness to invest in tools that can reduce research time, improve success rates, and support faster decision-making. Furthermore, the segment is set to hold a 42.1% share in 2026.

- For instance, in November 2025, Eli Lilly and Insilico Medicine announced a collaboration to combine Insilico’s Pharma.AI platform with Lilly’s development and disease expertise to discover and advance new therapies.

In addition, CROs/CDMOs are projected to witness 20.17% growth rate during the forecast period.

AI in Bioinformatics Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, Latin America, North America, and the Middle East & Africa.

North America

North America AI in Bioinformatics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 0.39 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 0.44 billion. North America dominated the market due to strong biotechnology research infrastructure, high investment in genomics research, and the presence of leading technology companies.

U.S. AI in Bioinformatics Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 0.47 billion in 2026, accounting for roughly 38.0% of global market.

Europe

Europe’s market is anticipated to grow at a CAGR of 17.08% during the forecast period. The regional market is driven by collaborative biomedical research programs, expanding use of AI in medicine development, and supportive policy direction around AI in healthcare and life sciences.

U.K. AI in Bioinformatics Market

The U.K. market in 2026 is estimated at around USD 0.07 billion, representing roughly 5.4% of global revenues.

Germany AI in Bioinformatics Market

Germany’s market size is projected to reach approximately USD 0.07 billion in 2026, equivalent to around 6.1% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach USD 0.29 billion by 2026. The region is expected to grow rapidly due to increasing biotechnology investments, rising sequencing adoption, and an increasing number of genomic research initiatives.

Japan AI in Bioinformatics Market

The Japanese market in 2026 is estimated at around USD 0.04 billion, accounting for roughly 3.6% of global revenues.

China AI in Bioinformatics Market

China’s market is projected to reach revenues of around USD 0.10 million in 2026, representing roughly 7.8% of global sales.

India AI in Bioinformatics Market

The Indian market in 2026 is estimated at around USD 0.04 billion, accounting for roughly 3.6% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.06 billion by 2026. Prominent factors such as the gradual strengthening of human genomics networks, regional knowledge-sharing, and rising awareness of precision medicine applications are boosting the market growth in these regions.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.03 billion by 2026, representing about 2.0% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and Product Innovation by Key Players to Strengthen Market Position

The global market features prominent players such as Illumina, Tempus, QIAGEN, SOPHiA GENETICS, DNAnexus, and Fabric Genomics, collectively holding a strong position in 2025. This is due to their AI-powered genomics, multi-omics analysis, clinical interpretation, and precision medicine platforms. Key industry leaders are adopting strategies such as product launches, platform expansion, strategic collaborations, and data-driven innovation to strengthen their market positions.

- For instance, in January 2026, Illumina launched Illumina Connected Multiomics, a cloud-based software platform designed to analyze and visualize multiomic and multimodal biological data at scale, strengthening its position in AI-enabled bioinformatics software.

Other significant participants include Recursion, DEEP GENOMICS, Owkin, Inc., and others. These companies are expected to prioritize new software innovation, precision medicine partnerships, and scalable data-platform development to improve their competitive positions over the forecast period.

LIST OF KEY AI in BIOINFORMATICS COMPANIES PROFILED

- TEMPUS (S.)

- SOPHiA GENETICS (Switzerland)

- DNAnexus, Inc. (U.S.)

- Fabric Genomics, Inc. (U.S.)

- Recursion (U.S.)

- BioSymetrics, Inc. (U.S.)

- Owkin, Inc. (France)

- BenevolentAI (U.K.)

- Illumina Inc. (U.S.)

- DEEP GENOMICS (Canada)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Tempus announced a strategic collaboration with Merck to accelerate AI-driven precision medicine and biomarker discovery in oncology using Tempus’ data and analytics capabilities.

- February 2026: Tempus announced HRD-RNA, a new AI-driven pan-cancer algorithm built on a 1,660-gene logistic regression model to improve identification of homologous recombination deficiency and support treatment selection.

- February 2026: SOPHiA GENETICS announced a major U.S. expansion by signing two large integrated health systems to its network, increasing deployment of its AI-driven precision medicine platform.

- December 2025: Insilico Medicine and TaiGen Biotechnology announced an exclusive pipeline out-licensing collaboration to develop and commercialize AI-discovered assets.

- September 2025: Illumina launched its new 5-base solution, enabling simultaneous genomic and epigenomic analysis from a single sample and supporting more scalable multiomic research workflows.

REPORT COVERAGE

The global AI in bioinformatics market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as technological advancements, innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers, and acquisitions, along with significant advancements in the industry within the market. The global market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.63% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.06 billion in 2025 and is projected to reach USD 4.80 billion by 2034.

In 2025, the North American market value stood at USD 0.44 billion.

The market is expected to exhibit a CAGR of 18.63% during the forecast period.

By component, the software segment led the market in 2025.

Rapid drug discovery acceleration and genomic data expansion are the key factors driving the market.

TEMPUS, SOPHiA GENETICS, DNAnexus, Inc., and Fabric Genomics, Inc. are some of the prominent players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us