Airborne SATCOM Market Size, Share & Industry Analysis, By Platform (Fixed Wing Aircraft (Commercial Aircraft, Business Aircraft, General Aviation Aircraft, and Military Aircraft), Rotary Wing Aircraft (Military Helicopters, and Civil Helicopters), and UAV), By Frequency Band (L-Band, Ku-Band, Ka-Band, X-Band, and Others), By Application (In-Flight Connectivity (IFC) & Passenger Broadband, Mission Communications & C2 (Command and Control), ISR, Video & Sensor Data Backhaul, & Others), By Component (Terminals, Antennas & Radomes, & Others), By End Use, and Regional Forecast, 2026-2034

Airborne SATCOM Market Size and Future Outlook

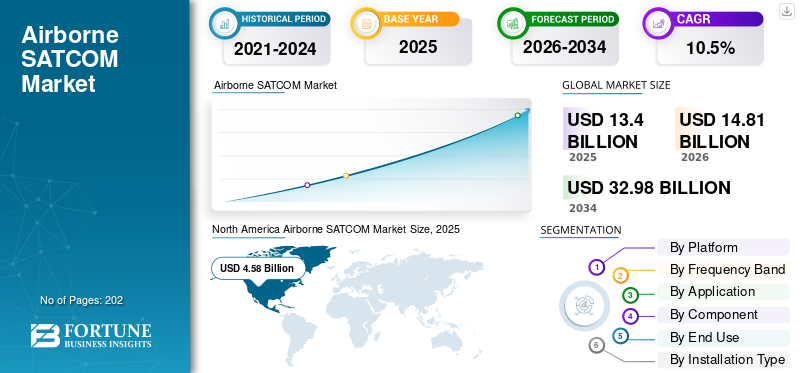

The global airborne SATCOM market size was valued at USD 13.40 billion in 2025. The market is projected to grow from USD 14.81 billion in 2026 to USD 32.98 billion by 2034, exhibiting a CAGR of 10.5% during the forecast period. North America dominated the global airborne satcom market with a market share of 34.17% in 2025.

Airborne SATCOM (Satellite Communications) refers to communication systems installed on aircraft or other airborne platforms that provide reliable, high-speed data, voice, and video transmission via satellites. These systems enable aircraft to maintain connectivity with ground stations, satellites, and other airborne assets regardless of their location or altitude, facilitating beyond-line-of-sight communication. Airborne SATCOM is crucial for real-time intelligence sharing, mission coordination, and operational agility, supporting high-data-rate connectivity across various satellite orbits.

The major players in the market include Thales Group (France), General Dynamics Corporation (U.S.), Collins Aerospace (U.S.), Honeywell International Inc. (U.S.), L3 Harris Technologies (U.S.), and Viasat Inc. (U.S.). Thales Group offers integrated airborne SATCOM systems with a focus on resilience and encryption for commercial, defense, and homeland security sectors. General Dynamics Corporation provides secure airborne SATCOM equipment, including tactical radios, advanced waveform modems, and data links.

Download Free sample to learn more about this report.

Airborne SATCOM Market Takeaways

- 2025 Market Size: USD 13.40 billion

- 2026 Market Size: USD 14.81 billion

- 2034 Forecast Market Size: USD 32.98 billion

- CAGR: 10.5% from 2026–2034

- North America dominated the airborne SATCOM market with a 34.17% share in 2025.

- The UAV segment is projected to register the highest CAGR of 13.6% during the forecast period.

- The Ka-Band segment is expected to grow at a CAGR of 12.3%, exceeding the overall market CAGR of 10.5%.

North America

North America led the global market in 2025 with revenue of USD 4.58 billion, supported by strong defense spending and advanced aviation connectivity infrastructure.

Europe

Europe is expected to witness steady growth, driven by extensive intra-European air traffic, regulatory focus on aviation safety, and investments in secure satellite communication systems.

Asia Pacific

Asia Pacific is projected to grow rapidly due to rising passenger traffic, increasing aircraft deliveries, expanding in-flight connectivity adoption, and higher defense modernization spending.

U.S.

The U.S. remains a key market owing to substantial investments in military communications, ISR operations, and next-generation airborne connectivity technologies.

Japan

Japan is witnessing increased airborne SATCOM adoption, supported by growing defense capabilities, aviation modernization programs, and demand for secure communication networks.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Demand for Reliable, High-Speed In-Flight Connectivity and Communication Expected to Drive Market Growth

One of the significant drivers for the market is the growing demand for reliable, high-speed in-flight connectivity and communication in both commercial aviation and military operations. Airlines are trying to learn ways to improve passenger experience by offering internet access, streaming, and real-time communication. Moreover, the defense sector from various countries is in need of secure, beyond-line-of-sight communications for operational efficiency and situational awareness. In addition, government agencies are partnering with numerous SATCOM solutions providers for secure, high-speed communication in mission-critical operations.

- For instance, in October 2025, the U.S. government agency provided a five-year contract to provide multi-band, multi-orbit airborne satellite communication. This solution was procured to enable secure high-bandwidth connectivity globally and support the agency’s critical mission communications across its entire airborne fleet.

MARKET RESTRAINTS:

High Cost of Development and Maintenance to Limit Market Expansion

The market faces restraint due to the high costs associated with the development, deployment, and maintenance of satellite communication infrastructure and equipment. There is a requirement for substantial capital investments and skilled labor to build & maintain earth station infrastructure and specialized satellite terminals. This is expected to limit airborne SATCOM adoption among smaller operators and emerging markets. In addition, the technical complexity of integrating these systems into aircraft and ensuring compliance with rigorous aerospace certifications adds to the overall cost, which hampers the airborne SATCOM market growth.

MARKET OPPORTUNITIES:

Rising UAV Adoption and Advanced Technologies Present Growth Opportunities for Market Growth

The market provides significant growth opportunities, owing to a surge in the adoption of unmanned aerial vehicles (UAVs) for both military and commercial applications. UAV operators demand continuous, reliable satellite connectivity for command, control, surveillance, and data transmission. This is expected to accelerate the need for lightweight, efficient SATCOM terminals. Moreover, the advancements in satellite communication technologies and software for UAV platforms to support high data rates, advanced mobility, and improve communication are expected to drive the growth of the airborne SATCOM industry.

- For instance, in November 2025, ST Engineering iDirect and Black Cat Systems Pty Ltd advanced the satellite communication technology with the launch of the Advanced Satcom Technology Demonstration Lab tailored to the Australian Defence Force (ADF). This initiative includes the development of ST Engineering iDirect’s 450 Software Defined Modem (450SDM), which features multi-waveform, multi-orbit capabilities supporting HEO, GEO, MEO, and LEO orbits.

Such technological advancements in the system, along with integration with AI and IoT, are improving service capabilities and operational efficiency, which is expected to offer lucrative opportunities for the growth of the market.

MARKET CHALLENGES:

Limited Spectrum Availability and Regulatory Constraints Act as a Challenge for Market

Another key market challenge for airborne satellite communication is the limited spectrum availability and regulatory constraints. Satellite communications require access to specific frequency bands, which are heavily regulated and often congested, leading to potential interference and limitations on bandwidth allocation. Coordination across international jurisdictions for frequency use, compliance with evolving electromagnetic compatibility standards, and managing spectrum sharing among multiple users hamper the growth of the market.

AIRBORNE SATCOM MARKET TRENDS:

Integration of Multi-Orbit Satellite Constellations is a Significant Trend in Market

A key trend in the market is the use of multi-orbit satellite constellations combining Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Earth Orbit (GEO) satellites to deliver seamless, resilient, and high-capacity connectivity. This multi-orbit approach improves geographic coverage, lowers latency, and boosts reliability by allowing airborne platforms to dynamically switch between satellites based on availability and mission needs. Therefore, key players in this industry are focusing on developing advanced, multi-orbit satellite communication platforms and solutions that enhance connectivity, security, and operational flexibility.

- For instance, in February 2024, Comtech Telecommunications Corp. launched its new ELEVATE 2.0 multi-orbit SATCOM platform, designed to provide seamless global connectivity by integrating networks across Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Earth Orbit (GEO), and Very High Throughput Satellites (V-HTS) in a single, low Size Weight and Power (SWaP) platform.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Demand for Secure Communication and Increased Aircraft Production Drives Fixed Wing Aircraft Segment Growth

By platform, the market is segmented into fixed wing aircraft, rotary wing aircraft, and UAV. The fixed wing aircraft includes commercial aircraft, business aircraft, general aviation aircraft, and military aircraft. The rotary wing aircraft comprises military helicopters and civil helicopters.

The fixed wing aircraft segment holds the largest Airborne SATCOM market share, and its growth is driven by the need for reliable and secure communication for a large number of commercial and military fixed-wing fleets, and an increase in aircraft production. The demand for the segment grows due to heavy investments from airlines and defense sectors to enhance passenger experience and operational efficiency through advanced SATCOM systems.

UAV is the fastest-growing segment and is projected to grow at the highest CAGR of 13.6%. The factors responsible for segment growth are a rise in demand for continuous command, control, and real-time data exchange in both military and commercial UAV applications. Moreover, defense sectors across the globe are partnering with SATCOM providers for compact, lightweight SATCOM terminals designed specifically for UAVs, which drives segment growth.

- For instance, in April 2025, Gilat Satellite Networks Ltd. announced that its Defense Division secured a contract exceeding USD 11 million from a UAV company for the delivery of DKET 3420 transportable satellite communication terminals designed for mission-critical operations.

By Frequency Band

Balanced Bandwidth, Reliability, and Mature Satellite Coverage Boosts Demand for Ku-Bands

Based on frequency band, the market is segmented into L-Band, Ku-Band, Ka-Band, X-Band, and others.

The Ku-Band segment acquires the largest share in the market, driven by its widespread adoption in commercial and military applications due to its advantages, such as a balance of bandwidth, cost, and reliability. Ku-band systems have dense satellite coverage and mature, advanced technology, which makes them highly reliable for in-flight internet access, voice calls, and video streaming at affordable rates. Moreover, the existing commercial aircraft are already equipped to accommodate Ku-band SATCOM terminals, which allows easy deployment and retrofit, driving segment growth.

The Ka-Band segment is experiencing the fastest growth with a CAGR of around 12.3% owing to increased demand for higher data throughput and bandwidth-intensive applications such as streaming video and cloud access. In addition, the continuous development of technologically advanced Ka-band antennas to support multi-orbit connectivity and uninterrupted mobile communication propels segment growth.

- For instance, in November 2025, Sivers Semiconductors and Doosan partnered to develop scalable electronically steerable array (ESA) panels in the Ka-band for satellite communications.

By Application

Rising Passenger Demand and Airline Partnerships Support In-Flight Connectivity (IFC) & Passenger Broadband Segment Growth

Based on application, the market is segmented into in-flight connectivity (IFC) & passenger broadband, mission communications & C2 (Command and Control), ISR, video & sensor data backhaul, safety services & air traffic management, and others.

In-Flight Connectivity (IFC) & Passenger Broadband segment leads the market as the airline industry is experiencing increased passenger demand for reliable internet access and in-flight entertainment services on commercial and business aircraft. Airlines are partnering with satellite service providers to install Ku-band and Ka-band multi-beam antennas that enable high-speed broadband, video streaming, and cloud applications on long-haul flights. All such factors are anticipated to increase the adoption of satellite communication systems for in-flight connectivity applications.

The ISR, video & sensor data backhaul segment grows with the fastest CAGR of 11.8%. The segment grows at a rapid rate due to increasing investments in ISR-enabled airborne SATCOM solutions to support network-centric warfare and battlefield situational awareness. In addition, the surge in requirements for resilient, compact, and mission-assured multi-frequency and multi-orbit connectivity solutions for the defense sector is expected to drive segment growth in the market during the forecast period.

- For instance, in September 2025, AERKOMM signed a Distribution Partner Agreement with VolitionRF to distribute VolitionRF's advanced Ku/Ka and X/Ka multi-band airborne SATCOM terminals across the Asia Pacific region, targeting defense, aerospace, intelligence surveillance and reconnaissance ISR, and unmanned platforms.

To know how our report can help streamline your business, Speak to Analyst

By Component

Retrofit Programs and Increased Demand for In-Flight Internet Access Drive Terminals Segment Growth

Based on component, the market is segmented into terminals, antennas & radomes, modems & routers, transceivers, power amplifiers, and others.

The terminals segment dominates the market due to the rising demand for in-flight internet access and entertainment in commercial aviation. Terminals are used to translate satellite signals, and they help to enable high-speed broadband and real-time military communication. It is an essential component that allows for secure data transfer and situational awareness. The growing fleet of connectivity-ready new aircraft and retrofit programs in older fleets further propel terminal installations, thus in turn driving the demand for the airborne SATCOM.

The antennas & radomes segment is expected to grow with a CAGR estimated between 11.7%. The segment is growing as the SATCOM systems become advanced, there is an increasing need for high-performance, multi-band antennas integrated with low-loss, aerodynamic radomes. Moreover, the component manufacturers are focused on the development of antennas that enhance connectivity and simplify integration of commercial SATCOM networks on diverse aircraft, which drives component demand, further propelling market growth.

- For instance, in September 2024, Viasat secured a USD 33.6 million U.S. Air Force Research Laboratory DEUCSI contract to develop low‑SWaP active electronically scanned array (AESA) phased‑array antennas that provide resilient, multi-band, multi-orbit, multi-vendor SATCOM links for tactical aircraft, including rotary-wing platforms.

By End Use

High Demand for Advanced In-Flight Connectivity Services Propels Commercial Segment Growth

Based on end use, the market is segmented into commercial and government & defense.

The commercial segment holds the largest market share and is growing with the fastest growth rate due to high demand for in-flight connectivity services such as internet access, streaming, and enhanced passenger experience. Airlines are increasingly equipping new aircraft with SATCOM line-fit solutions and retrofitting older fleets to meet passenger expectations.

- For instance, in January 2025, Etihad Airways announced the extension of its partnership with Viasat to deploy Viasat Amara, a next-generation in-flight connectivity solution, across its entire fleet, including the Airbus A321LR, A350, and Boeing 787 Dreamliner aircraft, enhancing passenger digital experience with high-speed internet for streaming, live TV, and other applications.

The government & defense segment is growing at a steady rate with a CAGR of 9.7%. Military adoption of aircraft satellite communication is supported by defense modernization budgets focused on integrating airborne SATCOM for UAV, fighter aircraft, and helicopters. The segment growth is driven by the need for encrypted, low-latency SATCOM systems capable of transmitting sensor data, video feeds, and operational communications globally.

- For instance, in June 2023, CesiumAstro was awarded a USD 3.6 million contract by the U.S. Air Force AFWERX Tactical Funding Increase (TACFI) program to build, integrate, and demo its satellite communications (SATCOM) terminal aboard the General Atomics MQ-9A Reaper remotely piloted aircraft.

By Installation Type

Aging Fleet Connectivity Upgrades and Regulatory Compliance Stimulate Retrofit Segment Growth

Based on installation type, the market is segmented into line-fit and retrofit/upgrade.

The retrofit/upgrade segment holds the majority share in the market as the operators are increasingly upgrading mid-life and aging aircraft to meet expanding connectivity, regulatory, and security requirements.

- For instance, in May 2024, Collins Aerospace achieved the first retrofit certification and installation of its IRT NX Satellite Communication (SATCOM) system, utilizing the Iridium Certus 700 network, on a Prince Aviation Cessna CitationJet 525.

Moreover, airlines extend aircraft service life by installing passenger broadband and enhanced operational communications through retrofitting, which acts as another driver for the segment growth.

The line-fit segment grows with the fastest growth rate in the industry, with a CAGR of 10.2%. The segment is growing rapidly due to the increasing number of connectivity-ready aircraft being delivered from OEMs in both commercial and military sectors. New aircraft models come pre-installed with integrated SATCOM antennas and terminals, reducing installation complexity and lifecycle costs. Moreover, airlines engage in partnership with SATCOM providers for linefit communication systems for fast, reliable, and seamless in-flight internet access.

- For instance, in November 2025, Neo Space Group (NSG) and Thai Airways partnered to line-fit NSG's advanced Skywaves in-flight connectivity (IFC) solution on all 34 of Thai Airways' Boeing 787 Dreamliner aircraft, offering broadband speeds up to 200 Mbps for high-speed passenger Wi-Fi and improved operational efficiency.

Airborne SATCOM Market Regional Outlook

By region, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Airborne SATCOM Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest share in the market, valued at USD 4.58 billion in 2025, and is expected to grow at a significant CAGR during the forecast period. The market in the region is growing due to strong demand for high-bandwidth in-flight connectivity across commercial airlines and business aviation fleets. Moreover, defense programs in the U.S. are prioritizing resilient, multi-orbit SATCOM architectures to support command-and-control. In addition, countries such as the U.S are constantly investing in the development of advanced antenna systems for enhanced satellite communication on aircraft platforms.

- For instance, in September 2025, the U.S. Air Force Research Laboratory awarded a contract to Cubic Defense for developing its Halo multi-link, multi-band, multi-orbit hybrid SATCOM antenna system, which supports simultaneous transmission and reception across various frequency bands.

In addition, the carriers and airlines are announcing upgrades to next-generation satellite connectivity packages, which are expected to drive demand for satellite communication solutions in the region.

Europe

In Europe, the market is expected to witness steady growth due to a dense network of intra-European air routes and a strong installed base of connectivity on narrowbody and widebody fleets. Moreover, there is a strong regulatory focus on safety services, datalink, and continuous communication with air traffic management authorities, which pushes the use of advanced SATCOM solutions. In addition, the development and deployment of satellite systems through various programs to provide secure and autonomous satellite communications for the defense sector drives market growth.

- For instance, in November 2025, Germany’s Bundeswehr awarded Airbus a USD 2.43 billion contract for the SATCOMBw 3 program to develop next-generation secure military geostationary satellites and ground systems.

Such satellite deployment enhances airborne SATCOM by providing an improved, secure, and resilient communication infrastructure that airborne platforms depend on for global, beyond-line-of-sight connectivity.

Asia Pacific

The Asia Pacific market is experiencing rapid growth driven by rapid passenger traffic expansion, large order backlogs for narrowbody aircraft, and increasing adoption of in-flight connectivity. Therefore, India’s expanding chemical industry and regulatory focus on workplace safety drive product demand during the forecast period. Moreover, rising defense and homeland security budgets in countries such as China, India, Japan, and South Korea in the region are accelerating the deployment of SATCOM-enabled ISR, maritime patrol, and special-mission aircraft. In addition, airlines and carriers are integrating in-flight connectivity systems in their aircraft fleet to enhance the overall flight experience and meet growing passenger demand for continuous connectivity.

- For instance, in May 2022, China Southern Airlines contracted with Airbus to install an advanced HBCplus in-flight connectivity system in its 30 A350 aircraft.

Such developments highlight increased demand for high-capacity, reliable connectivity solutions in commercial aviation, which is expected to propel the growth of the market in the region during the forecast period.

Latin America

The Latin America market is driven by increasing air traffic and a growing commercial aviation sector, which boosts the demand for advanced in-flight connectivity and entertainment services. Moreover, the government initiatives aimed at improving regional air infrastructure and expanding remote connectivity solutions also support market growth.

Middle East & Africa

In the Middle East & Africa, the market growth is fueled by large infrastructure projects, including smart city developments and expanded airport capacities, particularly in Gulf Cooperation Council (GCC) countries. These projects demand robust satellite communication solutions to manage urban air traffic, public safety, and city management efficiently. In addition, the Saudi Arabian market is projected to grow rapidly, driven by increased demand for high-throughput satellite links in commercial aviation, defense UAV reconnaissance, and government communications.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Innovation, Adoption of Advanced Materials, and Protective Technologies Drive Competitive Dynamics in Market

The airborne SATCOM market is characterized by a mixture of leading multinational defense and aerospace companies, including Airbus, Lockheed Martin, Northrop Grumman, Thales Group, and Raytheon Technologies. These firms offer strong and extensive portfolios, including satellite communication systems, antennas, modems, and integrated platforms. Moreover, these companies use R&D, global supply chains, and strategic partnerships to gain a competitive advantage in the market.

In addition, to strengthen their market position, key players are investing heavily in technological innovation, including the development of multi-orbit capable systems, software-defined radios, and enhanced security features. They are also forming alliances with satellite operators, defense agencies, and technology firms to co-develop next-generation solutions optimized for advanced military, government, and commercial applications.

LIST OF KEY AIRBORNE SATCOM COMPANIES PROFILED:

- Thales Group (France)

- Collins Aerospace (U.S.)

- Honeywell International Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- Viasat, Inc. (U.S.)

- Israel Aerospace Industries (Israel)

- L3Harris Technologies, Inc. (U.S.)

- Gilat Satellite Networks (Israel)

- Orbit Communication Systems Ltd. (Israel)

- Inmarsat plc (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Gogo Inc. announced at the Dubai Airshow that Action Aviation became the first Middle Eastern operator to equip its Boeing Business Jet BBJ 737 with the Gogo Galileo FDX connectivity terminal. This full-duplex, electronically steered antenna system offers high-speed, low-latency global connectivity.

- September 2025: Gilat Satellite Networks Ltd. received orders exceeding USD 7 million to supply additional DKET 3421 transportable SATCOM terminals and associated support services to the U.S. Army.

- May 2025: Honeywell’s JetWave X satellite communication system was selected by L3Harris to upgrade the U.S. Army’s Airborne Reconnaissance and Electronic Warfare System (ARES), providing high-speed, resilient global connectivity for mission-critical data transmission

- April 2025: Air Canada announced that it had become the first commercial airline to launch Eutelsat OneWeb’s LEO-powered in-flight Wi-Fi service, delivering high-speed, low-latency connectivity to passengers.

- January 2024: Viasat contracted with Lufthansa Group to equip more than 150 additional aircraft across Lufthansa, SWISS, and Austrian Airlines with the European Aviation Network (EAN) in-flight connectivity solution.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the airborne SATCOM market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. The market report includes Porter's five forces analysis, which illustrates the potency of buyers and suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform, By Frequency Band, By Application, By Component, By End Use, By Installation Type, and Region |

|

By Platform |

|

|

By Frequency Band |

|

|

By Application |

|

|

By Component |

|

|

By End Use |

|

|

By Installation Type |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 13.40 billion in 2025 and is projected to reach USD 32.98 billion by 2034.

In 2025, the market value stood at USD 4.58 billion.

The market is growing at a CAGR of 10.5% during the forecast period of 2026-2034.

The fixed wing aircraft segment leads the market by platform.

The key factors driving the market are the demand for reliable, high-speed in-flight connectivity and communication.

Thales Group (France), Collins Aerospace (U.S.), Honeywell International Inc. (U.S.), and General Dynamics (U.S.) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us