AI in Mental Health Market Size, Share & Industry Analysis, By Component (Hardware/Devices and Software & Services), By Deployment (Cloud-based, On-Premise, & Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing, & Others), By Indication (Depression, Anxiety Disorders, Substance Use Disorders, Bipolar/Schizophrenia, & Others), By Application (Screening & Assessment, Therapy Support/Digital Therapeutics, Care Navigation & Triage, Clinical Documentation, Remote Monitoring & Relapse Prediction, & Others), By End User, and Regional Forecast, 2026-2034

AI in Mental Health Market Size and Future Outlook

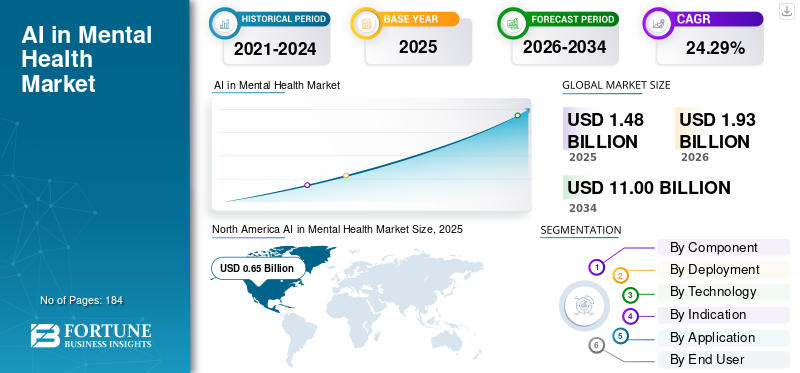

The global AI in mental health market size was valued at USD 1.48 billion in 2025. The market is projected to grow from USD 1.93 billion in 2026 to USD 11.00 billion by 2034, exhibiting a CAGR of 24.29% during the forecast period. North America dominated the AI in mental health market with a market share of 43.92% in 2025.

AI in mental health entails utilizing artificial intelligence, primarily via machine learning/deep learning and progressively natural language processing/speech analysis, to analyze clinical notes, patient-reported outcomes, dialogue exchanges, and passive data from smartphones and wearable devices. It enhances conventional mental health practices by refining screening and risk assessment, tailoring care navigation, facilitating therapy assistance through digital coaching/chatbots, simplifying clinical documentation, and reinforcing ongoing monitoring for relapse or symptom worsening with organized follow-up reminders. Elements influencing this market consist of the increasing global mental health challenges, ongoing deficits of psychiatrists/therapists leading to extended wait times, and rapid implementation of tele-mental health and virtual-first care models.

Prominent players such as Teladoc Health, Talkspace, Lyra Health, Headspace Health, and Wysa are improving AI-based mental health services through unified platforms that merge triage, care matching, coaching/therapy processes, and analytics for monitoring engagement and results.

Download Free sample to learn more about this report.

AI in Mental Health Market Key Takeaways

- 2025 Market Size: USD 1.48 billion

- 2026 Market Size: USD 1.93 billion

- 2034 Forecast Market Size: USD 11.00 billion

- CAGR: 24.29% from 2026–2034

- North America dominated the AI in mental health market with a 43.92% share in 2025.

- The hardware/devices segment is anticipated to rise at a CAGR of 20.56% over the forecast period.

- The natural language processing segment is anticipated to rise at a CAGR of 25.95% over the forecast period.

North America

North America maintained its leading position in 2025, with a market value of USD 0.65 billion.

Europe

Europe is expected to grow at a CAGR of 24.11% during the forecast period, supported by increasing adoption of AI-driven mental healthcare solutions.

Asia Pacific

Asia Pacific is expected to reach a market valuation of USD 0.40 billion by 2026, driven by growing investments in digital mental health technologies.

U.S.

The market is analytically approximated at around USD 0.77 billion in 2026, accounting for roughly 39.8% of the global market.

Japan

The market is estimated to reach around USD 0.06 billion in 2026, representing approximately 3.1% of global revenues.

Read More

AI IN MENTAL HEALTH MARKET TRENDS

Focus on Generative AI and LLM Integration is a Significant Market Trend

The integration of generative AI and LLM is emerging as a significant trend in the market, as it enhances the speed and scalability of language-intensive processes such as intake chats, session documentation, care navigation, and follow-up communications. Providers are utilizing LLMs to create session summaries, standardize records, and decrease clinician administrative time, thereby directly enhancing capacity in a market limited by therapist shortages. On the patient side, conversational experiences powered by LLMs provide continuous triage, coaching, and prompts for next-best actions, facilitating ongoing engagement between appointments. Simultaneously, safety influences adoption as suppliers are implementing guardrails, escalation procedures, and human-in-the-loop evaluations to address hallucinations and crisis-risk situations. Consequently, commercialization is transitioning from “chatbots solely” to comprehensive platforms where GenAI assists clinicians, care teams, and members throughout the entire care journey. These factors are supporting the global AI in mental health market growth.

- For instance, in October 2025, Lyra Health announced Lyra AI, positioning it as a clinical-grade AI experience designed to provide always-on mental health support alongside its provider network.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Large and Rising Unmet Need for Mental Health Services Globally and Shortage of Clinicians to Amplify Market Growth

The significant and expanding unaddressed demand for mental health services is a key factor propelling the market expansion, as the need is increasing more rapidly than the system can provide qualified treatment. Worldwide, mental health issues impact a substantial number of people, whereas the availability of services and financial support varies across nations, increasing the treatment disparity. Workforce limitations constitute a systemic obstacle and significantly lower figures in numerous LMICs, resulting in extended wait times and restricted continuity of care. This deficit drives payers, employers, and providers to utilize AI-powered tools for triage, care navigation, documentation automation, and remote monitoring, allowing clinicians to concentrate on more complex cases while additional patients obtain assistance. Consequently, platforms that integrate AI with scalable provider networks and virtual-first delivery approaches are experiencing greater uptake as they enhance access without significantly increasing personnel. All these factors cumulatively drive the global market growth.

- For instance, according to data published by WHO in September 2025, there is persistent shortages, with a global median of only approximately 13 mental health workers per 100,000 people and far lower levels in many LMICs.

MARKET RESTRAINT

Regulatory Complexity across Countries to Hamper Market Growth

Regulatory intricacies across markets are a significant constraint for the AI in mental health sector, as the same product may be subject to varied classifications and regulations based on the country. Vendors frequently need to adhere to various overlapping regulations, medical device processes, AI governance standards, and privacy/data-localization laws, which results in extended approval timelines and increased compliance expenses. Regulators anticipate enhanced risk management, transparency, monitoring for model drift, and escalation protocols for GenAI-enabled mental health features, which hinders rapid iteration. This fragmentation complicates global scaling. Firms need to localize claims, evidence bundles, and deployment frameworks for every jurisdiction. Consequently, go-to-market strategies may transition from global launch to phased deployments, restricting short-term revenue generation. This results in limiting the market growth to a certain extent.

- For instance, In July 2025, the U.S. FDA issued a Warning Letter to WHOOP, Inc. stating the company was marketing its Blood Pressure Insights feature without required clearance/approval.

MARKET OPPORTUNITIES

Increasing Investments in Robust Clinical Evidence and Pilot Programs to Offer Growth Opportunities

The rising investments in robust clinical evidence and payer-facing pilots is a major market opportunity as reimbursement is the fastest way to scale adoption beyond one-off employer or consumer subscriptions. As payers demand proof of clinical impact, cost offsets, and safety, vendors that fund trials, real-world outcome studies, and implementation pilots can convert nice-to-have tools into reimbursable pathways. This shifts buying from discretionary wellness spend to covered benefits, expanding eligible member pools and improving retention. Evidence-backed programs also help providers justify workflow integration and drive repeat usage through measurement-based care. Over time, stronger evidence lowers perceived risk for payers, accelerates contracting cycles, and supports broader reimbursement codes and benefit designs, creating a clear runway for clinically validated AI-enabled solutions. All these factors would drive the market growth in the coming years.

- For instance, in August 2024, Big Health announced that the U.S. FDA granted clearance for SleepioRx, reinforcing the role of clinical-grade evidence in enabling prescription and reimbursement pathways for digital mental health treatments.

MARKET CHALLENGES

Data Privacy Concerns to Pose a Prominent Challenge to Market Growth

Data privacy concerns are a major challenge in the AI in mental health market as these solutions routinely handle highly sensitive data such as therapy notes, symptom logs, crisis flags, medication history, and behavioral signals from chats/voice. Any perceived weakness in privacy controls can immediately reduce user trust, weaken engagement, and slow adoption by employers, payers, and providers. The risk is higher when platforms integrate GenAI/LLMs, as data can move across multiple systems, increasing exposure points. In parallel, privacy rules and expectations differ across countries, creating complex compliance and localization requirements. Breaches or improper disclosures can lead to regulatory actions, legal penalties, and costly remediation, forcing vendors to invest heavily in security, consent management, and auditability, often slowing product rollouts. All the factors cumulatively affect the market growth.

AI in Mental Health Market Segmentation Analysis

By Component

Increasing Demand from Healthcare Providers to Propel Segmental Growth

Based on component, the market is divided into software & services and hardware/devices.

In 2025, the software & services segment dominated the market, as most value is created through scalable, workflow-embedded platforms rather than physical devices. The segment’s leadership is driven by its ability to handle large volumes of sensitive clinical and behavioral data and convert them into actionable outputs such as automated intake/triage, care navigation, documentation support, and continuous symptom monitoring. These software layers also enable faster upgrades and deployment across provider networks through SaaS models, helping organizations expand access without proportionately increasing clinical staff. In addition, services remain essential as implementation is rarely plug-and-play as buyers typically require integration, configuration, training, and governance to ensure safe and compliant use. Moreover, the steady rollout of new AI-enabled features by leading vendors is further strengthening software & services adoption and reinforcing the segment’s dominance in the market.

- For instance, in January 2025, Talkspace announced the launch of Insights, a new AI-powered feature, designed to help providers prepare for sessions more efficiently and support care between sessions.

The hardware/devices segment is anticipated to rise at a CAGR of 20.56% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Shift toward Cloud-based Solutions to Support the Segmental Dominance

Based on deployment, the market is divided into cloud-based, hybrid, and on-premise.

The cloud-based segment captured the largest global AI in mental health market share in 2025. Cloud deployment allows providers, payers, and employers to roll out AI-enabled triage, coaching, and care navigation without heavy on-premise IT investment, which speeds procurement and implementation. It also enables continuous model updates, safety guardrails, and content refreshes which is critical in mental health where workflows and risk protocols evolve rapidly. In addition, cloud architectures make it easier to integrate with virtual care, mobile apps, and analytics dashboards, supporting longitudinal monitoring and population-level reporting. As a result, buyers prefer cloud-first deployments that can expand access while maintaining centralized governance, security controls, and standardized user experiences across locations. Furthermore, the segment is set to hold 79.0% share in 2026.

- For instance, in May 2025, Headspace announced a new stratified care model for organizations powered by its AI companion Ebb.

The hybrid segment is anticipated to rise with a CAGR of 19.74% over the forecast period.

By Technology

Soaring Product Launches to Boost Others Segmental Growth

In terms of technology, the market is divided into natural language processing, machine learning & deep learning, and others.

The others segment dominated the global market in 2025. This segment typically includes care-orchestration engines, personalization/recommender systems, safety/guardrail layers, multimodal and passive-sensing analytics, and speech/voice signal processing, which are critical to make mental health support continuous, contextual, and scalable. New product launches based on these technologies supports the segment growth. Furthermore, the segment is set to hold 42.7% share in 2026.

- For instance, in June 2025, Sword Health launched Mind, a mental health solution that combines AI and licensed clinicians to deliver continuous, personalized care, a model that depends heavily on orchestration, monitoring, and safety layers.

The natural language processing segment is anticipated to rise at a CAGR of 25.95% over the forecast period.

By Indication

High Screening Tests and Broad Patient Population to Boost Depression Segment Growth

In terms of indication, the market is divided into depression, anxiety disorders, substance use disorders, bipolar/schizophrenia, PTSD, dementia/cognitive, and others.

The depression segment captured the highest share of the global market in 2025. Depression represents one of the largest and most consistently screened mental health conditions across primary care, workplace programs, and virtual-first platforms. Depression also has widely used standardized measures which makes it easier for AI tools to support structured assessment, progress tracking, and outcomes reporting at scale. In addition, depression frequently co-exists with anxiety, sleep problems, and chronic diseases. Hence, addressing it creates broader downstream value for payers and providers through improved engagement and care continuity. Furthermore, the segment is set to hold 26.3% share in 2026.

- For instance, in March 2025, Dartmouth researchers reported results from a clinical trial of a generative-AI therapy chatbot (“Therabot”), noting that participants diagnosed with depression experienced a 51% average reduction in symptoms, reinforcing why depression is a leading focus area for AI-enabled mental health solutions.

The anxiety disorders segment is anticipated to rise with a CAGR of 23.32% over the forecast period.

By Application

High Usage in Screening and Assessment to Boost Therapy Support/Digital Therapeutics Segmental Growth

On the basis of application, the market is divided into screening & assessment, therapy support/digital therapeutics, care navigation & triage, clinical documentation, remote monitoring & relapse prediction, population analytics & quality reporting, and others.

The therapy support/digital therapeutics segment captured the highest share of the global market in 2025. These solutions support measurement-based care by tracking symptoms and engagement over time, which strengthens ROI discussions with payers and employers. In addition, therapy-support platforms are easier to scale through mobile and telehealth channels, allowing rapid access expansion without proportional workforce growth. As reimbursement pathways evolve, clinically validated digital therapeutics become even more attractive as they can be positioned as adjuncts to standard care with clearer evidence requirements and benefit design fit. Furthermore, the segment is set to hold 21.5% share in 2026.

- For instance, in April 2024, Otsuka and Click Therapeutics announced the U.S. FDA clearance of Rejoyn, described as the first prescription digital therapeutic authorized for adjunctive treatment of major depressive disorder (MDD) symptoms.

The remote monitoring & relapse prediction segment is anticipated to rise at a CAGR of 25.36% over the forecast period.

By End User

High Utilization by Healthcare Providers Supported the Segment’s Leading Position

Based on end user, the market is segmented into healthcare payers, healthcare providers, academic & research institutes, direct-to-consumer, and others.

In 2025, the healthcare providers segment held the leading position in the global market. This has been observed as providers have the strongest need to use AI for intake triage, symptom tracking, documentation support, and relapse monitoring to manage high caseloads and clinician burnout. They also control the clinical data and care pathways needed to operationalize AI safely, including escalation protocols for high-risk patients. Furthermore, the segment is set to hold 45.6% share in 2026.

- For instance, in February 2026, Valant announced expanded capabilities for its AI-powered documentation tool AI Notes Assist, designed specifically to generate structured clinical notes within behavioral health clinicians’ existing templates.

In addition, the healthcare payers segment is projected to witness a growth rate of 25.59% during the forecast period.

AI in Mental Health Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI in Mental Health Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the North America market achieved USD 0.49 billion, dominating the global market. In 2025, the area maintained its leading status, with USD 0.65 billion. In North America, growth is mainly fueled by a significant increase in unmet behavioral health needs alongside ongoing clinician shortages, compelling providers to implement AI for triage, documentation assistance, and scalable care navigation.

U.S. AI in Mental Health Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 0.77 billion in 2026, accounting for roughly 39.8% of the global market.

Europe

The Europe market size is expected to grow at a CAGR of 24.11% during the forecast period. In Europe, growth is supported by rising mental health burden and the need to modernize care pathways across public health systems, where scaling access without adding proportional headcount is a major priority.

U.K. AI in Mental Health Market

The U.K. market is estimated to touch around USD 0.11 billion in 2026, representing roughly 5.6% of global revenues.

Germany AI in Mental Health Market

The Germany market size is projected to reach approximately USD 0.12 billion in 2026, equivalent to around 6.3% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.40 billion by 2026, making it the third largest region in the worldwide sector. In Asia Pacific, growth is fueled by large population-scale demand, widening awareness, and rapid adoption of digital health delivery models that allow mental health support to reach underserved areas.

Japan AI in Mental Health Market

The Japan market is estimated to touch around USD 0.06 billion in 2026, accounting for roughly 3.1% of global revenues.

China AI in Mental Health Market

China’s market is projected to reach revenues of around USD 0.13 million in 2026, representing roughly 6.9% of global sales.

India AI in Mental Health Market

The India market is estimated to reach around USD 0.06 billion in 2026, accounting for roughly 3.1% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are anticipated to have slower growth during the forecast period. The market in Latin America is expected to reach a worth of USD 0.11 billion by 2026. Key elements such as the rising demand, restricted specialist availability, and growing digital health adoption are expected to drive market growth.

In the Middle East and Africa, the GCC market is estimated to reach around USD 0.03 billion by 2026, accounting for roughly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Software Rollouts and GenAI-Enabled Care Navigation to Strengthen Market Share

The global AI in mental health market features a moderately fragmented competitive landscape, where established virtual care providers and employer-benefit platforms face competition from specialized AI-driven digital therapeutics and conversational AI companies. Key contributors in the field are Teladoc Health, Talkspace, Headspace, Lyra Health, and others. These organizations are progressively highlighting the integration of LLM/GenAI for intake, triage, and documentation assistance, coupled with robust security and privacy measures to ease adoption challenges in provider and payer settings.

- For instance, in October 2024, OneDigital Resourcing Edge revealed a collaboration with Wysa to offer AI-driven mental health assistance for employees.

Additional key contributors are Talkiatry, K Health, and others. Emphasis on new software launches, customer expansion, and partnerships are key strategic undertaken by these players.

LIST OF KEY AI IN MENTAL HEALTH COMPANIES PROFILED

- Teladoc Health, Inc. (U.S.)

- Talkspace (U.S.)

- Wysa Ltd (U.S.)

- Talkiatry Management Services, LLC. (U.S.)

- Woebot Health (U.S.)

- Unmind Ltd (U.K.)

- Modern Life, Inc. (U.S.)

- Lyra Health, Inc. (U.S.)

- Headspace Health (U.S.)

- Cognoa, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Talkiatry raised USD 210 million Series D funding to support its next growth phase as a scaled virtual psychiatry provider.

- January 2026: Spring Health announced plans to acquire Alma to expand its mental health care navigation and provider ecosystem.

- January 2026: Carrum Health and Lyra Health launched an integrated specialty care and mental health solution, combining COE specialty care coordination with workforce behavioral health services.

- November 2025: Cigna Healthcare launched Headspace for Cigna Healthcare to expand everyday mental health support with self-guided resources and pathways to higher levels of care.

- November 2025: Lyra Health partnered with Thatch, allowing employers to access Lyra’s mental health offering through the Thatch Marketplace.

REPORT COVERAGE

The global AI in mental health market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.29% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Indication, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Indication |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.48 billion in 2025 and is projected to reach USD 11.00 billion by 2034.

In 2025, the market value stood at USD 0.65 billion.

The market is expected to exhibit a CAGR of 24.29% during the forecast period of 2026-2034.

By component, the software & services segment led the market in 2025.

Large and growing unmet need for mental health services globally and shortage of clinicians are key factors primarily driving market expansion.

Teladoc Health, Inc., Talkspace, Wysa Ltd, and Talkiatry Management Services, LLC. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 184

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us