Mental Health Screening Market Size, Share & Industry Analysis, By Platform (mHealth, Remote Platform, Telehealth, & Others), By Assessment Type (Self-reported Questionnaires, Clinical Interviews, Observational Tools, & Biomarker Tools), By Disease Indication (Depression, Alzheimer’s, OCD, Anxiety disorders, PTSD, ADHD, Schizophrenia, Sleep Disorders), By Age Group (Pediatric & Adults), By Application (Diagnostic, Clinical Trials, Training & Assessments), By Setting (Clinical Settings, Educational Institutions, Workplace/corporate Programs, Online Platforms), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

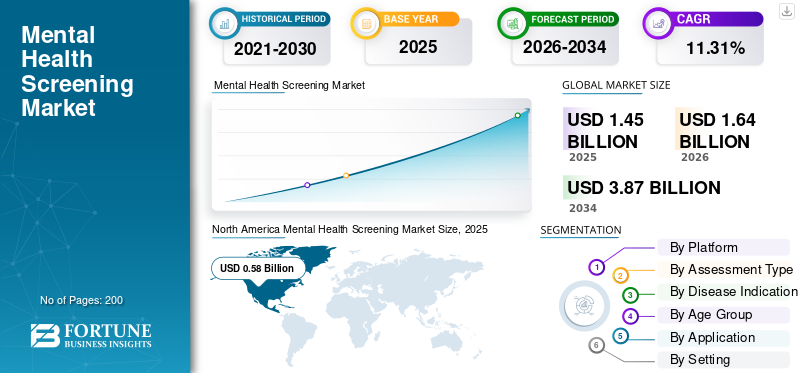

The global mental health screening market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.64 billion in 2026 to USD 3.87 billion by 2034, exhibiting a CAGR of 11.31% during the forecast period. North America dominated the global mental health screening market with a market share of 40.0% in 2025.

The mental health screening market includes numerous tools and solutions used to screen the mental health disorders. The market is poised for considerable growth over the forecast period, driven by increasing awareness of mental health disorders and the rapid expansion of teleconsultations to facilitate remote monitoring. The increasing awareness of mental health issues and the associated loss of productivity have highlighted the importance of effective screening. Additionally, advancements in the market are driving growth through AI integrations and innovative solutions for mental health screening. Moreover, numerous product launches and key collaborations among key operational players in the market support the growth opportunities in the market.

- For instance, in September 2022, the WHO reported that mental health issues cost the global economy USD 1.00 trillion in lost productivity. This represents a significant loss of productivity, with 12 billion working days lost each year due to depression and anxiety.

Furthermore, the market is dominated by various key operating players, including Aiberry, Qbtech AB, Empatica Inc., and Proem Behavioral Health, which direct their resources toward strategic mergers and acquisitions and new product launches to strengthen their market position and capitalize market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Mental Health Burden and Growing Awareness to Drive Market Growth

Some of the factors strongly driving the market's growth are the rising burden of mental health issues and increasing awareness about them. As the social and economic cost of mental illness becomes highlighted through lost productivity, suicide risk, and higher comorbidity with chronic diseases, governments, employers, payers, and health systems are prioritizing early identification. Also growing awareness through various government-led campaigns, celebrity advocacy is supporting to reduce stigma, encouraging more people to seek help and accept screening.

- For instance, in September 2025, the WHO reported that more than 1 billion people were living with mental health disorders, with conditions such as anxiety and depression.

Such high prevalence is boosting the global mental health screening market growth.

MARKET RESTRAINTS

Persistent Stigma Around Mental Health Limits Screening Uptake and Impedes Market Growth

A prominent factor impeding the market growth is stigma related to mental health disorders. People are subjected to the fear of discrimination from admitting they have symptoms or agreeing to formal screening. A mental health label could adversely affect their job, social standing, or family relationships due to discrimination, and treated differently due to their condition. Such factors keep screening volumes lower than prevalence and impede the market growth for these remote mental health platforms.

- For instance, in 2021, Rethink Mental Illness conducted a survey and reported that 42.0% of people with a severe mental illness, who have worked in large, corporate workplaces, experienced stigma and discrimination.

MARKET OPPORTUNITIES

Technological Advancement with AI Integration to Optimize Screening and Offer Significant Market Growth Opportunities

Technological advancement and rapid progress in AI and advanced analytics are transforming the market. Unlike traditional mental health assessments that rely heavily on self-reported questionnaires, such as the PHQ-9 and GAD-7, AI can be integrated into these tools to analyze facial expressions and emotional cues, offering a more objective and non-intrusive method for evaluating mental wellness. Newer models can also analyze speech, text, and behavioral data from smartphones or wearables, which can detect subtle changes earlier than traditional tools. This enables providers to transition toward continuous, remote monitoring, thereby increasing the value of screening through earlier diagnosis. Such factors offer market growth opportunities.

- For instance, in May 2025, Opsis Pte. Ltd launched SenseWell, an AI-powered mental wellness assessment tool to transform how social service agencies approach mental health screening and support. This tool utilizes AI to analyze facial expressions and emotional cues. Such technological advancements offer market growth opportunities.

MARKET CHALLENGES

Data Privacy & Security Concerns Pose a Significant Challenge for Market Growth

Mental health screening solutions extensively use screening mHealth apps and other teleconsultation apps for continuous monitoring. They handle a vast amount of sensitive data regarding symptom histories, self-harm risk, therapy notes, and psychiatric diagnoses. These services are at high risk of cyber threats for vulnerable users and providers. Additionally, large-scale analyses of health and mental health apps reveal inconsistent data privacy practices and sharing with third parties. Such factors pose a challenge for the market, as they can hinder the adoption of these tools.

- For instance, in July 2021, a team from Macquarie University compared 15,000 free mobile health (mHealth) apps available on the Google Play Store. It assessed their privacy practices against those found in 8,000 non-health apps, identifying and reporting serious privacy issues and inconsistent practices.

MENTAL HEALTH SCREENING MARKET TRENDS

Deeper Integration of Mental Health Screening into Primary Care and Public Health is a Prominent Market Trend

Underscoring the importance of mental well-being, various health systems and policymakers are pushing mental health screening into primary care and public health programs. This is a prominent trend observed in the market that supports demand for scalable screening tools. Many primary-care networks are standardizing routine mental health screening protocols and embedding them into EHR workflows, patient portals, and pre-visit questionnaires.

Additionally, key operating entities in the market are focusing on strategic collaborations to enhance their offerings and integrate these mental health screening tools into the primary care they provide.

- For instance, in February 2024, Southeast Primary Care Partners implemented behavioral health screening through the Mental Health Technologies SmarTest platform.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Telehealth Led Market Due to Its Wide Applications In Clinical Workflows

Based on platform, the global market is segmented into mHealth, remote platform, telehealth, and others.

In 2025, the telehealth segment dominated the global market. The dominance of the segment is due to its wide applications in clinical workflows, with mental health accounting for a disproportionately high share of all telehealth visits. The increasing adoption of teleconsults for psychiatry and counselling drives the segmental growth. These platforms are largely conversational and offer auto-scored screening forms, such as the PHQ-9, GAD-7, and PTSD scales, among others. Such advantages are encouraging key companies to launch new products specialized for these platforms.

- For instance, in November 2023, Sonde Health partnered with Together, an AI-based health assistant, to provide enhanced mental health screening and monitoring through its Mental Vitals feature. This collaboration aimed to access the voice analysis platform of the company for early detection of symptoms related to depression and anxiety. Such clinical screenings can lead to a telehealth appointment with a clinician, which can facilitate segmental growth.

On the other hand, the mHealth segment is expected to grow at a CAGR of 16.51% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Assessment Type

Self-reported Questionnaires Dominated Market as They are Cost-effective

Based on the assessment type, the market is classified into self-reported questionnaires, clinical interviews, observational tools, and biomarker tools.

The self-reported questionnaires segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 64.7% share. Self-reported questionnaires are the primary tool for mental health screening. They are cost-effective, quick, and validated across multiple populations. Such benefits make them ideal for large-scale deployment in primary care and digital programs driving growth. Such advantages encourage key companies to develop more clinically validated questionnaires, thereby boosting the growth of the segment.

- For instance, in November 2024, AXA launches Mind Health Self-check, its new mental health prevention tool. The questionnaire provides an individualized diagnosis and advice to help understand how skills, beliefs, and lifestyle influence one's mental health.

The biomarker tools segment is expected to grow at a CAGR of 15.03% over the forecast period.

By Disease Indication

Depression Segment Commanded Market Owing to Rising Patient Volume

On the basis of disease indication, the market is classified into depression, Alzheimer’s, OCD, anxiety disorders, PTSD, ADHD, schizophrenia, dc, and others.

The depression segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 25.02% share. The rising disease burden of depression increases the need for effective screening tools and provides support to the patients. The increasing patient volume reinforces the segment's dominance in the market.

- For instance, in March 2022, the WHO reported that the global prevalence of anxiety and depression increased by a massive 25.0%. Such a rising prevalence of depression is expected to drive the segmental growth.

The anxiety disorder segment is expected to grow at a CAGR of 10.75% over the forecast period.

By Age Group

Rising Need for Mental Health Screening in Adults to Propel Segmental Growth

Based on age group, the market is classified into pediatric and adults.

The adults segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 75.99% share. Adult depression and anxiety are highly prevalent and strongly linked to productivity loss, chronic disease, and healthcare costs. These factors result in prioritization in mental screening for the group. The U.S. Preventive Services Task Force (USPSTF) explicitly recommends routine depression screening for all adults, including pregnant and postpartum people and older adults. Commercially, many digital tools and tele-mental health services are explicitly targeted at working-age adults, who have a higher ability to pay. These factors result in the adult segment dominating the market. Underscoring these factors, new tools are also being developed to cater to the segment’s needs.

- For instance, in October 2025, Dr. Sandeep Vohra launched India’s first patented emotional wellness screening tool, the Emotional Wellness Index (EWI). The EWI is a 55-point digital screening scale designed to accurately assess stress and emotional well-being in students and adults. Such developments are expected to drive the segmental growth.

The pediatric segment is expected to grow at a CAGR of 13.08% over the forecast period.

By Application

Increasing Utilization of Various Platforms for Mental Health Diagnosis to Boost Diagnostic Segment Growth

On the basis of application, the market is classified into diagnostic, clinical trials, training and assessments, and others.

Among these, the diagnostic segment accounted for the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 62.22% share. Most mental health screening revenues are generated through diagnostic testing. Standard questionnaires, such as the PHQ-9, GAD-7, and EPDS, are specifically validated as screening and severity-rating tools to guide diagnosis and treatment adjustments. Repeated diagnostic screening in primary care, OB-GYN, oncology, chronic disease clinics, and behavioral health settings generates the highest test volumes and revenue, resulting in market dominance. Additionally, key partnerships among operating entities to facilitate diagnosis through various platforms drive the segmental growth.

- For instance, in October 2025, Calm Health partnered with LifeStance Health, one of the nation's largest providers of virtual and in-person outpatient mental health care. Through this partnership, the company users are guided directly to LifeStance for mental health care when higher-acuity treatment is recommended, making it easier to access support and diagnosis for a variety of mental health conditions through the app.

The training and assessments segment is expected to grow at a CAGR of 11.67% over the forecast period.

By Setting

Clinical Setting Acts as Epicenter for Mental Health Screening and Leads Segment Growth of the Segment

Based on the setting, the market is categorized into clinical settings, educational institutions, workplace/corporate programs, online platforms, and others.

The clinical settings segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 62.05% share. These settings provide primary-care centers, where EHR-integrated screening is most advanced. Many digital tools are designed specifically to slot into clinic workflows, making it easy to operate high-volume screening. Key companies are focusing their resources on new product launches specialized for these primary caregivers. Such developments are anticipated to drive the segmental growth.

- For instance, in April 2024, Proem Behavioral Health launched a new software version that provides a touchless workflow experience for clinicians and staff. The new release enables healthcare providers, including those in primary care, pediatrics, obstetrics, federally qualified health centers, and behavioral health and addiction clinics, to effectively screen, assess, diagnose, and track patients with mental illness.

The workplace/corporate programs segment is expected to grow at a CAGR of 13.30% over the forecast period.

Mental Health Screening Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Mental Health Screening Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant mental health screening market share in 2024, valuing at USD 0.51 billion, and also maintained the leading share in 2025, with USD 0.58 billion. The region's leading market share in mental health screening solutions is supported by high mental health awareness, strong digital health adoption, and policy frameworks that encourage behavioral health integration into primary care. In 2026, the U.S. market is estimated to reach USD 0.58 billion. Additionally, employers and educational institutions in the U.S. are increasingly investing in screening and early intervention programs.

- For instance, in May 2025, Mental Health America's (MHA) online National Prevention and Screening Program provided mental health screening for more than 5.9 million people worldwide, among whom 78.0% of screeners were located in the U.S. Such widespread adoption and increased awareness of mental health are expected to promote market growth.

Europe

Europe is poised for strong expansion, with the market projected to rise at a CAGR of 10.48%, the second-fastest globally and reach USD 0.48 billion by 2026. This momentum is driven by the growing incorporation of mental health screening across primary healthcare systems, workplace wellness programs, and community-based initiatives. Supported by these developments, the U.K. is expected to achieve a valuation of USD 0.10 billion, while Germany and France are predicted to reach USD 0.09 billion and USD 0.07 billion, respectively, by 2026.

Asia Pacific

In Asia Pacific, the market is expected to climb to USD 0.36 billion by 2026, securing its position as the third-largest regional market. Within the region, China is anticipated to reach USD 0.10 billion, while India is expected to account for USD 0.06 billion by 2026.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa are projected to grow at a moderate pace. The Latin American market is expected to attain USD 0.08 billion by 2026, supported by urbanization, economic strain, and heightened awareness of mental health concerns. Meanwhile, the GCC in the Middle East & Africa is projected to reach a valuation of USD 0.03 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Funding Opportunities for Key Players to Support Leading Positions

The global mental health screening market exhibits a consolidated market structure, with a few companies dominating the market. The market includes digital health companies, EHR and telehealth vendors, behavioral health platform providers, traditional healthcare IT firms, and developers of validated screening instruments. These players, along with their diverse product offerings, also participate in numerous strategic activities to accelerate their product offerings for the market. Aiberry, Qbtech AB, Empatica Inc., and Proem Behavioral Health are some of the major players in the market. These companies offer a wide range of systems for the numerous biologics used in spine care, along with graft substitutes.

- For instance, in March 2024, Aiberry secured USD 8.0 million in seed funding led by Confluence Capital Group, Inc. (CCG) with participation from the VC fund Ascension AI. The new funds were used to accelerate AI-powered mental health screenings.

Other notable players in the market include SonderMind Inc., Riverside Community Care, Headspace Inc., and others. These companies are undertaking various strategic initiatives, such as new product launches, to expand their product offerings.

LIST OF KEY MENTAL HEALTH SCREENING COMPANIES PROFILED

- Aiberry (U.S.)

- Qbtech AB (Sweden)

- Empatica Inc. (U.S.)

- Proem Behavioral Health (U.S.)

- TeleSage (U.S.)

- Qualifacts (U.S.)

- SonderMind Inc. (U.S.)

- Riverside Community Care (U.S.)

- Headspace Inc. (U.S.)

- Ellipsis Health, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Digital Health News Mentavi Health launched Mentavi Concierge, an AI-powered mental health platform to elevate standards of safety, transparency, and clinical oversight in digital care.

- July 2025: LISSUN acquired U.S.-based mental health startup, Being Cares Inc. The development combined clinical expertise with Being’s proprietary technology that decodes over 40 behavioral and emotional conditions. The company offers end-to-end mental health services, including early screening, digital counseling, and in-person therapy sessions.

- May 2024: Mirah and M-3 Information, LLC launched the M3 Checklist assessment for mental illness in the Mirah platform to enhance mental health screening in primary care settings.

- February 2023: Proem Behavioral Health collaborated with Psychiatric Medical Care (PMC), a national behavioral healthcare management company with multiple service lines, to help improve patient outcomes.

- December 2020: Jacobs, in collaboration with global mental health professionals, developed a free mental health check-in tool named One Million Lives to enhance users' understanding of their current mental state and provide proactive strategies for personal mental health development.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.31% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Region |

|

By Platform |

· mHealth · Remote Platform · Telehealth · Others |

|

By Assessment Type |

· Self-reported Questionnaires · Clinical Interviews · Observational Tools · Biomarker Tools |

|

By Disease Indication |

· Depression · Alzheimer’s · OCD · Anxiety disorders · PTSD · ADHD · Schizophrenia · Sleep Disorders · Others |

|

By Age Group |

· Pediatric · Adults |

|

By Application |

· Diagnostic · Clinical Trials · Training and Assessments · Others |

|

By Setting |

· Clinical Settings · Educational Institutions · Workplace/corporate Programs · Online Platforms · Others |

|

By Region |

· North America (By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Country) o U.S. o Canada · Europe (By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Platform, Assessment Type, Disease Indication, Age Group, Application, Setting, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.45 billion in 2025 and is projected to reach USD 3.87 billion by 2034.

In 2025, the market value stood at USD 0.58 billion.

The market is expected to exhibit a CAGR of 11.31% during the forecast period of 2026-2034.

The telehealth segment led the market in terms of platform.

The increasing prevalence of mental disorders to driving market growth.

Aiberry, Qbtech AB, Empatica Inc., and Proem Behavioral Health are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us