AI in Ultrasound Imaging Market Size, Share & Industry Analysis, By Component (Hardware/Devices, and Software & Services), By Deployment (Cloud-Based, On-Premise, and Hybrid), By Technology (Machine Learning & Deep Learning, Computer Vision, and Others), By Clinical Area (General Imaging/Abdomen, OB/GYN, Cardiology, Musculoskeletal, Vascular, Breast & Thyroid, and Others), By Application (Image Acquisition Guidance, Image Reconstruction/Enhancement, Measurement & Quantification, Lesion Detection/Triage, Workflow/Reporting, & Others), By End User, and Regional Forecast, 2026-2034

AI in Ultrasound Imaging Market Size and Future Outlook

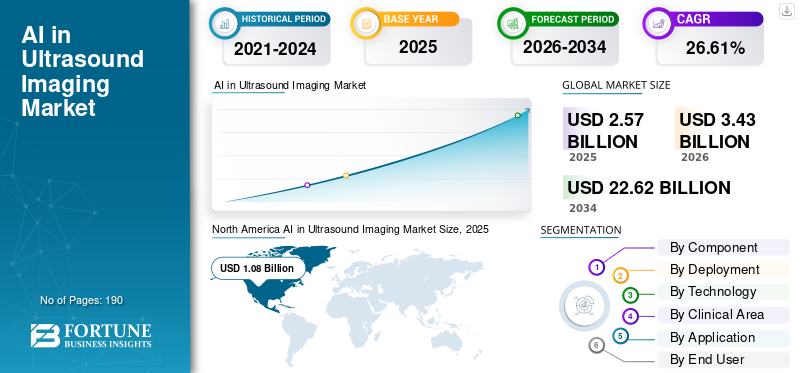

The AI in ultrasound imaging market size was valued at USD 2.57 billion in 2025. The market is projected to grow from USD 3.43 billion in 2026 to USD 22.62 billion by 2034, exhibiting a CAGR of 26.61% during the forecast period. North America dominated the AI in ultrasound imaging market with a market share of 42.02% in 2025.

AI is increasingly used in ultrasound systems to support image acquisition, automate image measurements, enhance visualization, and reduce operator dependence. These critical applications become especially important as healthcare providers face growing imaging volumes and staff shortages, driving elevated global demand for AI in ultrasound imaging. The market is estimated to grow exponentially over the forecast period. The rising need for faster diagnosis, improved workflow efficiency, and greater imaging consistency across healthcare settings drives the market.

Major companies operating in the market are directing their resources toward new product launches to capitalize on the market's growth potential and incorporate AI capabilities into their AI solutions.

- For instance, in August 2025, GE HealthCare launched Vivid Pioneer, its AI-powered cardiovascular ultrasound system designed to enhance speed and image quality. Such advanced product launches strengthen clinical adoption of AI-enabled ultrasound systems and support the market's overall growth.

Furthermore, key players in the industry, such as GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, and Samsung Healthcare, are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

AI in Ultrasound Imaging Market Takeaways

- 2025 Market Size: USD 2.57 billion

- 2026 Market Size: USD 3.43 billion

- 2034 Forecast Market Size: USD 22.62 billion

- CAGR: 26.61% from 2026–2034

- North America dominated the AI in ultrasound imaging market with a 42.02% share in 2025.

- Software & services held the largest market share in 2025, driven by AI-powered workflow, measurement, and reporting capabilities.

- Cloud-based deployment accounted for the largest market share in 2025 due to its scalability and enterprise integration benefits.

North America

North America led the market with USD 1.08 billion in 2025, supported by strong hospital adoption and rapid AI integration into imaging workflows.

Europe

Europe is projected to reach USD 0.79 billion in 2026, driven by increasing demand for workflow efficiency and cloud-connected imaging services.

Asia Pacific

Asia Pacific is expected to reach USD 0.91 billion in 2026, fueled by rising healthcare demand and expanding access to diagnostic imaging.

U.S.

The market is estimated at USD 1.34 billion in 2026, accounting for approximately 38.98% of global revenue.

Japan

The market is estimated at USD 0.20 billion in 2026, representing around 5.71% of the global market.

Read More

AI IN ULTRASOUND IMAGING MARKET TRENDS

Integration of Advanced AI Tools in Cardiovascular and Women's Health Ultrasound is a Significant Market Trend

The increasing adoption of advanced AI is a prominent market trend. Cardiovascular and women's health exams often require high image precision, multiple measurements, and fast clinical decision-making. When AI is integrated into these ultrasound systems, it helps automate workflows, improve measurement consistency, reduce exam complexity, and support faster diagnosis. This makes ultrasound more efficient for clinicians and more reliable across different care settings. As a result, companies are increasingly embedding advanced AI capabilities into cardiovascular and women's health ultrasound platforms. Companies are also increasingly launching suite-specific offerings to strengthen their market position.

- For instance, in August 2025, Koninklijke Philips N.V. launched the Transcend Plus, its EPIQ CVx, and Affiniti CVx cardiovascular ultrasound systems. Transcend Plus features FDA-cleared 2D- and 3D-image quality enhancements, along with a suite of AI-enabled clinical applications. Such developments are expected to boost global AI in ultrasound imaging market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Imaging Volumes and Radiology Workload is Driving Market Growth

The market is noticing growth as healthcare providers handle a rising number of imaging exams and face pressure to deliver faster, more consistent results. As patient volumes increase, radiologists, sonographers, and clinicians need tools that can reduce scan time, automate measurements, support image interpretation, and improve workflow efficiency. This creates strong demand for AI-enabled ultrasound systems, as they help manage heavy workloads, improve productivity, and reduce operator dependency. As a result, growing imaging volumes and rising clinical workload are directly supporting the adoption of AI in ultrasound imaging. Furthermore, due to the need for efficient AI tools, key companies are increasingly investing in innovative product launches catering to the product demand.

- For instance, in February 2025, Royal Philips introduced new AI-assisted workflow and quantitative measurement functions in its EPIQ Elite and Affiniti ultrasound systems to help speed up exams and improve clinical confidence. Such product developments show how companies are responding to increasing imaging workloads with automation-led solutions, which are expected to support the overall growth of the market.

MARKET RESTRAINTS

Limited Reimbursement Support for AI-Assisted Ultrasound Procedures to Hamper Market Growth

Challenges related to reimbursement support remain a leading restraint for the market. Reimbursement systems in many countries are designed to cover the ultrasound scan itself, but not always the added value created by AI-enabled automation, decision support, or measurement tools. When hospitals and diagnostic centers do not receive clear or separate payment for these AI functions, they often find it difficult to invest in the additional software costs and implementation expenses. This slows purchasing decisions, delays wider deployment, and reduces the commercial incentive for providers to adopt AI-assisted ultrasound solutions at scale. As a result, limited reimbursement support remains an important factor restraining the market growth.

- For instance, in November 2025, the Journal of the American College of Radiology published an article titled 'Reimbursement for Artificial Intelligence Software as a Medical Device in Radiology, ' which reported that adoption of AI software as a medical device remains limited by evolving, yet nascent, reimbursement policies. These published findings highlight that unclear payment pathways can still hold back market expansion.

MARKET OPPORTUNITIES

Expansion of AI-Enabled Point-of-Care Ultrasound Creates New Market Growth Opportunities

The market is noticing a strong growth opportunity through the expansion of point-of-care ultrasound. The increasing demand from healthcare providers for faster, more portable, and easier-to-use imaging tools supports the market's growth potential. When AI is added to point-of-care ultrasound systems, it helps guide image acquisition, automates documentation, improves workflow efficiency, and supports more consistent use across departments. This makes ultrasound more accessible beyond traditional imaging rooms and increases its value in emergency care, critical care, primary care, and hospital-wide clinical workflows. As a result, the expansion of AI-enabled point-of-care ultrasound is opening new revenue opportunities and expanding the market's adoption potential.

- For instance, in November 2025, Butterfly Network, Inc. launched Compass AI, an artificial intelligence-powered enterprise platform designed to reduce workflow friction and support scalable, revenue-ready point-of-care ultrasound programs for health systems. Such development highlights that companies are increasingly building AI-enabled platforms that help health systems expand Point-Of-Care Ultrasound (POCUS) at scale and create new long-term growth opportunities for the market.

MARKET CHALLENGES

Uneven Infrastructure in Emerging Markets is Limiting Market Growth

The market faces a challenge of uneven infrastructure in emerging markets. Many healthcare systems still lack the digital, clinical, and operational infrastructure needed to support advanced AI-enabled imaging solutions. When hospitals and clinics have limited connectivity, fewer trained users, restricted maintenance support, and lower access to sustainable imaging resources, the adoption of AI ultrasound systems becomes slower and more difficult. This reduces providers' ability to implement such tools consistently across healthcare settings, even when the clinical need is high.

- For instance, a 2025 article in BMC Pregnancy and Childbirth on AI-enabled obstetric point-of-care ultrasound in low and middle-income countries reported that widespread access to ultrasound is challenged by a lack of trained providers, workload pressures, and inadequate resources required for sustainability. These findings show that infrastructure and implementation gaps can directly slow market expansion in emerging regions.

Segmentation Analysis

By Component

Revenue Generation Potential of Software & Services Leads to Segmental Growth

Based on the component, the market is categorized into hardware/devices and software & services.

Among these, software & services dominated the market. Some of the critical functions of AI in ultrasound are driven by software, including image optimization, automated measurements, workflow support, decision support, and reporting tools. Many healthcare providers can adopt AI by upgrading or adding software to existing ultrasound platforms, enabling faster, more scalable deployment than replacing full systems. Such factors increase recurring revenue opportunities through licenses, upgrades, and service contracts. As a result, software & services are estimated to have a leading share in the market. Additionally, key players are launching new products, supporting the segmental growth.

- For instance, in February 2025, Philips introduced a new Elevate software release for its EPIQ Elite and Affiniti ultrasound platforms, featuring AI-assisted workflows and quantitative measurement functions to speed up exams and improve clinical confidence. Such developments show the way vendors are creating market value through software-led AI enhancements, which supports the dominance of the software & services segment.

The hardware/devices segment is expected to grow at a CAGR of 24.69% over the global market forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Scalability Opportunity Offered by Cloud-Based Deployments Leads to Segmental Growth

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

In 2025, the cloud-based deployment accounted for the largest AI in ultrasound imaging market share. The largest share was attributed to the segment as healthcare providers are increasingly preferring AI solutions that can be centrally updated, scaled across multiple sites, and these cloud solutions are integrated with enterprise workflow systems. Cloud delivery also makes it easier to manage data, compliance, analytics, and software upgrades without a heavy on-site IT burden. These features help health systems standardize ultrasound programs across departments and facilities. These advantages are prompting key players to focus on new product launches and drive the segmental growth.

- For instance, in November 2025, Butterfly Network launched Compass AI, an AI-powered enterprise software platform designed to support scalable and compliant point-of-care ultrasound programs for health systems. This kind of connected enterprise platform highlights why cloud-based deployment is gaining strong traction in the market.

The hybrid segment is projected to grow at a CAGR of 25.77% over the study period.

By Technology

Presence of Wider Cutting Edge Technology Including Intelligent Workflow Engines Leads to Other Segment Dominance

Based on technology, the market is segmented into computer vision, machine learning & deep learning, and others.

In 2025, the others segment dominated the market based on technology. AI applications in ultrasound are not limited to image recognition or deep learning models, but also include a wider set of enabling technologies such as intelligent workflow engines, autonomous scan guidance, software-defined imaging, beamforming, and embedded automation tools. These technologies are used to improve exam speed, standardization, and usability across broader clinical settings, which makes them highly valuable for routine adoption. Such varied use cases of other innovative technologies drive the growth of the segment.

Major companies operating in the market are focusing on technologically advanced offerings and strategic collaborations to strengthen their market position.

- For instance, in March 2025, GE HealthCare collaborated with NVIDIA to advance autonomous X-ray and ultrasound solutions, focusing on AI-driven software to capture and analyze medical images with less burden on technicians and radiologists. Such developments show that the market is increasingly moving toward broader enabling technologies, which supports the dominance of the other segment.

The computer vision segment is projected to grow at a CAGR of 27.80% during the forecast period.

By Clinical Area

New Product Launches in OB/GYN to Leads to Segment Growth

Based on clinical area, the market is segmented into general imaging/abdomen, OB/GYN, cardiology, musculoskeletal, vascular, breast & thyroid, and others.

In 2025, OB/GYN dominated the market as ultrasound is one of the most widely used imaging tools in women's health for routine pregnancy monitoring, fetal assessment, gynecological evaluation, and reproductive care. Thus, AI creates strong value in the area by improving image consistency, supporting faster measurements, reducing operator dependence, and helping clinicians manage high patient volumes more efficiently. Such critical applications make AI useful in OB/GYN settings where workflow speed and repeatability are critical for regular screening and follow-up.

- For instance, in January 2025, Samsung Medison launched the Samsung Z20, an AI-powered Ob-Gyn ultrasound system designed for advanced women's health applications. Such product launches show that companies are actively prioritizing AI innovation in OB/GYN imaging, which supports the segment's leading position in the market. underscoring the segment's market leadership.

In addition, the others segment is projected to grow at a CAGR of 27.26% during the study period.

By Application

Increasing Screening Volumes to Drive Demand for AI in Measurement & Quantification and Fuel the Segment Growth

Based on application, the market is segmented into image acquisition guidance, image reconstruction/enhancement, measurement & quantification, lesion detection/triage, workflow/reporting, training/QA, clinical trial matching & patient stratification, and others.

The measurement & quantification segment accounted for the largest share of the global market. The segment dominated as one of the most immediate uses of AI in ultrasound is automating repetitive measurements and standardizing exam outputs. These tools reduce manual effort, improve consistency between users, and help clinicians’ complete exams faster with fewer variations. This makes them easier to adopt in routine clinical practice than more advanced or experimental use cases. Key companies need to innovate their offerings through strategic collaborations.

- For instance, in 2024, Siemens Healthineers introduced AI Abdomen as part of the ACUSON Sequoia 3.5 ultrasound release, with the software automatically labeling and measuring organs in milliseconds to improve standardization and workflow efficiency. Such innovations show why automated measurement and quantification tools are gaining strong demand in ultrasound imaging.

In addition, the workflow/reporting segment is projected to grow at a CAGR of 27.53% during the study period.

By End User

Increasing Demand in Hospitals & Health Systems Due to Large Patient Volumes Leads to Segment Growth

Based on end user, the market is segmented into hospitals & health systems, diagnostic imaging centers, ambulatory/specialty clinics, primary care/emergency, and others.

By end user, the hospitals & health systems dominated the market as they manage the highest imaging volumes, handle more complex patient cases, and have greater budgets for advanced imaging technology. They also benefit abundantly from AI tools that improve workflow, standardization, and productivity across multiple departments. Since large health systems are under pressure to improve efficiency while maintaining diagnostic quality, they are usually the earliest adopters of AI-enabled ultrasound platforms.

- For instance, in February 2025, Canon Medical Systems introduced Aplio beyond, a premium ultrasound solution aimed at expert users in demanding, high-throughput clinical environments such as hospitals and busy imaging centers. Such developments reflect the continued dominance of large provider organizations as the primary target for advanced AI-enabled ultrasound solutions, supporting the hospitals & health systems segment.

The primary care/emergency segment is projected to grow at a CAGR of 29.60% over the study period.

AI in Ultrasound Imaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Ultrasound Imaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.80 billion and maintained its leading position in 2025 at USD 1.08 billion. The market in North America is expected to grow significantly over the forecast period, driven by high imaging volumes, strong hospital adoption of digital health tools, and faster commercialization of AI-enabled ultrasound platforms. It holds the largest regional share, supported by its chronic disease burden, strong reimbursement, and rapid AI integration into imaging workflows.

U.S. AI in Ultrasound Imaging Market

Given North America's substantial contribution, the U.S. market is estimated at around USD 1.34 billion in 2026, accounting for roughly 38.98% of global sales.

Europe

Europe is projected to grow at 26.69% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.79 billion by 2026. The market is growing in Europe as healthcare providers face pressure to improve workflow efficiency, standardize imaging quality, and expand cloud-connected radiology services across hospital networks.

U.K. AI in Ultrasound Imaging Market

The U.K. market is estimated at around USD 0.16 billion in 2026, representing roughly 4.76% of the global market.

Germany AI in Ultrasound Imaging Market

Germany's market is projected to reach approximately USD 0.20 billion in 2026, equivalent to around 5.72% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.91 billion in 2026 and secure the position of the third-largest region in the market. The market is growing rapidly in the region due to rising healthcare demand, a growing chronic disease burden, and a shortage of skilled diagnostic professionals in many densely populated and remote areas.

Japan AI in Ultrasound Imaging Market

The Japanese market in 2026 is estimated at around USD 0.20 billion, accounting for approximately 5.71% of the global market.

China AI in Ultrasound Imaging Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.28 billion, representing approximately 8.05% of global sales.

India AI in Ultrasound Imaging Market

The Indian market in 2026 is estimated at around USD 0.12 billion, accounting for roughly 3.52% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in the market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.18 billion in 2026. The region is experiencing market growth, as providers seek more portable, cost-effective imaging solutions to expand access beyond major urban centers. In the Middle East & Africa, the GCC is set to reach USD 0.05 billion in 2026.

South Africa AI in Ultrasound Imaging Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.41% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches and Regulatory Approvals by Key Players to Propel Market Competition

The market is highly consolidated, with companies such as GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, Inc., Samsung Healthcare, Canon Medical Systems Corporation, and FUJIFILM Corporation holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in March 2026, GE HealthCare received 510 (k) clearance from the U.S. FDA for View, the powerful viewer within the GenesisRadiology Workspace. View serves as the core anchor of the Genesis Radiology Workspace. This next‑generation solution aims to transform radiology workflows, unify the user experience, and empower radiologists with greater efficiency and precision. Such strategic collaborations aim to drive market growth.

Other notable players in the global market include Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Butterfly Network, Inc., and EchoNous, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period for the global market.

LIST OF KEY AI IN ULTRASOUND IMAGING COMPANIES PROFILED

- GE HealthCare Technologies Inc. (U.S.)

- Koninklijke Philips N.V. (The Netherlands)

- Siemens Healthineers AG (Germany)

- Samsung Healthcare (South Korea)

- Canon Medical Systems Corporation (Japan)

- FUJIFILM Corporation (Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Butterfly Network, Inc. (U.S.)

- EchoNous, Inc. (U.S.)

- Exo Imaging, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: EchoNous unveiled a major expansion of the Kosmos platform. The company added robust OB/GYN and vascular tools to its AI-enhanced ultrasound platform, expanding use cases in emergency medicine, labor and delivery, and global health. This strengthens the market by widening the clinical scope of AI-enabled point-of-care ultrasound.

- February 2026: GE HealthCare expanded its BARDA collaboration with approximately USD 35.0 million to advance AI powered ultrasound. The investment is aimed at developing AI-powered ultrasound solutions and new platforms for trauma assessment and emergency preparedness. It is a strong market signal that public-sector-backed funding is supporting the next phase of AI ultrasound innovation.

- January 2026: Butterfly Network announced plans to extend its proprietary 3D imaging capabilities to Butterfly Garden developers. The planned API release will, for the first time, allow third-party access to Butterfly's digital 3D beam-steering capabilities, enabling the development of advanced AI-enabled image-acquisition tools. This supports market growth by opening the platform to broader AI application development.

- November 2025: Butterfly Network launched Compass AI, an artificial intelligence-powered enterprise software platform built to reduce workflow friction and support scalable, compliant, revenue-ready POCUS programs for health systems. This launch highlights the growing role of enterprise AI workflow software in the ultrasound market.

- August 2025: Royal Philips launched Transcend Plus for EPIQ CVx and Affiniti CVx. Philips released the next generation of its cardiovascular ultrasound systems with FDA-cleared AI enhancements, including advances in image quality and intelligent automation. This launch reinforces the trend toward premium AI integration in cardiovascular ultrasound.

REPORT COVERAGE

The global AI in ultrasound imaging market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market over the forecast period. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 26.61% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Clinical Area, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Clinical Area |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.57 billion in 2025 and is projected to reach USD 22.62 billion by 2034.

In 2025, the North America market value stood at USD 1.08 billion.

The market is expected to grow at a CAGR of 26.61% over the forecast period of 2026-2034.

The software component segment is expected to lead the market.

Growing imaging volumes and radiology workload supporting AI adoption are driving market growth.

GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, Inc., Samsung Healthcare, and Canon Medical Systems Corporation are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us