Aircraft Door Market Size, Share & Industry Analysis, By Aircraft Type (Fixed-Wing (Narrow Body, Wide Body, Regional Jets, Business Jets, and Military Aircraft), Rotary-Wing (Commercial Helicopter and Military Helicopter), By End-user (OEM and MRO), By Door Type (Passenger Doors, Cargo Drones, Emergency Exit Doors, Service/access Doors, and Landing Gear Doors), By Mechanism (Plug Type doors, Non-plug type doors, Power-Operated Doors, and Manual-Operated Doors), By Material (Aluminum Alloys, Composite Materials, Titanium, and Steel), By Component, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

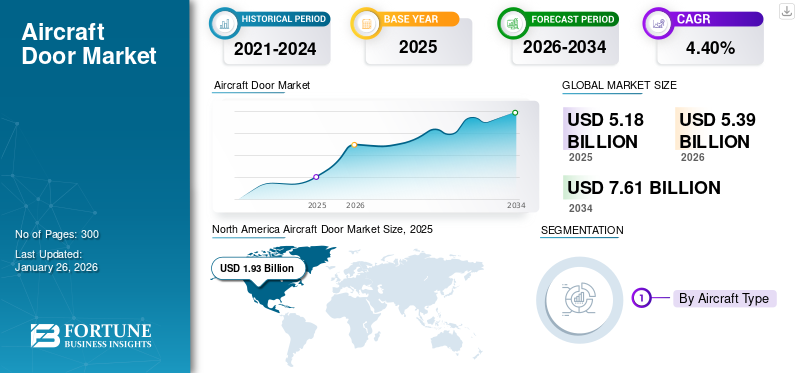

The global aircraft door market size was valued at USD 5.18 Billion in 2025. The market is projected to grow from USD 5.39 Billion in 2026 to USD 7.61 Billion by 2034, exhibiting a compound annual growth rate CAGR of 4.40% during the forecast period. North America dominated the global market with a share of 37.32% in 2025.

The aircraft door market encompasses the design, manufacture, and integration of passenger, cargo, service, emergency exits, and landing gear doors that provide both structural integrity and critical access functionalities in commercial, business, and military aircraft. These doors are engineered to withstand pressurization, aerodynamic loads, and extreme environmental conditions, forming an essential part of the airframe’s safety and performance system. The market’s expansion is being propelled by several converging factors — primarily the sharp rise in aircraft production rates driven by the resurgence in global air travel, fleet modernization programs, and increased deliveries of next-generation aircraft such as the Airbus A320neo, Boeing 737 MAX, and A350 families. A sustained shift toward lightweight and corrosion-resistant materials, especially advanced composites and titanium alloys, enables manufacturers to reduce overall airframe weight while improving lifecycle durability. Additionally, technological integration of smart actuators, electromechanical locks, and health-monitoring sensors transforms doors from static components into active safety systems, aligned with digital maintenance ecosystems.

Growth is further underpinned by defense procurement cycles emphasizing multi-role and transport aircraft and rising helicopter production for emergency medical, offshore, and law enforcement applications. Aftermarket demand remains strong, fueled by continuous maintenance, repair, and overhaul (MRO) activities across aging fleets. However, supply chain constraints in forged metal and composite subcomponents, coupled with certification complexities, remain challenges to scalability.

Leading participants in this market include Safran Cabin, Triumph Group, Latecoere, Spirit AeroSystems, Elbit Systems, Collins Aerospace (Raytheon Technologies), Mitsubishi Heavy Industries, and Aerosud. These players focus on collaborative design partnerships with OEMs and tier-1 integrators, developing lightweight, modular, and power-operated door systems optimized for next-generation airframes. Collectively, the aircraft doors market is evolving toward higher integration, automation, and sustainability — reflecting a strategic pivot in aero-structure manufacturing philosophy globally.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Aircraft Production and Fleet Modernization Fuels the Market Growth

A key driver for the aircraft door market is the rapid expansion in global aircraft production and fleet modernization efforts across both commercial and defense sectors. OEMs such as Airbus and Boeing are steadily increasing output to meet record backlogs, particularly for narrow-body aircraft, which dominate new orders globally. The ongoing replacement of aging fleets with more fuel-efficient and lightweight models has intensified the demand for advanced composite door systems offering enhanced performance and reduced maintenance. Moreover, defense modernization programs in North America, Europe, and Asia propel demand for specialized access and cargo doors in multi-mission and transport aircraft. This production surge is generating parallel growth opportunities across tier-1 aero-structure suppliers.

- July 2025: Airbus announced a production ramp-up plan for the A320neo family to 75 aircraft per month by 2026, underscoring increasing component demand across aero-structure systems, including doors.

MARKET RESTRAINTS

Supply Chain Constraints and Certification Delays to Restrain Growth

The aircraft door market faces persistent challenges from supply chain bottlenecks and complex certification cycles that delay program deliveries. The reliance on specialized materials such as titanium, aluminum forgings, and composite panels exposes manufacturers to global raw material supply volatility. Additionally, stringent regulatory testing and airworthiness certification add extended lead times, especially when integrating new materials or automated actuation systems. Smaller suppliers struggle to align with OEM schedule accelerations, leading to component shortages and project cost overruns. These constraints restrict scalability despite high-order backlogs.

- May 2025: Spirit AeroSystems reported production disruptions due to material shortages and delayed component validation, prompting temporary output reductions in key aerostructure programs, including door assemblies.

MARKET OPPORTUNITIES

Integration of Smart and Lightweight Door Systems Will Lead to Innovative Opportunities

The ongoing shift toward intelligent and lightweight door architectures presents significant opportunities for innovation. Aircraft OEMs prioritize smart door systems equipped with embedded sensors, automated latching, and predictive health-monitoring features that enhance operational safety and reduce unscheduled maintenance. The adoption of composite and hybrid-material designs enables weight reduction without compromising structural performance, directly supporting sustainability targets. As electric and hybrid aircraft platforms emerge, lightweight and modular door systems optimized for lower-pressure environments will gain traction. Partnerships between aero-structure specialists and avionics suppliers are driving this technological convergence.

- March 2025: Collins Aerospace unveiled a prototype smart passenger door with integrated sensors and electric actuation for future commercial aircraft and jets, enabling digital health tracking and reduced maintenance cycles.

AIRCRAFT DOOR MARKET TRENDS

Composites and Advanced Manufacturing in Door Assembly Leads to New Market Trends

A prominent technological trend shaping the aircraft door market is the application of advanced composite manufacturing and digital engineering techniques. The transition from conventional aluminum alloys to carbon-fiber-reinforced composites allows for substantial weight savings, corrosion resistance, and improved fatigue performance. Additive manufacturing and automated fiber placement (AFP) are enabling precision in structural door skins and hinge mechanisms. Digital twin and model-based design tools further reduce development cycles while improving certification efficiency. These innovations collectively enhance structural integrity and reduce total lifecycle costs.

- June 2025: Latecoere announced the expansion of its carbon composite door manufacturing facility in Toulouse, integrating robotic AFP systems to support next-generation Airbus and Dassault programs.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Balancing Weight Optimization with Structural Safety Can Overcome Several Challenges

One of the primary challenges for aircraft door manufacturers lies in maintaining structural safety while aggressively pursuing weight reduction. Doors are among the most critical pressure-bearing components in an airframe, and any failure can be catastrophic. Achieving compliance with stringent airworthiness standards while using thinner composite laminates or hybrid materials requires precise engineering and repeated testing, which increases cost and complexity. Additionally, integrating power-operated systems adds mechanical and electronic interfaces that must perform reliably under varying environmental and pressure conditions. Balancing innovation with proven safety margins remains a core technical challenge for Tier-1 suppliers.

- February 2025: The European Union Aviation Safety Agency (EASA) updated its certification guidelines for composite pressure doors, emphasizing enhanced fatigue and deformation testing protocols for next-generation aircraft designs.

Segmentation Analysis

By Aircraft Type

Increasing Narrow-Body Aircraft Production Will Drive the Fixed-Wing Segment

On the basis of aircraft type, the market is classified into fixed-wing and rotary-wing.

The fixed-wing segment, particularly narrow-body aircraft, will lead the aircraft door market growth as OEMs ramp up production to meet surging short-haul demand, with a expected share of 85.20% in 2026. Airlines favor high-frequency, fuel-efficient jets for domestic and regional operations, translating into higher door system installations. Aircraft such as the A320neo and 737 MAX require multiple precision-engineered door units per fuselage, ensuring consistent supply chain demand.

- July 2025: Airbus confirmed a 300-aircraft order from IndiGo for A321neo models, triggering increased component procurement for passenger and service doors.

By End-User

Rising Aircraft Production Strengthens OEM End-User Segment

On the basis of end-user, the market is bifurcated into OEM and MRO.

OEMs will remain the leading end-user segment as rising aircraft production rates drive line-fit installation of door systems, with a expected share of 74.64% globally in 2026. Long-term procurement contracts between airframes and Tier-1 suppliers ensure stable OEM demand, while MRO activity grows slower. Increasing automation in assembly and advanced composite integration further strengthens OEM dependence on high-quality door suppliers.

- August 2025: Safran Cabin renewed its multi-year contract with Airbus to supply door modules for A320 and A350 aircraft programs.

By Door Type

Surge in Commercial Deliveries Will Drive Growth of the Passenger Doors Segment

On the basis of door type, the market is classified into passenger doors, cargo doors, emergency exit doors, service/access doors, and landing gear doors.

The passenger doors segment will grow strongly as global aircraft deliveries accelerate, particularly for single-aisle commercial jets, expected for 36.96% market share in 2026. Each new aircraft requires multiple high-safety passenger doors, making this category critical to OEM assembly lines. Increasing airline fleet renewals, rising passenger traffic, and stricter safety requirements are leading to the adoption of lighter, pressure-resistant door systems. Integration of smart locking and health-monitoring features further boosts demand.

- April 2025: Airbus delivered its 2,500th A321neo featuring next-generation composite passenger doors with integrated sensor monitoring systems.

By Mechanism

Rising Safety Demands Will Propel Plug-Type Doors Segment Expansion

Based on the mechanism, the aircraft doors market is segmented into plug-type doors, non-plug-type doors, power-operated doors, and manual-operated doors.

Plug-type doors account for the largest segment because of their proven ability to withstand high cabin pressure differentials and provide enhanced safety, with a expected share of 49.12% in 2026. These doors are self-sealing under pressure, making them ideal for commercial jetliners and regional aircraft. OEMs are focusing on optimizing plug-door aerodynamics and maintenance simplicity. Their adoption continues to rise as next-gen narrow-body platforms demand higher structural performance and automated systems.

- February 2025: Boeing announced the introduction of a lightweight plug-type door assembly in its 737 MAX series, improving pressurization safety and reducing door maintenance intervals.

To know how our report can help streamline your business, Speak to Analyst

By Materiala

Advancements in Aluminum Alloys Will Sustain Growth of the Aluminum Doors Segment

Based on the material, the aircraft door market is segmented into aluminum alloys, composite materials, titanium, and steel.

Aluminum alloys will continue to dominate the aircraft door market share as manufacturers rely on their durability, fatigue resistance, and cost-effectiveness. Despite the rise of composites, aluminum remains the preferred choice for most airframes due to its proven performance in pressure-bearing structures. Advancements in heat-treated alloys and precision machining enhance its strength-to-weight efficiency, ensuring longevity in OEM contracts.

- May 2025: Spirit Aero Systems expanded its aluminum door panel manufacturing capacity in Wichita, supporting new Boeing 737 MAX and 787 production lines.

By Component

Adoption of Composite Structures Will Accelerate Growth of the Structural Panels/Skins Segment

Based on the component, the aircraft door market is segmented into hinge arms, latches, handles, girt, seals, structural panels/skins, actuation systems, and others.

Structural panels/skins will dominate door component demand as manufacturers shift to carbon-fiber composites for reduced weight and superior fatigue performance. These panels form the aerodynamic and pressurized core of door assemblies. Automation, such as automated fiber placement (AFP) and additive manufacturing, enhances structural precision and production speed, thus meeting stringent certification norms.

- March 2025: Latecoere inaugurated an automated composite door-skin facility in Toulouse to support Airbus A350 and Dassault Falcon aircraft programs.

Aircraft Door Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Aircraft Door Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 1.93 billion in 2025, representing 37.32% of the global market landscape, and is expected to reach USD 2.01 billion in 2026. North America will continue leading the aircraft door market due to its deep aerospace industry manufacturing base and established OEM networks. Boeing, Spirit Aero-Systems, and Collins Aerospace dominate production, while U.S. defense programs sustain specialized door demand. The region’s emphasis on automation and additive manufacturing supports scalability. The U.S. market is projected to reach USD 1.8 billion by 2026.

- June 2025: Boeing expanded its Wichita facility to increase the output of composite door structures for 737 MAX and 777X models.

Europe

Europe contributed 27.76% to the global market in 2025, with a valuation of USD 1.44 billion, and is projected to reach USD 1.5 billion in 2026. Europe’s dominance in engineering precision and composite design will drive steady expansion in aircraft door production. Airbus, Latecoere, and Stelia Aerospace leverage advanced materials and robotics for door assembly optimization. Rising A320 and A350 production volumes across European facilities further support demand. The UK market is projected to reach USD 0.29 billion by 2026, and the Germany market is projected to reach USD 0.59 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 1.03 billion in 2025, representing 19.89% of the global market share, and is projected to reach USD 1.08 billion in 2026. Asia-Pacific will record the fastest growth due to rapid airline expansion, surging air travel, and localized aircraft manufacturing in China and India. Indigenous programs such as COMAC’s C919 and regional assembly hubs boost component demand. Domestic suppliers are increasingly collaborating with OEMs for aero structure integration. The Japan market is projected to reach USD 0.23 billion by 2026, the China market is projected to reach USD 0.43 billion by 2026, and the India market is projected to reach USD 0.21 billion by 2026.

Middle East & Africa

In 2025, Middle East & Africa held 10.15% of the global market, reaching a valuation of USD 0.53 billion, and is projected to grow to USD 0.55 billion in 2026. The Middle East & Africa region will experience sustained growth driven by defense aircraft procurement and strengthening MRO capabilities. Investments from the UAE and Saudi Arabia in localized manufacturing are building long-term component supply chains. Rising demand for military transport and surveillance aircraft further adds to door assembly requirements.

Latin America

Latin America contributed approximately USD 0.25 billion to the global market in 2025, accounting for 4.88% share, and is expected to reach USD 0.25 billion in 2026. Latin America will experience gradual market growth, supported by new regional jet deliveries and modernization initiatives. Embraer’s E2-series programs continue to anchor OEM demand, while rising air-cargo conversions contribute to aftermarket door replacements. The focus on operational efficiency is accelerating the use of lightweight door systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and OEM Partnerships Will Shape the Competitive Landscape

The aircraft doors market is characterized by strong consolidation among Tier-1 Aerostructures manufacturers, where partnerships and long-term OEM contracts determine competitive advantage. Major players such as Safran Cabin, Latecoere, Triumph Group, Collins Aerospace, Spirit Aero Systems, Elbit Systems, and Mitsubishi Heavy Industries dominate through specialized engineering capabilities and proprietary composite technologies. The industry is shifting toward collaborative development with airframes like Airbus, Boeing, Embraer, and many other key players to co-design lightweight, modular, and digitally monitored door systems. Emerging suppliers in Asia are also entering the ecosystem through offset manufacturing and local assembly programs. Strategic acquisitions and production automation are further intensifying competition, emphasizing supply chain resilience and cost optimization as key differentiators.

- June 2025: Safran Cabin announced a joint program with Airbus to develop hybrid-material passenger and service doors for the next-generation A320 family, reinforcing its leadership in high-integration aerostructures systems.

LIST OF KEY AIRCRAFT DOOR COMPANIES PROFILED

- Safran Cabin (France)

- Latecoere (France)

- Collins Aerospace (Raytheon Technologies) (U.S.)

- Spirit AeroSystems (U.S.)

- Triumph Group (U.S.)

- Elbit Systems (Israel)

- Mitsubishi Heavy Industries (Japan)

- GKN Aerospace (U.K.)

- Airbus Aerostructures (Germany)

- Saab AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- October 2025 – EASA released updated certification guidelines for composite pressure doors, introducing new fatigue-testing and deformation-limit standards. The revision is expected to drive additional R&D in hybrid-material door systems to meet stricter airworthiness criteria for next-generation aircraft.

- August 2025 – Safran Cabin renewed its multi-year contract with Airbus to supply passenger and service door modules for the A320 and A350 programs. The agreement strengthens Safran’s position as a primary integrator of high-integration aerostructure systems within Europe.

- July 2025 – Airbus secured a 300-aircraft order from IndiGo for A321neo jets, directly boosting demand for door assemblies and related aerostructure components. The large order will sustain OEM supply chains and elevate Tier-1 supplier utilization over the next decade.

- May 2025 – Spirit AeroSystems expanded its aluminum door panel machining capacity in Wichita, Kansas, to support Boeing 737 MAX and 787 programs. The investment improves throughput and supports rising OEM production rates amid record single-aisle aircraft demand.

- April 2025 – Airbus delivered its 2,500th A321neo equipped with next-generation passenger doors featuring integrated sensor systems and composite construction. The milestone reflects Airbus’s focus on lighter, digitally monitored aerostructure assemblies for higher efficiency and safety compliance.

- March 2025 – Latecoere inaugurated a new automated composite door-skin facility in Toulouse to support Airbus A350 and Dassault Falcon programs. The expansion enhances production precision and scalability, advancing Latecoere’s leadership in composite aerostructure components.

- February 2025 – Boeing introduced a redesigned plug-type door assembly for its 737 MAX series, featuring lightweight actuators and enhanced pressure-sealing. The upgrade aims to improve operational safety, reduce maintenance downtime, and standardize door architecture across future narrow-body platforms.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.40% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Region |

|

By Aircraft Type |

· Fixed-Wing o Narrow Body o Wide Body o Regional Jets o Business Jets o Military Aircraft · Rotary-Wing o Commercial Helicopter o Military Helicopter |

|

By End-User |

· OEM · MRO |

|

By Door Type |

· Passenger Doors · Cargo Drones · Emergency Exit Doors · Service/access Doors · Landing Gear Doors |

|

By Mechanism |

· Plug Type doors · Non-plug type doors · Power-Operated Doors · Manual-Operated Doors |

|

By Material |

· Aluminum Alloys · Composite Materials · Titanium · Steel |

|

By Component |

· Hinge arms · Latches · Handles · Girt · Seals · Structural panels/skins · Actuation systems · Others |

|

By region |

· North America (By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Country) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Country) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Russia (By Aircraft Type) o Rest of Europe (By Aircraft Type ) · Asia Pacific (By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Country) o China (By Aircraft Type ) o India (By Aircraft Type ) o Japan (By Aircraft Type ) o Australia (By Aircraft Type ) o Rest of Asia Pacific (By Aircraft Type ) · Middle East & Africa (By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Country) o UAE (By Aircraft Type ) o Saudi Arabia (By Aircraft Type ) o Qatar (By Aircraft Type ) o Rest of Middle East and Africa (By Aircraft Type ) · Latin America (By Aircraft Type, End-User, Door Type, Mechanism, Material, Component, and Country) o Brazil (By Aircraft Type ) o Argentina (By Aircraft Type ) o Rest of Latin America (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.18 billion in 2025 and is projected to reach USD 7.61 billion by 2034.

In 2025, the market value stood at USD 1.87 billion.

The market is expected to exhibit a CAGR of 4.40% during the forecast period of 2026-2034.

The fixed-wing segment led the market by aircraft type.

Rising aircraft production and fleet modernization are the key factors driving the market growth.

Safran Cabin (France), Latecoere (France), and Collins Aerospace (Raytheon Technologies) (United States) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 300

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us