AI In Patient Engagement Market Size, Share & Industry Analysis, By Component (Software, and Services), By Deployment (Cloud-Based, On Premise, and Hybrid), By Technology (Natural Language Processing (NLP), Machine Learning & Deep Learning, and Others), By Therapeutic Area (Health & Wellness, Chronic Disease Management {CVD, Diabetes, Orthopedics, and Others}, Behavioral & Mental Health, and Others), By Application (Intelligent Appointment Management, Patient Financial Engagement, Communication & Messaging, & Others), By End User, and Regional Forecast, 2026-2034

AI in Patient Engagement Market Size and Future Outlook

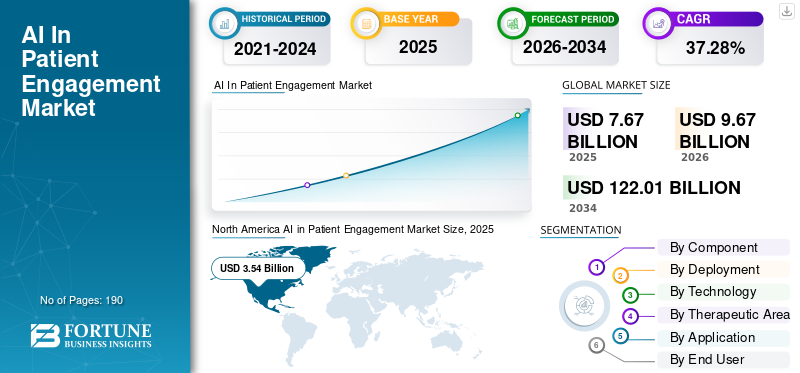

The global AI in patient engagement market size was valued at USD 7.67 billion in 2025. The market is projected to grow from USD 9.67 billion in 2026 to USD 122.01 billion by 2034, exhibiting a CAGR of 37.28% during the forecast period. North America dominated the AI in patient engagement market with a market share of 46.15% in 2025.

The global AI in patient engagement market is projected to grow significantly in the coming years, driven by the rising prevalence of chronic diseases and the increasing demand for continuous monitoring and personalized tools. It extensively uses tools such as chatbots, predictive analytics, and virtual assistants to keep patients actively involved in their healthcare beyond traditional visits. These systems automate tasks such as reminders and basic queries while analyzing data for personalized support. The surge in telemedicine adoption is expected to fuel global AI growth for patient engagement. Furthermore, innovative AI product launches for patient engagement boost growth in the global market.

- For instance, in February 2025, Inspire launched AI-Enabled Patient Insights, an innovative product designed to transform how life sciences organizations gather and leverage patient insights. The solutions provide real-time insights to support research, clinical trial design, and market strategies.

Leading players in the industry, such as Epic Systems Corporation, Salesforce, Inc., Oracle, and Microsoft Corporation, are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

AI IN PATIENT ENGAGEMENT MARKET TRENDS

Growing Use of AI Virtual Assistants is a Key Market Trend

AI virtual assistants becoming a core feature is a prominent global observation in the market. The growing use of AI virtual assistants as the first point of contact for patients reduces workload and automates repetitive tasks. As appointment volumes rise and care teams face staffing and time constraints, phone lines and inboxes become overloaded, slowing response times and increasing patient drop-offs. This drives demand for always-on assistants that can answer commonly asked questions and guide patients to the right service. These AI solutions also help complete routine tasks such as scheduling or follow-ups without waiting for staff. As a result, buyers increasingly treat virtual assistants as a core capability within patient engagement platforms, thereby improving access and the patient experience at scale.

Emphasizing these advantages, key companies are increasingly launching innovative products to meet growing demand.

- For instance, in November 2024, Medsender launched MAIRA, a 24/7 multilingual AI voice agent to streamline patient communication and improve operational efficiency for healthcare practices.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasingly Investing In AI Agents to Deflect Repetitive Calls to Drive Market Growth

A major driver in the global market is the growing pressure on patient access teams as appointment demand rises while staffing and capacity remain limited. When call volumes spike, patients face longer hold times, more abandoned calls, and slower scheduling, which directly reduces access conversion and lowers patient satisfaction. This creates a clear need for AI self-service tools that can answer routine questions, automate scheduling-related requests, and resolve common issues without relying on human agents for every interaction. As a result, providers are increasingly investing in AI agents to deflect repetitive calls, stabilize service levels, and keep access running efficiently as volumes grow. These advantages promote easy adoption of AI solutions and support market growth.

- For instance, in March 2025, Talkdesk launched AI Agents for Healthcare, highlighting a customer outcome where Evara Health managed 45.0% of call volume through automated systems, helping reduce handling time and improve access efficiency.

MARKET RESTRAINTS

Risk Associated with Patient Data Privacy and Cybersecurity to Hamper Growth Potential

A major restraint in the global AI in patient engagement market growth is the risk associated with patient data privacy and cybersecurity. These tools manage sensitive patient identity, appointment, and billing data, so any security weakness can quickly escalate into a high-impact incident. When providers fear exposure of patient health information, ransomware disruption, or regulatory penalties, they tighten approval processes and delay patient-facing AI rollouts. This increases implementation cost and lengthens sales cycles as buyers demand stricter security reviews, tighter integrations, and more vendor accountability. As a result, adoption often slows in organizations that have recently faced breaches or are under heightened compliance scrutiny.

- For instance, in October 2024, a ransomware attack on UnitedHealth's Change Healthcare was reported to have impacted over 100 million people, causing significant disruption and large-scale exposure of sensitive healthcare and billing data. This illustrates why providers are becoming more cautious about expanding connected, data-rich engagement platforms.

MARKET OPPORTUNITIES

Expansion of AI Workflow Automation to Offer Lucrative Growth Opportunities

A major growth opportunity for the global AI in patient engagement market is the expansion of AI workflow automation beyond large health systems into ambulatory practices, as clinics face rising appointment volumes and limited front-office staffing. Routine tasks such as answering calls and confirming appointments are increasing the demand for the market. Delays in responding to scheduling questions can lead to patient drop-offs and impact revenue generation. These factors push practices to adopt AI tools that can handle common patient requests 24/7, automate scheduling-related tasks, and reduce administrative workload without hiring more staff. As a result, key companies are packaging AI engagement workflows specifically for ambulatory settings, designed for faster deployments, with quicker implementation and clear ROI.

- For instance, in February 2026, athenahealth launched agentic patient communication tools that provide patients with 24/7 access to front-office AI agents to improve engagement, simplify scheduling, and reduce administrative burden for practices.

MARKET CHALLENGES

Low Digital Access and Connectivity Gaps to Pose a Challenge for Market Growth

A major challenge for the global AI in patient engagement market is limited digital access and connectivity gaps, which constrain adoption in emerging regions. Many patient-facing tools depend on reliable internet access, smartphones, and consistent connectivity to work effectively at scale. When large portions of the population are offline or have unstable connections, providers cannot rely on digital channels for appointment management, messaging, education, or AI assistants. Hence, utilization stays low, slowing procurement as health systems hesitate to invest in such AI engagement platforms. As a result, adoption in emerging regions often grows unevenly, with AI engagement scaling first in urban and higher-income areas and much more slowly in other areas.

- For instance, in 2021, the International Telecommunication Union reported that internet usage was 87.0% in Europe and 81.0% in the Americas, compared to only 33.0% in Africa, and 27.0% in least developed countries (LDCs), directly limiting the addressable user base for digital engagement solutions.

Segmentation Analysis

By Component

Revenue Generation Potential of the Software Segment Led the Segment

Based on component, the market is categorized into software and services.

The software segment accounted for the largest global AI in patient engagement market share. The segment is dominated by delivering the most value through scalable platforms that automate high-volume patient care. As providers seek consistent patient experiences across channels, they prioritize software that standardizes workflows, integrates with EHRs, and continuously improves performance through updates and analytics. The shift toward subscription-based platforms that can be deployed across multiple sites to support segmental growth. These solutions account for a significant revenue share, encouraging key players to invest in developing software solutions and strategic acquisitions to diversify their product offerings.

- For instance, in January 2024, 98point6 Technologies acquired Bright.md to expand its asynchronous care technology, highlighting machine-learning AI-driven modules that support intake, documentation, and broader patient access workflows.

The services segment is expected to grow at a CAGR of 34.00% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Various Advantages and Innovative Features of Cloud-Based Deployment Boosted Segment Growth

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

In 2025, cloud-based deployment accounted for the largest revenue share. Patient engagement requires 24/7 assistance, rapid scaling during demand spikes, and consistent experiences across multiple facilities and channels, all of which is facilitated by the cloud deployment. Such factors are attributed to its market dominance. With cloud-based delivery, organizations can roll out new engagement features more quickly, integrate third-party tools more easily, and support remote configuration without heavy on-site infrastructure. This reduces deployment friction and accelerates value realization. As a result, buyers increasingly favor cloud-based models for faster modernization and easier scaling of AI-driven engagement solutions.

The advantages of cloud-based deployment are also encouraging key players to pursue strategic partnerships and accelerate adoption.

- For instance, in February 2024, RingCentral announced a unified patient care communications solution with new EHR integrations and generative AI, aimed at simplifying patient engagement workflows across healthcare organizations.

The hybrid segment is projected to grow at a CAGR of 33.50% during the forecast period.

By Technology

Machine Learning & Deep Learning Segment Led Owing to Increasing Adoption of Analytics And Automation

Based on technology, the market is segmented into natural language processing (NLP), machine learning & deep learning, and others.

In 2025, machine learning & deep learning dominated the global market, attributed to the increasing adoption of analytics and automation. ML enables smarter automation beyond simple keyword responses, including intent detection, personalization, predictive routing, and continuous optimization of engagement outcomes. These AI tools can handle complex patient queries, reduce unnecessary escalations, and improve accuracy over time through their integration. They increasingly rely on ML/DL capabilities that learn from patterns in real-world interactions. As a result, ML/DL-led solutions capture a larger share of revenue compared with basic automation-only approaches. Additionally, key companies in the market are focusing on new product launches and research and development to advance these technologies, underscoring their high importance.

- For instance, in May 2024, Sorcero launched a generative AI platform initiative focused on improving patient accessibility by creating easier-to-understand medical information, reflecting how advanced AI is being commercialized to enhance patient engagement at scale.

The natural language processing (NLP) segment is projected to grow at a CAGR of 35.54% during the study period.

By Therapeutic Area

Increasing Prevalence of Chronic Conditions to Drive the Segmental Growth

Based on therapeutic area, the market is segmented into health & wellness, chronic disease management, behavioral & mental health, and others.

The chronic disease management segment dominated the market in 2025, attributed to growing incidences of chronic disorders. It results in sustained, repeat engagement over long periods, creating a recurring need for communication, education, reminders, and patient support. As chronic regimens become more complex, patients and care teams need continuous touchpoints driving growth. As a result, chronic disease programs generate higher engagement volume and stronger ROI, supporting a larger revenue share than episodic care categories. Key players operating in the market recognize its critical applications and benefits and are bringing innovative solutions to maximize output.

- For instance, in April 2025, Medisafe launched VIA, an AI voice assistant designed to improve patient engagement and reduce enrollment friction in specialty patient support programs, illustrating its investment in continuous engagement models common in chronic care.

The behavioral & mental health segment is projected to grow at a CAGR of 39.21% during the study period.

By Application

Chatbots and Virtual Assistants Segment Led due to Higher Abandonment Rates

Based on application, the market is segmented into intelligent appointment management, patient financial engagement, communication & messaging, patient education, chatbot & virtual health assistants, and others.

In 2025, Chatbots and virtual assistants dominated the global market, as they play a critical role in patient engagement. They address the critical challenge of high patient inquiry volume by providing instant, 24/7 responses and completing routine tasks without staff involvement. When access teams are overloaded, patients experience longer wait times and higher abandonment rates, which in turn reduce appointment conversion and overall satisfaction. Virtual assistants help stabilize service levels by answering FAQs, guiding patients to appropriate care pathway, and supporting scheduling or instructions at scale. As a result, providers increasingly treat these tools as a core engagement capability and allocate a larger share of budgets to this application.

- For instance, in October 2024, Parakeet Health launched a generative AI voice platform aimed at transforming patient engagement by handling patient communication at scale for healthcare providers.

The patient financial engagement segment is projected to grow at a CAGR of 37.73% over the study period.

By End User

Hospitals & ASCs Segment Dominated Due to Higher Patient Throughput

Based on end user, the market is segmented into hospitals & ASCs, home care centers/ clinics, and others.

Hospitals and ASCs dominated the global market. The segment holds a strong position due to higher patient throughput, more complex scheduling and pre-visit coordination, and larger call-center and administrative workloads. When large facilities experience tailbacks in registration, communication, and patient instructions, it adversely affects operational efficiency. This increases the ROI of these AI engagement tools as automation improves access efficiency and standardizes communication across locations. New product launches, along with these factors, continue to reinforce the segment's dominance.

- For instance, in March 2024, Intermedia launched Intermedia Healthcare Solutions, combining AI-powered communications with integrations into leading EHR systems to streamline healthcare operations and patient communication workflows.

The home care centers/clinics segment is projected to grow at a CAGR of 39.57% over the study period.

AI in Patient Engagement Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Patient Engagement Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 2.84 billion and maintained its leading position in 2025 at USD 3.54 billion. The market in the region is expected to grow significantly over the forecast period, driven by high patient volumes and persistent staff shortages.

U.S. AI in Patient Engagement Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 4.11 billion by 2026, accounting for roughly 42.52% of global sales.

Europe

Europe is projected to grow at 35.75% over the coming years, the second-highest among all regions, and reach a valuation of USD 2.77 billion by 2026. The region is expected to grow due to strong privacy and governance expectations, which are pushing vendors to deliver regulated, healthcare-grade AI solutions.

U.K AI in Patient Engagement Market

The U.K.’s market is estimated at around USD 0.43 billion in 2026, representing roughly 4.44% of the global market.

Germany AI in Patient Engagement Market

Germany is projected to reach approximately USD 0.72 billion in 2026, equivalent to around 7.42% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 2.01 billion in 2026 and secure the position of the third-largest region in the market. The region's growth is driven by rapid increases in patient demand, expanding private hospital networks, and government digital health programs that increase investment in digital access and engagement.

Japan AI in Patient Engagement Market

The Japanese market in 2026 is estimated at around USD 0.49 billion, accounting for approximately 5.04% of the global market.

China AI in Patient Engagement Market

China is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.68 billion, representing approximately 6.99% of global sales.

India AI in Patient Engagement Market

The Indian market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 1.70% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin American market is set to reach a valuation of USD 0.24 billion in 2026. The region is experiencing market growth driven by increasing adoption of AI to reduce manual call workloads and standardize outreach with limited staffing. In the Middle East & Africa, the GCC is set to reach USD 0.08 billion by 2026.

South Africa AI in Patient Engagement Market

The South African is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.26% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global AI in patient engagement market is highly consolidated, with companies such as Epic Systems Corporation, Salesforce, Inc., Oracle, Microsoft Corporation, Nuance Communications, Inc., and Hyro AI Inc. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in February 2026, Hyro, a leading AI Agent Platform, partnered with WebMD Ignite to help health systems deliver guided, clinically aligned conversational care journeys that move patients from initial questions to meaningful next steps – such as routing, scheduling, and care navigation. Such strategic collaborations aim to drive market growth.

Other notable players in the global market include Twilio Inc., Notable Health, Inc., and Cedar Cares, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY AI IN PATEINT ENGAGEMENT COMPANIES PROFILED

- Epic Systems Corporation (U.S.)

- Salesforce, Inc. (U.S.)

- Oracle (U.S.)

- Microsoft Corporation (U.S.)

- Nuance Communications, Inc. (U.S.)

- Twilio Inc. (U.S.)

- Notable Health, Inc. (U.S.)

- Hyro AI Inc (U.S.)

- Cedar Cares, Inc. (U.S.)

- Phreesia, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Pixel Health launched One Thread, an AI-powered solution that sits above a health system's EMR and existing tech stack to unify every patient touchpoint into one branded journey. One Thread acts as an identity-first orchestration platform and branded engagement layer that wraps around and extends a health system's portals, websites, apps, contact centers, and digital tools.

- December 2025: Novo Nordisk India partnered with Healthify to launch an AI-enabled patient support programme aimed at individuals receiving obesity treatment. The platform offered guidance on lifestyle, nutrition, and adherence, combining digital support with clinical treatment pathways.

- October 2025: Tebra launched AI Review Replies and AI Review Insights, two artificial intelligence features integrated natively within its EHR+ Patient Experience package. These solutions offer native AI-powered sentiment analysis and automated review response capabilities, positioning healthcare practices to manage their online reputation better while maintaining HIPAA compliance.

- July 2025: Experity, a leading healthcare solutions provider, launched Experity Care Agent, a clinical intelligence solution designed to empower urgent care consumers to take control of their healthcare. By leveraging data, analytics, and AI to redefine how patients interact with clinics, Care Agent facilitates the entire care journey while preserving each clinic's unique voice and brand identity.

- March 2025: Cedar collaborated with Twilio to improve patient billing experiences, including AI-powered voice capabilities and SMS/voice communications.

REPORT COVERAGE

The global AI in patient engagement analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 37.28% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Therapeutic Area, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Therapeutic Area |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.67 billion in 2025 and is projected to reach USD 122.01 billion by 2034.

In 2025, the market value stood at USD 3.54 billion.

The market is expected to grow at a CAGR of 37.28% over the forecast period.

By component, the software segment led the market.

Increasing investment in AI agents to deflect repetitive calls is driving market growth.

Epic Systems Corporation, Salesforce, Inc., Oracle, Microsoft Corporation, and Nuance Communications, Inc. are the top market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us