Aircraft Engine and Component Leasing Market Size, Share & Industry Analysis, By Lease Asset Type (Engine Leasing and Component Leasing), By Leasing Type (Dry Lease, Wet Leasing, Operating Leases, Finance Leases, and Sale and Leaseback), By Engine Type (Turboprop, Turbofan, and Others), By Aircraft Type (Narrowbody, Widebody, Regional, and Others), By End User (Commercial Airlines, Military Aviation, and General Aviation), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

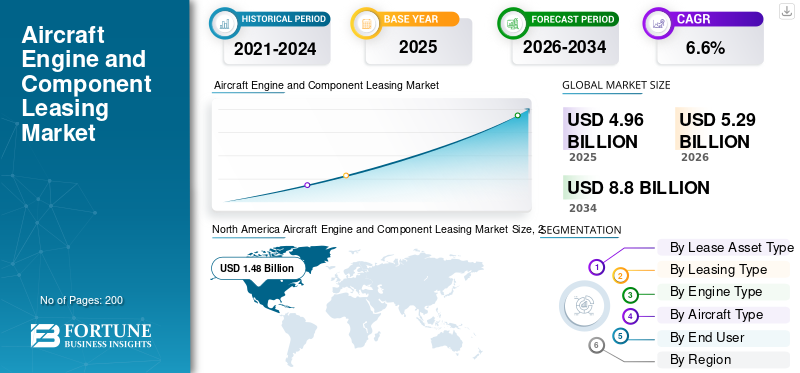

The global aircraft engine and component leasing market size was valued at USD 4.96 billion in 2025. The market is projected to grow from USD 5.29 billion in 2026 to USD 8.80 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. North America dominated the global aircraft engine and component leasing market with a market share of 29.83% in 2025.

The aircraft engine and component leasing market includes renting spare engines and valuable aircraft components to airlines and MROs for a set period. This helps keep aircraft flying while their engines are being serviced or parts are being repaired. Demand is rising due to high fleet usage, longer and less predictable shop-visit timelines, and the need for operators to avoid securing up cash in owned spares. Leasing provides a faster and more flexible way to ensure reliable dispatch.

Key players include engine lessors, aftermarket leasing platforms, and component pool operators. On the engine side, Willis Lease continues to grow its globally deployed engine portfolio under operating lease agreements. FTAI Aviation is also prompting the market toward exchange and availability models. For example, it has implemented its Perpetual Power Program agreements and developed a broader CFM56 ecosystem, supported by partnerships that increase the supply of serviceable materials in the aftermarket.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Unplanned Engine Removals and Long Shop Queues Drive Leasing Demand for Spare Capacity

When engines are taken off-wing earlier than expected or stay in the shop longer than airlines can manage, as operators cannot afford to wait, they need spare engines and ready-to-swap parts to keep aircraft flying and schedules on track. This is where leasing helps. It is faster than buying, avoids tying up capital in spare parts for emergencies, and allows airlines to handle disruptions such as AOG spikes, parts shortages, and overloaded maintenance slots without permanently increasing their inventory. This is fueling the aircraft engine and component leasing market growth.

In September 2023, RTX shared a fleet management plan for PW1100G-JM GTF engines (A320neo) related to a powder-metal issue. They estimated about 600 to 700 additional engine removals and shop visits between 2023 and 2026. They warned that this situation would result in more aircraft being on the ground. This type of event drives airlines toward leasing spare engines and pooling components to maintain their operations.

MARKET RESTRAINTS

Shortage of Leaseable Spare Engines and Certified Parts Restrains Market Expansion

Leasing demand exists, but the market cannot grow smoothly due to the limited physical supply of spare engines and serviceable parts. However, OEM delivery delays, longer shop turnaround times, and airlines extending current leases instead of returning assets can keep engines in fleets, reducing the number of available lease options. The results are higher lease rates, longer contract commitments, and fewer spare options. As a result, the market is sometimes limited not by the willingness to lease but by the availability to lease at a price that operators can afford.

In December 2024, IATA reported that supply chain issues were still expected to extend into 2025, with approximately 14% of the global fleet (around 5,000 aircraft) parked, including roughly 700 aircraft awaiting engine inspections. They noted that narrowbody leasing rates were about 20 to 30% higher than in 2019 as airlines scrambled for capacity, effectively limiting growth despite strong demand.

MARKET OPPORTUNITIES

Growing Used Serviceable Material Pipeline Creates a Big Opportunity to Scale Engine and Component Leasing

One of the best growth opportunities in this market is building larger, cheaper, and faster spare pools by using Used Serviceable Material (USM) and modular repairs, rather than relying solely on new OEM parts. When the USM supply is organized at scale through teardown, repair, certified inventory, and rapid exchange, lessors and pool providers can offer airlines shorter lead times and more predictable availability, often at lower total costs. This approach expands leasing beyond just emergency AOG coverage into routine operations for more carriers.

In March 2025, AAR and FTAI Aviation renewed their exclusive agreement for serviceable engine products until 2030. They focused on increasing the availability of CFM56 USM in the global aviation aftermarket and supporting FTAI’s Module Factory model for modular repair and refurbishment. This directly improves the parts and engine supply foundation that supports larger leasing and exchange pools.

MARKET CHALLENGES

Parts Provenance and Paperwork Integrity are Becoming Hardest Bottleneck for Leasing and Pooling

Engine and component leasing only works when every asset includes a clear, verifiable life status and traceability. An engine part that appears to be in good condition but has questionable paperwork remains unusable. As the market relies more on USM, exchanges, and global pool rotations, the risk associated with documentation increases. Mismatched serial numbers, gaps in back-to-birth traceability, and disputes over return conditions can slow down transactions or lead to failed deals. The impact is significant and operational. There are more inspections, increased audit work, stricter acceptance criteria, and longer induction times.

In August 2023, EASA issued a Suspected Unapproved Parts notification regarding AOG Technics and multiple CFM56 engine parts. The UK CAA published Safety Notice SN-2023/004, warning that many suspect unapproved engine parts were supplied with false release certificates (EASA Form 1 / FAA 8130). This led to widespread checks among operators and MROs and tightened parts acceptance processes.

Impact of Russia Russia-Ukraine War

Sanctions and Asset Stranding Changed the Risk Landscape for Engine and Component Leasing

The Russia-Ukraine war disrupted not just one country's aviation market, but it changed the risk model for engine and component leasing around the world. Sanctions cut off Russian operators, making it nearly impossible to recover many leased assets. As a result, lessors and financiers began to view geopolitical enforceability as a major concern, rather than just fine print. This shift led to tighter contract terms, more aggressive sanctions and diversion clauses, stricter KYC and end-use checks, and a higher risk premium in pricing and insurance expectations. This was particularly true for assets that can be moved, re-registered, or quickly re-exported, such as engines and rotables.

- In March 2022, the European Commission’s aviation sanctions FAQs explained how EU sanctions under Regulation (EU) 833/2014 impacted aircraft and engine leasing, as well as related services. It also discussed the limited options for navigating the restrictions, such as return flights and exceptions, which is why leasing in Russia quickly became very difficult.

AIRCRAFT ENGINE AND COMPONENT LEASING MARKET TRENDS

"Exchange and Pooling" Models Are Replacing Simple Rentals as Lessors Integrate Repair, Teardown, and Inventory to Guarantee Availability

The trend in engine and component leasing is the shift from offering an engine for a set number of months to programs focused on availability. In these models, the provider manages the whole process, including engine teardown, certified inventory, modular repair, and quick access to exchanges or pools. Airlines prefer this approach as it simplifies complex operational risks, such as aircraft on ground (AOG) situations, missing parts, and uncertain shop dates. With this model, you pay for uptime and predictability. For lessors and pool operators, vertical integration is important.

Download Free sample to learn more about this report.

Segmentation Analysis

By Lease Asset Type

Engine Leasing Dominates Market Due to High Asset Value and MRO Shop-Visit Bottlenecks

In terms of lease asset type, the market is categorized into engine leasing and component leasing.

Engine leasing currently dominates the market, as engines are the most crucial asset and the most expensive component on the list. Engines are also the hardest to replace when something goes wrong. As market conditions tighten, such as longer Maintenance, Repair, and Overhaul (MRO) queues, parts shortages, or unexpected removals, airlines in Asia Pacific and North America turn to engine leasing. It is the quickest way to protect schedules and manage operating costs without grounding aircraft. Component leasing matters, but engines generate a larger share of leasing revenue as the stakes are higher and the impact of not having a spare engine is immediate.

In December 2024, the International Air Transport Association (IATA) reported that approximately 14% of the global fleet, or around 5,000 aircraft, were grounded, including about 700 aircraft parked for engine inspections. They warned that this situation is expected to continue into 2025. This situation shows how engine-related challenges can limit available capacity and increase the demand for leased spare engines.

The component leasing segment is expected to show the fastest growth at a CAGR of 7.7% over the forecast period.

By Leasing Type

Operating Leases Dominate Market as They Offer Flexibility in Unpredictable MRO Cycles and Require Less Upfront Capital

On the basis of leasing type, the market is classified into dry lease, wet leasing, operating leases, finance leases, and sale and leaseback.

In the aircraft engine and component leasing market, the operating leases segment dominates the market, as airlines prefer these leases. This preference stems from the need for maximum flexibility as maintenance schedules are subject to change. If an engine shop visit takes longer than expected or a narrow-body aircraft fleet needs rapid coverage, an operating lease allows an operator to bridge the gap without incurring ownership risks or tying up cash needed for operating expenses, route changes, or fleet upgrades driven by fuel efficiency goals. For lessors, operating leases also help scale the business.

The sale and leaseback segment is expected to show the fastest growth at a CAGR of 8.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Engine Type

Turbofan Engines Led Market Due to Narrowbody-Led Fleet Modernization and Fuel-Efficiency Pressure

Based on engine type, the market is segmented into turboprop, turbofan, and others.

The turbofan segment dominated the aircraft engine and component leasing market share in 2025. In the aviation industry, the most common aircraft types are narrowbody planes for low-cost carriers and widebodies for long-haul flights. Both are mainly powered by turbofans. Consequently, most demand for engine leasing and component pooling focuses on this area. As international air travel continues to grow and airlines look to cut operating costs with new, more fuel-efficient jets, turbofan fleets are capturing a larger share of flying hours, especially in Asia Pacific and North America. This growth results in more maintenance visits and greater demand for leased spare parts when market conditions become tighter.

In June 2023, Air India signed purchase agreements for 470 Airbus and Boeing aircraft, including significant numbers of A320neo/A321neo and 737 MAX narrowbodies, and A350/787/777X widebodies. All these are turbofan aircraft, demonstrating that fleet growth and modernization primarily occur through turbofan models. This trend also increases the need for leasing and aftermarket support.

Turboprop is the second-fastest-growing segment in the market, with a CAGR of 4.7% over the forecast period.

By Aircraft Type

Narrowbody Aircraft Lead Market as They Have Large Global Fleets and are Used Frequently

Based on aircraft type, the market is segmented into narrowbody, widebody, regional, and others.

Narrowbody aircraft dominate the market as they are the most common type in the global fleet and are widely used. This combination drives the need for engine leasing and component sharing. There are more cycles, more removals, more scheduled and unscheduled events, and more pressure on maintenance, repair, and overhaul (MRO) capacity. In the current market, airlines, especially low-cost carriers in the Asia Pacific and those with extensive networks in North America, utilize leasing to keep planes in the air without tying up capital. They also focus on updating their fleets for better fuel efficiency and lower operating costs. While widebodies are crucial for long-haul and international flights, narrowbodies excel in scale and daily use, giving them a larger share of the leasing market.

In July 2024, Boeing’s Commercial Market Outlook reported that single-aisle (narrowbody) planes will make up 76% of commercial deliveries through 2043 and will account for 71% of the fleet by that year. This explains why narrowbodies dominate the leasing market, given their role in global aircraft growth and replacement.

The regional segment is expected to show the second-fastest market growth at a CAGR of 6.2% across the forecast period.

By End User

Commercial Airlines Lead Market Due to High Flight Usage and a Tight MRO Market

The market is segmented by end user into commercial airlines, military aviation, and general aviation.

Commercial airlines are central to daily operations in the aviation industry. They fly the most hours and operate the largest share of global aircraft, particularly narrowbody planes for short-haul and low-cost carrier networks. They also manage wide-body aircraft for long-haul international travel. Airlines feel the impact immediately when maintenance, repair, and overhaul capacity or parts availability is limited. When engines or parts are not available on time, airlines cannot pause their schedules. Instead, they depend on engine leasing and component pools to ensure reliable dispatch, manage operating costs, and keep fleet plans on track, including upgrades for better fuel efficiency. This resulted in commercial aviation dominating the market.

In January 2025, IATA reported that global passenger demand hit a record high in 2024. Traffic rose 10.4% year-over-year, with a load factor of 83.5%. This highlights the crucial role commercial airlines play in driving leasing activity.

The general aviation segment is expected to exhibit the second-fastest growth, with a CAGR of 4.2% across the forecast period.

Aircraft Engine and Component Leasing Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Rest of the World (Middle East & Africa and Latin America).

North America Leads Market as It Has the World’s Largest Domestic Air Transport Base and Makes Significant Use of Heavy Narrowbody Aircraft

North America

North America Aircraft Engine and Component Leasing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the leasing market in aviation. It has the highest volume of air transport and operates many narrow-body aircraft, which are the reliable workhorses of the industry. The U.S. leads the market in the North America region as airlines face ongoing pressure to keep their aircraft in the air while controlling operating costs. If maintenance slots get tight or an engine repair takes longer than expected, airlines can't afford extended downtimes. The region also benefits from a strong aviation finance system and a push for modernizing fleets, given that fuel efficiency is crucial with high utilization. As a result, North America consistently accounts for a significant share of leasing activity.

In August 2025, the International Air Transport Association (IATA) published its World Air Transport Statistics (WATS) 2024 update. It confirmed that the U.S. continues to be the largest aviation market in the world, with 876 million passengers in 2024. It also noted that narrow-body aircraft, including the Boeing 737 and Airbus A320 families, are among the most widely used globally.

Europe

Europe is expected to see significant growth in the aircraft engine and component leasing market in the coming years. During the forecast period, the Europe region is projected to have a CAGR of 6.2%. The European market reached USD 1.16 billion in 2025. In this region, both the U.K. and Germany are expected to reach USD 0.18 billion and USD 0.22 billion, respectively, in 2026. It operates busy short-haul services with a fleet of narrow-body aircraft, a well-developed maintenance, repair, and operations (MRO) system, and strong support for leasing, finance, and legal services. This mix keeps engine leasing and component pooling important. Airlines need dependable service without buying too many spare parts, especially as operating costs rise and fleets modernize for better fuel efficiency.

Asia Pacific

Asia Pacific is anticipated to be the fastest-growing segment in the global aircraft engine and component leasing market, growing at a CAGR of 8.4%. Busy domestic markets, the emergence of more low-cost carriers, and nonstop additions to fleets drive this growth. The region relies mostly on narrowbody aircraft, which leads to more cycles, shop visits, and pressure on MRO capacity. As a result, airlines are increasingly turning to leasing, especially for engines, as a safety net during tough market conditions. Based on these factors, countries such as China expect to reach a valuation of USD 0.62 billion, and India is set to reach USD 0.29 billion by 2026.

In December 2024, IATA’s market analysis showed that the Asia Pacific region accounted for over half of the global rise in passenger traffic that year, hitting 51.2%. The report noted that fewer new aircraft deliveries and engine problems put pressure on airlines. These issues typically lead to more reliance on leased spare parts and access to pools.

Rest of the World

The Rest of the World contributed 16.90% in 2025. The Middle East & Africa and Latin America have comparatively smaller shares but are growing at a CAGR of 6.9%. In the Middle East & Africa, long-haul networks focus on wide-body aircraft, and hub carriers prioritize availability. If an engine or rotable part is not ready, disruptions can occur quickly, which can be costly. In Latin America, airlines tend to be more cost-sensitive. Leasing helps they control operating costs while avoiding large upfront purchases of spare parts, all while ensuring stability in narrowbody-heavy networks.

In December 2024, IATA reported that the Middle East (10.7%), Latin America (8.6%), and Africa (2.7%) combined made up a significant part of the industry's growth in revenue passenger kilometers (RPK) for 2024. This shows why these markets continue to seek leasing capacity as traffic increases.

COMPETITIVE LANDSCAPE

Key Industry Players

Aircraft Engine and Component Leasing Players Compete on Spare Availability, MRO Access, and Documentation Integrity

The aircraft engine and component leasing market is competitive and focused on uptime. When a narrowbody aircraft experiences an AOG situation, airlines want more than just a promise. They need a spare engine or rotable that can be delivered quickly, installed correctly, and supported during the next shop cycle. This demand keeps the market centered around players who can consistently provide three key aspects: asset availability (engines and rotables that are actually available), maintenance, repair, and overhaul (MRO) access (to avoid delays), and paperwork integrity (to ensure parts can be installed). Airlines in North America and the rapidly growing Asia Pacific region require flexibility as market conditions change, operating costs fluctuate, and fleet modernization moves toward greater fuel efficiency.

At the forefront, large engine lessors such as AerCap Engines and Willis Lease compete by managing scalable spare portfolios. These portfolios can be redeployed across different aircraft types and regions. A second group includes integrated aftermarket platforms such as FTAI Aviation and GA Telesis. These companies promote availability as a service, combining leasing with teardown, module work, and exchanges to reduce downtime when MRO capacity is limited. On the component side, pool operators and PBH specialists, such as Lufthansa Technik and AJW Group, succeed by building extensive rotable inventories, ensuring fast logistics, and providing program support that turns unexpected failures into predictable turnaround times.

In summary, competition is shifting from merely renting assets to excelling in three key areas: fast availability, control over repair pathways through MRO access, and traceability and lifecycle response. In this context, data management, configuration control, and quick spare turnaround become crucial in securing the next contract.

LIST OF KEY AIRCRAFT ENGINE AND COMPONENT LEASING COMPANIES PROFILED

- AerCap Engines (Ireland)

- Avolon Aerospace Leasing (Ireland)

- SMBC Aviation Capital (Ireland)

- CDB Aviation (Ireland)

- Jackson Square Aviation (Ireland)

- BBAM (U.S.)

- Air Lease Corporation (U.S.)

- Willis Lease Finance Corporation (U.S.)

- FTAI Aviation (U.S.)

- GA Telesis (U.S.)

- Engine Lease Finance (U.K.)

- Castlelake (Ireland)

- Lufthansa Technik (Germany)

- AJW Group (U.K.)

- Air France-KLM Engineering & Maintenance (France)

- SR Technics (Switzerland)

- ST Engineering Aerospace (Singapore)

- HAECO (Hong Kong)

- SIA Engineering Company (Singapore)

- AAR Corp. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In August 2025, Air Europa renewed its Total Component Support (TCS) agreement with Lufthansa Technik for its entire Boeing 737 fleet. The deal now includes both current and future 737 MAX aircraft, which improves access to components and reliability for high-usage narrowbody operations.

- In April 2025, AJW Group secured a long-term Power-by-the-Hour (PBH) support program for Air Transat. This covers the A321ceo and a growing A320neo family fleet. The agreement combines component repair and pool support into a more predictable operating-cost model.

- In March 2025, AAR extended its exclusive agreement with FTAI Aviation until 2030 for used serviceable material (USM) for CFM56 engines. AAR will handle the teardown, repair, and marketing of parts from FTAI's CFM56 engine pool. This helps increase the supply for leasing and exchange programs.

- In February 2025, WestJet and Lufthansa Technik signed a 15-year exclusive agreement worth billions for LEAP-1B engine maintenance on WestJet's Boeing 737 fleet. Maintenance operations will begin in 2027. This shows a significant commitment to capacity for a key narrowbody engine type.

- In June 2024, Willis Lease Finance completed a purchase-and-leaseback deal with Pratt & Whitney for up to 15 PW1100G-JM GTF engines. This deal increases the availability of new-generation engines for leasing support.

- In May 2024, AerCap ordered 150 new CFM LEAP engines, valued at about USD 3 billion at list prices. Shannon Engine Support, a joint venture between Safran and AerCap, will manage these engines, effectively increasing spare-engine capacity for the A320neo family and 737 MAX fleets.

- In April 2024, FTAI Aviation signed a Perpetual Power Agreement with LATAM for CFM56 and V2500 engines. This agreement combines engine exchanges with a sale-and-lease transaction for over 30 aircraft. This approach aims to reduce downtime and limit shop visits where possible.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Lease Asset Type · Engine Leasing · Component Leasing |

|

By Leasing Type · Dry Lease · Wet Leasing · Operating Leases · Finance Leases · Sale and Leaseback |

|

|

By Engine Type · Turboprop · Turbofan · Others |

|

|

By Aircraft Type · Narrowbody · Widebody · Regional · Others |

|

|

By End User · Commercial Airlines · Military Aviation · General Aviation |

|

|

By Region North America (By Lease Asset Type, By Leasing Type, By Engine Type, By Aircraft Type, By End User, and By Country) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Lease Asset Type, By Leasing Type, By Engine Type, By Aircraft Type, By End User, and By Country) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Ireland (By Aircraft Type) o Rest of Europe (By Aircraft Type) · Asia Pacific (By Lease Asset Type, By Leasing Type, By Engine Type, By Aircraft Type, By End User, and By Country) o China (By Aircraft Type) o India (By Aircraft Type) o Japan (By Aircraft Type) o South Korea (By Aircraft Type) o Rest of Asia Pacific (By Aircraft Type) · Rest of the World (By Lease Asset Type, By Leasing Type, By Engine Type, By Aircraft Type, By End User, and By Country) o Latin America (By Aircraft Type) o Middle East & Africa (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.29 billion in 2026 and is projected to reach USD 8.80 billion by 2034.

In 2025, the market value stood at USD 1.48 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period of 2026-2034.

The narrowbody aircraft leads the market by aircraft type.

Unplanned engine removals and long shop queues drive leasing demand for spare capacity.

AerCap Engines, Avolon Aerospace Leasing, SMBC Aviation Capital, CDB Aviation, Jackson Square Aviation, BBAM, Air Lease Corporation, Willis Lease Finance Corporation, FTAI Aviation, GA Telesis, Engine Lease Finance, Castlelake, Lufthansa Technik, AJW Group, and others are the top companies in the market.

North America dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us