AI in Telehealth & Telemedicine Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (Cloud-based, On-Premise, and Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing, Computer Vision, and Others), By Modality (Synchronous, Asynchronous, and Hybrid), By Application (Clinical Care Enablement, Remote Patient Monitoring (RPM), Clinical Documentation & Clinician Productivity, Patient Engagement & Experience, & Others), By End User (Healthcare Providers, Homecare, & Others), and Regional Forecast, 2026-2034

AI in Telehealth & Telemedicine Market Size and Future Outlook

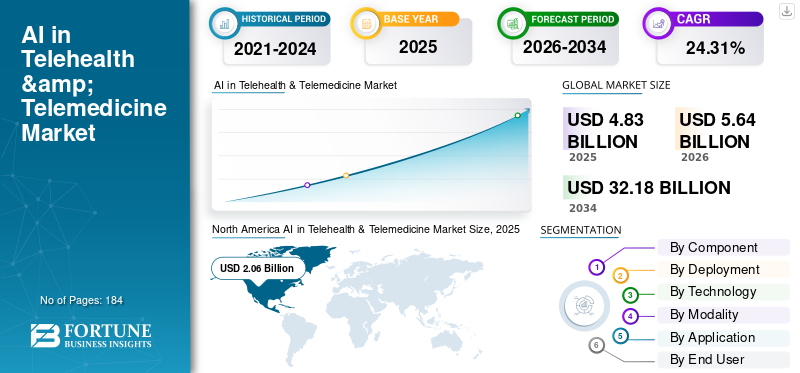

The global AI in telehealth & telemedicine market size was valued at USD 4.83 billion in 2025. The market is projected to grow from USD 5.64 billion in 2026 to USD 32.18 billion by 2034, exhibiting a CAGR of 24.31% during the forecast period. North America dominated the AI in telehealth & telemedicine market with a market share of 42.65% in 2025.

AI in telehealth & telemedicine involves using artificial intelligence to enhance virtual care through real-time video/voice consultations, asynchronous messaging, store-and-forward methods, and hybrid approaches. It improves traditional telehealth methods by alleviating clinician administrative tasks, increasing throughput and accessibility, tailoring patient education and involvement, and streamlining scheduling, capacity management, and contact-center functions via smart automation. Factors affecting this market comprise the ongoing standardization of virtual care after the pandemic, rising chronic conditions prevalence that necessitates continual monitoring, ongoing clinician shortages and burnout that elevate the need for automated documentation, and payer/provider emphasis on reducing costs.

Key companies such as Teladoc Health, Amwell, Included Health, Microsoft, and specialized AI firms are enhancing AI-driven telehealth solutions via integrated platforms that merge intake and navigation, virtual visit facilitation, ambient documentation, RPM analytics, and operational insights.

Download Free sample to learn more about this report.

AI IN TELEHEALTH & TELEMEDICINE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.83 Billion

- 2026 Market Size: USD 5.64 Billion

- 2034 Forecast Market Size: USD 32.18 Billion

- CAGR: 24.31% from 2026–2034

- North America dominated the AI in telehealth & telemedicine market, accounting for 42.65% of the market share in 2025.

- The software segment dominated the market in 2025.

- The cloud-based segment is expected to account for 60.8% of the global market share in 2026.

North America

Reached USD 2.06 billion in 2025 after recording USD 1.78 billion in 2024, supported by strong AI adoption and a robust healthcare ecosystem.

Europe

The market is expected to grow at a 22.91% CAGR during the forecast period, supported by mature healthcare systems and regulatory initiatives.

Asia Pacific

The market is projected to reach USD 1.03 billion by 2026, driven by expanding telemedicine infrastructure and digital health programs.

U.S.

The U.S. market is projected to reach USD 2.22 billion by 2026, accounting for approximately 39.4% of the global market.

Japan

The Japanese market is projected to reach USD 0.15 billion by 2026, representing approximately 2.7% of global revenue.

Read More

AI in TELEHEALTH & TELEMEDICINE MARKET TRENDS

Advances in AI Algorithms and Expansion of RPM Platforms is a Significant Market Trend

Improvements in AI algorithms and the growth of Remote Patient Monitoring (RPM) systems are emerging as a distinct trend in AI-enhanced telehealth, as providers transition from virtual visits only to ongoing, predictive care between appointments. Recent ML models can analyze high-frequency vital signs and symptom indicators to identify subtle declines sooner, minimize false alerts, and prioritize clinician intervention, in turn enhancing the scalability of RPM programs with limited personnel. Simultaneously, RPM platforms are broadening their scope beyond fundamental chronic care to include hospital-at-home, post-acute recovery, and virtual wards, where AI-powered triage and escalation protocols help maintain safety while reducing facility strain. This trend is further enhanced by the growing adoption of RPM data in virtual-care processes, driving higher recurring software and analytics revenues. These factors are supporting the overall global AI in telehealth & telemedicine market growth.

- For instance, in July 2025, Philips announced results from its partnership with Western Australia Health, highlighting remote monitoring innovation through the Health in a Virtual Environment (HIVE) service, enabled by Philips’ advanced patient monitoring technologies and reporting outcomes such as reduced ICU hours and per-patient cost savings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Shortage of Clinical Staff and Need for Automation in Remote Care Amplified Market Growth

Rising shortage of clinical staff is a strong driver of AI in telehealth & telemedicine market. Health systems are being forced to deliver more care with fewer clinicians, especially in primary care and nursing-heavy workflows. The World Health Organization has raised its projected global health workforce shortage by 2030 to 11 million, increasing pressure to redesign care models rather than rely solely on hiring. In remote care, this directly translates into demand for automation that reduces non-clinical load, AI-assisted documentation, automated intake/triage, smart routing, follow-up reminders, and escalation triggers, so that clinicians can focus on higher-acuity decisions. Automation also helps virtual programs scale safely by standardizing workflows and improving throughput during demand peaks without proportional staffing increases. All these factors cumulatively drive the overall market growth.

- For instance, in August 2025, Highmark Health announced an enterprise-wide collaboration with Abridge to deploy ambient AI clinical documentation and develop AI-enabled prior authorization at the point of conversation.

MARKET RESTRAINTS

Regulatory Uncertainty and Need for Clinical Validation to Hamper Market Growth

Regulatory ambiguity and the need for clinical validation hinder AI-enabled telehealth, as numerous tools exist in a gray area between workflow support and clinical decision/diagnosis, which can rapidly alter approval, documentation, and quality-system requirements. When vendors are unable to accurately predict whether their AI capabilities will be classified as a medical device, they postpone product launches, restrict claims, or defer entering specific markets, particularly for AI that screens, assesses risk, or recommends diagnoses remotely. On the buyer side, providers and payers require more robust validation evidence, which raises deployment time and costs and frequently extends pilot evaluation periods. Cross-border compliance introduces obstacles: standards for data governance, risk management, transparency, and post-market oversight may differ, making global expansion more challenging and costly. In general, uncertainty increases legal and compliance risks, leading procurement committees to be more cautious, which in turn decreases short-term adoption despite significant clinical demand. This limits market growth to a certain extent.

- For instance, in August 2025, the U.S. FDA issued a Warning Letter to SeniorLife Technologies, Inc. regarding its SeniorLife.AI mobile application, citing issues including marketing an AI-based product with diagnostic/screening claims without appropriate authorization.

MARKET OPPORTUNITIES

Increased Investor Funding into AI Healthcare Startups to Offer Market Growth Opportunities

The rise in investor funding for AI healthcare startups presents a significant market opportunity, as new capital enables vendors to progress from pilot projects to enterprise-level products that can be implemented widely. The investment focuses on AI that enhances the economics of remote care, automates intake and triage processes, provides tools to improve clinician productivity, and develops continuous remote monitoring models to minimize unnecessary utilization. This speeds up product development for regulated healthcare requirements such as security, clinical governance, integration with EHR/RPM systems, and ongoing model monitoring features that providers and payers are increasingly requesting before significant rollouts. It facilitates quicker geographical growth, partnerships with channels, and service capacity, which decreases adoption obstacles and broadens reachable customer segments. At the same time, broader investments in digital health have shifted the focus to AI, boosting the number of well-financed rivals and accelerating innovation processes, thereby broadening the market by expanding use cases and reducing time-to-value for purchasers. In summary, investor funding serves as a catalyst that transforms high demand for remote-care automation into scalable, commercial applications. All these factors would drive the market growth over the coming years.

- For instance, in October 2025, Brook.ai announced that it secured USD 28 million in Series B funding (led by UMass Memorial Health and Morningside) to accelerate growth and innovation in remote care, illustrating how investor funding is being used to scale AI-enabled virtual care delivery models.

MARKET CHALLENGES

Lack of Reliable Digital Infrastructure in Rural or Resource-Limited Settings Pose a Prominent Challenge to Market Growth

The absence of dependable digital infrastructure in rural or resource-constrained areas continues to pose a significant challenge for AI-driven telehealth & telemedicine, as the quality of virtual care depends on stable broadband or mobile connectivity, minimal latency, and sufficient bandwidth for virtual consultations, image uploads, and ongoing RPM data transmission. When the connection is poor, interactions transition from video to audio or don't occur at all, leading to deficiencies in clinical context and diminishing the efficacy of AI-driven processes such as automated intake, immediate risk evaluation, and CV-based remote evaluations. Intermittent networks also lead to increased drop-outs during onboarding and follow-ups, resulting in reduced program adherence and making outcomes more challenging to demonstrate, hindering payer/provider expansion. In AI, inadequate infrastructure restricts access to high-quality multimodal inputs such as video, high-frequency vitals, and images, leading to more false alerts or necessitating conservative thresholds that diminish effectiveness. All the factors cumulatively affect the market growth.

- For example, the Digital Progress and Trends Report 2023 from the World Bank Group indicated that in 2022, merely one out of four people in middle-income nations had access to the internet. In high-income and upper-middle-income countries, fixed broadband subscriptions surpassed 30 per 100 individuals, whereas in lower-middle-income and low-income nations, the numbers were significantly lower at 4.4 and 0.5, respectively.

Segmentation Analysis

By Component

Software-centric Virtual Care Workflows to Drive the Software Segment’s Dominance

Based on the component, the market is divided into services and software.

In 2025, the software segment dominated the market, as most AI value in telehealth is delivered through scalable platforms and modules such as AI-enabled intake/triage, clinician-facing documentation and summarization, workflow orchestration, RPM analytics dashboards, and intelligent scheduling/routing. These capabilities are typically monetized through subscriptions and usage-based licensing, and they can be rolled out rapidly across sites and specialties without proportionate headcount increases. In addition, tighter integration of AI into telehealth platforms and EHR-connected “digital front doors” has increased recurring license spend versus one-time services.

- For instance, in March 2025, Zoom announced Zoom Workplace for Clinicians and a select beta of Custom AI Companion for Healthcare, highlighting AI-driven workflow and documentation enhancements within its healthcare software stack.

The services segment is anticipated to rise with a CAGR of 26.56% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Faster Rollouts and Easier Scaling to Drive the Cloud-based Segment’s Dominance

Based on the deployment, the market is divided into cloud-based, hybrid, and on-premise.

The cloud-based segment is anticipated to capture the largest global AI in telehealth & telemedicine market share in 2025. Most telehealth AI tools need quick setup, elastic compute, and frequent model updates, which are easier to deliver through the cloud. Cloud deployment also helps providers and payers scale virtual care across multiple sites without buying and maintaining heavy IT infrastructure. In addition, cloud platforms simplify integration with EHRs, contact centers, and RPM dashboards, enabling standardized workflows for AI triage, documentation, and alerting across service lines. As virtual care volumes fluctuate, cloud systems handle peak demand better and support usage-based pricing, which buyers prefer for cost control. Furthermore, the segment is set to hold a 60.8% share in 2026.

- For instance, in February 2025, Caregility launched next-gen virtual care coordination and ambient AI solutions built on the Caregility Cloud virtual care platform.

The hybrid segment is anticipated to rise with a CAGR of 21.52% over the forecast period.

By Technology

Predictive Analytics and Signal Interpretation to Drive the ML & Deep Learning Segment’s Growth

In terms of technology, the market is divided into natural language processing, machine learning & deep learning, computer vision, and others.

The machine learning & deep learning segment dominated the global market in 2025. ML/DL models handle large volumes of time-series data from wearables and home devices and convert it into actionable insights, which directly improve clinical efficiency in remote care. These algorithms are also widely embedded inside telehealth platforms for automated triage, escalation rules, and population-level monitoring, making them easier to scale than specialist point solutions. Additionally, new product launches based on these technologies also support the segment growth. Furthermore, the segment is set to hold a 39.7% share in 2026.

- For instance, in August 2025, InfoBionic.Ai announced FDA 510(k) clearance for its MoMe ARC 1-Lead Patch, extending its AI-enabled remote cardiac monitoring platform.

The natural language processing segment is expected to grow with a CAGR of 26.34% over the forecast period.

By Modality

Real-time Doctor–Patient Interaction to Drive the Synchronous Segment’s Dominance

In terms of modality, the market is divided into synchronous, asynchronous, and hybrid.

The synchronous segment captured the highest share of the global market in 2025. Most telehealth care still relies on live video/voice consultations where clinicians can ask follow-up questions instantly, assess urgency in real time, and make faster treatment decisions. Synchronous visits are also preferred for higher-acuity cases such as urgent care, complex symptoms, and medication changes, where payers and providers want stronger clinical confidence and clearer documentation. In addition, many hospitals scaled synchronous virtual workflows in inpatient and emergency settings, such as virtual rounding and specialist consults, which improve access to clinicians without delaying care. Furthermore, the segment is set to hold a 54.0% share in 2026.

- For instance, in February 2025, hellocare.ai announced a planned system-wide implementation at AdventHealth to expand virtual care across more than 13,000 inpatient and emergency department beds—highlighting ongoing investment in real-time (synchronous) provider engagement and monitoring workflows.

The asynchronous segment is anticipated to rise with a CAGR of 29.14% over the forecast period.

By Application

Core Virtual Care Functions to Propel the Clinical Care Enablement Segment’s Growth

On the basis of application, the market is divided into clinical care enablement, Remote Patient Monitoring (RPM), clinical documentation & clinician productivity, patient engagement & experience, revenue cycle & administrative automation, virtual care operations optimization, and others.

The clinical care enablement segment captured the highest share of the global market in 2025. Providers and payers prioritize this segment as it improves access and throughput without increasing clinical staff proportionally. As virtual care volumes grow, standardized enablement software reduces variability across sites and makes quality easier to manage. Even when other applications expand, enablement remains the base layer that connects patient entry, clinician workflow, and follow-ups, keeping it the largest revenue pool in many deployments. Furthermore, the segment is set to hold a 21.5% share in 2026.

- For instance, in April 2025, CareXM launched its AI-powered Artificial Intelligence Decision Assistant (AIDA) to guide clinical triage and speed up virtual care coordination for home-based/post-acute care.

The revenue cycle & administrative automation segment is anticipated to rise with a CAGR of 25.31% over the forecast period.

By End User

Provider-led Adoption of AI Virtual Care Platforms to Drive the Healthcare Providers Segment’s Dominance

Based on end user, the market is segmented into healthcare payers, healthcare providers, homecare, and others.

In 2025, the healthcare providers segment held the leading position in the global market. Hospitals and clinics are the main controllers of clinical workflows in which AI is used daily, such as patient admission, triage, online consultations, record-keeping, and decision-making for escalations. Providers are also the primary buyers of telehealth platforms and AI modules to enhance access and reduce clinician workload, meaning that the majority of revenue is initially generated at the provider level. Additionally, healthcare providers require AI to standardize care protocols across various departments and locations, particularly for high-demand scenarios such as urgent care, inpatient virtual nursing, and specialist consultations. As capacity limitations increase, provider-led implementations expand more rapidly since they provide instant operational ROI. Furthermore, the segment is set to hold a 56.0% share in 2026.

- For instance, in March 2026, Cooper University Health Care selected hellocare.ai as its enterprise platform for AI-assisted intelligent hospital rooms, virtual nursing, and virtual sitting.

In addition, homecare segment are projected to witness 30.63% growth rate during the forecast period.

AI in Telehealth & Telemedicine Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI in Telehealth & Telemedicine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the North America market reached USD 1.78 billion, accounting for the largest share of the global market. In 2025, the region maintained its leading position, with USD 2.06 billion. In North America, growth is mainly fueled by the largest adoption of AI-enabled telehealth, a strong payer/tech ecosystem, and workforce shortages that push automation.

U.S. AI in Telehealth & Telemedicine Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 2.22 billion in 2026, accounting for roughly 39.4% of global market.

Europe

Europe’s market size is expected to grow at a CAGR of 22.91% during the forecast period. The regional growth is supported by regulatory push toward cross-border health data availability, mature healthcare systems, and increasing chronic disease burden across European countries.

U.K AI in Telehealth & Telemedicine Market

The U.K. market in 2026 is estimated at around USD 0.32 billion, representing roughly 5.7% of global revenues.

Germany AI in Telehealth & Telemedicine Market

Germany’s market size is projected to reach approximately USD 0.36 billion in 2026, equivalent to around 6.4% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 1.03 billion by 2026, making it the third largest region in the global market. In the Asia Pacific, growth is propelled by rapid adoption in key countries such as China, India, and South Korea, by expanding telemedicine infrastructure, and by increasing national digital health infrastructure programs across Asia.

Japan AI in Telehealth & Telemedicine Market

The Japanese market in 2026 is estimated at around USD 0.15 billion, accounting for roughly 2.7% of global revenues.

China AI in Telehealth & Telemedicine Market

China’s market is projected to reach revenues of around USD 0.34 million in 2026, representing roughly 6.0% of global sales.

India AI in Telehealth & Telemedicine Market

The Indian market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 2.8% of global revenues.

Latin America and the Middle East & Africa

The Middle East & Africa and Latin America are expected to experience slower growth throughout the forecast period. By 2026, the market value in Latin America is projected to hit USD 0.41 billion. Crucial factors, such as significant unmet patient needs, rising healthcare expenditures, and government-initiated digital transformation initiatives, are expected to drive expansion in these areas.

In the Middle East & Africa, the GCC market is projected to attain approximately USD 0.11 billion by 2026, representing about 2.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Client Base of Key Companies to Strengthen Market Share

The global AI in telehealth & telemedicine market reflects a moderately fragmented structure, with the presence of well-established players and an increasing number of new market entrants. Key entities in this space include Teladoc Health, Microsoft, Oracle, and others. These organizations are progressively highlighting LLM/GenAI integration for symptom capture, care navigation, and visit summarization, along with stronger security and governance, and integrations with EHR/RPM/RCM systems to reduce provider adoption friction and accelerate enterprise rollouts.

Other prominent players in the market include Ada Health GmbH,Infermedica, TytoCare Ltd., Abridge Al, Inc. and others. Emphasis on new software launches, customer expansion, and partnerships is a key strategic undertaking for these players.

- For instance, in July 2025, Fabric announced a strategic partnership with Rush University System for Health to launch AI-powered Rush Connect, using Fabric’s AI assistant and virtual care platform to guide patients from symptom intake to appropriate care while expanding capacity and improving access.

LIST OF KEY AI in TELEHEALTH & TELEMEDICINE COMPANIES PROFILED

- Epic Systems Corporation (U.S.)

- Microsoft (U.S.)

- Alphabet Inc. (U.S.)

- Oracle (U.S.)

- Hello Heart (U.S.)

- Teladoc Health, Inc. (U.S.)

- Ada Health GmbH (Germany)

- Infermedica (Poland)

- TytoCare Ltd. (U.S.)

- Abridge Al, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Ardent Health partnered with hellocare.ai to deploy AI-assisted virtual physicians, virtual nursing, and virtual patient safety monitoring across 2,000+ patient rooms, scaling remote care operations.

- February 2026: Ubie and Mayo Clinic announced a collaboration to co-develop an AI-driven chat/voice triage that routes patients and supports scheduling 24/7, strengthening digital front door telehealth workflows.

- January 2026: VSee announced a strategic partnership with DocBox to build an AI-native Virtual ICU operating system that embeds augmented intelligence into tele-ICU workflows for scalability.

- October 2025: League and Amwell announced a collaboration to combine AI-driven member experience/engagement with virtual care programs, aiming to reduce friction and improve care navigation.

- February 2025: Andor Health announced that it received a Vizient national contract for its AI-first virtual care collaboration platform, expanding access for provider organizations to deploy AI-enabled virtual workflows at scale.

REPORT COVERAGE

The global AI in telehealth & telemedicine market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers, and acquisitions, along with significant advancements in the industry within the market. The market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.31% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Modality, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Modality |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.83 billion in 2025 and is projected to reach USD 32.18 billion by 2034.

In 2025, the North Americas market value stood at USD 2.06 billion.

The market is expected to exhibit a CAGR of 24.31% during the forecast period.

By component, the software segment led the market in 2025.

Rising shortage of clinical staff and need for automation in remote care are the key factors driving the market.

Teladoc Health, Inc., Epic Systems Corporation, and Microsoft are some of the prominent players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 184

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us